INDB - Independent Bank: Slump Continues Despite Q3 Above Expectations

2023-10-26 05:58:18 ET

Summary

- Independent Bank's stock price has dropped under $45 per share, causing concern among investors.

- The bank's Q3 2023 results were rather positive, with higher-than-expected EPS and revenues.

- The main concern is the bank's large loan portfolio, particularly in commercial real estate, which is over 300% of total capital.

It is not an easy time for Independent Bank (INDB), in fact the price per share in the days following the release of Q3 2023 has plummeted to just under $45. This is a level already reached during the peak of the banking crisis at the beginning of the year, which denotes some concern among investors. In any case, this collapse I believe is more due to a general panic toward the banking industry rather than toward Independent Bank, in fact the quarterly results were quite positive:

- EPS was $1.38, $0.05 higher than expected.

- Revenues were $183.42 million, $2.64 million higher than expected.

Certainly, there was a deterioration in the net interest margin, but the market had already discounted this scenario. Probably the main concern is CRE's huge loan portfolio, still over 300% of total capital.

Margins are about to stabilize

Although there is a good chance that the Fed Funds Rate has stopped rising, the pressure on the cost of deposits continues to be one of the main dilemmas for all banks. Clients no longer accept low returns on their deposits as Treasury-Bills yield more than 5 percent.

Independent Bank Corp. (INDB) Q3 2023

{kind=link}

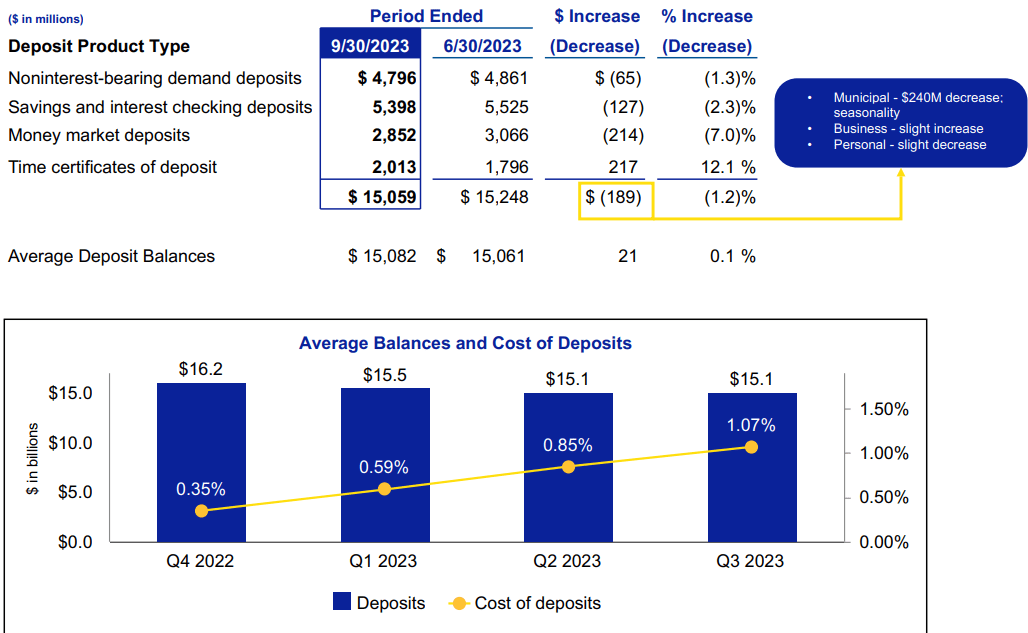

Since Q4 2022, Independent Bank's cost of deposits has tripled to 1.07%. In any case, it represents a rather low rate when compared to peers. Also, the decline in deposits seems to have stopped since they remained unchanged from the previous quarter, $15.10 billion.

Independent Bank Corp. (INDB) Q3 2023

Independent Bank is successfully managing the difficulties on the liability side, but still could not avoid yet another deterioration in the net interest margin. Yield on assets has failed to offset the increase in the cost of deposits.

Management expects this pressure to continue in the coming quarters, but there is some important news on the asset side. In fact, a number of repricing benefits are expected that will mitigate the rise in costs. We are not only talking about maturing securities and loans, but also about hedging.

Over the next 12 months $300 million of hedges will mature, with an average strike rate of 2.80 percent. In the current rate environment, the rate would be about 5 percent, 220 basis points higher on a notional of $300 million. In other words, if the bank keeps the cost of deposits low and manages to reprice maturing assets at hundreds of basis points more, the net interest margin can only benefit. According to CFO Mark Ruggiero , the latter will stabilize heading into 2024, so the market has already discounted a further decline in the next quarter.

CRE loans, securities portfolio and buyback

Independent Bank Corp. (INDB) Q3 2023

{kind=link}

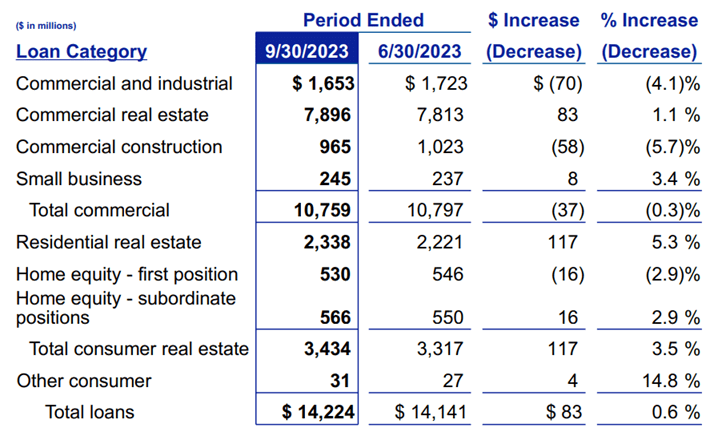

Compared with the previous quarter, total loans are up 0.60%, driven mainly by residential real estate, up 5.30%. Total commercial did not increase, but the proportion of non-owner occupied CRE to total capital remains too high.

Independent Bank Corp. (INDB) Q3 2023

Typically, a value above 300% indicates a red flag, as CRE loans have three times the weight of total capital. In other words, the bank is primarily exposed to cyclical loans that depend on how the underlying markets will perform, and total capital may not be high enough to cover unexpected losses. Over the past two quarters, this ratio has increased.

In the event of an economic slowdown or recession, I believe there are conditions for Independent Bank to suffer more than peers. For now, however, mine remains a guess, because there are no signs that this bank's loans are deteriorating.

Independent Bank Corp. (INDB) Q3 2023

In fact, the opposite is happening as nonperforming loans have improved and have reached 0.28 percent. At the same time, delinquent loans are also declining. As previously discussed, there will be a major repricing of assets in the coming quarters that will put more stress on borrowers, so it will be interesting to see if these ratios worsen.

As the last two topics, I would like to discuss unrealized losses and the buyback plan.

Independent Bank Corp. (INDB) Q3 2023

{kind=link}

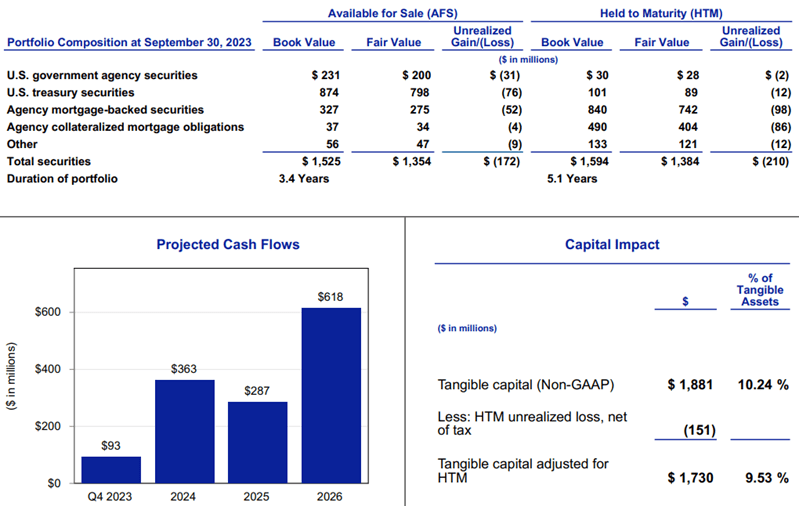

On the first issue, Independent Bank is not suffering from rising interest rates since its securities portfolio is relatively small compared to total assets, 8 percent to be precise. In fact, unrealized losses account for only 5.5 percent of equity and little change if Treasury yields continue to rise a bit more. In addition, the duration of AFS securities is 3.4 years and in 2024 Independent Bank will get cash inflows of $363 million. This capital can be reinvested at high interest rates and would improve net interest income.

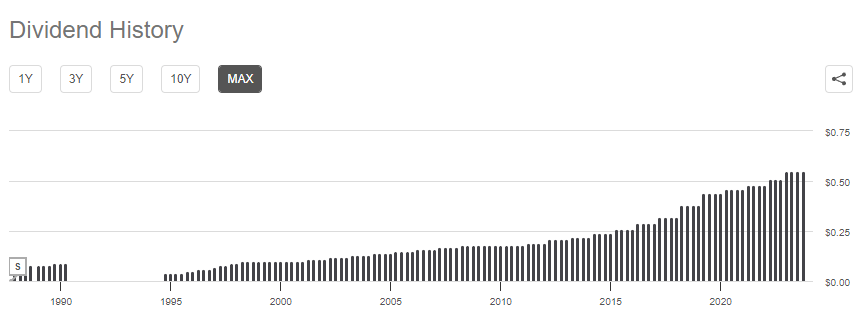

Finally, in Dec. 20, 2022 , the BoD had authorized the bank to repurchase in 2023 about 5 percent of the outstanding common stocks - 1,100,000 shares - but for the first 9 months only 288,401 shares were repurchased. Probably, management has thought of suspending this operation since it causes a reduction in equity. At this stage where retained earnings struggle to increase and there are unrealized losses, it is better to retain this wealth than to remunerate shareholders. In any case, the dividend remains a priority.

{kind=link}

The current dividend yield is 4.84 percent, and throughout history, with the exception of the 1990s, it has always been increased or held steady. During the 2008 financial crisis there was a stall in growth, but the dividend has never been suspended. Personally, in the event of a recession, I assume that the same scenario may occur.

Conclusion

Independent Bank's quarterly report was not in my view so bad as to justify a drop below $45 per share in a few days. Probably, a rising pessimism in the banking industry is weighing on its valuation. In fact, somewhat surprisingly, long-dated bond yields are rising faster than expected and the spread between the 10-year and 2-year yields is turning positive again. Typically, a recession has always followed when this has happened in the past.

In any case, for the time being, the situation remains stable, and Independent Bank has experienced an increase in tangible book value per share.

{kind=link}

After a difficult 2022, there was finally an improvement over 2021 in the latest quarterly report. In other words, the market may have been too hard on Independent Bank, but it is good not to underestimate recession risk since any losses in CRE loans would have a significant impact on total capital.

For further details see:

Independent Bank: Slump Continues Despite Q3 Above Expectations