BMY - Immutep: Nipping At The Heels Of LAG3.Is It Impressive Enough?

2023-09-01 18:57:51 ET

Summary

- Immutep Limited is a small cap biotech focusing on the development of eftilagimod alpha, a novel molecule that activates MHC class II molecules to enhance the immune response.

- The company is conducting late-stage trials in head and neck cancer, non-small cell lung cancer, and metastatic breast cancer.

- Immutep has sufficient cash to support its clinical efforts and is a tentative buy, but there is a risk that the add-on therapy may not show significant benefits in randomized trials.

Topline Summary

Immutep Limited ( IMMP ) is a small cap biotech betting its house on a novel molecule with a recently established target. They have late-stage trials, tightening costs, and a recent capital raise that could carry them through some critical catalysts. They're worth a second look for you, and this article is going to explain my rationale behind that.

Pipeline Overview

IMMP is currently in full-throttle development of one agent: eftilagimod alpha. This is a soluble version of the immune checkpoint inhibitor LAG-3, designed to bind MHC class II molecules and activate them, essentially intending to remove the brakes put on by the tumor's expression of LAG-3 that would deactivate T cells nearby.

Now, if you're paying attention to the field, you already know that we have an approved LAG3 inhibitor, which is Bristol Myers Squibb's ( BMY ) relatlimab (in a co-formulation with nivolumab). And there is a burgeoning pipeline of other LAG-3 antibodies. All of these are designed as blockers of LAG-3 signaling. IMMP's approach is to use soluble LAG-3 as an activator of MHC class II, which leads to broader-spectrum activation of antigen-presenting cells and, hopefully, an enhanced immune response.

In essence, they have a different way of exploiting LAG-3, so there's a chance to have a differential effect.

IMMP is developing eftilagimod in a variety of indications, including head and neck cancer, breast cancer, lung cancer, bladder cancer, and sarcoma. I want to focus this article on the most developed aspects of this pipeline of trials, since these have the biggest chances to be real catalysts for the company.

First-line head and neck cancer - The TACTI-003 study

TACTI-003 builds on previous encouraging findings in head and neck cancer for eftilagimod combined with pembrolizumab, with a 31% response rate in the second-line setting. In the final results presented at ASCO 2023, the combination yielded a median overall survival of 15.5 months in patients with relatively high PD-L1 expression (20% by CPS or higher). In PD-L1-positive patients, the response rate was 38.5%.

At a glance, these findings compare favorably with historical second-line therapy using PD-1 antibodies alone ( nivolumab monotherapy in PD-L1 CPS >1 had a median overall survival of 8.7 months, while pembrolizumab had median overall survival of 10.8 months in PD-L1 CPS 1-19). First and foremost, these are completely different trials with different populations, so this is not a fair comparison. Moreover, the PD-L1 cutoffs being assayed here are not the same, so take these numbers with a huge grain of salt and for nothing more than historical context.

Regardless, based on these findings, IMMP has initiated a multicenter, open-label, randomized phase 2b trial to evaluate eftilagimod plus pembrolizumab as frontline therapy for recurrent or metastatic head and neck squamous cell carcinoma. IMMP guides that we can expect top-line results from TACTI-003 in the second half of calendar year 2023, and I would expect the earliest full data readout to come maybe around ASCO 2024.

Non-small cell lung cancer - The TACTI-002 study

In a similar vein, IMMP is also exploring the benefit of eftilagimod-based therapy in non-small cell lung cancer. The NSCLC cohort B of TACTI-002 was presented in final form at ELCC 2023 , enrolling 36 patients with PD-1-refractory NSCLC to undergo treatment with eftilagimod plus pembrolizumab.

The overall response rate in this refractory population was 8.3%, with median overall survival of 9.9 months. When looking at high PD-L1 expressors (50% or higher by CPS), the response rate seemed to be improved (33%), as well as median overall survival, which was not reached by the data cutoff of December 31, 2022.

An important caveat is that only 2 patients in the study had this high PD-L1 expression. In addition, patients who had previously achieved a response to anti-PD-1 therapy and then relapsed appeared to have more favorable outcomes than did those who had "primary" resistance (ie, those that never responded to PD-1 therapy).

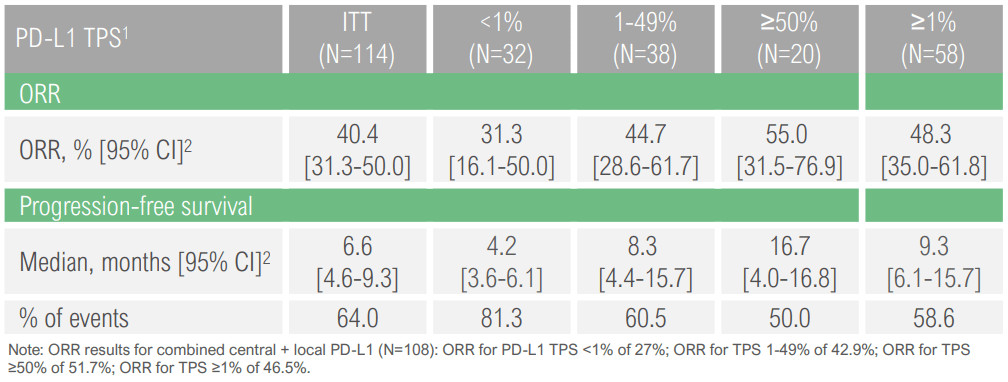

TACTI-002 also included a cohort of 114 patients with previously untreated, advanced NSCLC. In a data presentation at SITC 2022 , the efti-pembro combination yielded a response rate of 40.4% among the patients with intention to treat. Moreover, this appeared to be associated with increasing PD-L1 scores, although it should be noted that these tested TPS, and not CPS, which means that it included PD-L1 staining only on the tumor cells.

TACTI-002 first-line NSCLC efficacy findings (IMMP SITC 2022 Poster Presentation)

{kind=link}

Again, we have to be very wary of cross-trial comparisons, but these findings do compare favorably with studies like KEYNOTE-024 , which demonstrated benefit for pembrolizumab over chemotherapy in patients with high PD-L1 expression. There, the median progression-free survival in patients with PD-L1 TPS of 50 or higher was 10.3 months, with a 44.8% response rate.

Updated overall survival findings from TACTI-002 are going to be presented at this year's ESMO meeting in late October . So we'll have a chance to see more discussion on this combination.

IMMP has guided that they've received positive feedback from the FDA to support initiating a registrational trial in the first-line NSCLC setting, enrolling patients with a PD-L1 TPS of 1 or higher. The company has Fast Track designation for eftilagimod plus pembrolizumab in this setting, so it will be interesting to see when this study begins.

Metastatic HER2-negative or -low breast cancer - The AIPAC study

IMMP is conducting a phase 2b trial evaluating eftilagimod plus the chemotherapeutic agent paclitaxel in patients with metastatic, hormone-receptor positive breast cancer. In the primary analysis at SABCS 2020 , no progression-free survival benefit was observed, but there were higher response rates and overall survival with eftilagimod. Whether these findings were clinically meaningful is up for debate, since the increases were relatively small.

Still, the company has initiated a wider-ranging trial, AIPAC-003, a placebo controlled, randomized trial of paclitaxel plus eftilagimod or placebo in patients with hormone positive disease (first-line or later), triple-negative breast cancer, and hormone-negative, HER2-low breast cancer. The primary objective of the study is improvement in overall survival.

Financial Overview

In their most recent update on financial activities, IMMP disclosed that they held $123.4 million in cash and equivalents after completing an $80 million equity raise back in June. Their operational expenses included $5.41 million in R&D and $1.61 million in general/admin expenses. The company was able to drop negative cash flow from $14.17 million in the last quarter to $8.35 million in the most recent quarter.

If they keep pace with those losses, IMMP has somewhere between and around 10 and 15 quarters of cash left. The company estimates that this cash will carry them into summer of 2026.

Strengths and Risks

IMMP has a broad suite of trials tackling significant areas of unmet need, and I did not even go into detail on their earlier-stage efforts to target the likes of sarcoma and bladder cancer. There's enough to chew in the thoracic space alone.

Breaking it down, the head and neck data look most promising to me, with that 15.5 month overall survival comparing favorably to the standards that patients would see in practice today. The breast data I am not convinced by at this time, since a trend toward response and OS benefit is not really moving the needle. Hopefully the AIPAC-003 study will have sufficient power to show something real, but at this time I'm not seeing it.

The lung cancer data are encouraging, but cautiously so. There appears to be some kind of benefit in patients with high PD-L1 expression, but it's not a night-and-day difference, so shareholders should eagerly await bona fide, randomized trial data.

One concern I have is that the efficacy of this combination really seems to be depending on PD-L1 expression in these small studies. This does not lend a lot of support for the idea that eftilagimod is really driving much more efficacy than pembrolizumab would have alone. I know the premise of the molecule is to act as a sort of immune booster, but how do we know that those patients with high PD-L1 expression wouldn't have done just as well without the add-on therapy that would come with extra cost and toxicity?

Without a head-to-head study to really lean on, this presents a significant risk for investors. Regulatory authorities and practicing physicians are not going to want to throw extra drugs onto the standard of care willy-nilly for an unconvincing benefit, or at least that would be my fear moving forward here. Add on top of that the fact that IMMP is basically a one-drug company, with only the faintest glimmer of other work being done outside of eftilagimod.

Financially, IMMP is in a solid place to move their projects forward. I believe there is enough cash runway to get a really solid look at eftilagimod in randomized trials without further financing needed. So that is an essential de-risking event.

Bottom-Line Summary

IMMP is a tentative buy at these levels. They're entering a stage where the fog should start to part on their clinical efforts, and they've established enough signals of efficacy that I feel we could see something positive emerge. Take caution, though, because I would also not be surprised at all if these randomized studies, with their adequate power, show no real difference with add-on eftilagimod. If that happens, there is basically no reason to be holding this company at that time. I would consider a small position here, but watching carefully for opportunities to take profit and have a loss-free holding, because this is still a rather risky project.

Thank you for reading. I hope you find this perspective on an oncology company helpful in your research. If there are any cancer therapy ideas you'd like covered, please let me know in the comments or a private message. I'm also happy to answer any questions you have. Have a great day!

For further details see:

Immutep: Nipping At The Heels Of LAG3.Is It Impressive Enough?