CSR - Independence Realty Trust: What's Not To Like?

2023-08-23 09:00:00 ET

Summary

- Apartment REITs have outperformed the Equity REIT Index but lag behind the Nasdaq 100 and S&P 500.

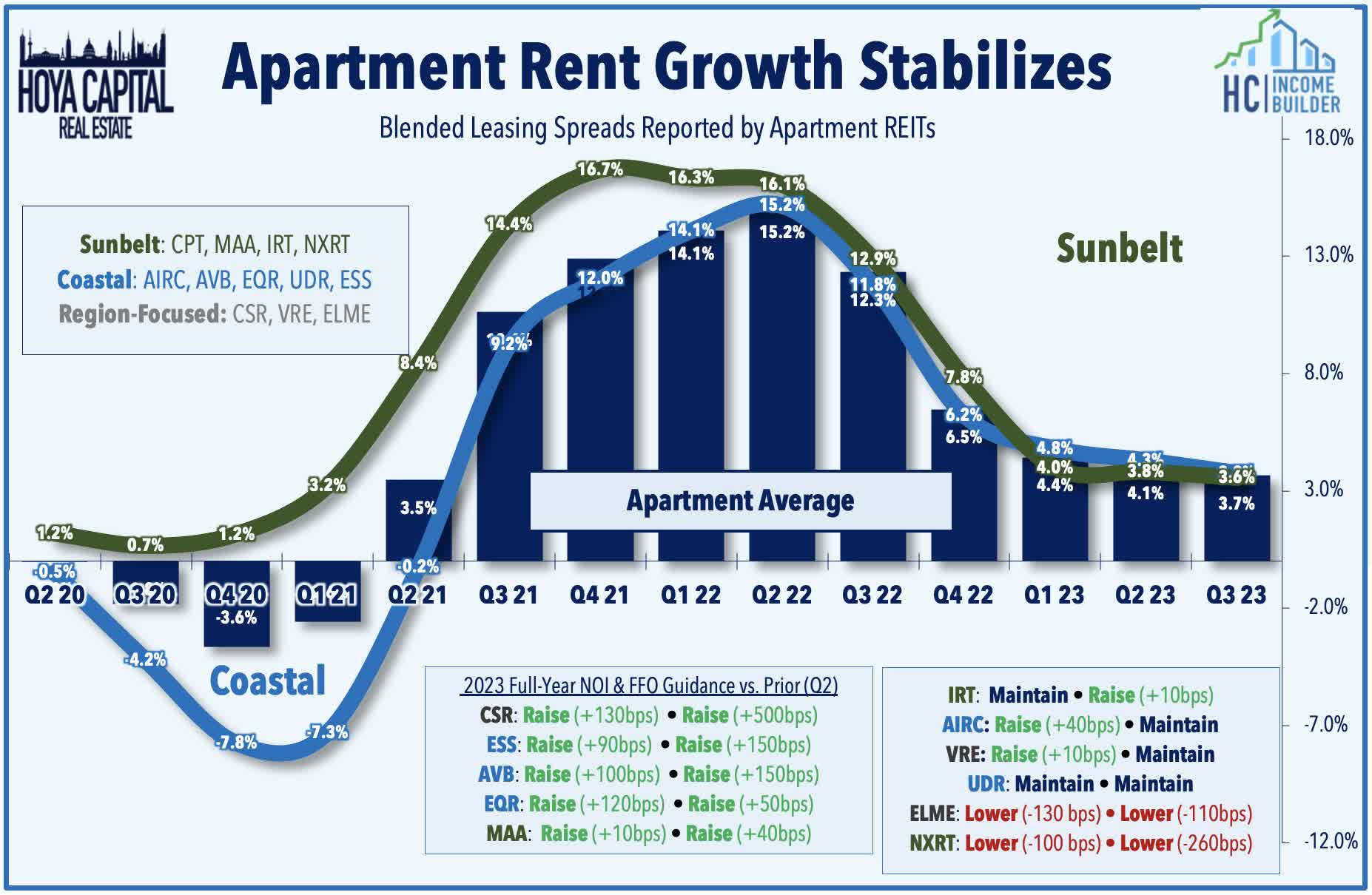

- Rent growth has stabilized slightly above inflation, defying expectations of negative growth.

- Apartment supply pressures are expected to ease by 2024 due to challenging financing for new development.

- Independence Realty Trust offers rapid growth, solid and safe dividends, and a surprisingly low price.

Apartment REITs as a whole have been the fifth-best performing of the 18 REIT sectors this year, outperforming the Equity REIT Index by a margin of 2.27% to (-3.37%), but badly lagging the Nasdaq 100 (36.66%) and the S&P 500 (14.88%).

Hoya Capital Income Builder

Apartment REITs turned in a strong Q2, however. Rent growth, which many analysts had expected to go negative, appears to have stabilized at a rate slightly faster than inflation.

{kind=link}

Six of the eleven Apartment REITs that provide full-year FFO guidance raised their full-year FFO outlook in reporting Q2 results, while eight of the eleven raised their same-store NOI expectations.

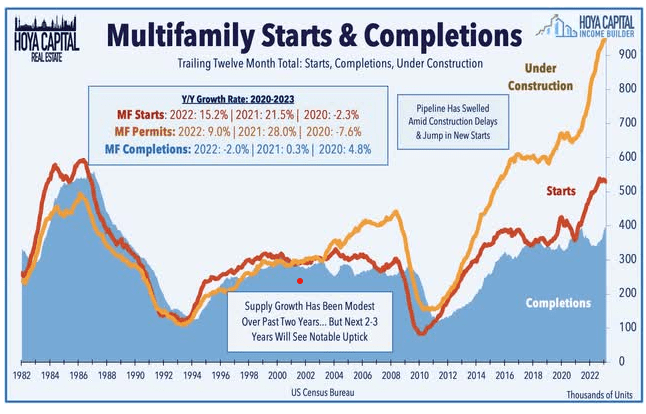

Soaring rents coming out of the pandemic sparked a wave of new development that will come to market over the next 18 months, but that new supply was offset almost completely by a matching decline in single-family supply. Thanks to longer completion timeframes created by labor and material shortages, this increased supply will likely have a more muted effect on rents.

{kind=link}

There was an overwhelming consensus on Q2 earnings calls that supply pressures will abate into 2024, given the extremely challenging financing environment for new development.

Looking more closely at the markets in which supply growth is largest, we see that for the most part, job growth in those markets is even stronger. Since job growth is the best predictor of apartment demand, it would appear that demand is outstripping supply.

Hoya Capital Income Builder

Meanwhile, Freddie Mac estimates that the U.S. housing market is still more than 3.8 million housing units short of what's needed to meet the country's demand.

Meet the Company

Independence Realty Trust

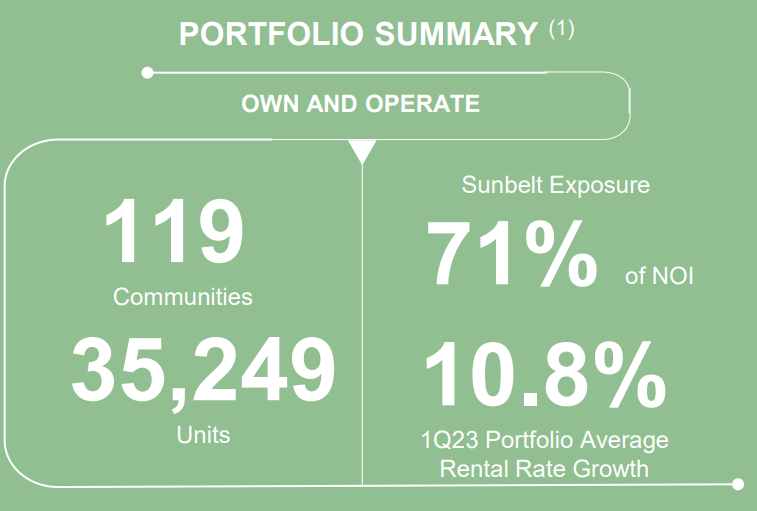

Headquartered in Philadelphia and founded in 2009, Independence Realty Trust (IRT) owns and operates nearly 120 apartment communities totaling over 35,000 units.

{kind=link}

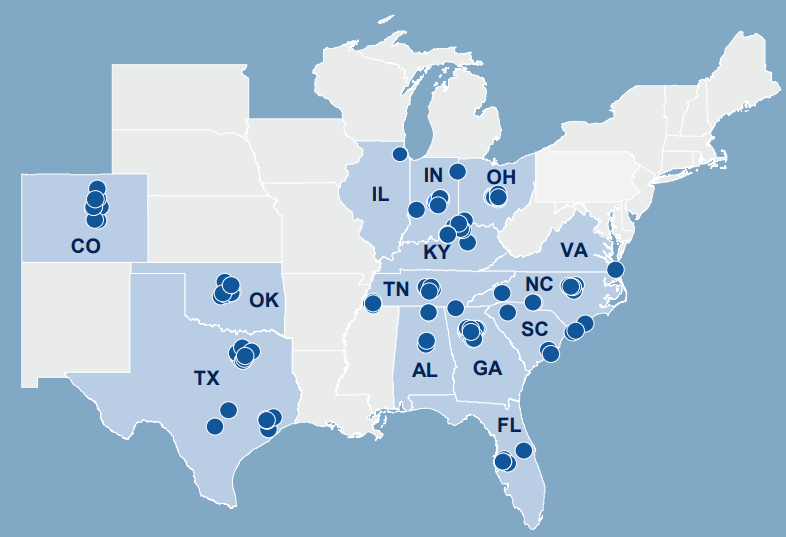

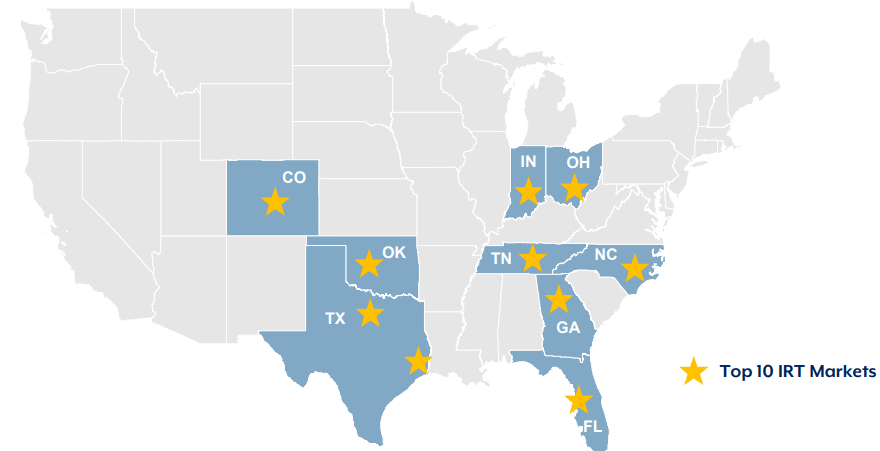

Of these, just over 70% are located in Sunbelt markets. The entire portfolio averaged 10.8% rental growth in Q1 2023, more than double the sector average.

{kind=link}

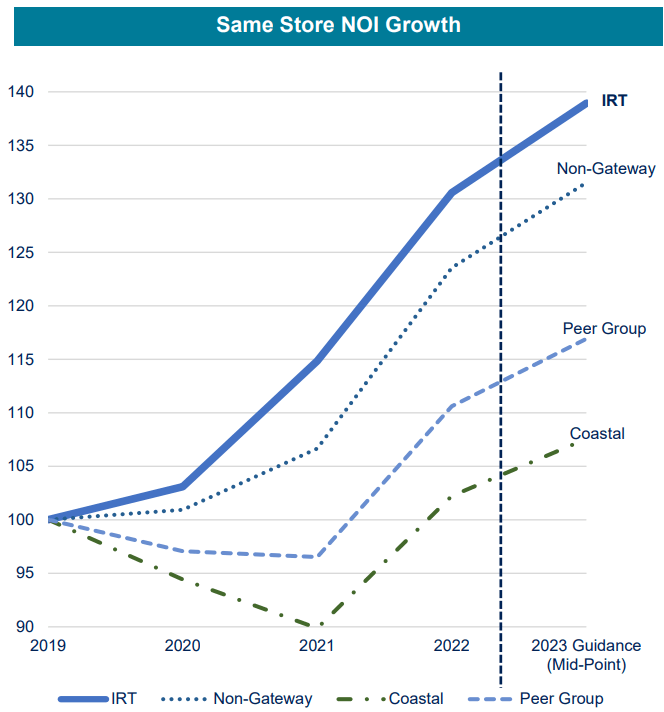

Since 2019, IRT has blown away its Coastal and Non-Gateway peer groups in same-store NOI growth. The Non-Gateway peer group includes Camden (CPT), Mid-America (MAA), Centerspace (CSR), and NexPoint (NXRT), while the Coastal peer group includes AvalonBay (AVB), Equity Residential (EQR), Essex (ESS), and UDR (UDR).

{kind=link}

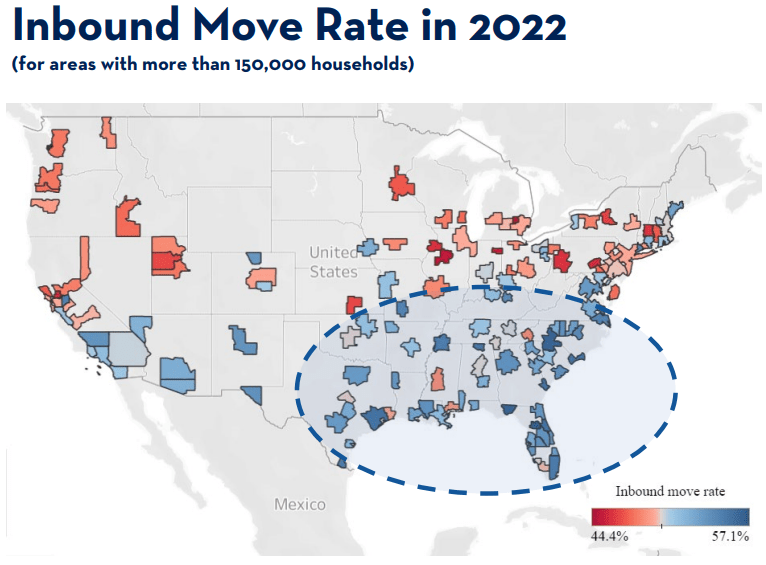

Americans have been on the move since 2020, with Sunbelt states experiencing the greatest influx of new residents, and 2022 continued that trend.

{kind=link}

In IRT's top 10 markets, the average age of residents is 37, and the average income is $86,809.

{kind=link}

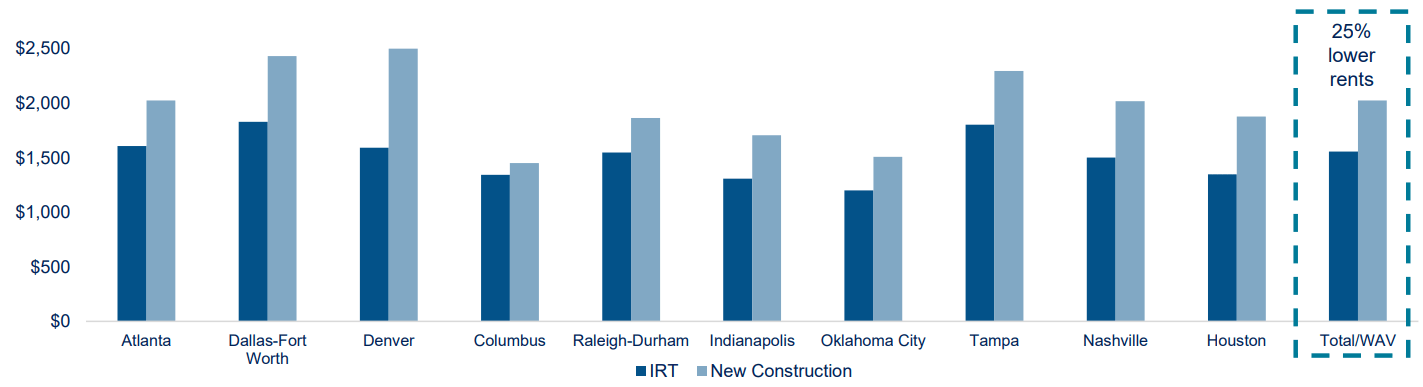

Meanwhile, the average IRT apartment rent is $1533 per month (about 25% lower than rents on newly constructed apartments in the same top 10 markets), which works out to a 21.2% rent-to-income ratio. These are not rent traps. Households can form capital to buy a home if they wish.

{kind=link}

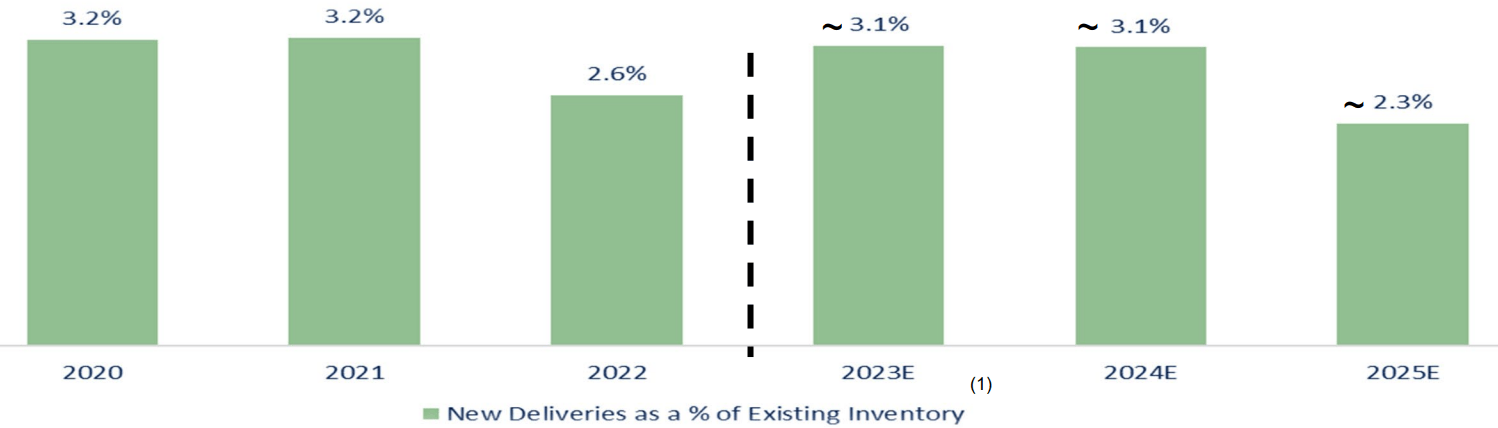

Estimated new deliveries of apartments for 2023 - 2025 in IRT's markets, as a percentage of existing inventory, are expected to be little changed. Thus, IRT is somewhat shielded from the specter of oversupply that troubles many analysts where Apartment REITs are concerned.

{kind=link}

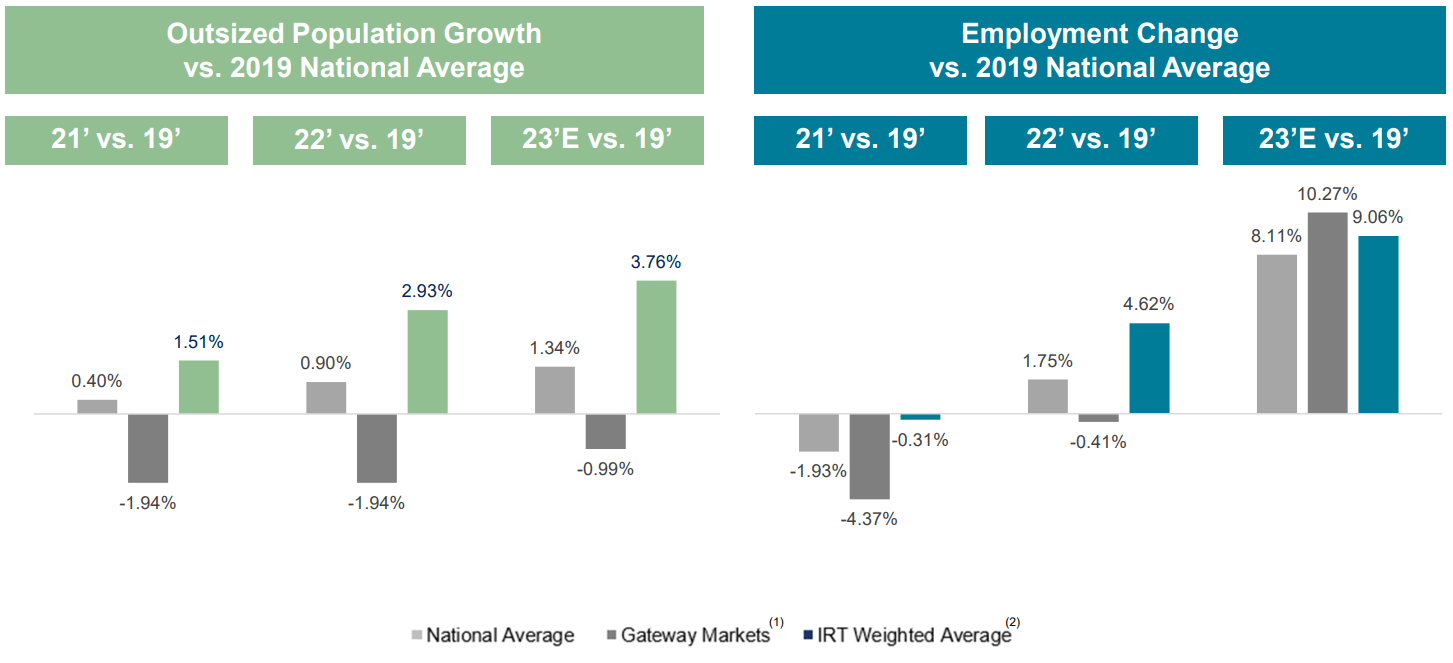

In addition, IRT's markets have seen faster growth in population and employment than the national average over the past 4 years.

{kind=link}

IRT relies mostly on Class B apartments, which do comparatively well in all economic conditions. Residents of Class A units move down to Class B when rent growth outstrips income, as in a recession, while Class C residents move up to Class B in good times, as their income grows.

IRT makes money 3 ways:

- More than half (approximately 19,000) of IRT's units are strong candidates for value-add renovations, which tend to be very profitable, generating returns in the neighborhood of 20%.

- The company also uses proceeds from dispositions to expand its presence in attractive markets through acquisitions at break-even or accretive returns, and

- IRT provides capital to third-party developers, providing 15 - 20% returns and a ready-made acquisitions pipeline.

The company expects to raise $35 to $40 million through dispositions this year, but has no plans to spend on acquisitions of existing properties.

Quarterly Results

- Same-store NOI up 6.3% YoY (year-over-year).

- Core FFO of $63.7 million, up 8.7% YoY.

- Adjusted EBITDA of $89.2 million, up 7.2% YoY.

- Completed value-add renovations at 625 units, with a weighted average return on investment of 16.2%.

- Net income of $10.7 million, compared to a loss of -$7.2 million in the year-ago period.

- Earnings per share of $0.05, compared to a loss of (-$0.03) in Q2 2022.

- Occupancy declined 130 basis points to 94.2%.

- Average rental rate rose 8.0% YoY, and 9.4% thru H1 2023.

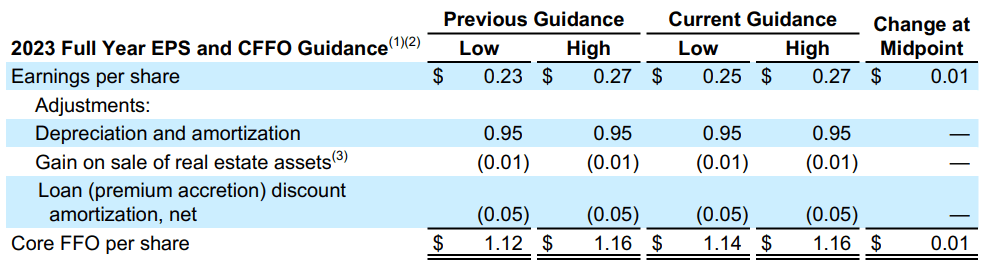

- Slightly raised FFO and earnings per share guidance.

IRT Quarterly Earnings Supplement

{kind=link}

Growth Metrics

Here are the 3-year growth figures for FFO (funds from operations), TCFO (total cash from operations), and market cap. IRT was growing at a healthy clip until 2021, when it bought Steadfast Apartment REIT. But the investment paid off phenomenally in 2022, as FFO per share skyrocketed 29%, while TCFO more than tripled and FFO exploded 7-fold.

| Metric |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 3-year CAGR |

| IRT share price Aug. 21 |

| $11.46 |

| $20.42 |

| $21.20 |

| $15.89 |

| -- |

| IRT share price Gain % |

| -- |

| 78.2 |

| 3.8 |

| (-25.0) |

| 11.5% |

| VNQ share price Aug. 21 |

| $80.88 |

| $106.59 |

| $99.52 |

| $79.70 |

| -- |

| VNQ share price Gain % |

| -- |

| 31.8 |

| (-6.6) |

| (-20.0) |

| (-0.5) |

Source: MarketWatch.com and author calculations

IRT Balance Sheet

Independence Realty's balance sheet sets it apart from other value-add apartment REITs, such as NXRT and BRT Apartments (BRT). Its liquidity ratio of 2.20 is not only above both the Apartment REIT and overall REIT averages, it is positively FROG-worthy . Its somewhat elevated Debt Ratio and Debt/EBITDA, however, are characteristics of value-add apartment REITs.

| Company |

| Liquidity Ratio |

| Debt Ratio |

| Debt/EBITDA |

| Bond Rating |

| IRT |

| 4.53% |

| 0.0% |

| 4.53 |

| 60% |

| A- |

Source: Hoya Capital Income Builder, TD Ameritrade, Seeking Alpha Premium

Dividend Score projects the Yield three years from now, on shares bought today, assuming the Dividend Growth rate remains unchanged.

(Note: Ordinarily I use the 3-year track record for dividend growth to arrive at Dividend Score. However, 3 years ago the market was in the icy grip of the pandemic, so 3-year dividend growth scores are currently distorted and produce unrealistic Dividend Scores. So just for the next several months, I will use the 5-year dividend growth track record instead).

IRT Valuation

Growth like IRT's usually comes at a high price, but not in this case. IRT sells for just 13.8x FFO '23, which is below both the Apartment and Overall REIT averages, and its rather spectacular (-30.9)% discount to NAV is also more attractive than average.

| Company |

| Div. Score |

| Price/FFO '23 |

| Premium to NAV |

| IRT |

| 4.53 |

| 13.8 |

| (-30.9)% |

Source: Hoya Capital Income Builder, TD Ameritrade, and author calculations

From a growth investor's perspective, the low price is cause for suspicion. But from a value investor's point of view, this combination of high growth and safe yield at a low price is very attractive.

What Could Go Wrong?

IRT's assets are skewed toward the Sunbelt states. Should adverse economic changes occur in that region, IRT's bottom line could be affected.

The company depends in part on joint venture partners. If any of those partners prove to be incompetent, dishonest, or otherwise unprofitable, IRT would be adversely affected.

A higher-for-longer interest rate regimen from the Federal Reserve could make it difficult to acquire assets at acceptable rates of return. Together with labor and material shortages, it could also cut into the profit margin from redeveloping the company's existing portfolio.

Investors' Bottom Line

Regardless whether you are a FROG hunter or COWhand (value investor), IRT is a solid buy, with growth in revenue, cash flow, and dividends well beyond average, excellent liquidity, a safe above-average yield, and a below-average price. What's not to like?

Seeking Alpha Premium

Of the 11 Wall Street analysts covering IRT, 8 rate the company Buy or Strong Buy, and the other 3 rate it a Hold. The average price target is $20.73, implying 30% upside. Hoya Capital Income Builder deems IRT to be 26% undervalued.

TipRanks, The Street, Zacks, and Ford Equity Research are all Neutral or Hold on IRT.

However, as always, the opinion that matters most is yours.

For further details see:

Independence Realty Trust: What's Not To Like?