IMBBY - Imperial Brands: Too Far Behind The Competition

2023-05-18 00:46:54 ET

Summary

- Imperial Brands is still too dependent on tobacco sales.

- The NGP segment is only growing in Europe and is negatively affecting margins.

- Competitors such as Philip Morris are much further ahead in the process of transitioning to products that are less harmful to health.

- Dividends and buybacks are still sustainable, but for how long if free cash flow does not increase?

Imperial Brands PLC's ( IMBBY ) (IMBBF) five-year plan to become a more sustainable company with a more promising future continues, but there are several obstacles. The segment or Next generation product (NGP) is definitely the most promising one, in fact it achieved an overall growth of 19.80% over the first half of FY 2022. Tobacco, is still the main segment and net revenues have increased slightly, but volumes are declining, both due to lower demand and price increases. However, there are several red flags.

Let us now look at this in detail.

Comment on the first half of FY 2023

Imperial Brands H1 2023 results

As a first thing, here is a table summarizing the key income results for this first half of FY 2023:

- Revenues had a slight increase of 0.30%, while operating income improved by 27.70% to £1.53 billion.

- As for dividend per share, it increased by 1.50% to 43.18p. Also affecting this figure was the £1 billion share buyback program.

Currently the dividend yield is 7.70%, which is quite high even considering the low dividend taxation in the UK. What is more, from the words of CEO Stefan Bomhard , shareholder remuneration seems to be a crucial point for the company, and therefore we can expect increasing dividends and new buybacks in the future:

We remain on track to deliver the acceleration in adjusted operating profit growth in the second half in line with our guidance and expectations. I am confident the actions we have taken are creating a stronger, more resilient business capable of driving shareholder returns through a growing dividend and an ongoing share buyback.

But how feasible is this goal really?

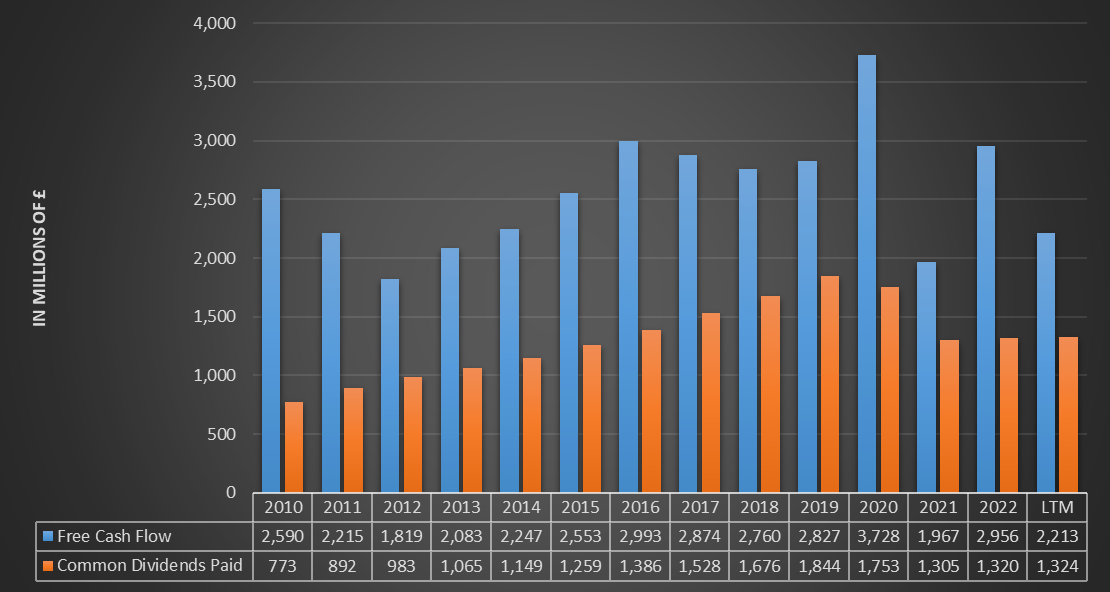

Considering the full FY 2022 figures, free cash flow was £2.95 billion and dividends issued were £1.32 billion. So, a differential of £1.63 billion that makes the high dividend absolutely sustainable. There is one problem, however: the free cash flow generated in 2022 is virtually the same as that generated in 2016, and close to that generated in 2010.

{kind=link}

In short, now the dividend is more than sustainable, but if the free cash flow does not grow in the long run, then it will be increasingly difficult to boost the dividend and buy back own shares.

Since the tobacco segment is in decline, Imperial Brands' main source of growth comes from the sale of next generation products (NGP). Let us now look at the key figures for each individual geographic area.

Imperial Brands H1 2023 results

{kind=link}

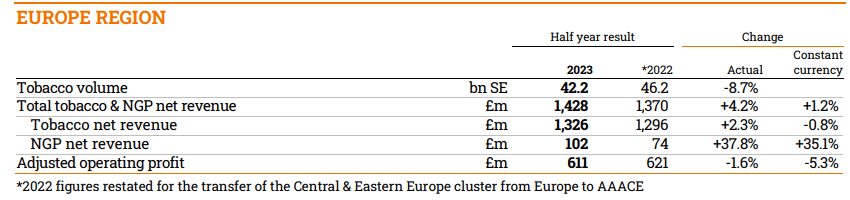

Tobacco sales volume in Europe decreased by 8.70%, probably due to the 7.90% price increase. The overall result was a decline in net revenue of 0.80% in constant currency. This segment has little prospect for growth for obvious reasons, both social and health.

NGP net revenue increased by 35.10% in constant currency to £102 million. This strong growth positively affected total net revenues from Europe, in fact the two segments combined achieved 1.20% growth in constant currency; however, in terms of profitability the NGP segment is still a drag. In fact, overall adjusted operating profit is down 5.30% from the first half of FY 2022.

Major investments in NGP products and market launches are impacting Imperial Brands' profitability, but it is in my opinion an inevitable choice. This segment is the only one that can bring long-term growth, and at the moment achieving 35% revenue growth can be considered a good result. The problem, more than anything else, is that NGP revenues are still minuscule when compared to those of Tobacco sales. In this regard, Philip Morris ( PM ) is far ahead and projected into the future. I suggest you read this article if you are interested in the topic.

Anyway, here are the new launches in Europe made in the last 6 months:

- Pulze 2.0 is now available in Greece, Italy, Portugal and Bulgaria

- blue 2.0, has now been launched nationwide in the UK, France and Spain, Germany, Portugal, Greece and the Canary Islands

Imperial Brands H1 2023 results

{kind=link}

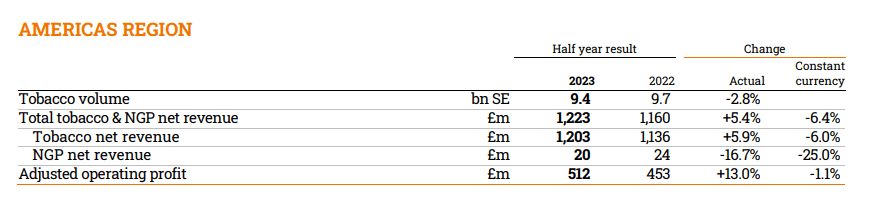

Tobacco sales volume also declined in the Americas, but in this case the 25% reduction in NGP net revenues in constant currency is worrying. A disappointing result to say the least: this should be the future for Imperial Brands.

The reason for such a negative performance in this segment is due to the myblu product non-marketing order issued in April 2022 by the FDA. An appeal has been filed and the company is awaiting the response.

A positive response would be critical for Imperial Brands, as the Americas is a key business area. NGP's growth rates are higher in the West than in the East, where exclusively tobacco sales dominate.

Imperial Brands H1 2023 results

{kind=link}

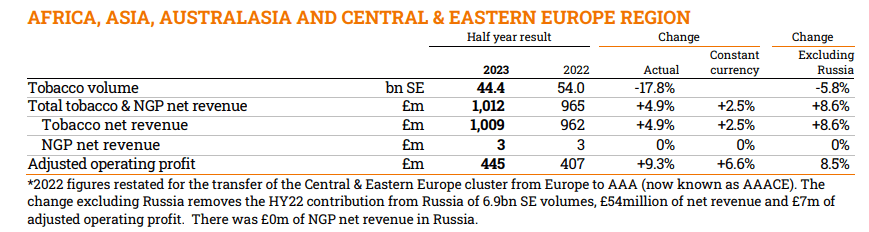

As we can see in the AAACE area, tobacco reported 8.60% growth (excluding Russia), while NGP net revenues are virtually nonexistent, only £3 million in the first half of FY 2023.

Overall, the tobacco segment once again drove net revenue growth, despite declining volumes. However, my view is that this positive news may somewhat underestimate the importance of NGPs. This segment is growing fast in Europe, but in America and the East there is no improvement. What's more, even though sales are increasing in Europe, margins in this sector are negative. This is what emerges from this first half of FY 2023.

In short, I think Imperial Brands is relying too much on tobacco sales, which may be good in the short to medium term, but a serious problem in the long run. Right now the demand for tobacco is still high, but it has been declining for decades. By the time tobacco is no longer such a profitable segment, it may be too late. Other companies such as Philip Morris are already ahead in this process; in fact, suffice it to say that 32.20% of its revenues come from smoke-free products.

For further details see:

Imperial Brands: Too Far Behind The Competition