IDEXF - Inditex: Superior To Peers On Multiple Parameters

2023-11-29 09:17:04 ET

Summary

- Even with a 51% price rise YTD, Zara owner Inditex lags peers. Its competitive TTM P/E makes it even more attractive.

- The company's fundamentals are strong too, with double-digit revenue growth and robust margins.

- Even considering that growth has softened from 2022 and next year could pose continued macroeconomic challenges, IDEXY still looks like a good Buy.

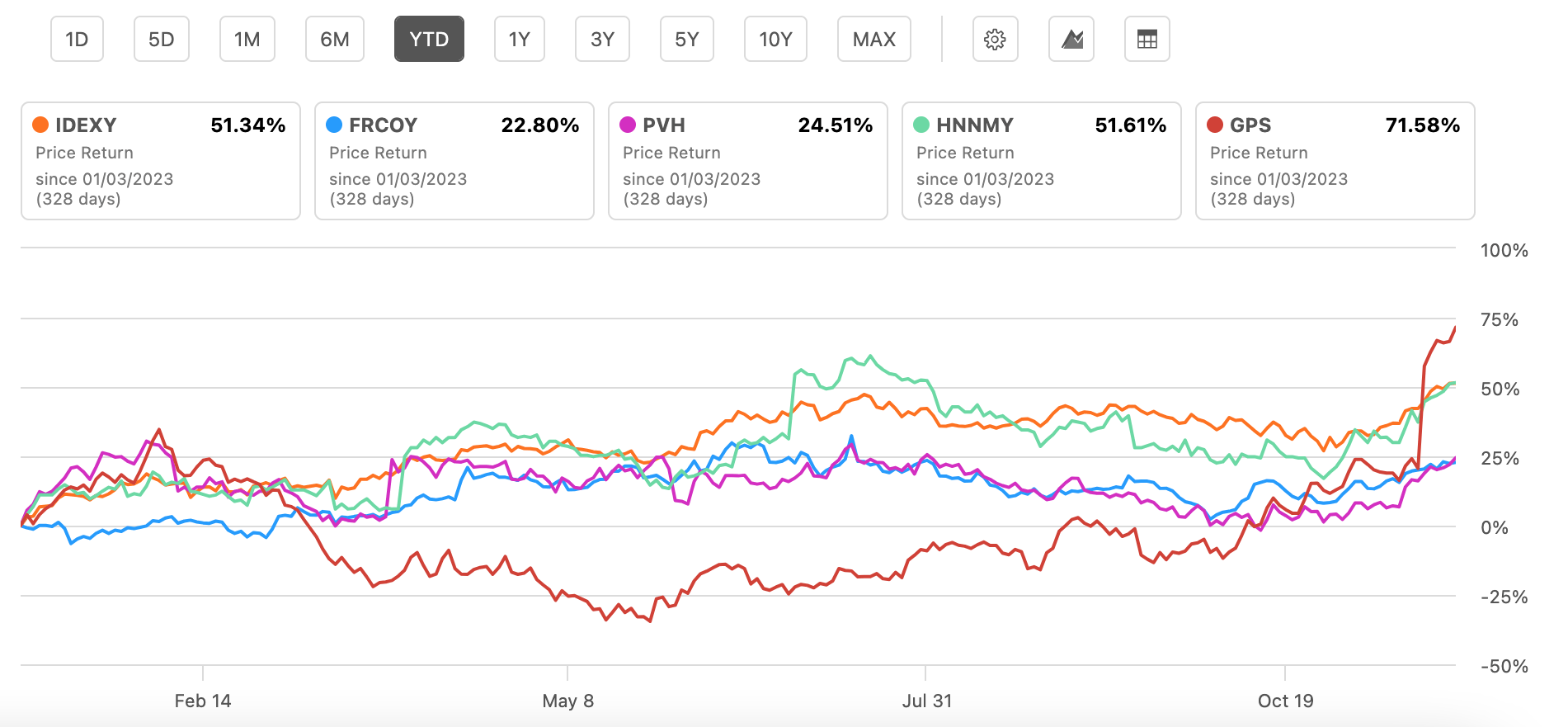

Zara owner Inditex ( IDEXY ) has seen a healthy 51% price growth year-to-date [YTD]. Interestingly, though, it’s not the biggest riser among its peers. The Swedish H & M ( HNNMY ) and The Gap ( GPS ) have seen even higher increases (see chart below).

Price Returns, Select Apparel Retailer stocks (Source: Seeking Alpha)

{kind=link}

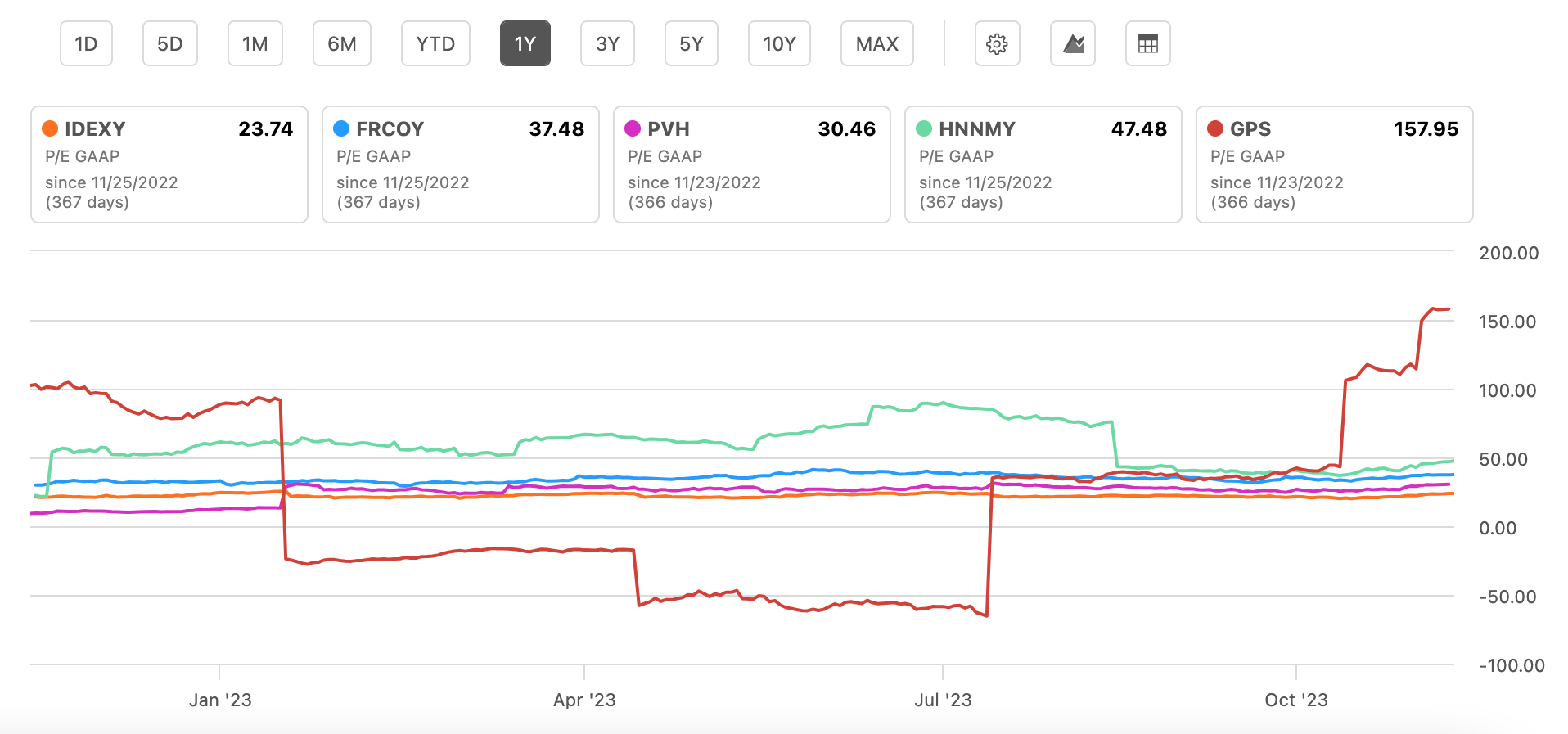

There’s more. Inditex’s trailing twelve months [TTM] price-to-earnings (P/E) ratio is also the lowest among these peers at 23.7x. The next lowest is the Tommy Hilfiger and Calvin Klein owner PVH Corp. ( PVH ). But even that is noticeably ahead of Inditex at 30.5x, while The Gap is at a massive 157.9x.

GAAP P/E, TTM, Select Apparel Retailer Stocks (Source: Seeking Alpha)

{kind=link}

This then, is a good starting place. The combination of a relatively lower price increase and a competitive P/E indicate that there could be potential for a further rise in IDEXY. All that's required now is a look at its fundamentals to assess if there's any reason why it's lagging behind.

Strong fundamentals compared to peers

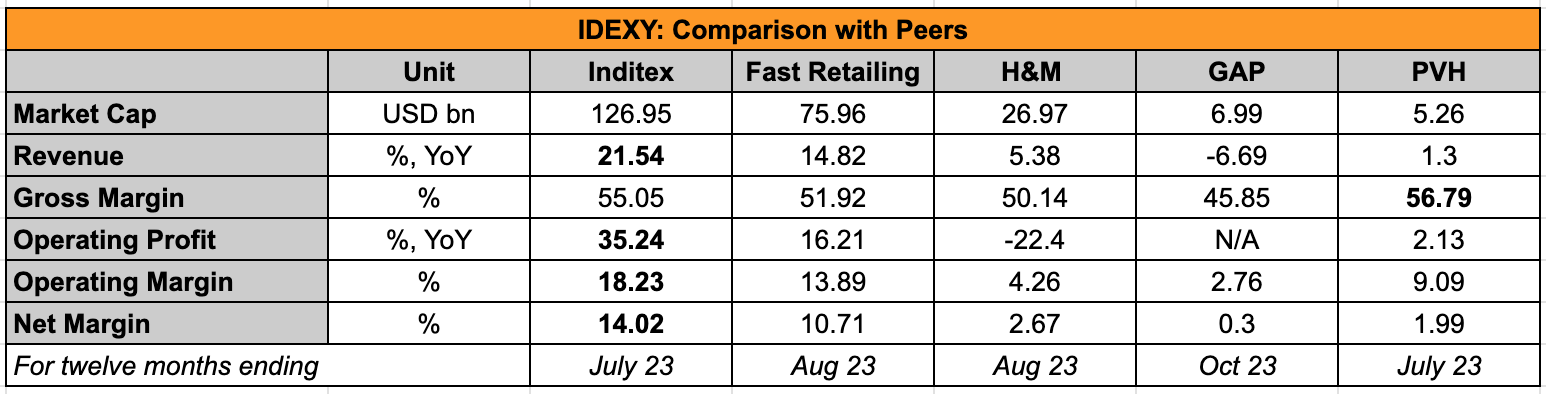

There isn't. Quite the contrary. Comparing the company’s fundamentals to peers shows that it’s significantly ahead of them. Here, I’ve considered apparel retail companies’ TTM performance in USD terms, for better comparison, since they are otherwise reported in different currencies. The numbers are all for slightly different time frames, depending on the period for which the latest update is available, but they do give the big picture.

{kind=link}

The comparison above shows that Inditex’s performance far exceeds that of peers with respect to TTM revenue growth at 21.5% year-on-year (YoY). The same is true for growth in operating profit, with growth not available for GAP because it was loss-making during the base period. For H&M, the operating profit has actually declined over the period.

The company’s profit margins are also the best among peers, save the gross margin at 55.1%, which comes second to PVH at 56.8%. Its operating margins are, however, double that of PVH. They are also non-marginally ahead of the second-best performer, the Uniqlo owner Fast Retailing ( FRCOY ) . At 14.2% it's also the only one among peers besides Fast Retailing to have a double-digit net margin.

Growth across markets

It's notable that Inditex has been able to maintain its lead despite the fact that the company’s growth has slowed down over the past year. In its reported currency, the Euro, it saw a 13.5% revenue growth in the first half of 2023 ending July 31, 2023 (H1 2023) compared to 24.4% in H1 2022. But it’s still healthy and all its markets are growing too.

Importantly, its biggest market of Europe ex-Spain, with a 48% share in total continues to grow in double digits (see chart below). Including Spain, Europe has an even bigger share of 62%, which has also seen a good growth of 16.7%.

Source: Inditex

The slowdown in Americas’ growth is concerning of course, but that the market is growing is still a positive and also, it’s not surprising. Just yesterday, I wrote about the German sportswear company adidas ( ADDYY ) which has seen exactly the same trend of slowing demand in North America compared to other markets. And it’s the larger trend among consumer discretionary companies as well.

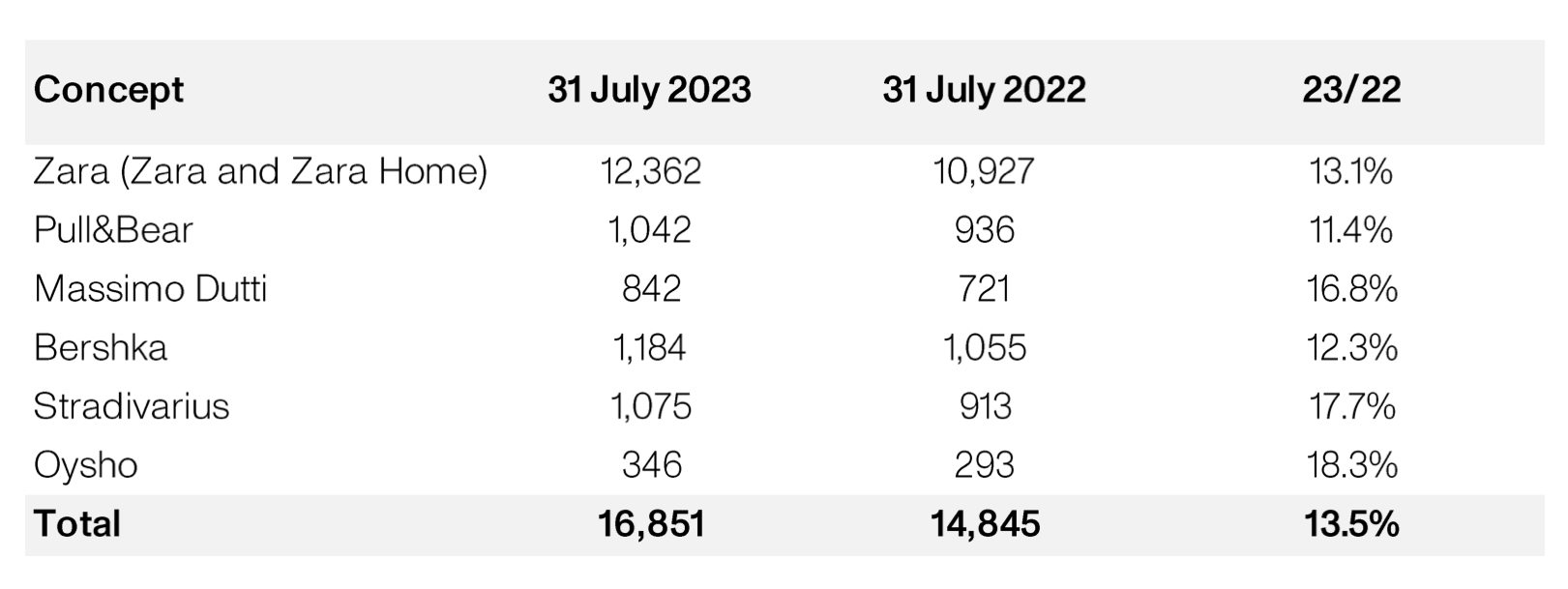

Underpinning Inditex's growth is the continued performance of the Zara brand, which accounts for 73% of the company’s H1 2023 revenue. However, the rest of the brands have seen healthy double-digit growth as well (see table below).

Growth across Segments (Source: Inditex)

{kind=link}

The outlook and forward P/E

To assess how IDEXY’s ADRs are placed in the context of future earnings, the following assumptions have been made. It’s assumed that revenue growth continues to be 13.5% for the full year 2023, as seen for H1 2023.

The company expects gross margin to come in at around 57% (+/- 50bps), so it’s assumed it will be at exactly this level for the full year, even though the company has seen a higher margin of 58.2% in H1 2023. Next, it’s assumed that the ratio of net income to the controlling company to gross profit stays at 25.6%, as seen in H1 2023.

This results in a net attributable income of USD 5.94 billion for 2023, a 43% increase from 2022. It also gives a forward P/E of 21.3x. In stark contrast with the trends for TTM P/E, the forward P/E for IDEXY is second only to Fast Retailing at 36.5x. The average forward P/E for the peer set is 21.5x, which indicates that there’s little upside to IDEXY.

However, it’s a different story when considering the TTM P/E. I have excluded The Gap from the average here because it has an outlier P/E as noted earlier. The average of the rest comes in at 35x, compared to IDEXY’s ratio at 23.8x.

This indicates a price upside of almost 60%. Considering that we are in a time when there can be continued macroeconomic challenges going forward, I’m not sure if this kind of price rise will materialise. But it still shows that on balance, there’s potential upside ahead.

This is particularly so going by its non-trivial dividend yield of 3.2%. And if the kind of net income growth projected actually comes about, investors can see bigger dividends next year.

The risks

Over the medium to long term, however, I do believe that it's important to watch how Inditex's online sales progress. While it hasn't reported developments in digital sales for H1 2023, the share of these sales touched a three year low in 2022 of 22.4% (see table below). This was to be expected, considering that 2020 and 2021 were lockdown years that resulted in a boom in online spending.

Online sales as % of total sales (Source: Inditex)

{kind=link}

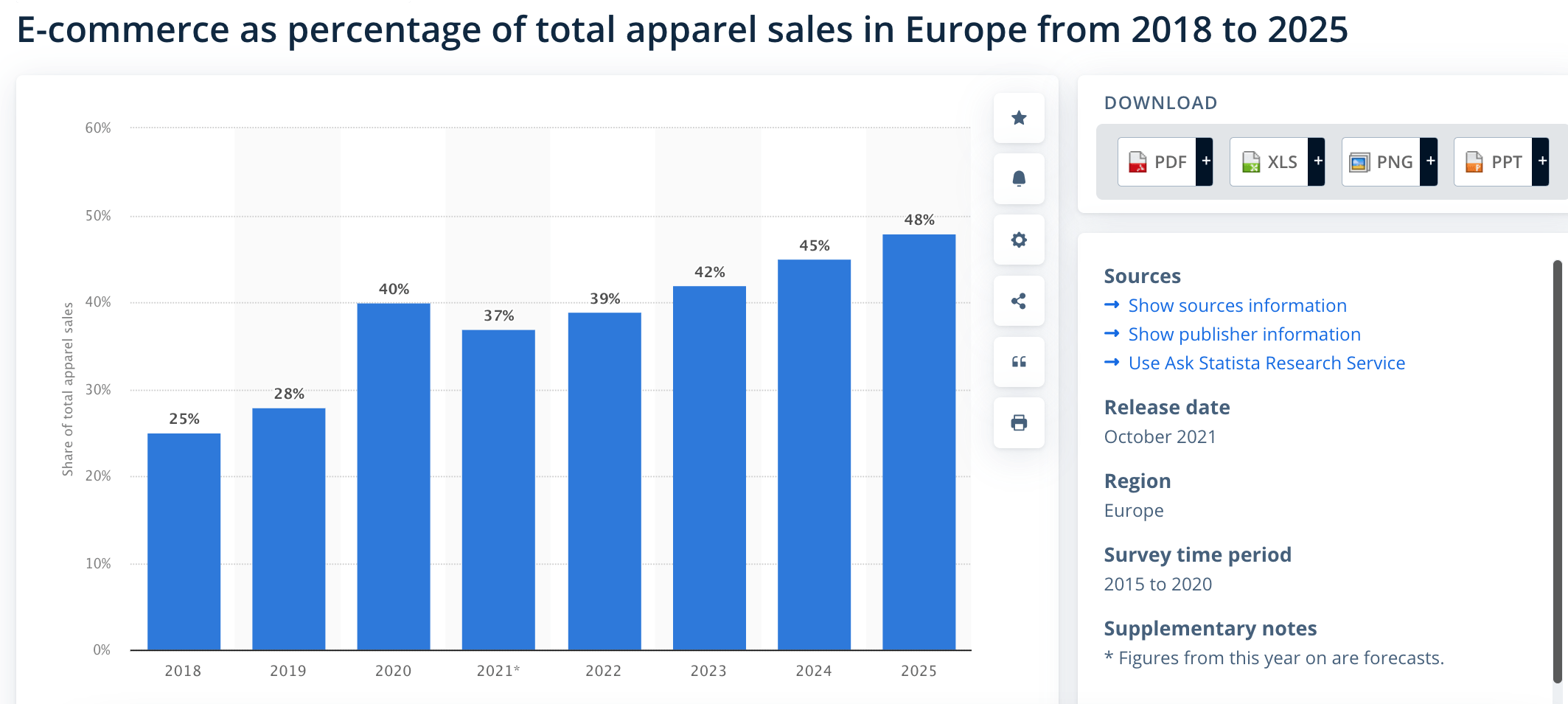

However, I am concerned that in 2022, the company saw just 4% growth in online sales compared with a 17.5% total sales growth. This is particularly so going by the growth of multi-brand apparel marketplaces from the German Zalando ( ZLDSF ) to the London based Farfetch ( FTCH ). Online apparel sales are estimated to be 48% of the total in the company's big European market by 2025 (see chart below). Essentially, this means that over time Inditex would stay relevant if there's robust growth in e-commerce sales.

{kind=link}

Besides this, as I was alluding to earlier, the softening in consumer discretionary goods' sales is visible across companies. This of course is matched with macroeconomic trends. In Europe, consumer confidence "still scores well below its long-term average" according to the European Commission. While growth can improve next year in the EU, as per the IMF , it's still expected to stay muted. And the US economy is expected to see weakness as well.

What next?

Despite the risks however, Inditex’s fundamentals don’t show any red flags for now. In fact, the company’s revenue growth is still strong, even after slowing down from last year, supported by its flagship brand Zara. Its margins are robust too. It compares well to peers too. The relatively lower price rise among peers and still competitive TTM P/E also go in its favour.

Going by the softening in growth across consumer discretionary goods performance recently, I’m somewhat concerned for next year. At least in 2023, there was the benefit of expanding margins as inflation subsided. Next year can be harder if demand continues to slow down.

All things considered, however, I’m more bullish on Inditex than not. I’m going with a Buy rating on it.

For further details see:

Inditex: Superior To Peers On Multiple Parameters