IMBBY - Imperial Brands: NGP Growth Encouraging But Tobacco Volumes Need To See Recovery

2023-11-17 12:02:07 ET

Summary

- Imperial Brands has seen growth in its stock price, with earnings growth having been influenced by stock buybacks.

- While pricing growth across the tobacco segment has continued, volume growth needs to see recovery.

- I rate Imperial Brands as a hold at this time.

Investment Thesis: I continue to rate Imperial Brands (IMBBY) a hold, on the basis that volume growth across the tobacco segment needs to rise to justify upside in the stock.

In a previous article back in October, I made the argument that Imperial Brands needs to see a rebound in volume growth across both the cigarette and mass market cigar segments before upside can be expected in this stock.

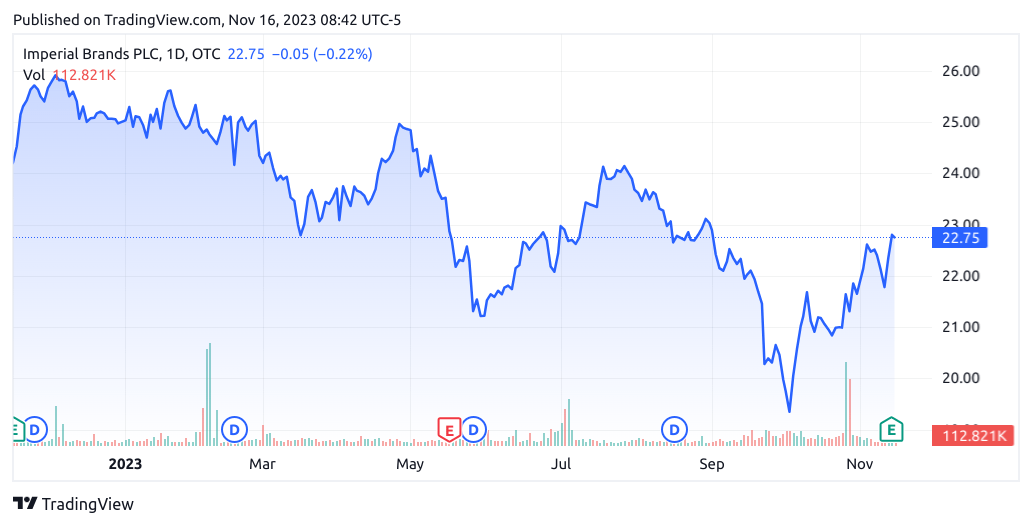

However, the stock has ascended to a price of $22.75 at the time of writing:

{kind=link}

The purpose of this article is to assess why the stock has been rising and whether Imperial Brands has the ability to see continued growth from here taking recent performance into consideration.

Performance

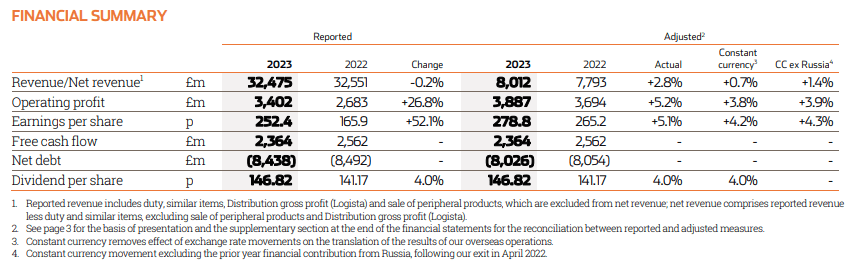

When looking at full-year earnings results for Imperial Brands as released on November 14, we can see that on an adjusted constant currency basis - revenue is up by 0.7% and 2.8% on an actual basis.

Imperial Brands Full Year Results Statement: 14 November 2023

{kind=link}

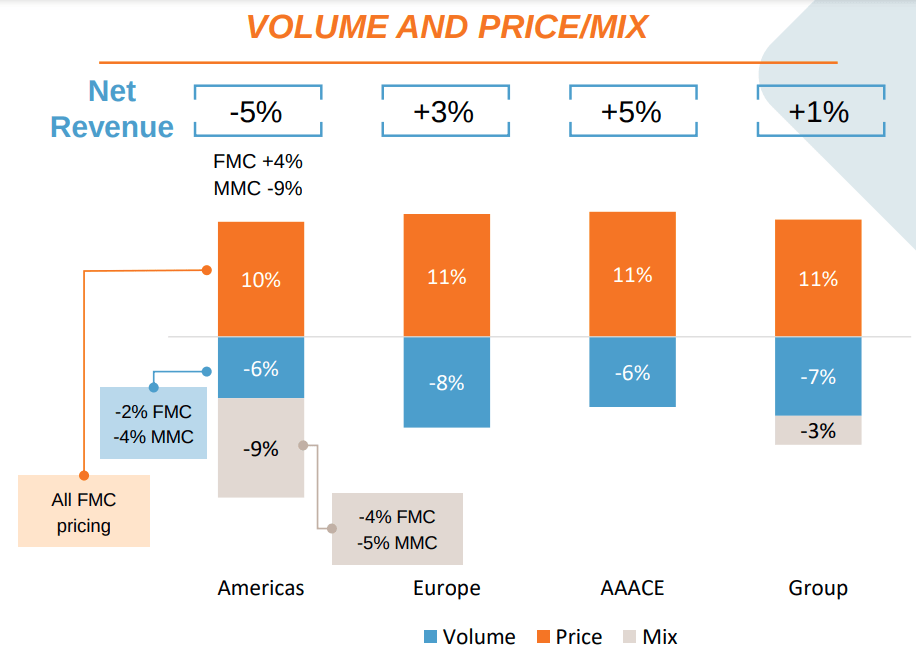

I had previously stated in my previous article that one of the reasons for the decline in tobacco volume that we had been seeing across the company's half-year results was related to a decline in mass market cigars. This is due to the pricing differential as compared to the factory made cigarettes segment, with Imperial Brands estimating that the revenue per cigar is approximately 2.6 times that of cigarettes. For instance, across the Americas - while there was a 1% growth in volume for FMC (factory made cigarettes), there was also a volume drop of 4% for MMC (mass market cigars) - which resulted in a 3% drop in volume for the region overall.

When now looking at full-year results, we can see that both FMC (factory made cigarettes) and MMC (mass market cigars) saw a decline in volume of -2% and -4% respectively.

{kind=link}

However, we have still seen a favourable rebound in stock price which may have been driven by rising tobacco prices having helped to offset volume declines, but particularly - earnings per share has seen a strong rise due to ongoing share buybacks by Imperial Brands resulting in a reduction in share count.

Specifically, the company announced on October 5 a £1.1 billion share buyback for FY24, which represents a 10% increase on the £1 billion share buyback for 2023. In this regard, the recent rise in stock price is likely to have been significantly influenced by such buybacks and in my view, this will likely continue to be the case for as long as such buybacks continue to increase earnings per share.

We can see that in spite of a significant fall in earnings per share through to 2023, the same rebounded strongly to $3.173 per share, with the P/E ratio down to 7.306x and trading near a five-year low.

YCharts.com

With regards to short-term liquidity, we can see that the quick ratio of Imperial Brands (calculated as total current assets less inventories all over total current liabilities) has increased slightly but remains significantly below 1.

| Mar 2022 |

| Mar 2023 |

| Sep 2023 |

| Current assets |

| 7867 |

| 8541 |

| 8595 |

| Inventories |

| 4445 |

| 5025 |

| 4522 |

| Current liabilities |

| 11158 |

| 11523 |

| 11899 |

| Quick ratio |

| 0.31 |

| 0.31 |

| 0.34 |

Source: Source: Figures (in £ millions except quick ratio) sourced from Imperial Brands plc Half Year and Full Year Results Statements for 2023. Quick ratio calculated by author.

That said, we can also see that non-current borrowings to total assets has also decreased slightly during this time:

| Mar 2022 |

| Mar 2023 |

| Sep 2023 |

| Non-current borrowings |

| 7979 |

| 8376 |

| 7882 |

| Total assets |

| 28111 |

| 29212 |

| 29491 |

| Non-current borrowings to total assets ratio |

| 28.38% |

| 28.67% |

| 26.73% |

Source: Figures (in £ millions except ratios) sourced from Imperial Brands plc Half Year and Full Year Results Statements for 2023. Non-current borrowings to total assets ratio calculated by author.

My Perspective and Looking Forward

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, I take the view that while share buybacks could artificially spur significant earnings growth going forward - I continue to maintain that Imperial Brands ultimately needs to see a revitalisation in volume growth going forward to ensure long-term upside.

In terms of potential performance for the mass market cigar segment going forward, this segment continues to be affected by a wholesaler destock with inventories having been increased ahead of Hurricane Ian in September 2022. Additionally, the higher pricing of mass market cigars as compared to cigarettes and pressure on consumer disposable income has in turn placed pressure on volume demand.

Imperial Brands states that with the company's investment in alternative products such as vape, heated tobacco and modern oral - the company is in a good position to expand revenue across its NGP (next generation product), which incidentally saw growth of 26% in net revenue.

With that being said, I am optimistic that the mass market cigar segment has the capacity to see growth in volume once again - Statista estimates that revenue for the cigars market worldwide will amount to US$22.4bn in 2023, and the market as a whole is expected to see a CAGR of 4.17% through to 2028. Additionally, with the U.S. cigar market generating the highest revenue and demand among younger consumers now rebounding following a historically long-term downward trend - Imperial Brands strong presence in the mass cigar market with its Backwoods brand puts the company in a good position to capitalise on industry growth.

Risks

In terms of the potential risks to Imperial Brands at this time, the potential for volume demand to head lower due to both adverse macroeconomic conditions as well as a continued switch on the part of customers to next generation products could place further pressure on revenue growth across the Tobacco segment.

While Imperial Brands is expanding its NGP offerings - the Tobacco segment still accounts for the majority of the company's revenue. As such, there will come a point where price increases alone cannot sustain revenue growth - volume will need to rise in order to sustain such growth.

Conclusion

To conclude, Imperial Brands has seen pressure on volume growth which has been partially offset by higher pricing. The company's continued share buybacks aim to artificially push earnings higher which could see the stock appreciate. However, I take the view that we ultimately need to see a revitalization in volume growth for meaningful upside at this point. In this regard, I continue to rate the stock a hold.

For further details see:

Imperial Brands: NGP Growth Encouraging, But Tobacco Volumes Need To See Recovery