IMPP - Imperial Petroleum Makes Massive Profits But Are Those For All Shareholders?

2023-04-03 01:41:16 ET

Summary

- Imperial Petroleum was a spin-off from StealthGas Inc.

- IMPP is currently extremely undervalued.

- However, I don't think the value will ever get unlocked due to the different incentive structure between shareholders and the CEO.

Introduction

Imperial Petroleum Inc. (IMPP) is an extremely undervalued stock from the current perspective. It operates in one of the most cyclical industries, and the oil tankers are enjoying record profits not seen in the past 25 years.

However, it is also a story about dilution, financial engineering, leverage, and, most importantly, conflict of interest, which leads to different incentives between the CEO and the rest of the shareholders.

Since the spin-off, there has been a massive share count increase. As they haven't published FY 2022 20-F filing yet, I scrolled through 100+ SEC filings since the spin-off to get an understanding of what happened with all the crazy dilution, different share classes, and warrants.

Total share count after the spin-off:

4,775,272 common shares.

795,878 - 8.75% Series A convertible redeemable perpetual preferred shares at a liquidation value of $25 per share.

Total share count at the time of writing this article:

193,111,176 common shares.

795,878 - 8.75% Series A convertible redeemable perpetual preferred shares at a liquidation value of $25 per share.

16,000 shares of series B preferred stock (granting the CEO 25,000 votes for each share, limited to a maximum of 49.99% of voting control.)

13,875 C convertible perpetual preferred shares with a liquidation preference of $1,000 per share. Entitle to 5% annual dividend into perpetuity and entitled to conversion with a lower of the following price; past 10 days volume weighted average share price but at most $0.50 per share but not lower than $0.10 per share. Thus if converted total share count will increase between 27,750,000 to 138,750,000.

78,278,862 warrants at an exercise price of $0.55 per share.

2,090,909 warrants at an exercise price of $0.6875 per share.

31,150,000 warrants at an exercise price of $0.80 per share.

43,000 warrants at an exercise price of $1.25 per share.

552,000 warrants at an exercise price of $1.375 per share.

11,802,000 warrants at an exercise price of $1.60 per share.

1,725,000 warrants at an exercise price of $2.00 per share.

To SUM up everything, the share count increased by 3,944%, and the C convertible preferred shares could be converted into common stock to increase the share count by an additional 14% to 72%. The CEO was also granted special voting shares to control 49.99% of the voting power, and 78 million warrants are outstanding at a conversion price of $0.55 per share to limit any upside potential.

In total, IMPP raised net proceeds of $157 million. $11 million went into stock issuance fees, and a total of $49 million were given in discounts compared to the closing stock prices during issuances. It looked like IMPP needed to offer a greater discount at every capital raise round in order to get the capital.

Look at the incentives

Why has IMPP done such destructive share dilution? Well, if you look at the incentives, you'll understand. Two affiliated companies are owned by the CEO, Stealth Maritime, which does their fleet management, and Brave Maritime, from where they acquired some of their recent ships.

{kind=link}

The CEO's ownership has fallen from 18.6% during the spin-off to only 0.5%, worth less than $200,000.

{kind=link}

Compare that to the approximately $250,000 + 1.25% of revenues his fleet management company receives annually from a single ship. Depending on the market situation, the CEO's fleet management company earns $320,000 - $450,000 for each vessel. With 10 ships fleet, that is $3.2 to $4.5 million. With 30 ships fleet, that is $9.6 to $13.5 million in annual revenues.

In my opinion the incentive structure is tilted toward growing the fleet at the cost of IMPP shareholders' returns.

In the latest ship acquisition, IMPP bought ships from the CEO's owned company Brave Maritime, partly paid by series C convertible shares that pay a guaranteed dividend and, on top of that, can be converted into common stock at extremely dilutive conditions.

Industry analysis

I looked at a few of their competitors to see the current situation in the industry.

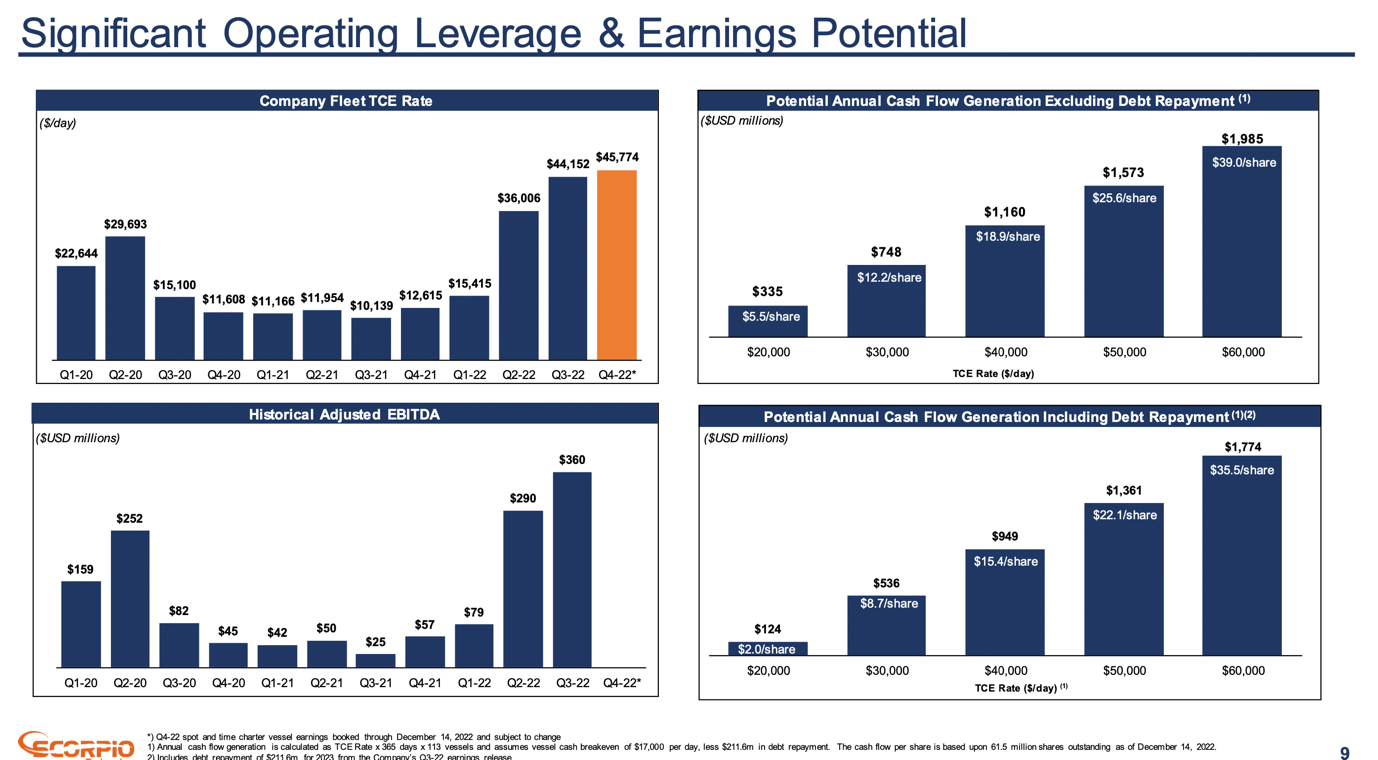

Scorpio Tankers (NYSE: STNG ) is cash flow break even at just over $10,000 TCE rates. Also, their fleet is slightly newer, with an average age of around 7-8 years. Currently, the rates are above $40,000 , so everyone is making massive profits. The question is, just how long do the rates stay at these levels?

Scorpio Tankers Q4 2022 presentation

{kind=link}

The shipping industry is extremely cyclical. In normal times shipping companies either make tiny profits or lose money. Usually, every 5 to 10 years, there will be some shock in the market, which makes the shipping rates go crazy, and during those times, all of the profits are made to cover the previous losses and to reward shareholders.

Unfortunately, the long-term data seems to be behind a paywall on every site, so I can't see the historical average TCE rate. However, since 1997 the TCE has never been this high.

Investing in the shipping industry is not something to put your money in and then forget. When things look good, it's usually a wise time to exit your investment. Otherwise, you might get burned, as many investors did in 2008.

{kind=link}

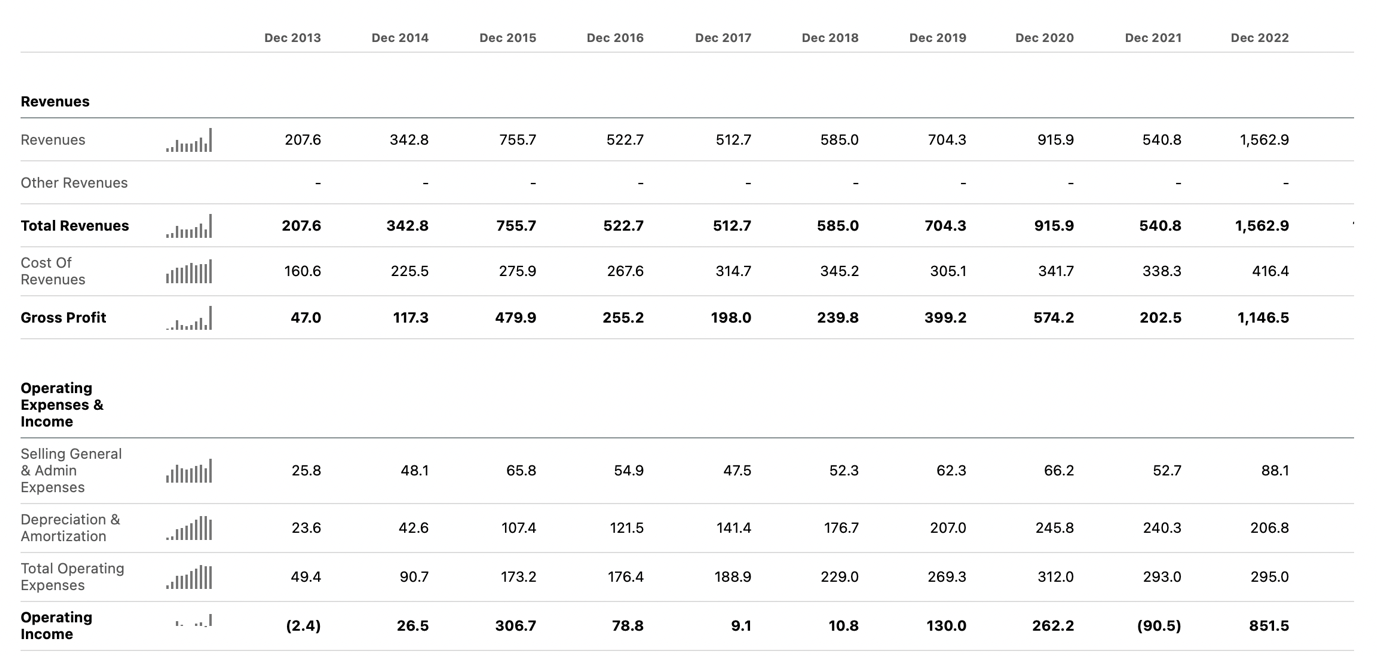

Scorpio Tankers' financials show that 2015, 2020, and 2022 were exceptional years, but in normal years they are either losing money or, at best, making small profits.

{kind=link}

{kind=link}

Over the past 10 years, they made a total of $6,650 million in revenues and $362 million in net income, leading to a profit margin of 5% over the past decade or in other words, they lost almost $300 million in 9 years and then covered the loss and made some profits in 2022.

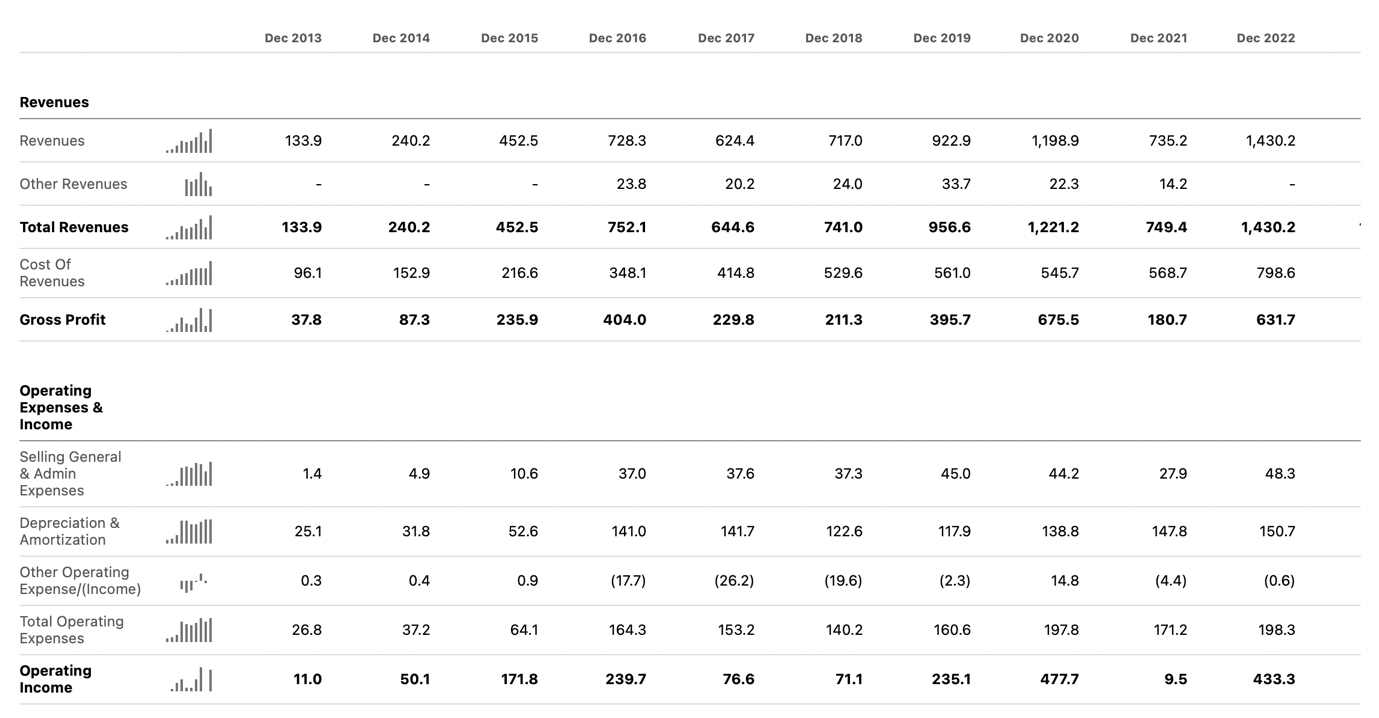

Another competitor's Frontline's (NYSE: FRO ) financials are similar.

{kind=link}

{kind=link}

Total revenues were $7,184 million, and net income was $1,231 million leading to a total net income margin of 17%. Frontline does have a more modern fleet which could explain their better profitability during down markets. Maybe some long-term contracts also make the difference there. I would have to dig deeper to figure out what makes the difference between these companies, but the point is that the industry is extremely cyclical, and on average, profit margins are quite low. Keep in mind that 2022 was the most profitable year for oil tankers over the past 25 years.

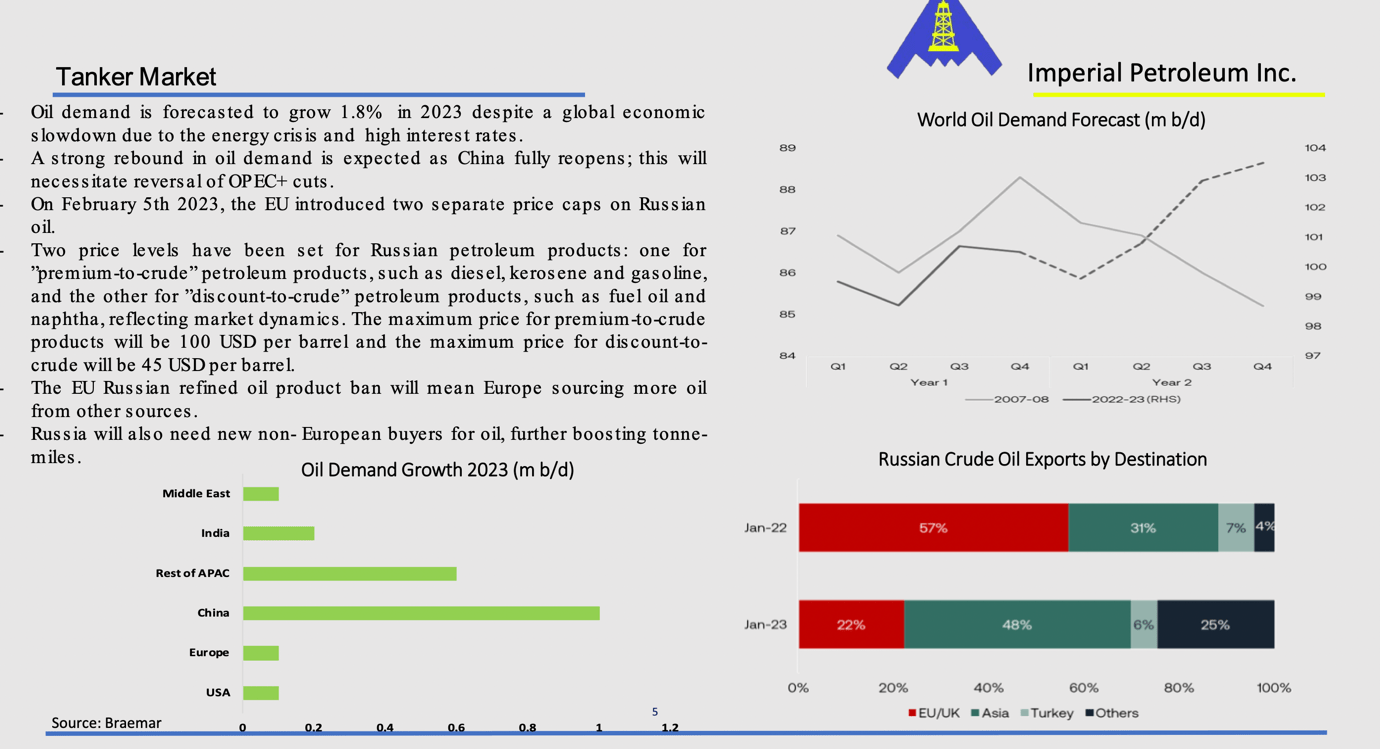

However, there is the potential for a longer oil tanker bull market. The IMPP's investor presentation SUMS it all quite well. The EU's oil sanctions against Russia will increase tonne-miles significantly as the Russian oil goes more towards places like Asia. Also, the newbuilds are still low, and the construction time is between 1 to 2 years. The currently hot market doesn't incentivize new investments as the long-term outlook for oil tankers isn't that great, and the new builds most likely couldn't even benefit from the currently elevated TCE rates in 2024-2025.

{kind=link}

IMPP's current value?

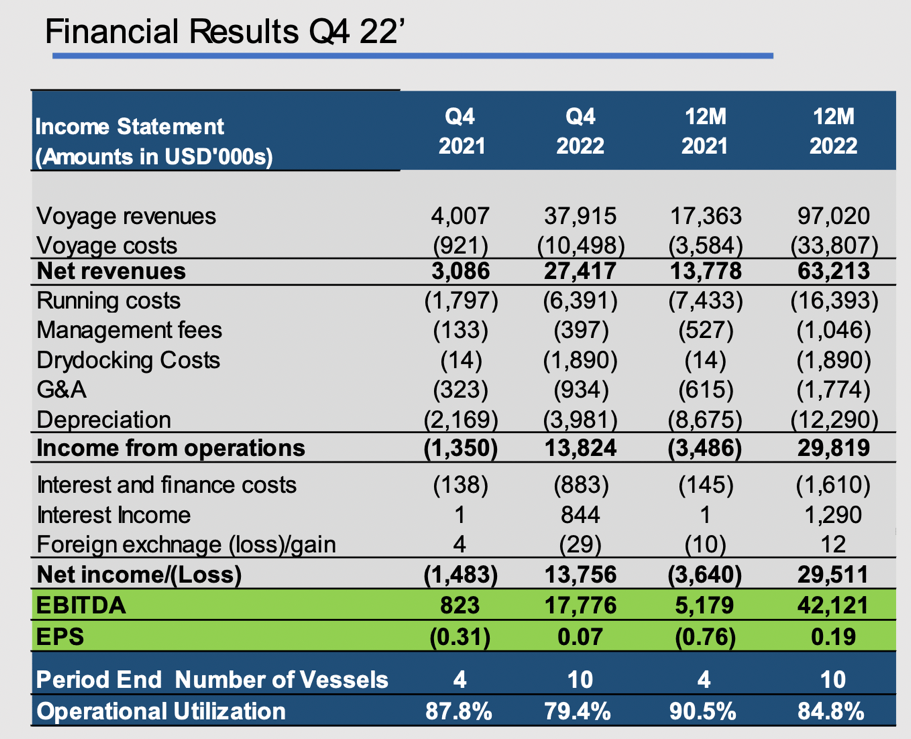

In Q4, daily TCE was $33,600. Two of their ships were not operational due to dry docking, so 8 ships made net revenues of $27.4 million. Expenses excluding 100% of the drydocking and including only 80 % of the G&A and depreciation were $10.7 million. The ships operate at a breakeven level before interest expense at $13,100 daily TCE.

{kind=link}

As long as TCE stays at these elevated levels, they'll make about $20 million in quarterly profits or 50% of the market cap. Even if there was a 40% dilution from convertible C shares, IMPP's quarterly earnings still make about a 30% yield for diluted market cap.

{kind=link}

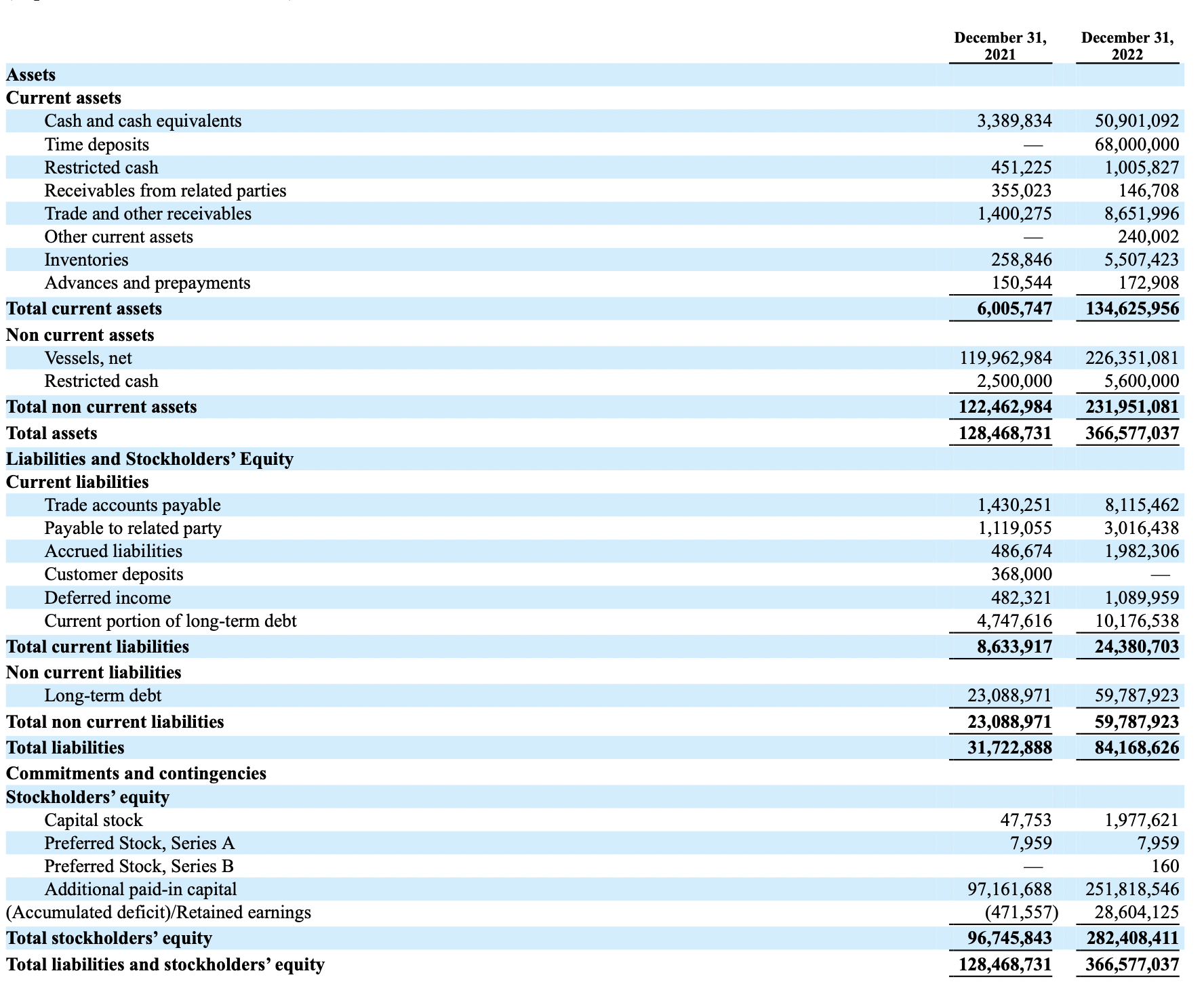

Total current assets + non-current restricted cash is $140 million. Total liabilities are $84 million. Then you'll have to deduct the series A and C convertible notes, as those are practically debt-like instruments but not shown on the liabilities side on the balance sheet as those are equity-accounted items. So, the combined liquidation value of A and C convertibles is $34 million. So adjusted net cash on the balance sheet is $22 million. Not as much as first indicated, but still, more than 50% of the market cap is in net cash, and on top of that, they own 10 ships with an accounting value of $226 million. Looks ridiculously cheap.

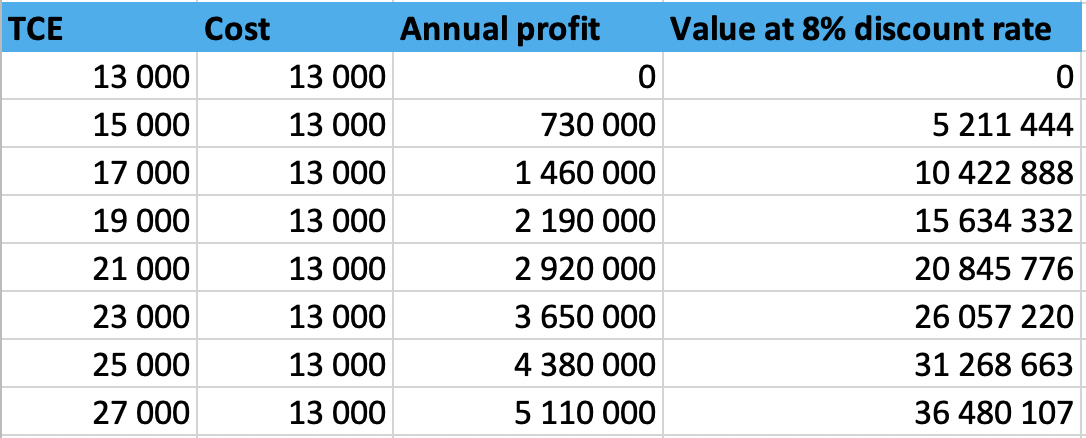

Currently, the average age of the fleet is 14 years. Assuming 11 years of economic life left, I made an earnings model with an 8% discount rate to see their fleet's expected value based on different TCE rates.

{kind=link}

Based on minor changes in TCE rates, the fleet value changes drastically (note: the table shows a single ship value, so the entire fleet value is 10x that amount). Nobody knows what the TCE will be over time.

Problems

The problem is that IMPP keeps leveraging its balance sheet and acquiring new ships during an extremely hot market. In the Q4 earnings call, the CEO said they want to grow the fleet size from the current 10 ships to 20 or 30, while old oil tanker prices have doubled in a year . So, when the CEO keeps leveraging the balance sheet by acquiring more tankers during a market peak when valuations are sky-high, what happens when the market turns around?

Just imagine if they leverage the balance sheet by $400 million over the next year and after the tanker market tanks and valuations fall by 50%. There goes all of the shareholders' wealth.

When asked about doing buybacks, the CEO stated that they won't do any as they focus on expanding the fleet. So instead of buying back their own stock at something of 0.15 book value, they are acquiring more ships with likely hefty margins above the book values.

Conclusion

The company is currently extremely undervalued, and if the CEO's incentives were aligned with shareholders' interests, it would be a screaming buy. The rational thing would be to stop buying new ships during the hot market and instead use the cash for buybacks until the stock price returns between $1-$2 per share.

However, in my opinion, the purpose of this company does not seem to be serving the shareholders but rather to benefit the CEO's affiliated companies. If the TCE rates stay at these levels over at least one, but probably the next two years, then the newly purchased fleet will make enough profits to compensate for the current extremely expensive purchase prices. However, if the TCE rates normalize before that, the company will be stuck with extremely high debt levels, and there will be no return. You will lose if you pay 2x more than the competition from a thing that generates the same amount of revenue in a low-margin environment. It will be a game over for the current equity holders, who will get wiped out slowly.

Additionally, there is the upcoming potential dilution from C preferred shares, and as IMPP will keep raising additional capital for new fleet acquisition, I doubt there will be any fool enough investors left to whom they could raise capital against pure equity even by giving huge discounts. So going forward, there will likely be more preferred share issuances with guaranteed dividend yields and other nasty special conditions, making future equity raises even worse for existing shareholders. For example, the latest ship acquisition was made partly by guaranteed 5% dividend-yielding preference shares. Those instruments are also great at leveraging the balance sheet even further than what would normally be possible, as the preference shares pay guaranteed dividends but act like equity. So practically, they can use those instruments to acquire new ships with 100% leverage.

In my opinion, the only hope for this company would have been some activist investor taking it over and firing the current board and CEO. Sadly, that is no longer possible as the board granted the CEO special voting shares with 49.99% voting power.

So while there is definitely value at the moment, the value won't be distributed to shareholders in the foreseeable future. If you believe that after leveraging the balance sheet to 30 ships fleet and the TCE rates normalize, the company will still be in a healthy position with positive cash flow potential and high equity per share balance left, and the CEO, for some reason, finally starts rewarding shareholders' instead of building the fleet, it could be a good investment. I just don't think it is going to happen. So far, based on the previous actions and current incentive structures, I think all of the existing shareholders' wealth you see on the balance sheet will get destroyed over time.

For further details see:

Imperial Petroleum Makes Massive Profits But Are Those For All Shareholders?