DUK - Increasing Debt Will Pressure Duke Energy's Valuation

2023-12-11 19:43:32 ET

Summary

- Duke Energy is approaching high debt levels that may reduce its ability to finance dividends.

- The company is further expected to increase its debt burden, leading to higher fixed costs.

- Duke is trading close to intrinsic value with an unjustified assumption of business as usual. My outlook is negative.

Duke Energy (NYSE: DUK ) is an electric utility company that generates, transmits, and distributes electricity to more than 7.5 million customers in the US. They own and sell over 50 thousand Megawatts of power, stemming from coal, nuclear, hydro, solar and wind sources.

Wall Street analysts have a “buy” rating on the stock with an average price target of $98. However, I see this as a result of a business as usual assumption, and I think that high leverage presents a risk factor that the market is neglecting and will come into play in 2024.

Few things threaten a regulated utility stock, and one of them is the mismanagement of debt. In this analysis I will evaluate Duke’s debt burden and present why the next few years may be tough for equity investors. The company is poised to increase its debt burden, which is on the edge on turning material for equity investors.

There are multiple challenges with Duke’s debt:

- Its increase over time

- New interest rates

- The higher portion of debt in its capital structure

I will elaborate on each point and present an intrinsic valuation for Duke at the end.

Debt Increase Over Time

Duke has some $79B in debt and a market cap around $73B, making its debt to capital ratio 52%. This is a highly levered company, which is not a problem of itself should the risk be sufficiently low and the cash available for interest payments high enough.

Duke's Capital Structure KPIs (Author, data from FMP)

In the picture above, we can see that Duke has a history of increasing leverage, while cash stays close to $300M. Duke’s EBIT is $6.7B and current interest payments are around $2.85B, reflecting an interest coverage ratio of 2.4x. This is roughly equivalent to a BBB/Baa2 synthetic credit rating.

Duke has -$2.6B in unlevered free cash flows which has been negative for quite some time, despite having a high $6.8B operating income (23% EBIT margin). This is likely why the company needs to continuously increase its debt load in order to pay around $3.2B in dividend commitments.

Interest Rates Will Get Harder to Service

While I believe that having a dividend is preferable as opposed to accumulating cash, I see a potential issue with the company sustaining its returns to equity investors. As we saw before, Duke may have difficulties financing dividends and needs to resort to using debt. However, the price of refinancing is not optimal and may get worse in the future.

Duke's Financing Obligations (Investor Presentation)

The interest rates on Duke’s debt range from 4.125% to 5.65%. These are past rates, and using a simple cost of debt calculator, I estimate that Duke will be able to refinance closer to a 6.2% pre-tax interest rate. Duke’s $79B debt is further expected to increase to $85B due to its infrastructure investments. The increase of $6B in debt may be financed at an average long term rate of 6.2%, which will gradually add $372M to the $2.845B interest expense, resulting in about $3.2B of future interest expenses. The key takeaway is that the fixed costs to the bottom line will increase.

As of June 30, 2023 Duke had $6B of outstanding liquidity available via debt and cash. This may start straining dividend payments after 1.9 years, and prompt the company to further increase debt. In the meantime, investors may become increasingly aware of Duke's dividend servicing pressures which is why I note 2024 as a negative catalyst for the stock.

While it is great to see a company investing in core assets, I’m not sure that Duke is moving at the right pace. Management seems to want to grow their infrastructure, but their growth may not be productive for shareholders, as I estimate a 4.7% ROIC: (NOPAT / (equity + net debt) = 5.8 / 128.2), while having around a 5.5% cost of capital. In my opinion, investors would rather see an improvement in asset efficiency, as opposed to cheaply financed growth.

Duke’s Leverage Increases Risk

As mentioned before, Duke’s debt to capital is around 52%. This is a high ratio because it increases interest obligations leaving less returns to equity investors.

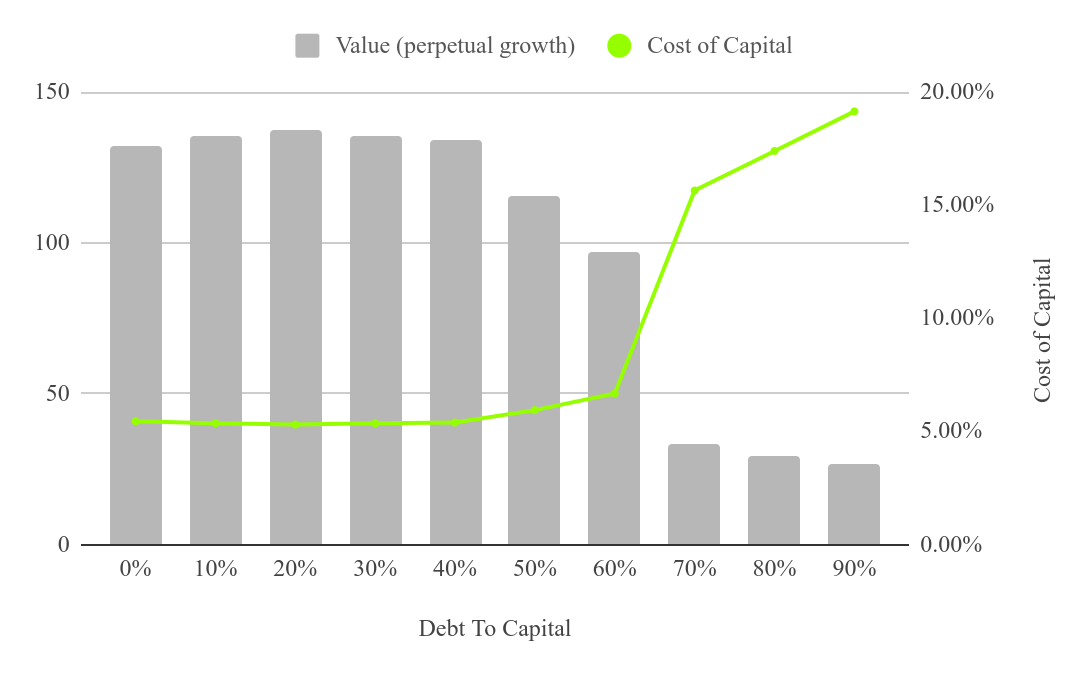

My optimal capital structure simulation strives to minimize the cost of capital for a company, which in turn maximizes value. In this model, I find that the optimal debt to capital for Duke is between 20% and 40%, while the company is currently close to increasing the risk from debt. Here is how the simulation changes the cost of capital at different leverage ratios:

Optimal Capital Structure for Duke (Author, data from FMP)

{kind=link}

We can see that the ideal spot is around 20%. However, after 50% the company may have to deal with increases in interest rates, beta, cost of debt & capital, and a possible credit downgrade.

Capital Structure Scenarios

For example, in a scenario with a debt to capital ratio of around 45%, Duke's cost of capital is around 5.5%. With free cash flows of $4.2B, the company's value comes out to $120B (calculated as 4.2 / (0.055 - 0.02)).

By reducing the debt to capital ratio to 20%, Duke gets a lower cost of capital of 5.3%. Using the same calculation, (4.2 / (0.053 - 0.02)) we get a value of $127B. This is the "optimal" version of the simulation.

If we flip to the other side, and lever up to 60% the company's picture changes. Interest coverage drops, possibly degrading credit rating below B2, increasing cost of capital to 6.7%. Now the value is $89.4B (4.2 / (0.067 - 0.02)), a -$38B difference from the optimal scenario. Note that this is a high-level simulation, using a single stage DCF.

The key takeaway here is that while finessing the capital structure may help investors, the risk lies in relying too much on leverage.

This is something that happened to highly levered companies like AT&T ( T ) and Verizon ( VZ ), where the risk of servicing debt was material to the stock price, and I estimate that Duke is in a similar trajectory.

Valuation

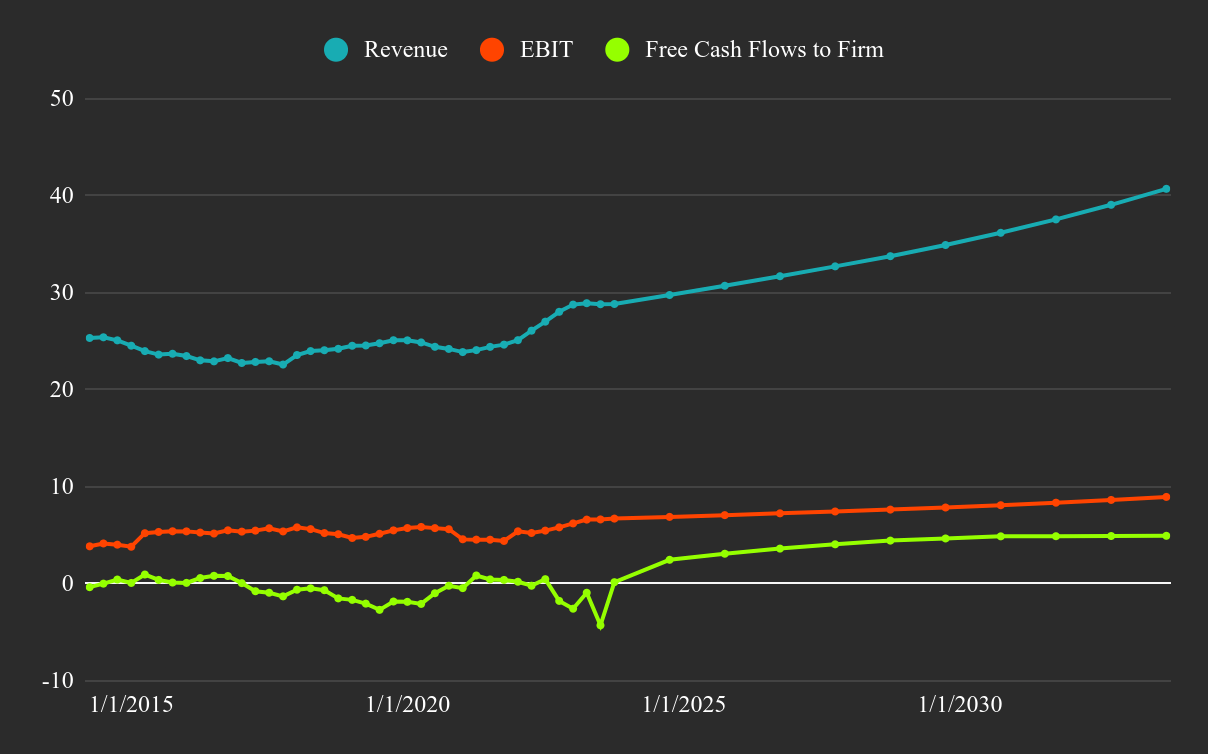

In my full valuation model, I expect Duke to make a cumulative $42B in unlevered free cash flows in the next 10 years. Given growing interest expenses of $3.2B and likewise dividends of $3.2B, Duke would need $64B of free cash flows to keep things stable.

Here is how I expect the company to perform in the future: I estimate a revenue growth around 4.3% in the next five years, and average free cash flows around $4.2B. By taking the future cash flows and discounting them at a cost of capital of 5.5% I get a present value of $142B. Finally, I clean up and net out debt to get an intrinsic value of $60B for Duke. This corresponds to an $78 value per share, or a 17% downside for the stock.

Valuation Forecast for Duke (Author, data from FMP)

{kind=link}

You can view and copy my full model and make your own scenario for Duke.

Risks To My Thesis

The counter argument to this hypothesis is that Duke is a play on interest rate cuts, i.e. a decrease of inflation. This could be net positive for the value of the company and future refinancing.

The company is also partnered with the government in reaching net 0 carbon emissions and supporting climate change goals, this may give them access to beneficial financing for capital projects.

The future capital projects may be technologically more advanced and result in a growth at a higher return on invested capital, outpacing the effects of debt.

The company may find ways to restructure, increase efficiency and improve the bottom line. Duke is also employing energy hedging, that is shielding the business from price shocks, and may realize gains from these activities.

Conclusion

I believe that the increase in leverage will create negative catalysts and the current dividends will be put into question, this may erode returns and investors may need to wait some time before Duke stabilizes. While the company has a great asset base and revenue generation, I see more negative scenarios than positive in the future. Wall Street seems to be assuming “business as usual”, however I don’t think this will last, and my outlook is negative.

For further details see:

Increasing Debt Will Pressure Duke Energy's Valuation