BTAFF - Imperial Brands: No Growth In Sight

2023-06-11 01:27:23 ET

Summary

- Imperial Brands PLC produces and sells tobacco and tobacco-related products across the world.

- Revenue growth has remained positive in the last few years but IMB is failing to diversify away from tobacco.

- Margins continue to be impressive, allowing for outsized dividend payments (c.7% yield). We believe these to be sustainable.

- Comparing IMB to its consumer staple and tobacco peers, we consider IMB to be unattractive beyond a pure income play.

Investment thesis

As economic conditions worsen and investors continue to see markets struggle, many are looking for defensive stocks that can perform well under downturns. We believe that Imperial Brands may be a good option for this purpose. To determine this, we will conduct a thorough analysis of Imperial Brand's financials to evaluate the sustainability of its business operations and its ability to generate FCF.

Company description

Imperial Brands PLC ( OTCQX:IMBBY / OTCQX:IMBBF ) produces and sells tobacco and tobacco-related products across the world. Its product portfolio includes cigarettes, fine-cut tobacco, cigars, and next generation products like e-vapour and heated tobacco products.

Its products are sold under various brands such as Davidoff, Winston, blu, and Golden Virginia, among others.

Share price

IMB's share price has trended down in the last decade as tobacco consumption in the west declines and IMB seeks to diversify away from this income stream. We are in the middle of a several-decade shift in consumer habits, as developed countries legislate consumption away.

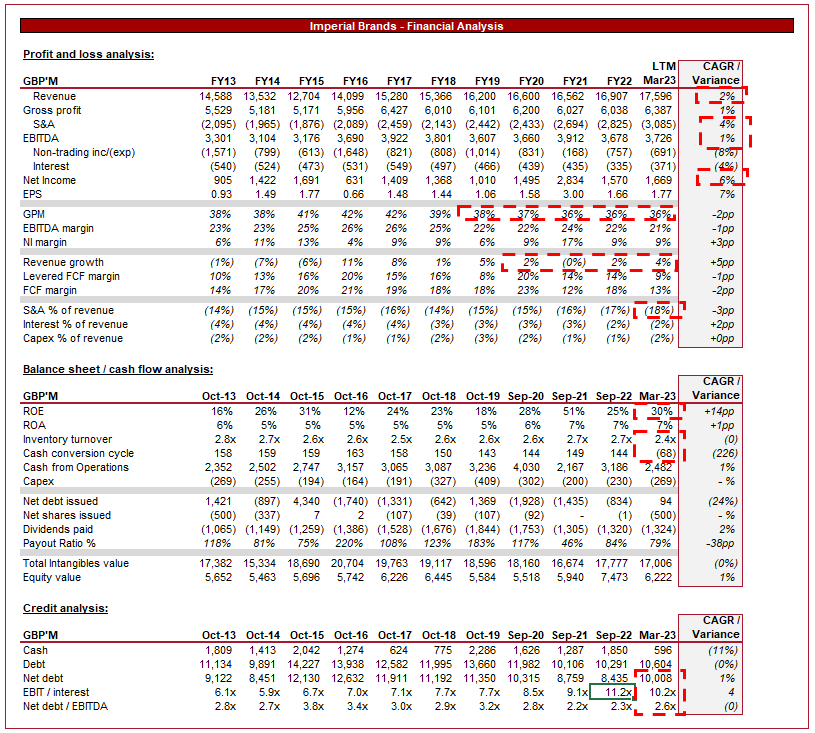

Financial analysis

{kind=link}

Imperial Brands financials (Tikr Terminal)

Presented above is Imperial Brand's financial performance for the last decade. Our view is that the company is surprisingly robust, presenting an attractive alternative to many consumer staples.

Revenue

Although some might expect a noticeable decline, revenue has actually grown at a CAGR of 2%.

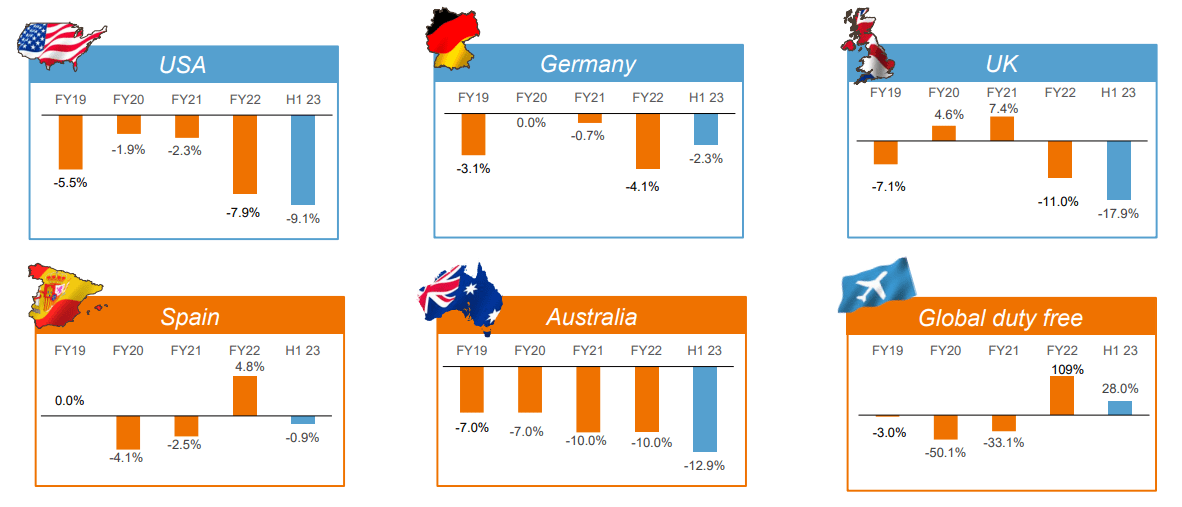

IMB will continue to face the negative trend in tobacco consumption as Governments around the world implement strict regulations and policies to discourage consumption. Additionally, with a greater understanding of the human body, consumers are choosing to lead healthier lives, accelerating the impact. The response to this outside of developing alternatives is to focus on key consumption regions, such as the developing world, as well as material price increases. This said, as the following illustrates, the volume trend has been noticeably negative.

{kind=link}

Volume (IMB H1)

Although market focus has been useful in partially offsetting the decline in volume, the eventuality is that these regions will also see greater regulation and a downward trend in consumption.

With the decline in tobacco consumption, there has been an increase in the demand for alternative products such as e-cigarettes and other vaping products. These products are perceived to be less harmful than traditional tobacco products and are often marketed as a way of quitting smoking. IMB owns the company blu, which has a market share of 2.3% according to Statista (as well as Pulze and ID in the HT segment). This has allowed IMB to benefit from the decline in tobacco consumption while growing a new market based on the perception that it is an activity that is healthier than tobacco. This being said, tobacco is still the majority of what the company does and so the gains from this segment can only have so much of an impact. Further, unlike many of its peers, IMB has struggled to gain market share in line with its Tobacco positioning.

{kind=link}

Tobacco/NGP sales (Imperial Brands)

As the above table also illustrates, IMB has chosen to exit Russia , significantly impacting a key region of the business. This resulted in a P&L write-down, but more importantly, is another region lost which had scope for growth.

Reduced-risk products do not come without risk, however, as the FDI has recently issued a marketing denial order on severa l BTI vape products. This represents a genuine ongoing risk to the business and could see this segment grind to a halt very quickly. This stresses the importance of a genuine pivot away from nicotine-related goods. Altria ( MO ), a tobacco peer, has hinted that it could enter the caffeine and cannabis industry.

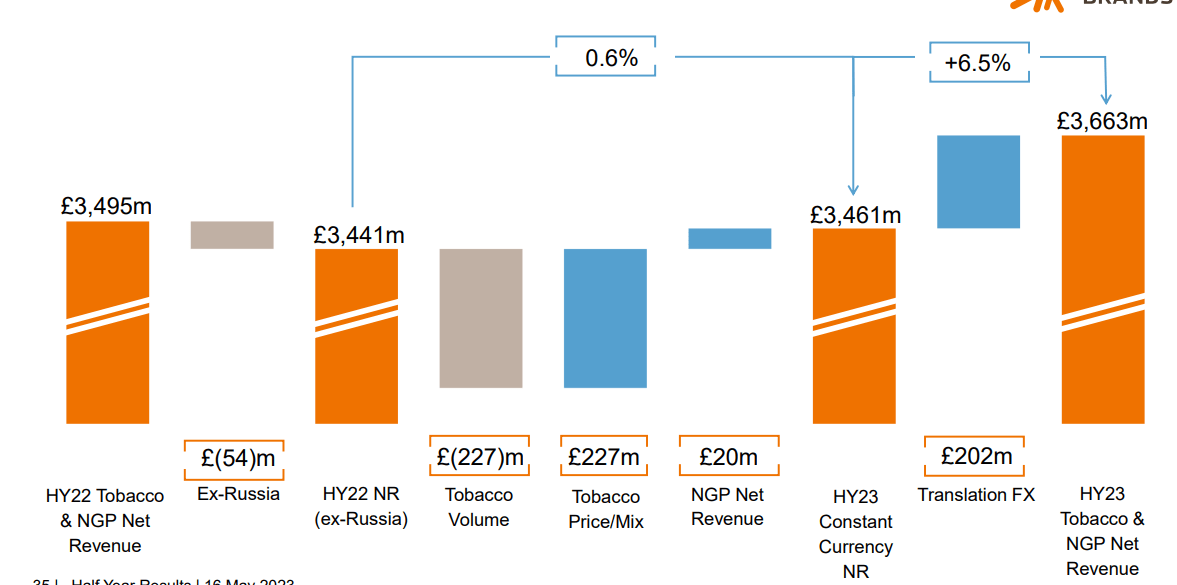

We are currently experiencing inflationary pressures driven by supply chain issues, among other factors. This is contributing to a decline in discretionary income, as a greater portion of income is spent on living costs. This is an issue for businesses from both a demand and supply perspective. In the case of IMB, the business should experience inelastic demand. Tobacco is addictive in nature, making it difficult for consumers to forego. As the following illustrates, the net benefit for IMB by increasing prices is nil.

{kind=link}

Net Revenue Bridge (IMB)

We would expect a far higher level, suggesting big Tobacco does not have the pull it once did. With gains so marginal (c.1.3% in FY22), the company has seen its GPM decline in recent years. The lack of noticeable pricing power is a highly unattractive trait for a consumer business.

Margins

IMB has not performed well operationally in our view, experiencing an increase in S&A expenses in excess of revenue. This suggests a misallocation of resources, which is a bigger issue when revenue growth is 2%. The company has seen its interest payments declining which is a small positive but profitability has essentially remained flat.

Balance Sheet

Moving onto the balance sheet, we can see how the company has allocated its resources. Dividend payments have increased, while debt has been repaid. This is a good allocation of resources and allows for the company to be more flexible going forward. IMB's ND/EBITDA ratio has declined to 2.25x, which is a healthy level in order view. Management has stated that they will begin share buybacks in FY23, which looks to be a good decision, with interest payments now representing 2% of revenue.

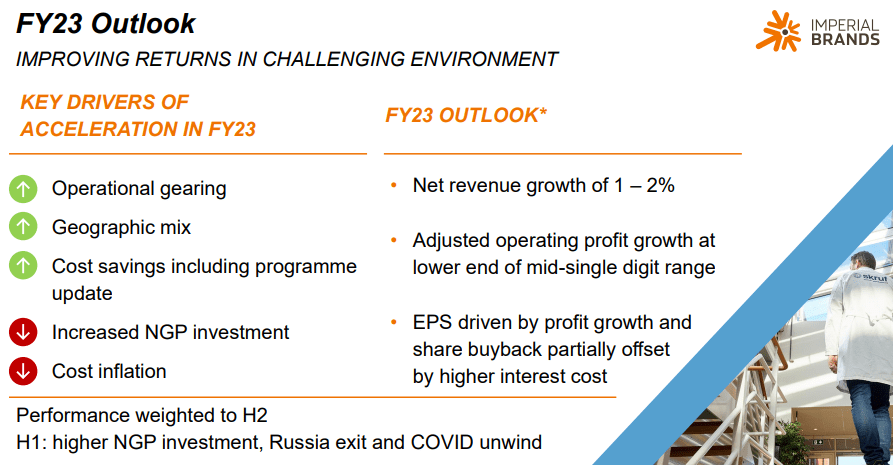

Outlook

{kind=link}

Management outlook (Imperial Brands)

Management is forecasting revenue to grow at a rate of 1-2%, essentially following its current trend. This looks like a reasonable estimate, but the volume data is not pretty. All of the company's key geographical markets have seen quite noticeable declines, with the gains being offset by other geographies and products (NGP). Management describes this geographical shift above as a positive, but it could be the early signs of another period of declining revenue. Geographical diversification also comes with greater FX risk, which has the potential to cause single-digit revenue movements which, in the case of IMB, could wipe out any gains.

Dividend

IMB's current dividend yield is 8%, representing the return required to entice an investor into a declining industry. In the most recent period, IMB had a payout ratio of 79%, which looks high but is a metric that has varied wildly as non-trading items have impacted underlying operating profits. If we look at OCF instead, the company generated £2.5BN in the most recent year, with only a £0.4BN CFI. Based on this, the company has c.£2BN to put toward deleveraging and distributions. The most recent dividend payment was £1.3BN, suggesting a sufficient buffer to continue at this level.

Peer comparison

{kind=link}

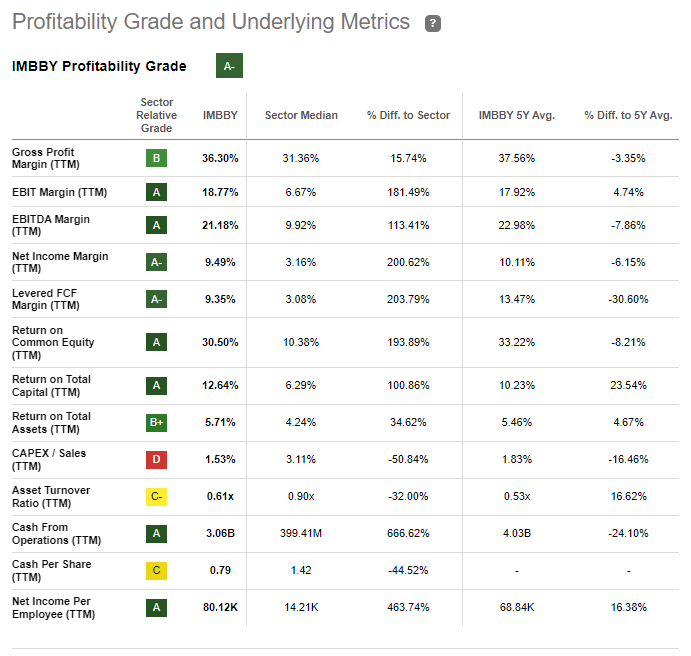

Profitability (Seeking Alpha)

As our objective is to assess IMB from the perspective of being an alternative to traditional consumer staples, we have utilized Seeking Alpha's rating system, which compares the company's key metrics to this sector group.

From a profitability perspective, IMB performs extremely well, achieving an outperformance across all of the key metrics. The ones we care about most are the NTM EBITDA-M and FCF-M, both of which are substantially above the average. For this reason, IMB is one of the lower-risk income plays, as the company generates far too much cash to see dividends not growing in the next few years.

{kind=link}

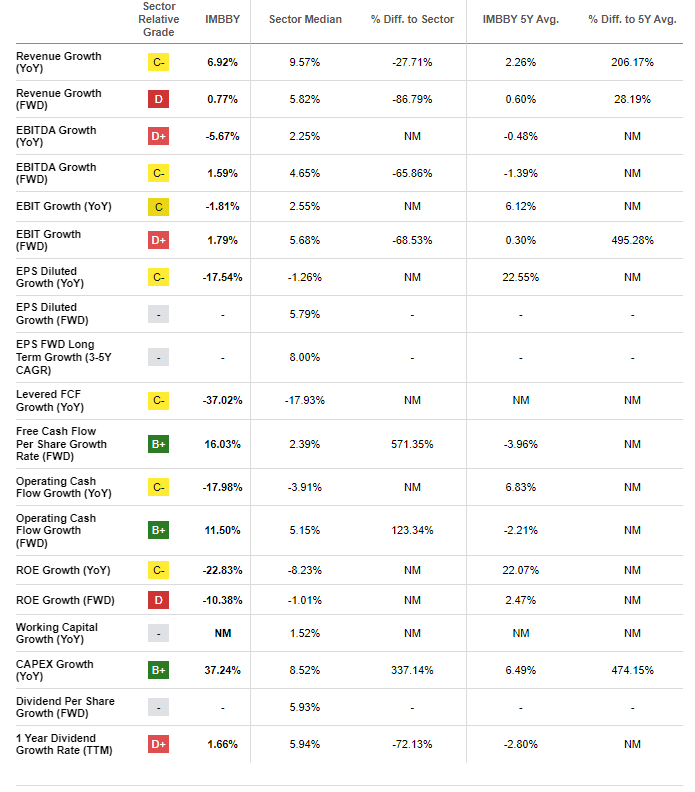

Growth (Seeking Alpha)

The issue as we have already established is growth, with the company scoring incredibly poorly across all metrics. Revenue and EBITDA growth look non-existent, while the sector as a whole experiences gains above the sustainable inflation rate.

Valuation

{kind=link}

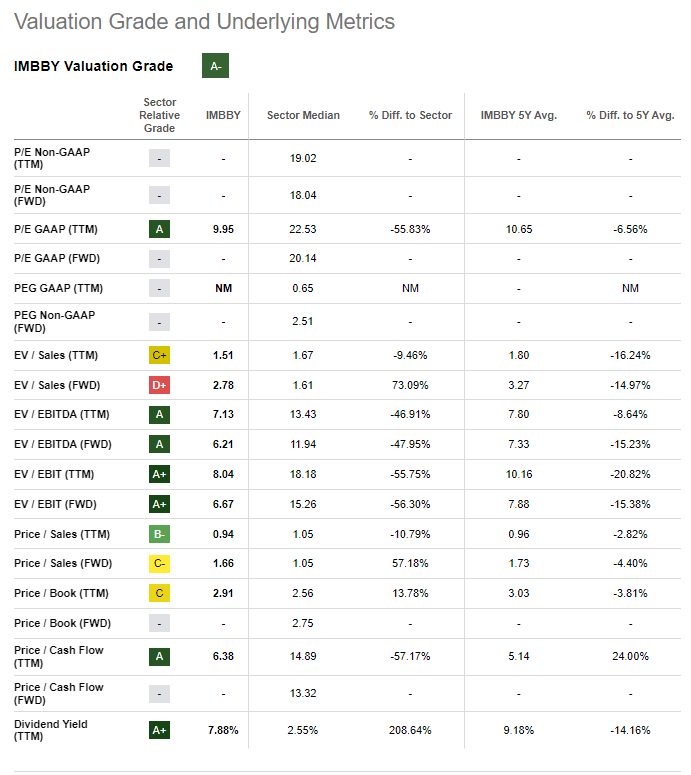

Valuation (Seeking Alpha)

From a valuation perspective, the company looks relatively attractive. IMB is trading at a discount across all of the key metrics, with a 48% NTM EBITDA delta and a 47% LTM earnings delta. Once again, this is a reflection of the risks associated with a declining industry, as investors price an appropriate discount for the lack of top-line upside.

Tobacco peers

{kind=link}

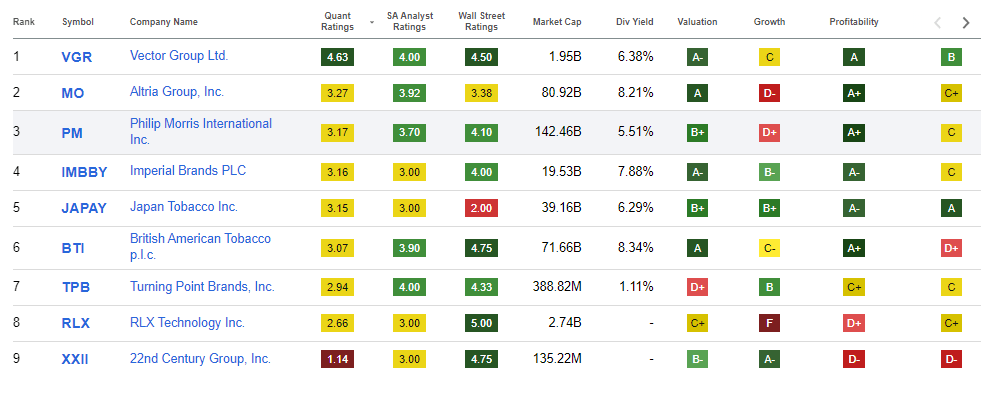

Peers (Seeking Alpha)

When comparing the company directly with its Tobacco peers, it looks to be lacking the performance of its larger peers. From a commercial perspective, we do not see anything to write home about, making it difficult to justify this as an investible tobacco stock, let alone a consumer staple. Why would investors buy IMB when BTI pays a higher dividend while trading at a 2x discount? (NTM P/E) Further, if investors are looking for growth, PM is forecasting 6% in the NTM, while trading at a 5x premium. The only positive valuation-wise is that the company is trading close to its all-time lows, suggesting it is at the bottom.

Final thoughts

IMB is not a good alternative to traditional consumer staples. The company's commercial profile remains unattractive, as it has been unable to diversify away from tobacco. For this reason, it will continue to see western demand dwindle as other geographies slow the decline. From a pure income play, the company does represent some value, as investors can receive substantial dividend payments which remain protected against cuts in the near term.

For further details see:

Imperial Brands: No Growth In Sight