IMBBY - Imperial Brands: Troubling Read-Across From Peers' Q4 Results

Summary

- Imperial Brands had only reported results up to September, and will not report again until May - but its peers have released Q4 results.

- The read-across is worrying. Cigarette industry volume fell by 8% or more in 3 of Imperial Brands' top-5 markets in 2022.

- Competitors have continued to dominate Reduced Risk Products categories, even where IMB has launched its own offerings.

- Altria and British American Tobacco are deleveraging, signalling pessimism ahead; Philip Morris is preparing for its U.S. expansion.

- The stock has a 7.7x P/E and 7.0% Dividend Yield, but Altria’s Divided Yield is higher and BAT’s P/E is similar. Avoid.

Introduction

Imperial Brands PLC ( IMBBY ) (referred here as "IMB") last reported FY22 results (ending September 2022) in November, and is not scheduled to release another set of results until May 2023. However, with Japan Tobacco ( JAPAY ) having reported their Q4 results on Wednesday (14 February), we now have 2022 read-across from all four other major Tobacco companies.

Cigarette industry volume fell by 8% or more in three of IMB's top-5 markets, including the U.S., with declines accelerating through the year. Reduced Risk Products from IMB's competitors have continued to dominate their respective categories in countries where IMB has launched its own offerings. Altria ( MO ) and British American Tobacco ( BTI ) (referred here as "BAT") have decided to reduce their leverage significantly, likely signalling pessimism ahead. Philip Morris ( PM ) has now acquired Swedish Match and is preparing for a major expansion in the U.S. IMB has a superficially attractive 7.7x P/E and 7.0% Dividend Yield, but Altria's dividend yield is higher and BAT's P/E is similar, both with arguably fewer structural risks. We continue to believe IMB shares should be avoided.

Cigarette Volume Declines Accelerating

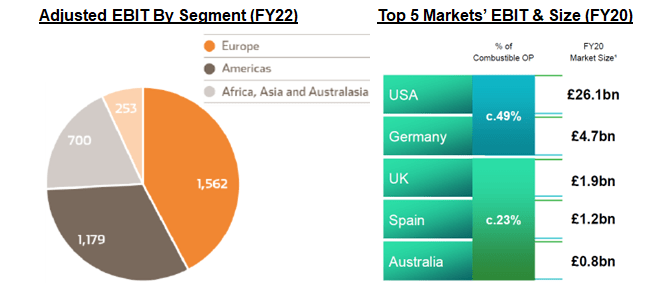

IMB's top-5 markets are the U.S., Germany, the U.K., Spain, and Australia, with the U.S. generating approximately 30% of its EBIT and Germany generating around 20%; Europe is its largest region, with 45% of FY22 EBIT:

| IMB EBIT By Segment & Top 5 Markets NB. U.S. not reported separately since FY19. |

{kind=link}

Based on results from IMB's peers, we believe 2022 cigarette industry volume results for IMB's top-5 markets were:

- U.S. down 8%, including down 9% in Q4

- Germany down 5.1%, including down 9.0% in Q4

- U.K. down 17%, including down 20% in Q4

- Spain up 4.5% in 2022, including up 1.0% in Q4

- Australia down 8.2% in 2022, including down 11.5% in Q4

(U.S. figures were from Altria results; Germany, Spain, and Australia figures were from Philip Morris results; U.K. figures were estimated by us from Japan Tobacco volume and market share numbers.)

Cigarette industry volume decline was at or above 8% in three of IMB's top-5 markets, including the U.S. Volume growth in Spain is likely due to the return of tourists (including from the U.K.), after COVID-19 restrictions were lifted. However, Spain is a smaller market than the U.K., and revenue per cigarette there is also lower, and IMB has acknowledged that the shift in volume from the U.K. to Spain is dilutive to revenues.

In four of IMB's top-5 markets, cigarette industry volume trends worsened in Q4 than in Q1-3. We know from our review of Altria's Q4 2022 results that volume decline in the U.S. had definitively accelerated through 2022, both on a year-on-year basis and on a three-year stacked basis (i.e., comparing to pre-COVID 2019):

| Altria Cigarette Volume Declines (Adjusted) (Since 2020) Source: Altria company filings. |

Tobacco executives have generally attributed the acceleration in cigarette volume declines to macroeconomic headwinds. This is almost certainly the case in the U.S., where Heated Tobacco products are not available, and Vapour volumes have been stagnating since Q2 (partly due to FDA enforcement actions). However, we believe that Reduced Risk Products could have had an impact in Europe, with Philip Morris Heated Tobacco Units volume growing 40% year-on-year (to 39.5bn sticks) in the European Union, and BAT growing its Heated Tobacco volume in Europe by 34% (to 13.0bn sticks) and its Vapour volume by 14% (to 197m pods), respectively.

We expect IMB cigarette volumes to come under further pressure during H1 FY23.

Rival Reduced Risk Products Still Dominate

Reduced Risk Products by IMB's competitors have continued to dominate their respective categories in countries where IMB has launched its own offerings.

In Heated Tobacco , IMB has been selling its (Pulze and ID) products in Greece and the Czech Republic since September 2021 and has launched them in Italy, Portugal, and Hungary during FY22. Philip Morris data shows that its IQOS continues to dominate and grow in these countries, for example with an 18.1% share (up 2.3 ppt year-on-year) of the overall tobacco market in Greece and a 15.9% share (up 4.1 ppt) in the Czech Republic:

| PM Heated Tobacco Offtake Share in Selected E.U. Countries (Q4 2022) NB. The U.K. is reported in PM's E.U. region. |

{kind=link}

IQOS's share of the Heated Tobacco category is likely to exceed two-thirds in most countries, leaving little for IMB.

In Vapour , IMB has launched its new blu 2.0 products in the U.K. and France, and has also launched a "blu bar" disposable Vapour product in the U.K. in November 2022. IMB has also continued to sell myblu Vapor products in the U.S., while it appeals the FDA's Marketing Denial Order in April 2022. BAT data shows that its Vuse product continues to dominate the closed category in France and has a nearly 37% value share in the U.K., little change from the start of year, implying IMB's Vapour products have made little progress in either country:

{kind=link}

In Oral Tobacco , IMB is selling its Zone X products in the Nordic and Austria. However, this is a small market, and IMB is behind both Swedish Match ( SWMAY ) (now part of Philip Morris) and BAT, so we do not expect IMB's efforts here to have a material impact on the group.

Peers' Deleveraging Signals Pessimism

Altria and BAT have decided to reduce their leverage significantly, likely signalling pessimism in the cigarette market.

BAT is now targeting "the middle" of their 2-3x Net Debt/EBITDA target range, i.e., 2.5x, compared to 2.89x at 2022 year-end. This means no new buybacks were announced for 2023. Management was satisfied with Net Debt/EBITDA being below 3x previously, having spent £2bn on share buybacks in 2022. Reasons cited by management include "the uncertain macro environment, higher interest rates, outstanding litigation, and regulatory matters", but the change also came after BAT saw 10%+ declines in its cigarette volumes in both the U.S. and Europe in 2022.

Altria has decided to pay back about $1.3bn of debt due with cash, despite Net Debt/EBITDA already being just 2.1x at 2022 year-end. (The debt repayment will take it down to below 2x.) Management expects $1bn of share buybacks in 2023, lower than the $1.8bn in 2022, despite a pending $1.7bn plus interest payment from Philip Morris (related to the agreement to hand back U.S. IQOS rights). Altria had just reported a 12.1% decline in its cigarette volume in Q4.

If cigarette volume declines accelerate, even temporarily, investor confidence may decline, and Altria and BAT would find it more expensive to refinance debt. We believe this is a key motivation behind the decision to deleverage.

IMB had a Net Debt/EBITDA of 2.0x at November 2022, the low end of management's 2.0-2.5x target range. 17% of its borrowings (£1.54bn) will come due during FY24-25:

{kind=link}

We expect IMB's interest expense to rise when these are refinanced, as its all-in cost of debt was just 3.5% in FY22.

Philip Morris Signalling Major U.S. Expansion

Philip Morris has acquired Swedish Match and is actively working on expanding in the U.S., as CFO Emmanuel Babeau explained on their Q4 2022 call :

"A key focus this year will be supporting and further driving strong ZYN growth in the U.S. … In parallel, we will be actively enhancing Swedish Match's U.S. distribution and commercial capabilities for the launch of IQOS in 2024"

As we explained in our review of Philip Morris's Q4 results, ZYN has continued winning in the growing U.S. nicotine pouch category, there will be an application for U.S. marketing approval for its VEEV Vapour product in 2023, and IQOS stands a good chance to succeed at scale in the U.S. in 2025.

These are all growing threats to IMB.

Valuation: Is Imperial Brands Stock Cheap?

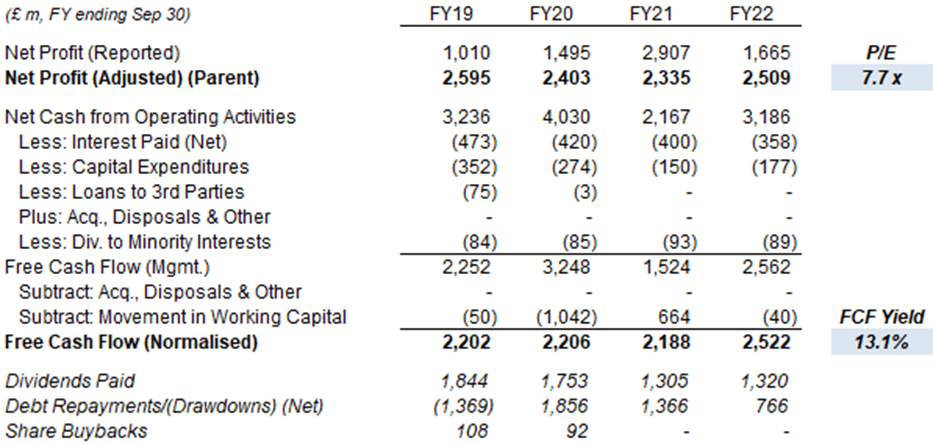

At 2,022.0p, IMB shares have a 7.7x P/E and a 13.1% Free Cash Flow Yield:

| IMB Net Income, Cash Flow & Valuation (FY18-22) NB. Cash flows not adjusted for sale of Premium Cigars. |

{kind=link}

IMB stock also has a Dividend Yield of 7.0%, based on its FY22 dividend of 141.17p (1.5% higher year-on-year). IMB announced a new £1bn share buyback program in October and expects to complete it by FY23 year-end. The £1bn amount is equivalent to 5.2% of the current market capitalization.

While these figures may sound superficially attractive, we do not believe they sufficiently compensate for IMB's structural risks.

In addition, Altria and BAT offer similar (or even cheaper) valuations, depending on the metric used, and much fewer structural risks.

- Altria has a higher Dividend Yield of 7.7% (based on an annual dividend of $3.76) and a 9.7x P/E, while BAT has a similar P/E of 8.4x and a Dividend Yield of 7.4% (based on FY22 dividend of 230.9p).

- Altria's U.S. business is likely much more defensible (due to lower cigarette prices and tough FDA regulations against new products), while BAT also generates 50% of its earnings from the U.S. and has the second-best Reduced Risks Products portfolio after Philip Morris.

Both Altria and BAT remain Buy-rated in our coverage, as does Philip Morris.

Is Imperial Brands a Buy? Conclusion

We reiterate our Hold rating on Imperial Brands, meaning the stock should be avoided.

For further details see:

Imperial Brands: Troubling Read-Across From Peers' Q4 Results