IDEXF - Inditex: Fashion Powerhouse Winning

2023-05-16 09:47:19 ET

Summary

- Inditex is a retail company that distributes clothing, footwear, accessories, and household textile products.

- Revenue has grown at a CAGR of 7%, driven by a shift in the apparel industry which Inditex has led.

- Inditex has an EBITDA-M of 21% and a NIM of 17%, which have been relatively sticky.

- Key value drivers are its range of brands, geographical footprint, and supply chain investment.

- Inditex's valuation does not suggest any upside based on a DCF.

Investment thesis

Our current investment thesis is:

- Inditex is a strong business due to its diversified range of brands and global footprint. Its supply chain allows the business to be highly profitable and remain culturally relevant.

- Our key concern is whether the trend toward sustainability and brands such as Shein (Oxymoronic, we know) could slow Inditex's growth.

- Inditex's current valuation does not imply upside.

Company description

Industria de Diseño Textil, S.A., ( OTCPK:IDEXY ) also known as Inditex, is a retail company that distributes clothing, footwear, accessories, and household textile products.

The company sells its products under different brands such as Zara, Pull & Bear, Massimo Dutti, Bershka, Stradivarius, Oysho, and Zara Home. Additionally, Inditex is involved in textile manufacturing, logistics, design, insurance, construction, real estate, and financial services businesses.

Share price

Inditex's share price has had a mild decline, making no substantial gains. Despite this, the company has seen wild variability Y/Y, as investor sentiment changes.

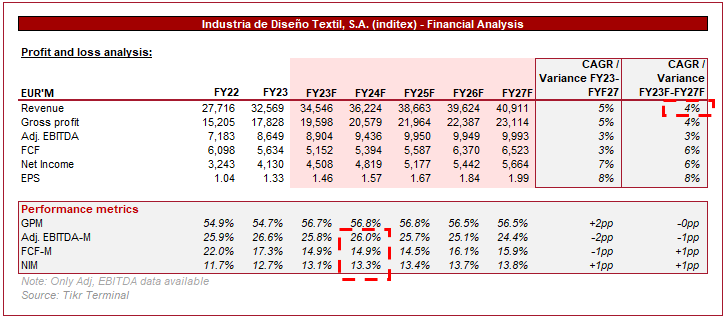

Financial analysis

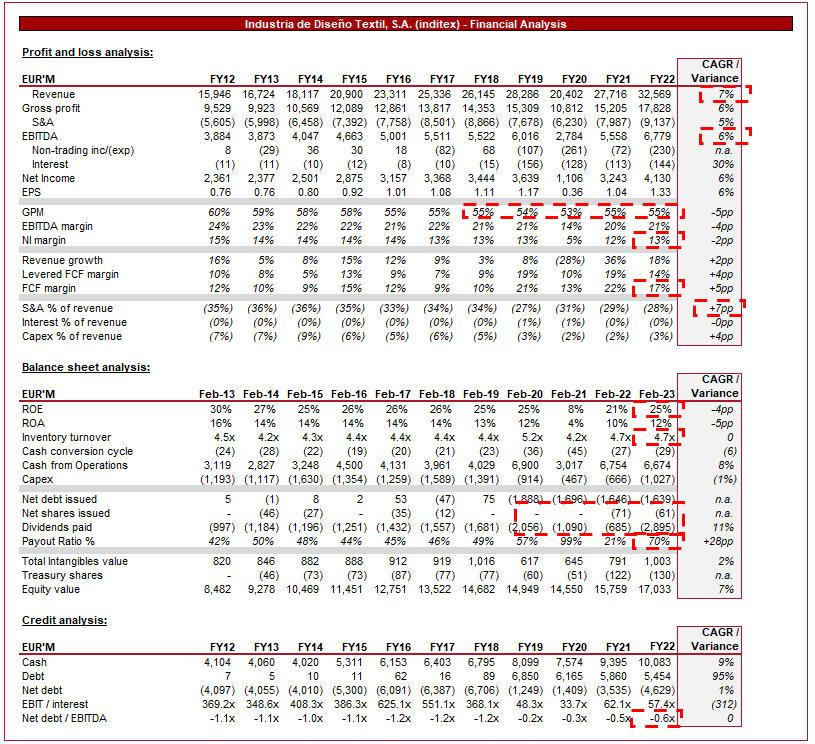

Inditex financial performance (Tikr Terminal)

{kind=link}

Presented above is Inditex's financial performance for the last decade.

Revenue

Inditex has grown its revenue at a CAGR of 7%, as the business has led a structural shift in the affordable apparel segment.

Inditex has invested heavily in supply-chain innovation, intending to shorten the time between design and production. This allows its brands to respond faster to fashion trends than their competitors, with the flexibility to adjust as required. This created the concept of "fast fashion", which is mass-produced affordable clothing that aligns with the trends luxury fashion houses dictate.

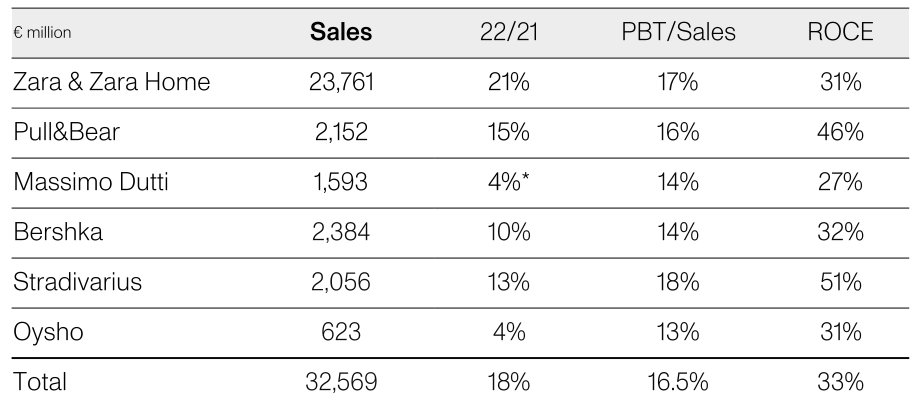

Further, Inditex has benefited from having a wide variety of brands and products. This reduces the risks around underwhelming designs or falling out of favors, as the goods produced are sufficiently different to target different individuals, but also encourage the same to shop around. From a financial perspective, these brands are all accretive to Inditex's ROCE, with no dilution of returns.

This also provides the business benefits from an operational perspective. Given the brands sell similar products for the most part, they can all benefit from Inditex's market-leading supply chain, allowing for shared competencies. This is the primary reason each of these brands has been able to grow as they have.

{kind=link}

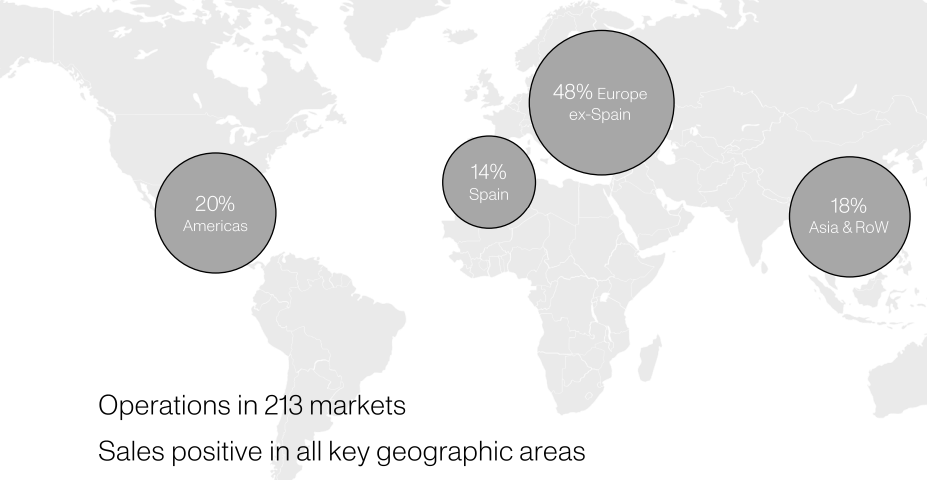

Moreover, Inditex is highly diversified globally, with no single country generating over 15% of its revenue. This is a reflection of global fashion harmonizing, partially due to the impact of social media. This allows the business to further optimize its supply chain, with many of its products exported globally. Significant expansion efforts are going into developing nations, with Inditex intending to find growth outside of the West. Further, this reduces concentration risk, should there be weakness in any given region.

{kind=link}

The rise of e-commerce and social media has transformed the way consumers shop for fashion, and thus how businesses look to attract sales. Online sales are growing rapidly, and many consumers are using social media platforms like Instagram to discover new brands and products. Inditex has done a fantastic job in developing its digital presence. Its brands have arguably the best websites in their respective segments, with a strong social media offering. Further, the business has focused on utilizing its several distribution channels to develop an omnichannel approach, partnering its physical locations with e-commerce.

Consumers are becoming increasingly concerned about the environmental and social impact of fashion. As a result, there is a growing demand for sustainable and ethically produced clothing. Inditex has come under significant pressure in recent years in regard to this, as it is the poster child for fast fashion. McKinsey found 60% of consumers would be willing to pay more for sustainably sourced products, reflecting the importance of sustainable practices. Despite investment in improving its supply chain, Zara receives a "not good enough rating" (By goodonyou , a business that analyzes ESG factors). The difficulty here is that for Inditex to improve its rating, it would need to fundamentally change its business, which is not going to happen. This is one of our major concerns as if the sustainability trend continues, Inditex will be forced to transform its supply chain or face declining relevance. For this reason, Inditex has taken an alternative approach, launching "ZARA Resell", where consumers can resell their Zara products to extend the longevity of its products. We like this idea. Margins for such services are high so is accretive (eBay as an example has a GPM of c.70%+) and the products will not compete with Zara's current range as they will likely be from former seasons.

{kind=link}

An additional concern, which is an oxymoron to the above point, is the rise of what we are dubbing "faster fashion". There are several businesses that have seen the innovation by Inditex and others and taken it a step further. Examples of this are Shein, Romwe, boohoo ( OTC:BHHOF ), and PrettyLittleThings. These businesses have taken the fast fashion approach of designing culturally relevant products while producing them at even lower costs / quality through the use of supply chains in countries such as China. Further, without a physical presence, these businesses can price even more aggressively. Consumers have flocked to these brands. Our concern is that this could slow Inditex's growth as its brands struggle to compete.

Economic considerations

Current economic conditions represent a near-term headwind for the business. Inflation globally remains high, with interest rates continually being increased to bring it under control. This is negatively impacting consumers' finances and leading to reduced retail spending. Apparel generally performs purely in such a market, as consumers can easily reduce spending without impacting their living conditions.

Margin

Inditex's margins are fantastic, with an EBITDA-M of 21% and a NIM of 13%. These have trended down slightly in the last decade, with increased competition resulting in greater discounting and pricing adjustments.

Further, we have seen this partially offset by Inditex's continued investment in developing its supply chain. This has come in two avenues. Firstly, scale economies and shared competencies, as production increases with growth. Secondly, is the development in technological capabilities. An example of this is Inditex's new security tag technology, which is expected to reduce checkout times by 50% and improve online packing.

Balance sheet

Inditex is conservatively financed, with a negative net debt balance. This has allowed the business to increasingly distribute to shareholders, with dividend payments increasing 11% in the decade. Despite this, the company has increasingly accumulated cash, with a CFO of €6.7bn and Capex of €1bn. With Mr. Ortega owning over 50% of the business, the cash accumulation is likely a choice, suggesting we may not see a material increase in distributions, which the business is capable of.

We have highlighted the quality of Inditex's supply chain numerous times, but for a final time, we will give the company credit. It has an inventory turnover of 4.7x, which in our view is very impressive, maximizing the company's cash usage. We expect a leading retailer to achieve >4x.

Outlook

Wall St outlook (Tikr Terminal)

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Revenue is forecast to grow at a CAGR of 4%, with margins remaining relatively flat. This looks to be a reasonable estimate based on the company's current trajectory, although we certainly see scope for sales outperformance.

{kind=link}

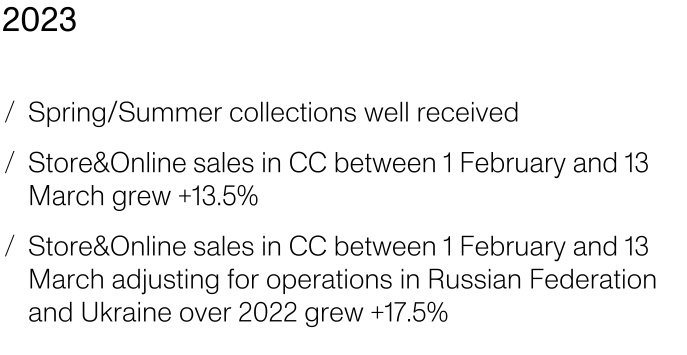

The current Spring/Summer collections are performing well, with sales strong. This suggests macro factors are not having a material effect and should mean a good Q1.

Valuation

Valuation (Tikr Terminal)

Inditex is currently trading at 11x LTM EBITDA, 10.5x NTM EBITDA, and 24x earnings. This is below its historical average, potentially due to investors pricing in greater competition and thus slower growth. This is a reasonable estimate, especially when there is a risk that margins slip alongside slowing demand.

In order to value the business, we have conducted a DCF valuation. Our key assumptions are:

- Revenue growth between 3-6%, reflecting greater competition. This is followed by a perpetual growth rate of 2.5% in line with inflationary price increases.

- Margins remain flat, with a FCF conversion of 14-15%, improving over time.

- A discount rate of 10%.

Based on this, we derive a downside of 4%. Analysts land at a similar level, with a downside of 0.3%. This suggests the company is valued appropriately, with the key driver for outperformance being if growth can be accelerated.

Final thoughts

Inditex has transformed the fashion industry for the everyday individual. Consumers can find products designed in line with luxury fashion houses for a fraction of the price. In conjunction with a superior supply chain, Inditex has become a profitability machine. The only real concerns around the business are whether these new-school fast fashion brands can materially impact Inditex's growth. Although we like this business, it looks to be valued appropriately, implying caution.

For further details see:

Inditex: Fashion Powerhouse Winning