IMVT - Immunovant: Immune Boost From Clinical Trials To An Aggressive Bullish Stock

2023-09-27 05:30:40 ET

Summary

- Although Immunovant's stock has rallied around 100% since January, recent data on its therapeutic candidate, IMVT-1402, has further bolstered confidence, and we expect more upside from here.

- IMVT-1402's proposed subcutaneous route of administration allows for patient self-administration, potentially reducing healthcare costs and improving compliance.

- IMVT-1402 has shown deep IgG reductions and a potentially favorable safety profile, positioning it as a major challenger to competitors in the FcRn inhibitor class.

- We maintain our contrarian buy rating on Immunovant moving forward.

Maintaining our Buy Rating on Immunovant ( IMVT ) Based on Recent Data Readout:

Since we initiated Immunovant in January this year, the stock has rallied around ~100%, and our thesis has played out perfectly; the key part of our original thesis was that the asset and the platform's potential optionality have been neglected by the general market and overshadowed by argenx's phenomenal performance, and any sprinkle of positive news should drive up the stock meaningfully. With the recent data readout (Phase 1 healthy volunteer (HV) study), our confidence in Immunovant's therapeutic candidate, IMVT-1402, has been further bolstered. The readout details the impact of single ascending dose (SAD) and the 300 mg multiple ascending dose ((MAD)) cohorts, and based on this data, we believe IMVT-1402 has emerged as a potential game-changer within the domain of anti-FcRn inhibitors under clinical development and a major challenger to argenx's FcRn franchise moving forward. One may argue that the data is too early stage for us to build conviction, but we think differently considering that the FcRn class is highly de-risked as we have seen with argenx's Efgartigimod approval and UCB Roza's approval.

Following are BTVI's key takeaways from Immunovant's corporate presentation .

Subcutaneous Administration & Patient Independence

We believe IMVT-1402's proposed subcutaneous ((SC)) route of administration is noteworthy. This allows the potential for patients to self-administer the drug at home, positioning it differently from competitors like argenx’s SC and IV efgartigimod and UCB’s SC-infused rozanolixizumab , which necessitate administration by a healthcare provider. This self-administration is not only convenient for patients but could also lead to reduced healthcare costs and improve patient compliance; as such, it can be preferred by the payor moving forward and will be beneficial for market access once the drug launches (provided that the drug gets approved).

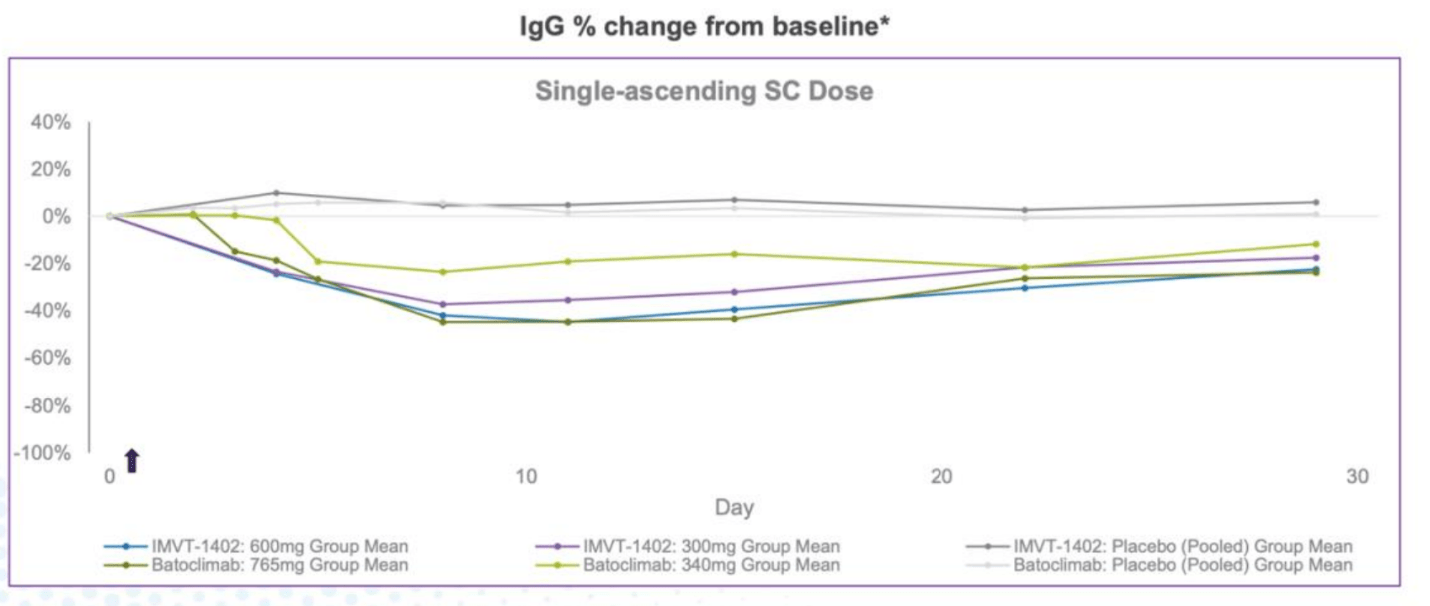

Deep IgG Reductions Indicating Potency

The data from the Phase 1 HV study has been particularly promising in terms of IMVT-1402’s impact on IgG levels. Historical precedents indicate that profound IgG reductions often translate to better efficacy amongst FcRn inhibitors as IgG is a validated cause of various autoimmune diseases (IgG attacking our own organs). We believe, the initial data presented for IMVT-1402 not only aligns with these precedents but also showcases its potential superiority in this regard.

Corporate presentation (IMVT)

{kind=link}

When compared with batoclimab's data, another FcRn inhibitor, IMVT-1402's data readout, was highly compelling. We believe the potency of a single 300 mg SC dose of IMVT-1402 seemed at least comparable, if not superior, to a 340 mg SC dose of batoclimab. Even more impressively, the 600 mg SC dose of IMVT-1402 mirrored the efficacy of a 765 mg dose of batoclimab, further underscoring its potency and potential advantage.

Safety Profile and Impact on Albumin and LDL

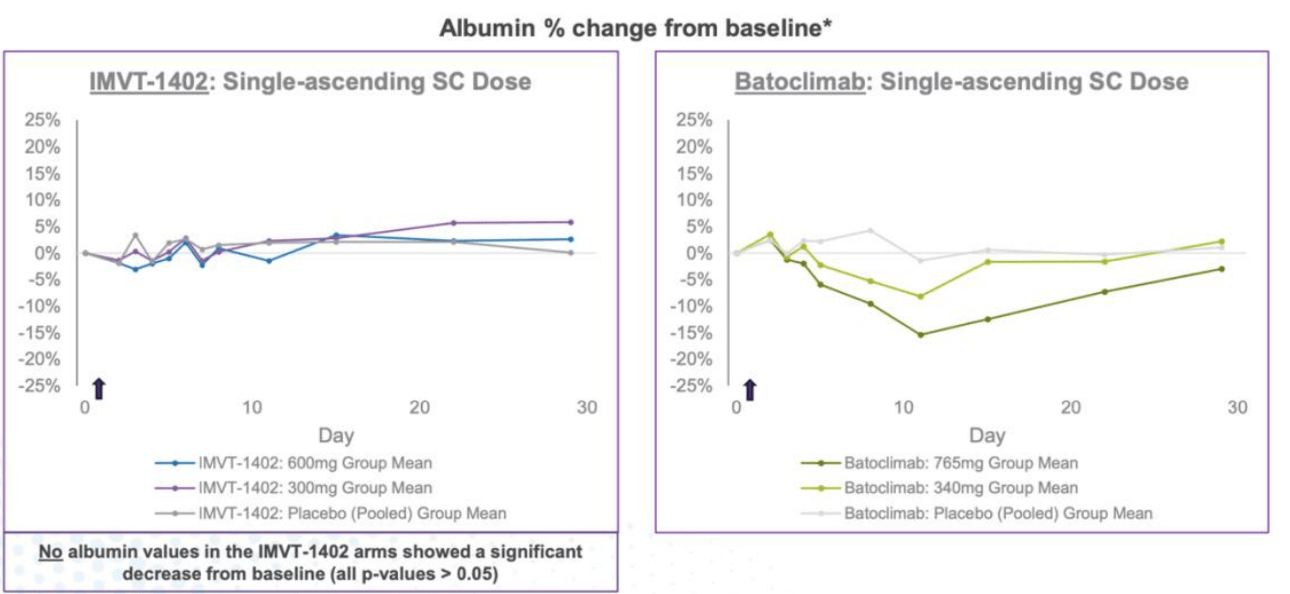

One of the standout features of IMVT-1402 is its potentially favorable safety profile. Pertinently, it appears to have no substantial impact on albumin and LDL, concerns that have plagued other contenders in this category (and one of the areas that argenx bulls have been pounding the table on). Albumin and LDL levels remained relatively stable across the board for participants in the SAD and 300 mg MAD cohort, making the drug potentially safer for long-term use.

{kind=link}

We find FcRn Inhibitor Class Highly Attractive with tremendous market expansion, similar to Anti-TNFs

The FcRn inhibitor class represents an area with massive market potential where major pharmaceutical players are jumping in to secure a leading edge. Two good examples would be companies like argenx, boasting a market cap of $20-30 billion, especially with the recent CIDP readout , and Momenta, acquired by JNJ for approximately $6.5 billion USD back in 2020 .

In our view, given IMVT-1402’s impressive data and the potential it brings to the table, there's a considerable opportunity for Immunovant to carve a significant niche in this market and potentially be an acquisition target or a key competitor to argenx moving forward. Furthermore, we believe the recent efficacy signal observed in a Phase 2a trial with Janssen/Johnson & Johnson’s FcRn inhibitor for rheumatoid arthritis ((RA)) further validates the broader potential of the FcRn inhibitor class across different indications, not limited to MG, CIDP, and ITP. We believe the class to come with various indications expansion opportunities similar to the anti-TNF class, where multiple blockbuster agents arose, making tremendous wealth for companies such as JNJ.

Another area that we further appreciate is the long patent protection of the candidate; a pending composition of matter patent may potentially extend intellectual property protection for IMVT-1402 up to ~2043, which is a highly attractive IP duration in our view for an early-stage candidate.

Risks

-

Clinical Trial Failures: Like all biopharmaceutical companies, Immunovant's success largely depends on the positive outcomes of its clinical trials. There's always a risk that the company's lead candidate, IMVT-1402, or any other pipeline candidates, may fail in future clinical studies. A failure can occur at any stage of testing, even if earlier trials showed promise.

-

Regulatory Approvals: Even if clinical trials are successful, there's no guarantee that IMVT-1402 or other future drug candidates will receive regulatory approval. The U.S. Food and Drug Administration (FDA) and other global health authorities have rigorous standards. If Immunovant doesn't secure approval for its lead drug candidate or if there are significant delays in the approval process, it could heavily impact the company's financial position and stock price.

-

Market Competition: The FcRn inhibitor class is a rapidly evolving field with several companies working on potential treatments. Competitors like argenx and UCB, as mentioned in the research, already have established products in the market or in advanced stages of development. If these companies or others bring more effective, safer, or cheaper treatments to the market before or after Immunovant, it could impact the company's market share and potential revenues.

-

Commercialization and Manufacturing Challenges: Assuming IMVT-1402 or other drug candidates receive approval, Immunovant would then face the challenges of commercializing the product. This involves building a sales force, marketing the product, establishing distribution channels, and ensuring manufacturing capabilities. Any hiccups in this process, whether in producing the drug at scale, setting pricing, or convincing physicians to prescribe the treatment, can impact the company's revenue and profitability.

Conclusion

Net-net, considering the presented data, IMVT-1402’s promising safety profile, its potency in terms of IgG reductions, its user-friendly SC administration, and the vast market potential of the FcRn inhibitor class, we are affirming our buy rating on Immunovant. The company is well-poised to establish a commanding presence in the industry, offering both a therapeutic breakthrough and a lucrative investment opportunity. Furthermore, with the recent raise of $ 300m , IMVT has a cash buffer of >$ 600m , and we expect this to be at least 2-3 years of cash runway (considering the company's ~US$200m annual cash burn), which is highly assuring for a pre-commercial cashflow negative biotech stock.

For further details see:

Immunovant: Immune Boost, From Clinical Trials To An Aggressive Bullish Stock