IMPUF - Impala Platinum: A Mixed Picture

2023-06-12 09:14:50 ET

Summary

- Platinum market offers attractive investment opportunities due to strong fundamentals and projected growth in the hydrogen industry.

- Impala Platinum stands out among platinum group miners, but faces challenges in maintaining production due to rising costs and South Africa's energy crisis.

- Despite challenges, Implats remains profitable with a strong balance sheet and solid capital returns policy, but short-term prospects may face headwinds.

Platinum Market

Platinum offers an attractive investment proposition at the moment. The prevailing belief is that platinum demand is declining due to the shift from internal combustion engines (ICEs), which utilize platinum in catalytic converters, to electric vehicles (EVs) that do not require it. Platinum is particularly used in diesel engines, which have seen reduced adoption since 2015, especially in developed countries. However, platinum boasts strong fundamentals. While automotive demand may dwindle, the projected growth in the emerging hydrogen industry is expected to more than compensate for it. Additionally, platinum benefits from widespread industrial use, particularly in glass fabrication. ICE vehicles will continue to expand, especially in developing countries like India and China.

Another reason to be optimistic about platinum is the likelihood of production disappointments in the coming years. The majority of platinum production is concentrated in Russia and South Africa. Russian producers like Norilsk Nickel ( NILSY ) may encounter difficulties in maintaining current production levels due to challenges in procuring mining equipment and other materials as a result of sanctions. South African producers are currently grappling with a devastating energy crisis, as power shortages force companies to spend millions of dollars on fuel for generators to sustain operations during load curtailments. As a consequence, new projects are being delayed, and production costs are rising.

The platinum market is already experiencing a deficit and is projected to post its largest deficit on record in 2023. In general, stable or growing demand coupled with a challenged supply landscape make for a compelling bullish thesis in the commodity sector. Typically, this would prompt further investigation into the financial results of producer companies to identify the most attractive listed options. Mining company shares offer inexpensive exposure to the underlying commodity and often provide a yield compared to futures or options-based strategies.

However, there are challenges with this approach when it comes to platinum. Firstly, there are no companies exclusively focused on platinum mining since it is often found alongside other metals due to its natural occurrence in certain geological formations. Platinum group metals (PGMs) include platinum, palladium, rhodium, ruthenium, iridium, and osmium. These metals share similar chemical properties and tend to form complexes and alloys with one another. While platinum plays an important role in the green economy, palladium and rhodium do so to a lesser extent. Moreover, the palladium and rhodium markets are projected to experience oversupply.

The second reason is more fundamental. My bullish thesis on platinum relies partly on the assumption that production from South Africa will disappoint. With Norilsk Nickel being unsuitable for investment and most other miners having significant exposure to South Africa, there seems to be no good way to gain exposure to platinum without supply risks, except by investing directly in the metal itself.

Impala Platinum

Impala Platinum ( IMPUY ) stands out among platinum group miners as one of the best options. Approximately one quarter of its revenues come from platinum, with the rest derived from other platinum group metals. It maintains strong margins and has a robust shareholder returns policy in place. Although the company's value has more than halved since its peak, it currently offers an almost 10% yield and is undervalued. However, at the moment, I still don't see the current price as a buying opportunity. Impala is facing challenges in maintaining production, as its input costs rise due to inflation. The energy crisis is compelling it to postpone projects and make costly investments to mitigate the impact of rolling blackouts. Some of its South African assets are aging, expensive to maintain, and situated at deep levels.

Overall, I consider Implats a well-managed company that unfortunately has to confront challenges beyond its direct control. Compared to competitors, it offers some geographical diversification outside of South Africa, thanks to its assets in Zimbabwe and Canada. It is also investing in new growth projects to replace declining and high-cost assets. In particular, it has recently managed to complete its acquisition of Royal Bafokeng Platinum, putting an end to a lengthy takeover battle with rival Northam Platinum. This acquisition secures a growth future for Implats in the promising Rustenburg mining complex.

Currently, I am keeping Implats on my shortlist and I am open to re-evaluating it if the situation in South Africa shows clear signs of improvement. In the short-term, I anticipate headwinds to dominate, including pressure on platinum group metals in the event of a recession in the second half of 2023, as well as margin erosion due to inflation and electricity shortages. Therefore, at the moment, I view Implats as more suitable for a short position, along with a basket of other platinum miners, as part of a pair trade (long platinum, short platinum miners).

The good

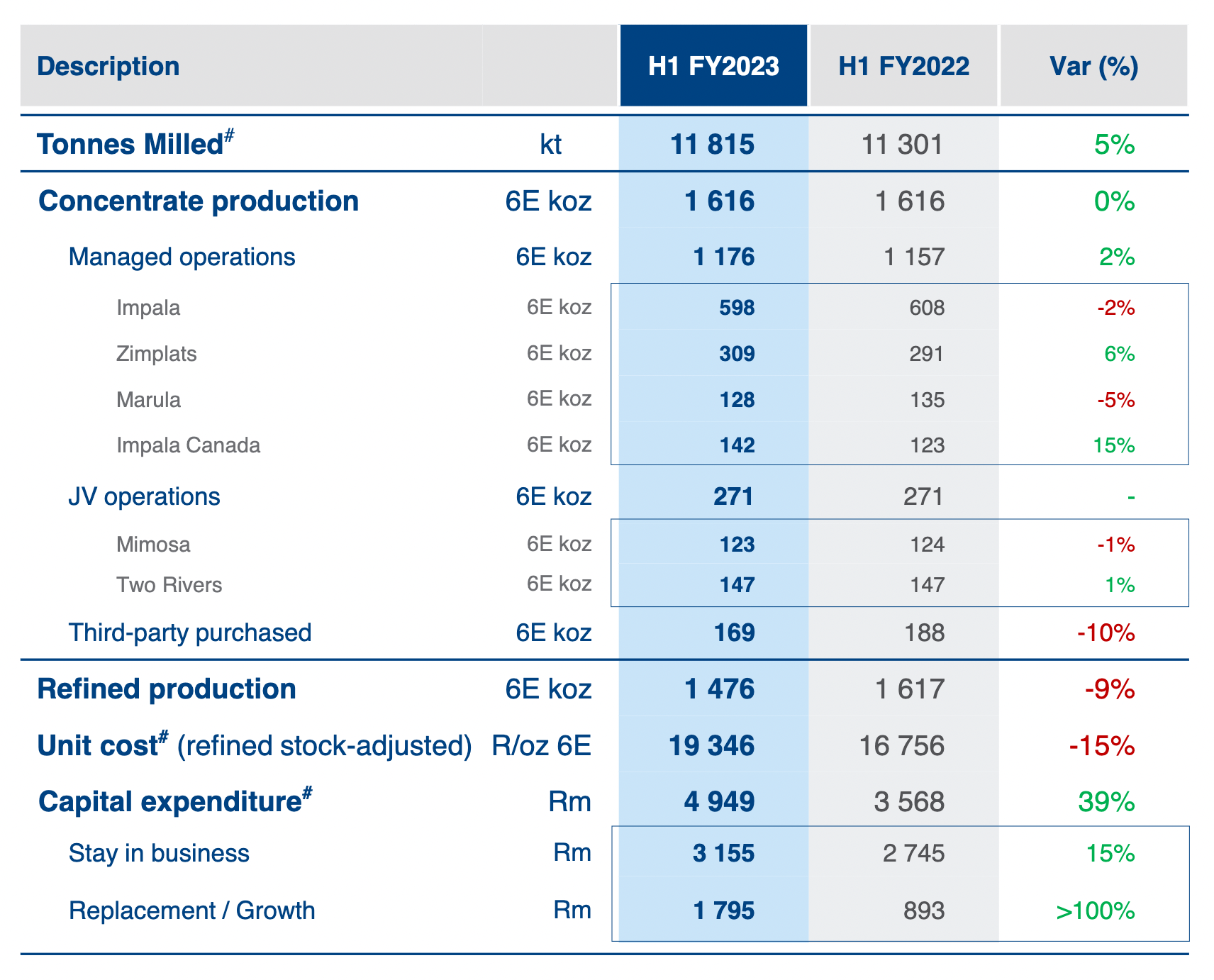

Despite the challenging operating environment, Implats has managed to maintain its current production levels. In the first half of fiscal year 2023, tonnes milled actually increased by 5% to 11,815 tonnes compared to the same period last year. Concentrate production remained relatively stable at 1,616 6E thousand ounces, while refined production decreased by 9% to 1,476 6E thousand ounces.

Operational overview for H1 FY 2023 (Company's presentation)

{kind=link}

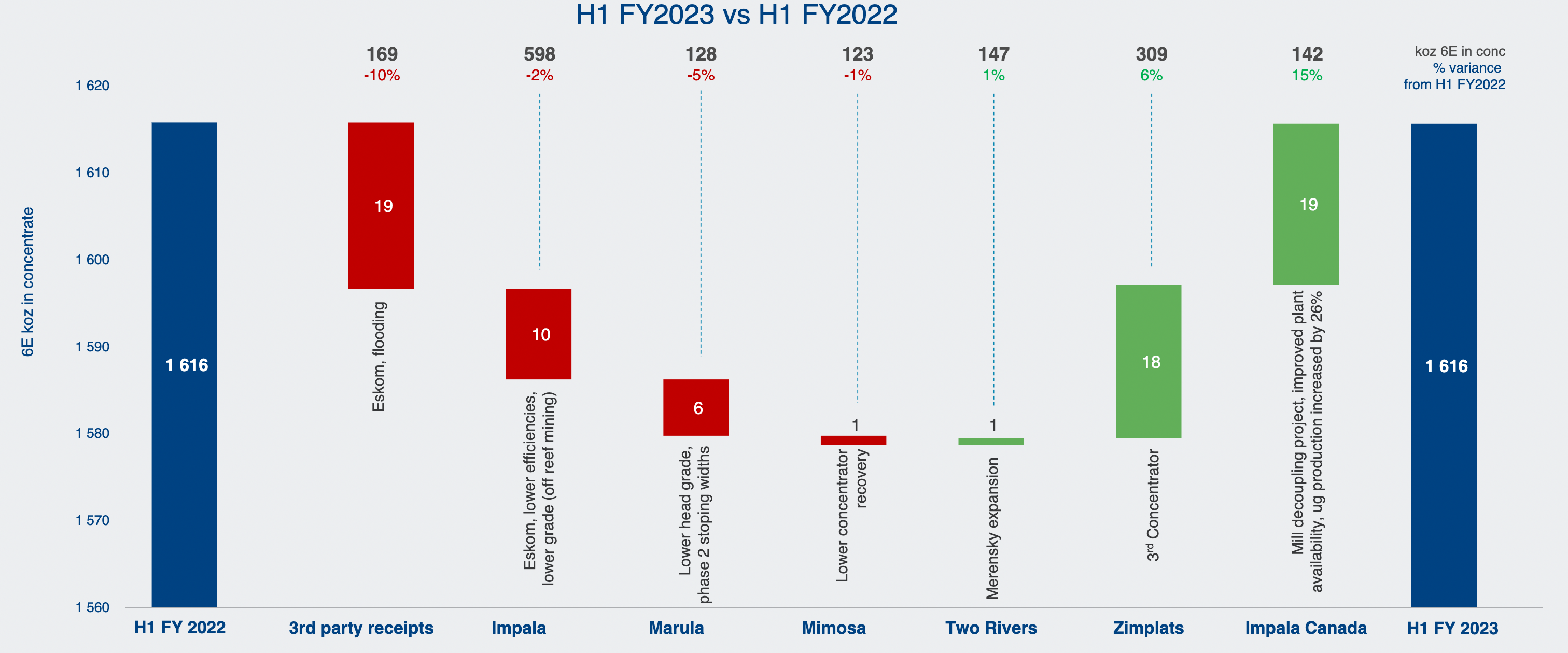

When examining the performance of individual assets, a clear trend emerges: the South African assets are facing operational challenges due to the Eskom situation, community unrest, and lower grades, whereas the Canadian and Zimbabwean assets are performing well. Impala Canada saw a 15% increase in performance, benefiting from higher grades and improved plant stability following the commissioning of the mill decoupling project. Zimplats also experienced a 6% increase in performance, thanks to the commissioning of its third concentrator. On the other hand, Marula and Impala Rustenburg underperformed, experiencing a 5% and 2% decline, respectively, due to load curtailment and infrastructure breakdowns.

Change in concentrate production H1 FY2023 vs H1 FY2022 (Company's presentation)

{kind=link}

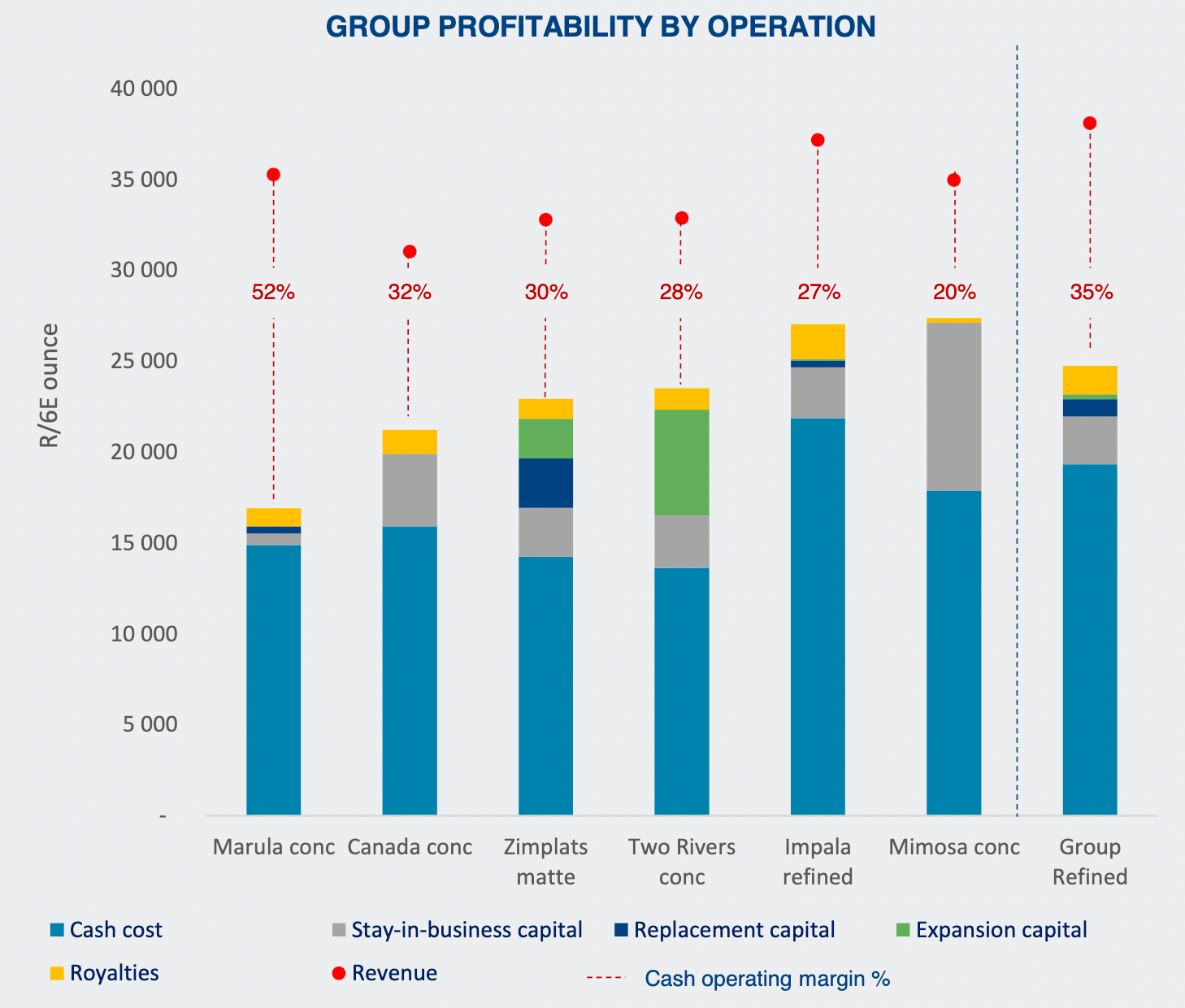

Despite falling PGM metal prices and rising costs, profitability remains strong, with most assets maintaining strong margins around 30%.

{kind=link}

Implats generated R11 billion in free cash flow for H1 2023. The company boasts a strong balance sheet and a net cash position of R27 billion. Its current market capitalization of R135 billion implies a relatively low multiple of approximately 5x EV/FCF. Implats also returns 30% of free cash flow to shareholders, resulting in a trailing dividend yield of around 10%.

The company is strategically investing in various expansion and growth projects to replace ounces from its aging assets. A positive development occurred in May when Implats successfully closed its acquisition of Royal Bafokeng Platinum. This acquisition involved purchasing a 9.26% stake from Africa's largest fund manager, Public Investment Corp. The acquisition is significant as RBPlat has mechanized and shallower mines adjacent to Implats' Impala mine. RBPlat has a substantial resource base of 2.3 million 6E ounces and an estimated mine life of over 20 years. Moreover, it has a higher platinum bias, which is advantageous given the more bullish outlook for platinum compared to other platinum group metals.

The acquisition is highly strategic. RBPlat has mechanised and shallower mines adjacent to the company's Impala mine. It has a large resource base of 2.3 million 6E ounces and an estimated life of mine of over 20 years. It also has a heavier platinum bias, which is an advantage in my opinion given the more bullish outlook for platinum compared with other platinum group metals.

The bad

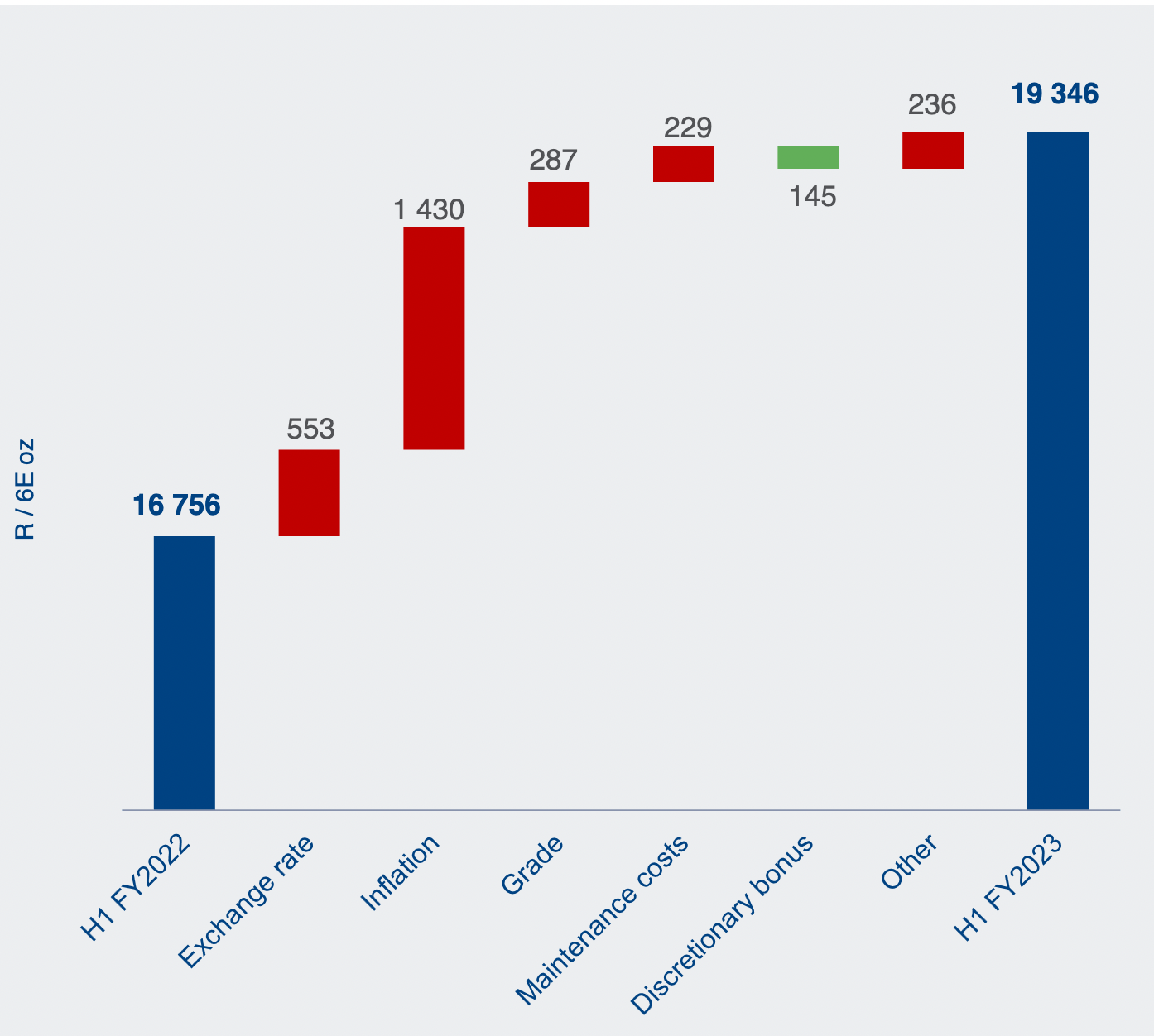

In H1 2023, costs increased by 15% to R19,346 per ounce. A portion of this increase can be attributed to accounting practices, as Implats reports costs in South African rand. The weaker rand leads to higher reported costs from its foreign operations. Other contributing factors include higher labor costs, lower grades, and inflation, with inflation alone responsible for an 8.5% rise in costs.

{kind=link}

Inflation also affects capital expenditures, which reached nearly R5 billion in H1 2023, a 40% increase compared to the previous year. Expenditures associated with maintaining production, excluding replacement and growth projects, rose by 15%. Going forward, capital expenditures will remain elevated as Implats aims to replenish its reserves and resource base. The company expects capex of R11.5 to R12.5 billion in 2023, representing a 38% increase compared to 2022.

The ongoing energy crisis in South Africa, specifically load curtailment by Eskom, poses a significant negative impact on Implats. To mitigate the situation, the company has implemented costly operational interventions, such as reducing power to smelters and adjusting milling, hoisting, and re-mining rates. While the impact on production volumes may be relatively benign, estimated at 16 thousand 6E ounces of lost production over the last quarter, it significantly affects production costs and leads to delays in developing new projects.

As a result, Implats is revising downward its production and cost guidance. From Q3 production report :

The increased severity of domestic and regional power constraints has been well documented and was a notable impediment to operational delivery in the quarter. [...] Given the constrained operating environment, FY2023 production is likely to be towards the lower end of the previously guided range, while unit costs are trending toward the top end of the provided guidance.

Conclusions

While I see value in the current valuation, a combination of headwinds make me hesitant to take a long position in Implats. Electricity shortages in South Africa still show no sign of abating. Their effects will flow through financial results over the next 6-12 months. Costs are rising due to inflation and production remains challenged. On the other hand, Implats is quite profitable, has a robust balance sheet, a solid capital returns policy, and a good capital allocation strategy.

In the short term, the potential for a rerating of Implats seems dependent on a significant increase in metal prices. However, such a scenario is most likely to occur in the event of a further deterioration in the South African situation. While I have a positive long-term outlook on platinum, considering its growing role in the green economy and projected deficits, the short-term prospects for all platinum group metals may face challenges due to a potential recession impacting industrial and automotive demand. For the time being, I prefer to remain on the sidelines.

For further details see:

Impala Platinum: A Mixed Picture