HZNP - Improved Outlook For Horizon Therapeutics And Amgen

2023-08-16 14:31:30 ET

Summary

- Horizon Therapeutics reports better-than-expected Q2 results, easing concerns about the Amgen acquisition failing to close due to Horizon's business underperformance.

- Net sales of Tepezza have been a key issue, but positive label changes and phase 4 results are expected to drive demand, and the major headwinds are now behind.

- Krystexxa and Uplizna continue to show strong growth, adding value to the acquisition.

Horizon Therapeutics ( HZNP ) reported upbeat Q2 results , exceeding the revenue consensus by $71 million and reducing the fear of the Amgen ( AMGN ) acquisition not going through due to the worse-than-expected business performance since the deal was announced in December 2022.

The two key issues since the deal was announced were the pushback from the FTC and the decline in net sales of Tepezza since the deal was announced.

It seems more or less clear that the FTC does not have a case against this acquisition given the lack of overlap in therapeutic areas, but the lawsuit the FTC filed did result in a delayed expected closing date. Amgen has made it clear that it expects the deal to close by mid-December and it also said that their repeated attempts at engaging with the FTC have gone unanswered .

In this article, I will focus on the operational performance of Horizon since the acquisition was made, and primarily the second quarter results and the growth outlook for Tepezza which remains Horizon’s key asset and the primary reason for the $28 billion price tag.

Improved outlook for Horizon and Tepezza after Q2 results

Net sales of Tepezza flatlined last year and started to decline Y/Y in Q3 2022. As mentioned, this has contributed to concerns about the deal going through as it was thought Amgen could use FTC pushback as an excuse to back out of the deal (and pay a $974 million breakup fee to Horizon).

Horizon Therapeutics earnings reports

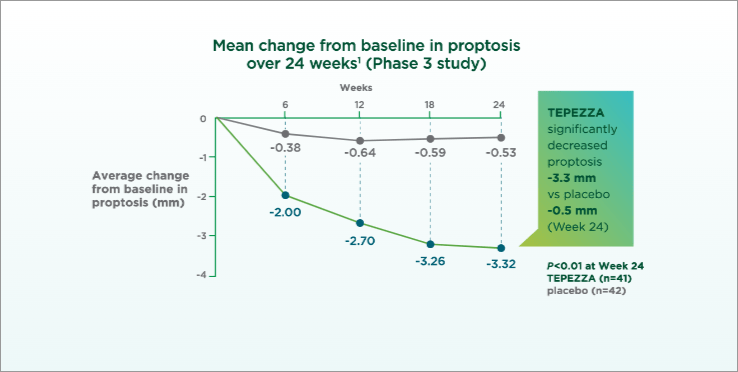

Horizon did make positive comments about the demand for Tepezza after the first quarter report, as the company secured a label change for Tepezza that now allows the treatment of thyroid eye disease (‘TED’) patients regardless of disease duration and severity and it also reported positive phase 4 results of Tepezza in chronic TED patients in the second quarter. The label change and the positive phase 4 results are both meant to drive demand in the chronic TED population and to improve reimbursement for these patients as Horizon has seen pushback from payers due to the lack of clinical data supporting the use in this population (Tepezza was only studied in active TED patients in phase 2 and phase 3 trials).

However, there was also another recent label change for Tepezza with a more pronounced warning added to the label for hearing impairment and a warning of increased severity compared to the clinical trials of Tepezza. This label change added to the concerns about Tepezza’s growth ahead of Q2 results. The risk-benefit profile of Tepezza still seems heavily on the benefit side and this is a known side effect that resolves in the majority of patients receiving Tepezza.

There is still not a determined treatment protocol for hearing loss caused by Tepezza, but that does not mean there will not be such a protocol going forward. This case report shows that prompt treatment with oral prednisone led to complete resolution and that the patient managed to complete the whole 8-infusion course of Tepezza. This is just one case and it is entirely possible that it would have resolved on its own, but provides an idea and potential option for patients with hearing impairment side effects.

Even if this side effect was known and well described, that has not stopped the lawsuits against Horizon from mounting in the last few quarters. I expect the lawsuits to go nowhere, but it is still a nuisance for Horizon and it eventually will be for Amgen if and when it completes the acquisition.

One of the actual reasons for the decline in Tepezza sales in the last few quarters is significantly reduced compliance because it is widely believed that the last 2-3 infusions add no benefit to TED patients. Even the clinical data support this belief – there was a very modest benefit from week 18 to week 24 in the phase 3 trial and there was even slight worsening in the phase 2 trial.

{kind=link}

New England Journal of Medicine, publication of Tepezza's phase 2 results in TED patients

And patients receiving an average of 4-5 infusions versus 7-8 makes a big difference for quarterly sales. If we take seven infusions as the average at launch and then reduce it to five over the course of the last several quarters, the net revenue per patient would drop nearly 30%. It is more than likely that this is the key driver of reduced sales that took time to flow through the quarterly sales updates.

The second reason was the payer pushback for chronic TED patients and this too caused lower demand for Tepezza, or at least a much longer and more difficult process of obtaining reimbursement for each chronic TED patient.

And lastly, the prioritization of production of COVID-19 vaccines caused a supply disruption for Tepezza in Q1 2021, and the subsequent surge in net sales in Q3 2021 and Q4 2021 was driven by the bolus of patients who were prescribed Tepezza in Q1 and Q2 but only started to receive infusions in the second half of 2021. This bolus made the launch trajectory better than it actually was in the second half of 2022 and management did warn of this phenomenon at the time.

All this brings us to the Q2 report where Horizon reported that net sales increased to $446 million from $405 million in Q1. This was still down 7% compared to the same quarter in 2022, but a significant sequential improvement and an improvement from 20%, 16%, and 19% Y/Y declines in the previous three quarters, and delivers the initial proof of Tepezza’s recovery. I believe that the above-mentioned headwind of reduced average infusions per patient is largely reflected in the Q2 numbers and that it will at the very least be far less of a headwind going forward or not a headwind at all.

And the reimbursement challenges should be addressed by the label change and the positive phase 4 data in chronic TED patients. Horizon has already started to leverage both the label change and the phase 4 data and the company said in the Q2 earnings report that it has obtained favorable policy changes for greater than 20% of U.S. covered lives and that this will take effect in the second half of 2023 and especially in 2024.

Based on the evidence we have today, I believe Tepezza’s quarterly sales have bottomed in the first quarter of 2023 at $405 million and that it will likely return to Y/Y growth before 2023 is over and to double-digit growth in 2024 and beyond. And starting in 2025, we should see contributions from non-U.S. territories and this will help drive sales to new highs in 2025 and the following years, although I do expect disruption from competitors starting in 2026 – primarily from other IGF-1R drugs that share the mechanism with Tepezza, and the companies that are the most advanced in this area - Viridian Therapeutics ( VRDN ), and Acelyrin ( SLRN ).

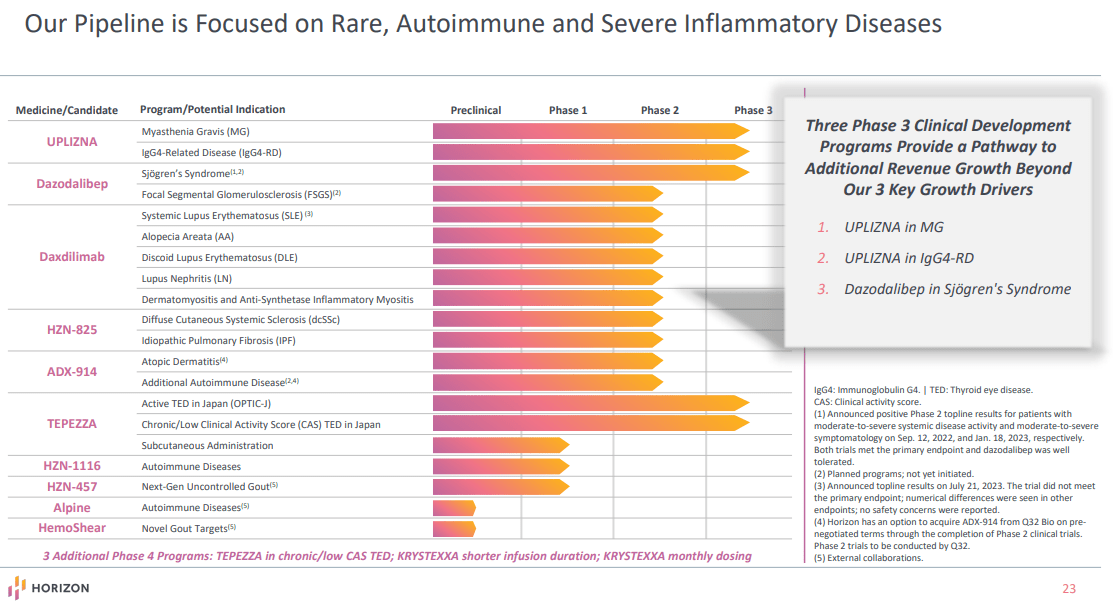

Krystexxa, Uplizna, and the pipeline – the acquisition is not just about Tepezza

Krystexxa had an excellent second quarter and the first half of the year. Q2 net sales rose 46% Y/Y to $244 million and it is now a matter of time before it becomes a blockbuster product. These are fascinating growth rates for a 13-year-old product and the renewed growth phase was driven by the label expansion to include combination treatment with immunomodulators that significantly increase Krystexxa’s response rate compared to Krystexxa monotherapy. I continue to see Krystexxa as at least a $1.5 billion a year product at peak, and potentially a $2 billion+ product for Amgen later this decade.

Horizon Therapeutics earnings reports

Uplizna net sales continue to grow rapidly and it should soon become Horizon’s third largest product ahead of Ravicti. Net sales rose 76% Y/Y to $68 million and Uplizna could exceed my $500-$600 million peak sales estimate range in NMOSD. There are also two additional shots on goal for Uplizna with two phase 3 readouts expected in 2024 – IgG4-related disease and generalized myasthenia gravis. If successful in one or both trials, Uplizna could become a $1.5 billion to $2 billion a year product before the end of the decade.

Horizon Therapeutics earnings reports

The rest of the pipeline can also deliver significant value for Amgen later this decade, but the risk of that not happening is much higher than for the already approved and proven products such as Krystexxa and Uplizna.

{kind=link}

Amgen remains enthusiastic about the acquisition

Amgen still sounded optimistic about the acquisition of Horizon on the Q2 earnings call . In his prepared remarks, Amgen's Chairman and CEO Bob Bradway said the following:

Turning to our planned acquisition of Horizon Therapeutics, we remain very enthusiastic about what our companies can achieve together for patients suffering from rare serious diseases. Horizon has certainly accomplished a great deal as an independent company. Amgen’s global commercial manufacturing and R&D capabilities, especially for biologic products, will enable Horizon’s medicines to reach even more patients more quickly than Horizon could have achieved on its own.

When asked about Tepezza and its recent underperformance and how they see the growth outlook, Bradway responded:

Let me just reiterate that we remain very excited and of course, we’re watching carefully developments in the marketplace and talking as appropriate with our friends at Horizon about that. And again based on our view of the clinical data and our view of the international opportunities and ability to expand the reach of the product, we’re very excited about what we think we can do there.

And finally, when Evercore ISI's Umer Raffat asked about Tepezza "falling dramatically short" of expectations, Murdo Gordon, Amgen's EVP of Global Commercial Operations said:

We remain enthusiastic about proceeding on the basis of the deal that we announced. I would take issue at least with our perspective is different from what was implicit in your question, but we’ll leave that for another day.

After Horizon's second-quarter results and Tepezza's improved outlook, I believe they actually meant what they said, and absent a significant deterioration in the growth outlook for Tepezza relative to current expectations, it seems unlikely that Amgen would want to get out of this deal.

Conclusion

While I no longer believe Amgen paid less than Horizon was worth because of a worse-than-expected outlook for Tepezza compared to my expectations back in December 2022 , I still think it is getting a good deal by acquiring it, especially now that it is more likely that Tepezza sales are about to recover and as Krystexxa and Uplizna continue to deliver exceptional growth.

I do not do arbitrage and am neutral on Horizon after closing my position in early January.

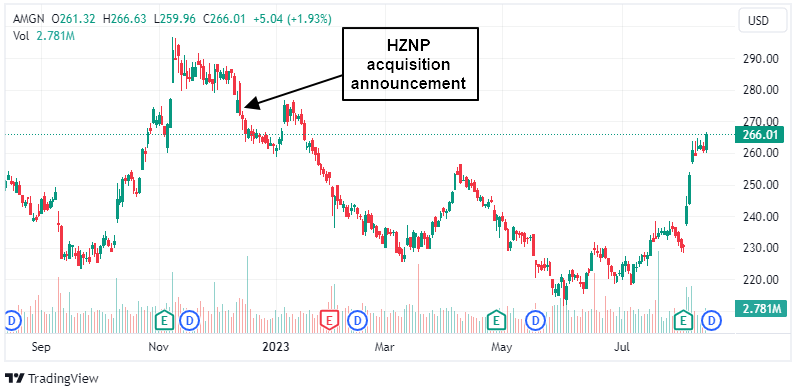

Amgen, on the other hand, is now seemingly out of the penalty box. The stock lost nearly a quarter of its value since the December 2022 acquisition announcement through late May, but it has since recovered and sits just slightly below the pre-deal levels. The upbeat second-quarter report has helped improve investor sentiment, and perhaps the much better-than-expected Q2 report by Horizon.

{kind=link}

The acquisition of Horizon should boost Amgen's revenue growth, earnings, and cash flows in 2024, and Horizon's pipeline should add potentially significant growth drivers toward the end of the decade.

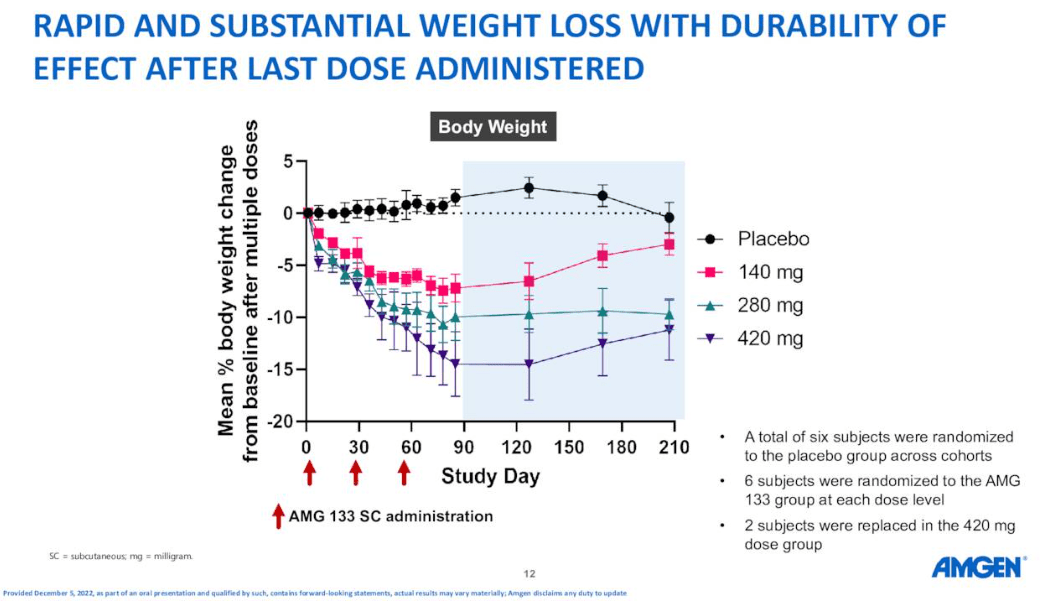

Longer-term, Amgen has some potentially significant growth drivers in its existing pipeline, including a potentially very valuable shot on goal in the rapidly growing obesity market through maridebart cafraglutide (formerly AMG133) with a potential advantage of being dosed once a month as a subcutaneous injection versus once-weekly administration of current market leaders semaglutide (brand names Ozempic for type 2 diabetes and Wegovy for obesity) and tirzepatide (brand name Mounjaro for type 2 diabetes and it is not yet approved for the treatment of obesity). Initial phase 2 results looked promising with significant weight reductions after only three months of treatment and which seemed durable four months after the last dose, at least for the two higher doses.

{kind=link}

Amgen also has a small molecule candidate AMG786 in a phase 1 trial for the treatment of obesity that is not incretin-based but the target is undisclosed.

Amgen's pipeline also includes various additional potentially high-value candidates, but also a biosimilar pipeline targeting several multi-billion blockbuster products - Eylea, Stelara, Opdivo, and Soliris.

Amgen is too big and growing too slowly to be considered a candidate for our model growth portfolio, but I see it as one of the better-positioned big biopharma companies in terms of potential shareholder value creation in the following years.

For further details see:

Improved Outlook For Horizon Therapeutics And Amgen