IZQVF - Indivior: Hamstrung By Litigation

2023-04-07 08:09:06 ET

Summary

- Opioid treatment provider Indivior has seen a 20%+ price rise in 2023, but its latest financials are not supportive.

- The company swung into a loss for FY22 on the provision for litigation, which is a red flag, considering that these costs could mount over time.

- Despite its healthy revenue growth and relatively positive guidance for FY23, I am changing my rating on it from Buy to Hold until its legal situation becomes clearer.

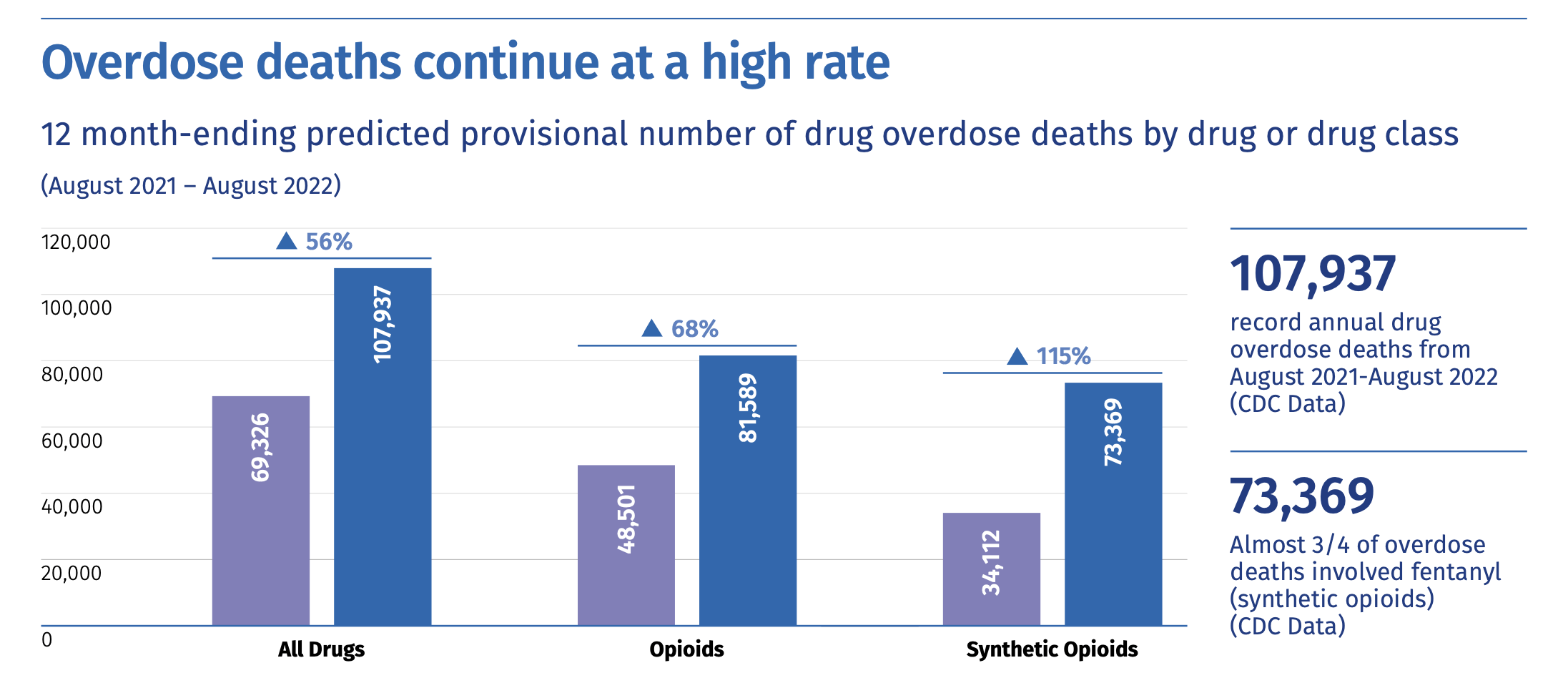

The opioid treatment provider Indivior (INVVY) is up by an impressive 23% year-to-date [YTD]. There are good reasons for this. It is a growing company and defensive healthcare at a time when the macroeconomy looks uncertain. This is particularly true for its main market which is the US that account for over 80% of its revenues, where forecasters like The Conference Board see a 99% probability of a recession in 2023. Importantly, its treatments can be life-saving at a time when there is a rising incidence of overdose deaths (see chart below).

{kind=link}

But all is not going great at the company. It swung into a loss in FY22 . Here I take a closer look at its latest results and its guidance for FY23 to assess what they might mean for its price going forward.

Revenue forecasts on point

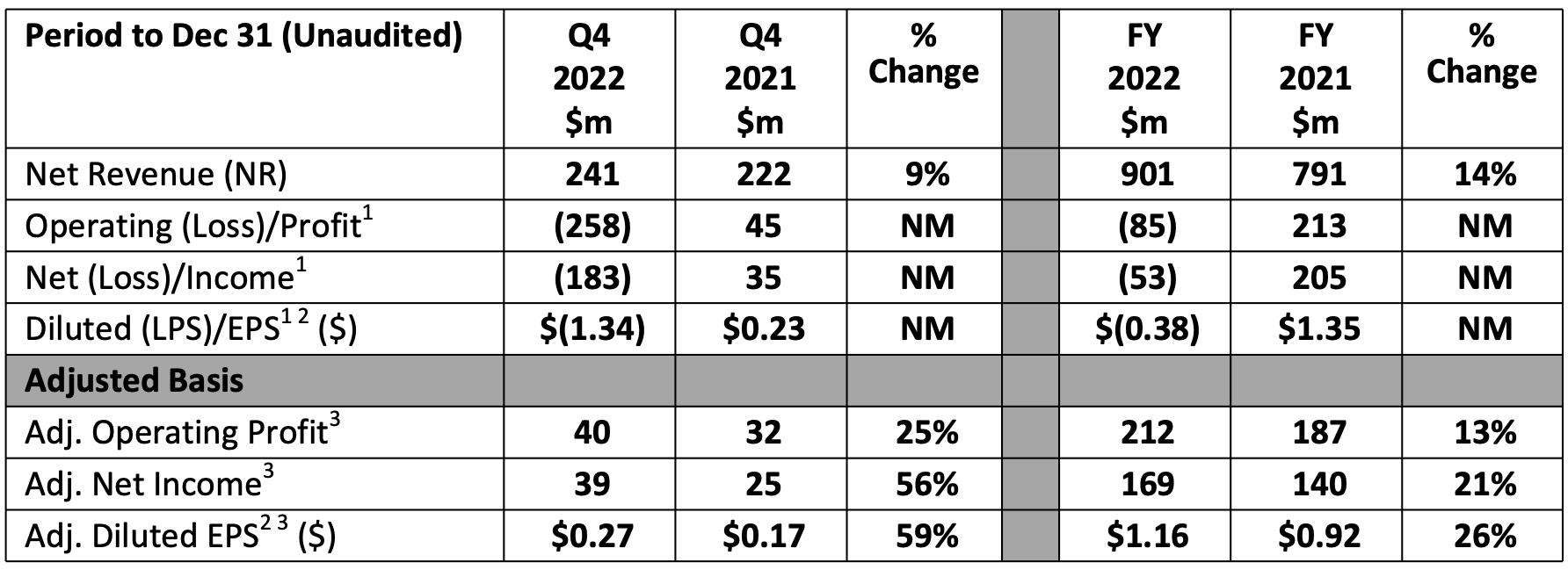

Indivior was bang on target when it predicted a 14% revenue increase in FY22. At the time I wrote about it in January this year, this forecast stood out since it was lower than the 16% increase seen for the first nine months of the year (9M FY22). This, I expected would be down to the conversion of international revenues into USD, the currency in which Indivior reports its figures since that was already visible when it released its Q3 FY22 results. And that has indeed played out. Revenue from the rest of the world at actual exchange rates fell by 10% in 2022, even though it grew by 1% at constant currency. By contrast, its US revenue grew by 21% for the full year.

Unexpected loss

While the company hadn't provided any guidance for reported operating or net figures, the loss looks odd at first glance, considering that its operating profit was up by 3% for 9M 2022. Also, even keeping in mind that its net profit had declined by a significant 23% then, the fact remains that was due to higher taxes for FY22 and a tax benefit for FY21. And it was still clocking a profit.

{kind=link}

In Q4, however, the company reported a loss due to a provision for litigation of USD 297 million. The key litigation states that the company delayed the entry of generic alternatives (see Page 53 of link) to its SUBOXONE tablets, which help in withdrawal symptoms that occur when patients are recovering from opioid usage.

If it were not for this provision, the company would have reported a net profit of USD 212 million compared to a loss of USD 85 million. While it sounds like a one-off, to me it is a red flag. Litigation has been a thorn in Indivior's side earlier as well, including one that brought it much disrepute as it was found falsely marketing the safety of its drugs.

Even this one could drag on, at the very least. As the company's CEO, Mark Crossley says "Because these matters are in various stages, Indivior cannot predict with any certainty how these matters will ultimately be resolved, or the costs, or timing of such resolution."

Elevated P/E ratio

That said, on an adjusted basis, its numbers do look better. Its adjusted operating profit is up by 13% and net income by 21% for FY22. Its adjusted earnings per share [EPS] stand at USD 1.16, which yields a trailing twelve months [TTM] price-to-earnings (P/E) ratio of 23.4x. This is higher than the non-GAAP P/E of 18.8x for the healthcare sector.

A slightly higher P/E ratio could be justified considering its guidance for FY23. The company says that it expects adjusted operating profit to be higher than it was in FY22 without giving any numbers. Assuming that this translates into a higher net income as well, we can expect its EPS to rise as well. Its gross margin is also expected to stay robust at 80% plus levels, which is notable by any standards.

Revenue growth slowdown expected

Revenue growth, however, is expected to slow down to 9% from 14% this year. This is despite the healthy 41% increase expected in its opioid treatment drug SUBLOCADE, which accounted for 45% of the revenues in FY22. The growth softening is expected because of an erosion in the market share of Suboxone film. The erosion has been ongoing since back in 2019 when access to cheaper alternatives was allowed in the US.

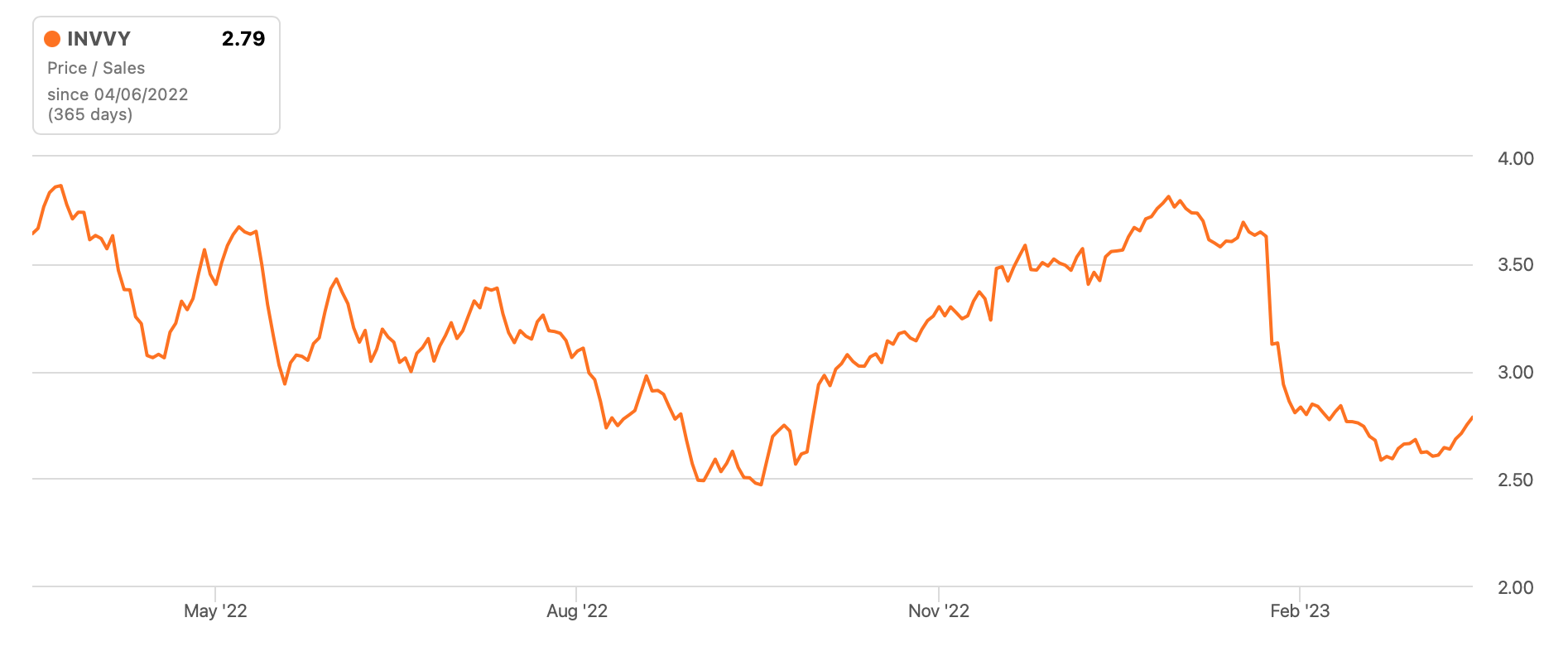

Despite this expected dip in revenue rise, however, the company's forward price-to-sales (P/S) ratio is competitive at 2.4x compared to 4.1x for the healthcare sector. Even now for that matter, its TTM P/S is at 2.8x while that for healthcare is at 4x.

{kind=link}

What next?

In sum, there are both positives and negatives to the Indivior story. At a macro level, its big advantage is as a defensive company in a challenged economy, targeting a growing problem. Its good revenue growth also goes in its favour as do its adjusted profit figures. The company also stands out because of a high gross margin at a time when others are struggling to maintain theirs in a high inflation environment.

However, I find its latest loss hard to get over. Indivior is no stranger to legal wrangles so I would take this seriously, especially since it has had dire consequences in the past. In any case, its non-GAAP P/E ratio is higher than that of the healthcare sector, which makes it less attractive than it was the last time I wrote about it.

Its competitive P/S does make some case for it, especially considering that the gap P/E did not come into consideration as it reported a loss for the full year. But I believe that the P/E is actually a better indicator of future share price movements than the P/S, even if we are considering the non-GAAP figure.

I had a Buy rating on Indivior in January, since which time its price has seen a healthy 14% rise, but I also said that I will change the rating at the slightest hint of legal trouble. That trouble is here, and in a tangible, financial way and we do not know for how long and how much it will actually cost. I believe the more prudent rating, for now, is a Hold until there is more clarity.

For further details see:

Indivior: Hamstrung By Litigation