IMPUF - Impala Platinum: A Turnaround Is On The Horizon

Summary

- Key variables suggest that Impala Platinum is set for a turnaround.

- Most PGM prices are below their moving averages, with supply shortages and higher demand en route.

- Impala struggled with load curtailment and industrial action issues during 2022. However, the latter is resolved, while higher PGM prices will likely phase out the prior's influence.

- Although a higher country risk premium must be considered, Impala Platinum's stock is priced at a cyclical discount.

- Lastly, the stock provides a lucrative dividend opportunity with the firm's 30% of operating cash flow distribution policy.

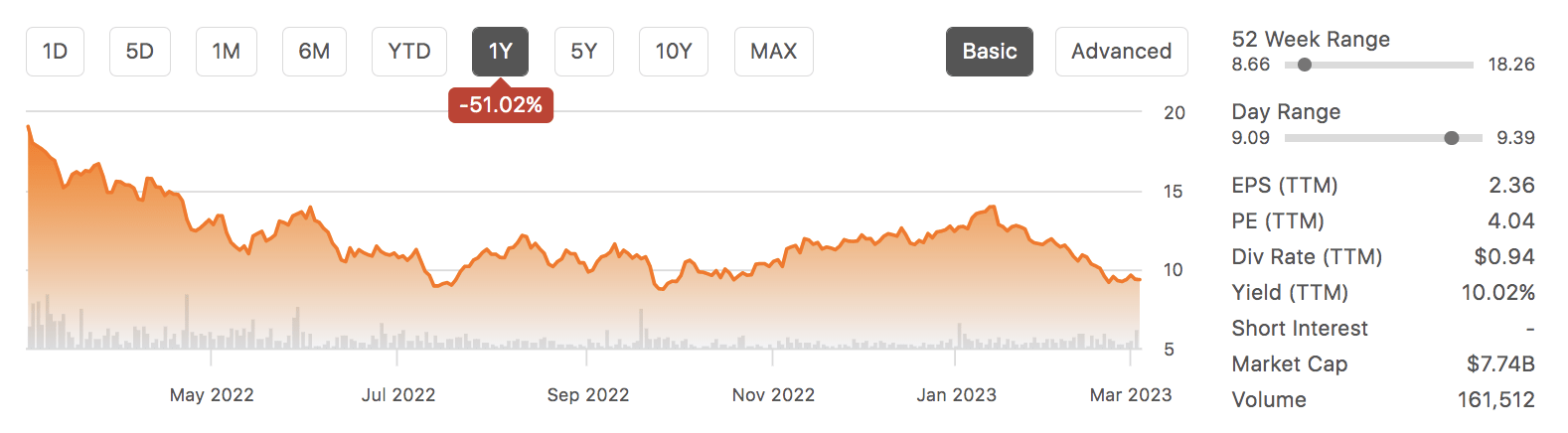

Impala Platinum Holdings Limited's (IMPUY) more than 50% year-over-year drawdown should not be neglected, as the firm's embedded risks somewhat justify the trajectory. However, the market has likely overreacted, consequently presenting risk-seeking investors with a lucrative value gap.

{kind=link}

After assessing the stock's key variables, we discovered evidence of a potential turnaround stemming from structural and systemic changes. Thus, we retain our bullish outlook on the stock; here is why.

A PGM Price Recovery Is In The Cards

Platinum Group Metal ((PGM)) prices have taken a beating during the past year, which was to be expected for a few discreet reasons. First of all, the broad-based macroeconomic slowdown implied lower industrial production.

Furthermore, the easing of global supply chains allowed for higher supply, consequently shifting the supply/demand landscape back toward equilibrium. And lastly, although PGM prices are usually exponentially distributed, they still possess moving averages, meaning that a downward reversion was inevitable.

A closer look at Platinum's price action indicates that the metal is trading below its moving averages, which leaves a technical arbitrage opportunity, especially considering an enhanced macroeconomic outlook in the United States, the EU, and China. Furthermore, it is anticipated that Platinum will move into a supply deficit during 2023 amid factors such as slow output from South Africa and adverse weather across the globe.

In essence, we anticipate better Platinum prices for the rest of the year, which could act as a tailwind to Impala Platinum. Impala's platinum metals sold for 9.3% lower in 2022 than they did in 2021. At the very least, we anticipate these prices to stabilize due to the aforementioned reasons.

Palladium Moving Average (Kitco)

{kind=link}

Similar to Platinum, Palladium is trading well below its moving averages. The commodity is more volatile than Platinum as it is more easily fused. However, slow production from South Africa, higher-than-anticipated global economic growth, and a pivot in global interest rate policies might cause the commodity to recoup much of its 20% year-over-year drawdown.

Implats suffered from compressed Palladium price recognition in 2022 as its average sales price slipped 8.7% year-over-year. As claimed with Platinum, we could see higher prices if the current implied influencing variables were to hold.

Platinum 10Y Moving Average (Kitco)

{kind=link}

Production Update

Let's start by discussing a few challenges.

As anticipated, Eskom's woes resulted in load curtailment for Impala Platinum, leading to lower refined production and sales volumes. However, the company still achieved substantial sales across the board, especially considering that 2022 hosted softer demand-side attributes.

Furthermore, a depreciating South African Rand resulted in less cross-border purchasing power. The softer Rand also meant that Impala's CapEx expenditures at Impala Canada climbed. Additionally, the firm's expansion of ZimPlats (in Zimbabwe) was affected by hyperinflation in Zimbabwe.

{kind=link}

Despite Impala Platinum's recent woes, good news exists.

Although production at the company's Marula asset suffered from lower throughput, its operations in Rustenburg, Zimplats, and Impala Canada all produced high grades.

Carrying on with operational coverage, the Two Rivers mine suffered from lower throughput during Implats' fourth quarter as lower grades were realized from its stockpiles. However, Two Rivers might act as a catalyst in the coming quarters as Impala recently increased its milling capacity.

Keep in mind that the Two Rivers mine is a high-margin asset. Shared with African Rainbow Minerals (AFBOF), Two Rivers is regarded highly as a springboard to Impala Platinum.

{kind=link}

Returning to Impala Rustenburg. Readers need to consider that much of the mine's lower-than-anticipated production during the past year was due to regional industrial action amid multiyear high inflation in South Africa.

In our opinion, an inflection point in South African inflation and Impala's recent wage settlements will result in smoother operations at the mine. Sure, sustained load curtailment is likely; however, much of this will be phased out by fading wage demands and higher PGM prices.

{kind=link}

A final mention of Impala's operations is its ongoing pursuit of Royal Bafokeng Platinum (RBPlat).

Impala currently owns a little over 40% of RBPlat and intends to acquire an additional stake in the company to garner majority control, allowing it to leverage the RBPlat as a strategic asset and take advantage of synergies.

However, the other large shareholders in RBPlat, namely Northam and South Africa's Public Investment Company, seem reluctant to sell as the prior believes a sale would enhance Impala Platinum's competitive position beyond an acceptable level, while the latter wants to keep ahold of a profitable financial asset.

What does this mean to Impala Platinum's shareholders?

An end to Impala Platinum's pursuit of RBplat might benefit the firm's shareholders as the dragged-on process has enhanced the risk of overpaying for the acquisition. In addition, the process has resulted in "tied-up" capital, which investors might see as unfavorable.

Total Return Prospects

South Africa's exponentially growing country risk means Impala Platinum's justified price multiples are probably much lower than those of foreign mining companies. Nevertheless, Impala Platinum's price-to-book ratio is at a 91.10% discount relative to its cyclical average, lending substance to the argument that this is a tremendously undervalued stock.

{kind=link}

I will not succumb to bias and state that Impala's net lower half-year dividend is good. However, the stock's recent drawdown, coupled with its 30% payout of operating cash flow, means investors can secure lucrative future yields.

Impala Platinum's dividend will always be cyclical, as that is just the company's nature. Nevertheless, a 12.44% forward yield during an unfavorable cyclical trough is not bad at all.

{kind=link}

Noteworthy Risks

Risks were outlined throughout the article. However, I would like to reiterate two significant faultlines.

The primary risk to Impala is the continued load curtailment, which is especially relevant to its refineries. Impala Refining Services suffered a 13% drop in quarterly refined production in 2022. It is unlikely that a substantial reversal will be realized as refineries are exceptionally difficult to ramp up when grid issues arise.

Furthermore, the global economy is in better shape than implied a few months ago. However, several central macro variables remain uncertain, and input costs are adrift from their moving averages. As such, our bullish consensus on PGM prices might not materialize if highly possible adverse macroeconomic events occur during 2023.

Final Word

Impala Platinum has been up against it during the past year as both supply and demand side headwinds surfaced. However, a turning point seems near amid a potential turnaround for PGM prices.

The company is faced with load curtailment issues. Nevertheless, industrial action has found calm, and higher implied PGM prices will likely phase out load curtailment risks.

Furthermore, the RBPlat acquisition looks like a coin toss. A deal looks unlikely. Yet, a failed agreement will result in freed-up capital and prevent an unnecessary acquisition premium.

Impala Platinum's stock is trading at a discount relative to its cyclical price multiples after shedding more than 50% of its market value in the past twelve months. Additionally, the stock presents a substantial dividend. Therefore, we retain our bullish outlook on the asset.

For further details see:

Impala Platinum: A Turnaround Is On The Horizon