JAPAF - Imperial Brands: Expected Profit Growth Bodes Well For Dividends

2023-11-07 17:16:27 ET

Summary

- Imperial Brands has had a sluggish year in the stock market so far, but this has only served to make it more attractive in terms of market multiples.

- Its reported revenues and earnings are likely to see an uptick in its full year FY23 results due next week. This bodes well for both its stock price and dividends.

- Over the longer term much depends on how far it's able to grow its smoking alternatives' business. But for the medium term, it looks like a good buy anyway.

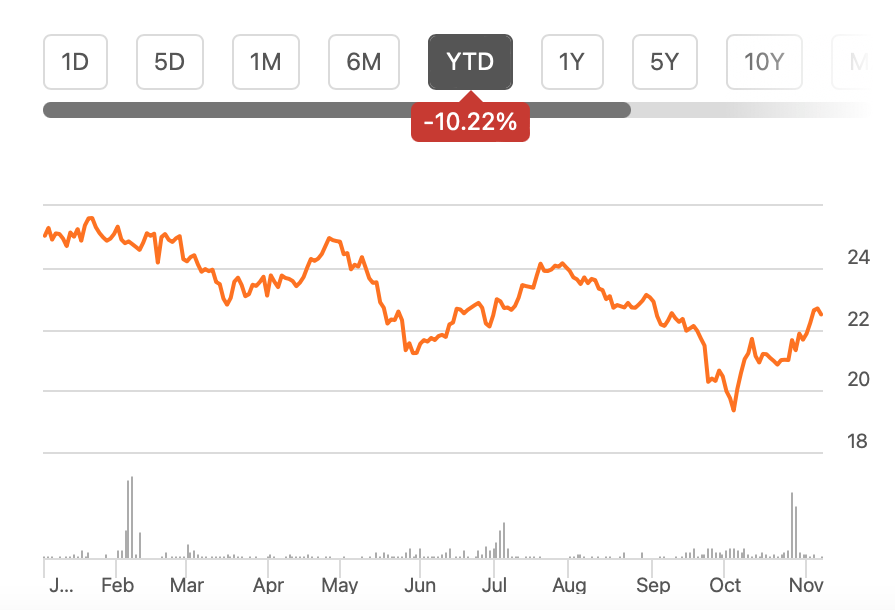

It hasn't been a good year for tobacco stocks. Four of the five biggest stocks in the category by market capitalisation trading on US markets have seen a price decline year-to-date [YTD]. The fifth biggest of these and the manufacturer of Davidoff cigars, Imperial Brands PLC ( OTCQX:IMBBY ), is no exception (see chart below).

Its solid dividend yield of 7.7% has softened the price blow to some extent, but the total returns are still down by 5.75%. With its full year FY23 (year ending September 30, 2023) results due next week, here I analyse if the tide can turn for the stock and its ADRs going forward.

{kind=link}

The revenue outlook

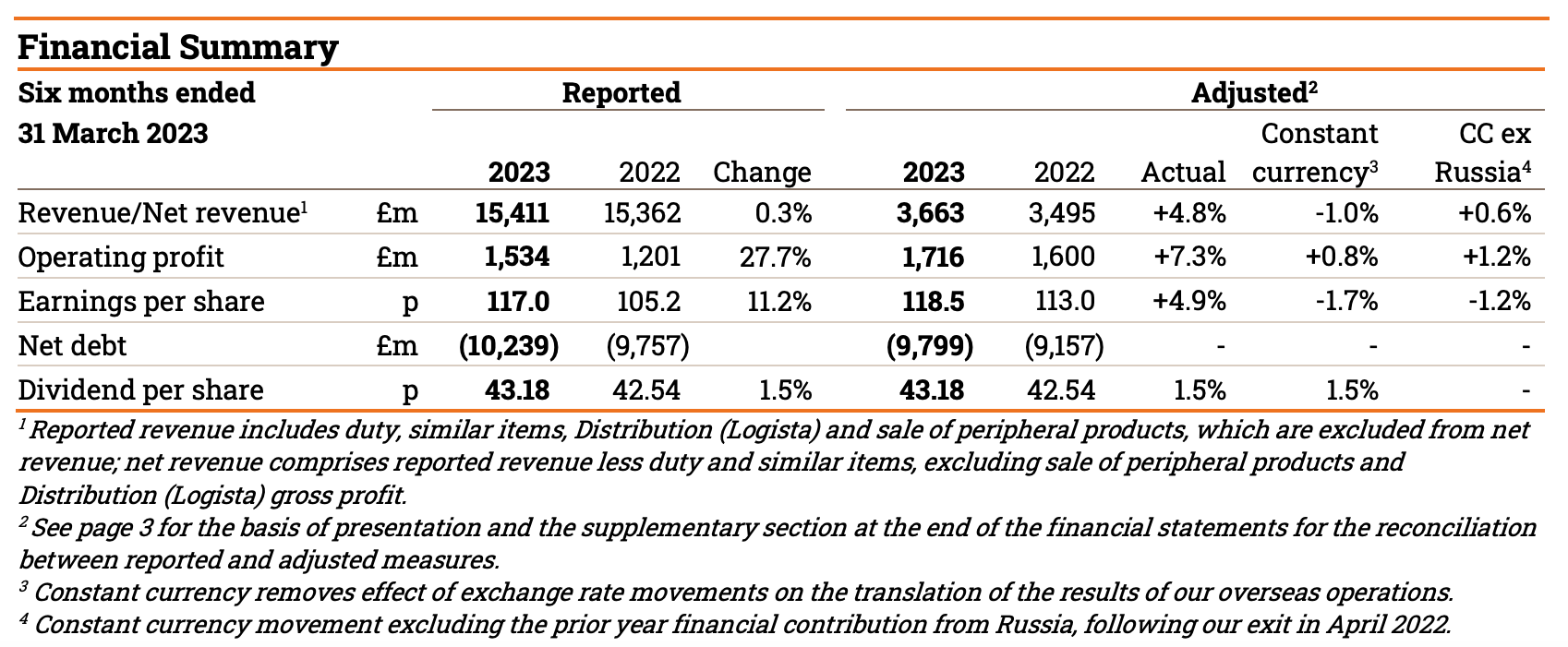

The company expects net revenue on a constant currency [CC] basis "in the low single digits" for FY23 as per its latest trading update . It also mentions that this forecast is inclusive of the company's Russia business in the base year, a point worth noting considering that in the first half of the year (H1 FY23, six months ending March 31, 2023), the company actually saw a revenue decline of 1% when the market is included. The decline happened because the company exited Russia in April 2022. Excluding Russian operations from the prior year period resulted in only 0.6% growth in revenues.

Essentially, the forecasts indicate that the company's full year revenue growth might be similar to ex-Russia adjusted revenue growth at CC. The actual adjusted revenue has grown by 4.8% revenue growth in H1 FY23. With the company expecting positive exchange rate trends for the full year FY23, we can expect revenue growth to be slightly higher than current rates.

{kind=link}

The operating profit forecast

On profits, Imperial Brands expects the adjusted operating profit at CC to come in "at the lower end of our mid-single digit range at constant currency". For context, for H1 FY23, adjusted operating profit grew by just 0.8% inclusive of the impact of the Russia business and at 1.2% excluding it.

The growth so far is clearly lesser than the range forecast, indicating that it can improve in H2 FY23. The company does allude to expected improvements in adjusted operating profit growth in this time in its half year financial release , resulting from both pricing actions and cost savings.

Even now, in reported terms, adjusted operating profit growth isn't bad at 7.3%. Going by the company's expectation of favourable exchange rate trends for the full year FY23, it's likely to be even higher in the next update.

Competitive forward P/E

To assess its forward market multiples, let's assume for now however that the reported adjusted operating profit growth stays the same as in H1 FY23. It's also assumed here that the net profit to operating profit ratio remains static at 69%. the profit figure comes at USD 3.35 billion for its latest financial year.

This in turn translates into a forward non-GAAP price-to-earnings (P/E) ratio of 5.9x. Among the biggest five tobacco stocks, this is the most competitive of the lot (see chart below), with the ratio being unavailable for Japan Tobacco Inc. ( OTCPK:JAPAY ).

Source: Seeking Alpha, Author's Estimates

Even its trailing twelve months [TTM] GAAP P/E ratio is second only to British American Tobacco p.l.c. ( BTI ), as seen in the chart above. On average, IMBBY compares favourably to peers' average forward P/E at 8.98x and TTM P/E at 11.22x. This in turn reflects that there's a 15-20% upside to the Imperial Brands price right now.

With share buybacks of GBP 1.1 billion (USD 1.35 billion) slated for FY24, which are a little under 7% of the current market capitalisation, the potential share price uptick is even more.

Healthy dividends

Additionally, there are dividends to consider. The company has a healthy TTM dividend yield of 7.7%. It's not the highest among its peers, as British American Tobacco and Altria Group, Inc. ( MO ) have 9%+ yields. But it isn't the worst either, being higher than yields offered by Japan Tobacco and Philip Morris International at 6.05% and 5.58% respectively. In any case, on its own, the yield is high. For context, the consumer staples sector on average has a TTM yield of 2.8%.

The dividend outlook is also good considering the company's progressive dividend policy, which means that it intends to grow dividends every year based on business performance. In H1 2023, Imperial Brands has already seen a reported earnings per share [EPS] increase of 11.2% and an adjusted EPS rise of 4.9%. Coupled with expectations of improved adjusted operating profit growth in H2 FY23, there's then reason to expect further dividend increases.

NGP growth is key

Over the medium term, the company's expectations for revenue and profit growth are no different really than what it expects for FY23. This hardly makes it the fastest-growing company around, but it does mean that the dividends can be stable going forward, which is its unique selling point.

However, there's a red flag for Imperial Brands when it comes to the realignment of its business to smoking alternatives. In H1 FY23, NGPs had just 1.3% share in revenue which is exceptionally low. BTI, for instance, has a 12.3% share for the same as per its latest financial report . NGPs are growing fast, to be sure, at almost 30% in H1FY23.

But I'd look out for this aspect, because it's key to long-term growth in the business, especially as the company has reported a 12.7% decline in tobacco volumes recently. While it attributes the softening to the exit from Russia and a post-COVID-19 adjustment in buying patterns, it's not an entirely convincing argument. While tobacco volumes are expected to decline globally this year, some companies like Japan Tobacco are bucking the trend , for instance.

What next?

Putting aside the small share of NGPs right now, I think the Imperial Brands story looks good right now. Even though its revenues are growing at a snail's pace, its profits are growing faster. This in turn has made its market multiples competitive compared to peers.

Further, with a progressive dividend policy in place, growing profits means that it can continue to reward investors with better passive income over time. In sum, while there's a question mark on its long-term story, for now, Imperial Brands is a Buy.

For further details see:

Imperial Brands: Expected Profit Growth Bodes Well For Dividends