JNK - Income Opportunities Come Back In The Triple Dip

Summary

- The income market has gyrated widely this year in response to changing market conditions and Fed's stance.

- We discuss why we didn't chase the June-August rally and why we are now seeing value reemerge in this latest bout of weakness.

- We currently view selective decent-quality, shorter-maturity assets as more compelling given the relative moves in Treasury yields vs. credit spreads.

- If credit spreads move past their June peaks of around 6%, we expect to turn our focus to more credit-sensitive securities.

This article was first released to Systematic Income subscribers and free trials on Sep. 12.

The income market has gyrated widely this year in response to changes in the outlook on inflation and macro activity as well as the Fed's increasingly hawkish stance. In this article we discuss why we have remained on the sidelines during the most recent bounce and why we are starting to see attractive opportunities re-emerging in the income space. We also highlight the specific internal dynamics of the sell-off we are going through now and why some securities hold more appeal than others.

Why We Didn't Chase The June-August Rally

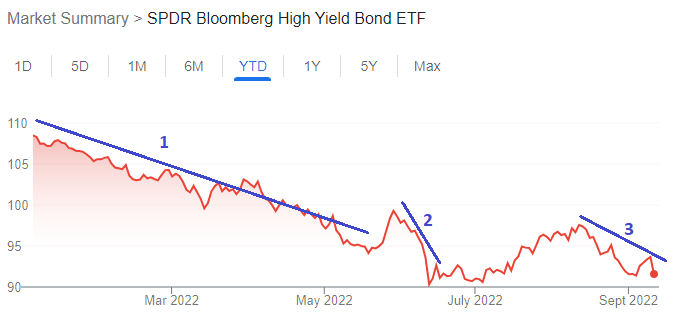

After bottoming in mid-June income assets rose over the next two months, faltering again around mid-August. Using the popular high-yield corporate bond benchmark SPDR Bloomberg High Yield Bond ETF ( JNK ) we can see this behavior in the following chart. This most recent sell-off marks the third sizable dip in the income space.

{kind=link}

Our view through the recent bounce has been not to chase the June-August bounce. This was due to a number of reasons.

First, valuations jumped very quickly off a previously attractive level in mid-June. High-yield corporate bond credit spreads, which are a good proxy for valuations across the broader credit market, tightened sharply from the middle of June of around 6% to a level where they offered little if any margin of safety for the deteriorating macro picture as well as an increasingly hawkish Fed.

Second is the general pattern that we don't tend to see a market recovery before the Fed stops hiking. The Fed has been very vocal that they will not only want to see a peak in inflation but also a significant drop closer to its actual target. With the Fed Funds rate miles away from its expected peak, the chances of the market having troughed has little historical support.

Three, leading indicators continued to deteriorate, painting a more difficult macro picture over the medium term.

{kind=link}

Re-Emerging Opportunities

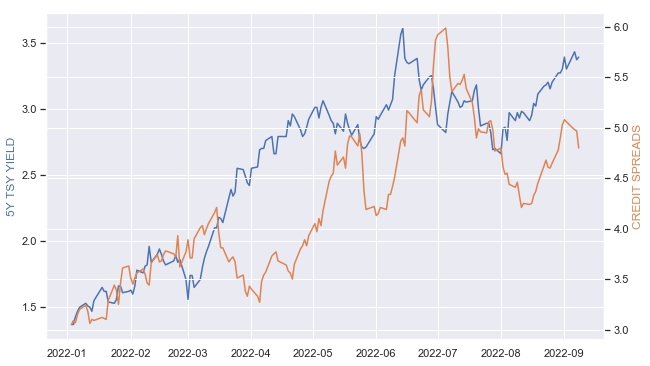

As with all market dips, not all sectors are impacted the same way. In this third dip what we have seen is that while Treasury yields have moved back to record or near-record highs of the year, credit spreads have not reacted as strongly. We can see this in the chart below showing 5Y Treasury Yields (blue line) versus high-yield corporate bond credit spreads (orange line).

{kind=link}

What this means is that we consider floating-rate and medium-maturity decent-quality assets more attractive and we would wait to pull the trigger on lower-quality / longer-duration assets simply because these assets would be more vulnerable to a back-up in credit spreads.

Given this market environment some of the securities that tick the box are the following.

The Janus Henderson B-BBB CLO ETF ( JBBB ) primarily allocates to floating-rate investment-grade CLO Debt (90% to BBB-rated CLOs). It has a distribution yield of 6.2% which has been growing this year and will continue to do. Only 0.5% of BBB-rated CLOs have defaulted between 1996 and 2020. By comparison the annual default rate for BBB-rated corporate bonds has been 0.3%.

Systematic Income Funds Tool

The Golub Capital BDC ( GBDC ) features a floating-rate middle-market loan profile. The company has a strong underwriting track record and features net realized gains over the last couple of years despite a clearly difficult macro environment that bookends this period. It trades at a 8.7% dividend yield and at a very attractive 9% discount to book value.

Systematic Income BDC Tool

The Angel Oak Financial Strategies Income Term Trust ( FINS ) holds primarily floating-rate investment-grade bank / financials bonds which has allowed it to strongly outperform the broader corporate bond CEF sectors as well as generate a higher level of income. It trades at a 8.1% current yield and a 11% discount.

Finally, we continue to see value in the Western Asset Mortgage Opportunity Fund ( DMO ) which primarily holds floating-rate non-agency mortgage securities. It does have a sub-investment-grade quality profile, however, it carries exposure to the household rather than corporate sector which is well-positioned both due to the still-strong labor market as well as high level of housing equity. It has outperformed the broader corporate CEF space this year. DMO trades at a 10.1% current yield and a 10.7% discount.

Takeaways

The rally from June to August that the income space has enjoyed has not lasted as asset prices have fallen back lower. In this latest sell-off Treasury yields have moved up much more than credit spreads. This is why we currently see more value in shorter-maturity / floating-rate assets that are less vulnerable to a potential back-up in credit spreads particularly as the Fed rate cycle has not yet run its course.

For further details see:

Income Opportunities Come Back In The Triple Dip