AZNCF - Indivior: Healthy Defensive In A Difficult Economy

Summary

- Drug addiction is on the rise but so are treatments for it, like those provided by Indivior for opioid usage. With growing revenues and exceptional margins, its price is rising.

- Its price is already up by 55% over the year, and going by the fact that its P/E is lower than that for the healthcare sector, it could rise more.

- The company's not without risks though, with uneven financials over the past decade and a lawsuit with dire consequences for it.

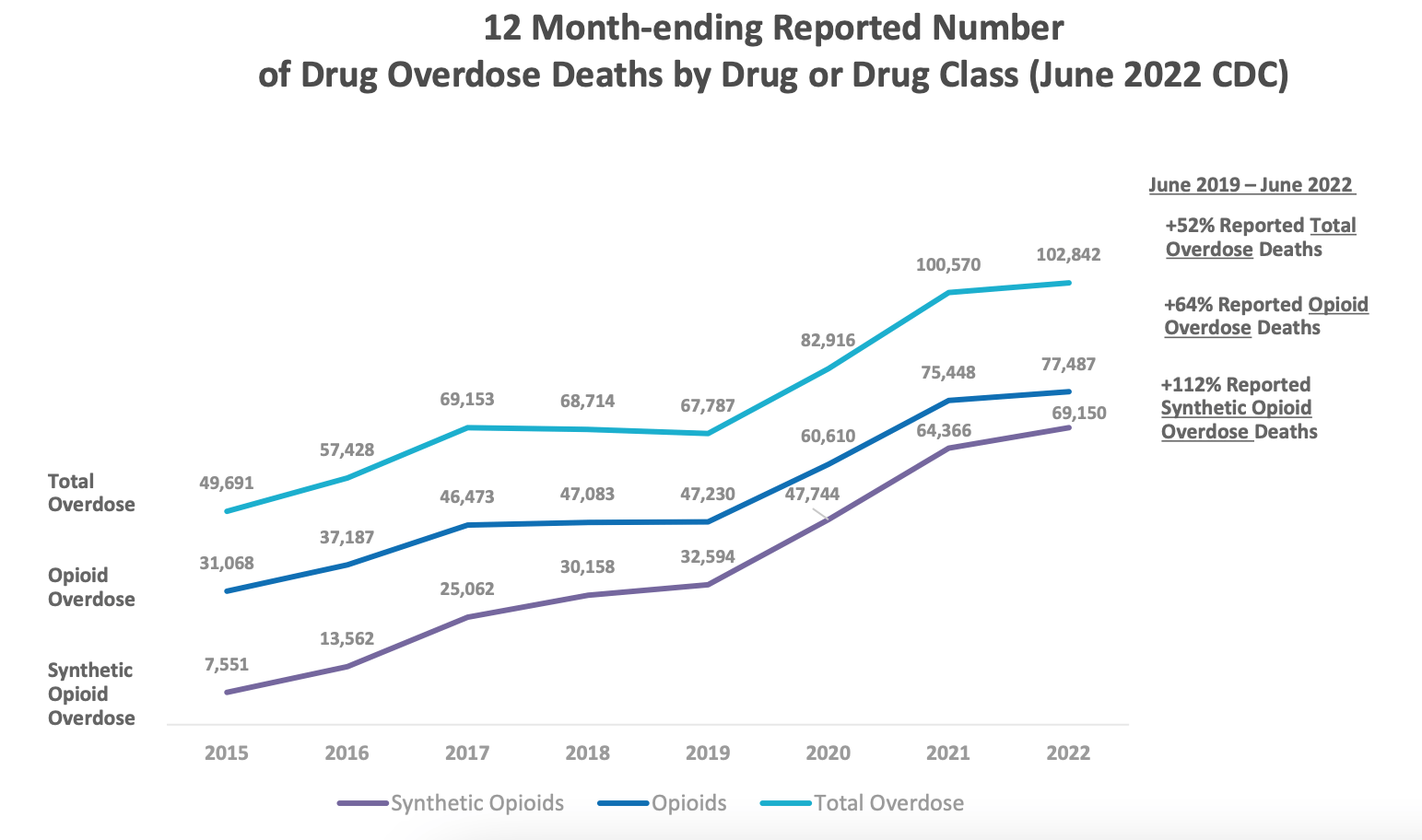

Drug addiction is fast on the rise. According to the WHO, as of 2019, 36.3 million people suffered from drug use-related disorders. In the US alone, more than 100,000 people died from a drug overdose in the 12 months to June 2022. Besides cannabis, amphetamines and cocaine, a number of drug users consume opioids, with the number estimated at 61 million. They also account for 70% of drug-related deaths and some 30% of these are the result of an overdose. The situation worsened during COVID-19. In the US, there was an estimated 15% increase in opioid-related deaths.

With this as the somber background, it’s little wonder that Indivior ( INVVY ) is growing fast. The company provides treatments for opioid usage, with a market-leading position in the US for the treatment of moderate to severe opioid use disorder.

{kind=link}

Strong growth

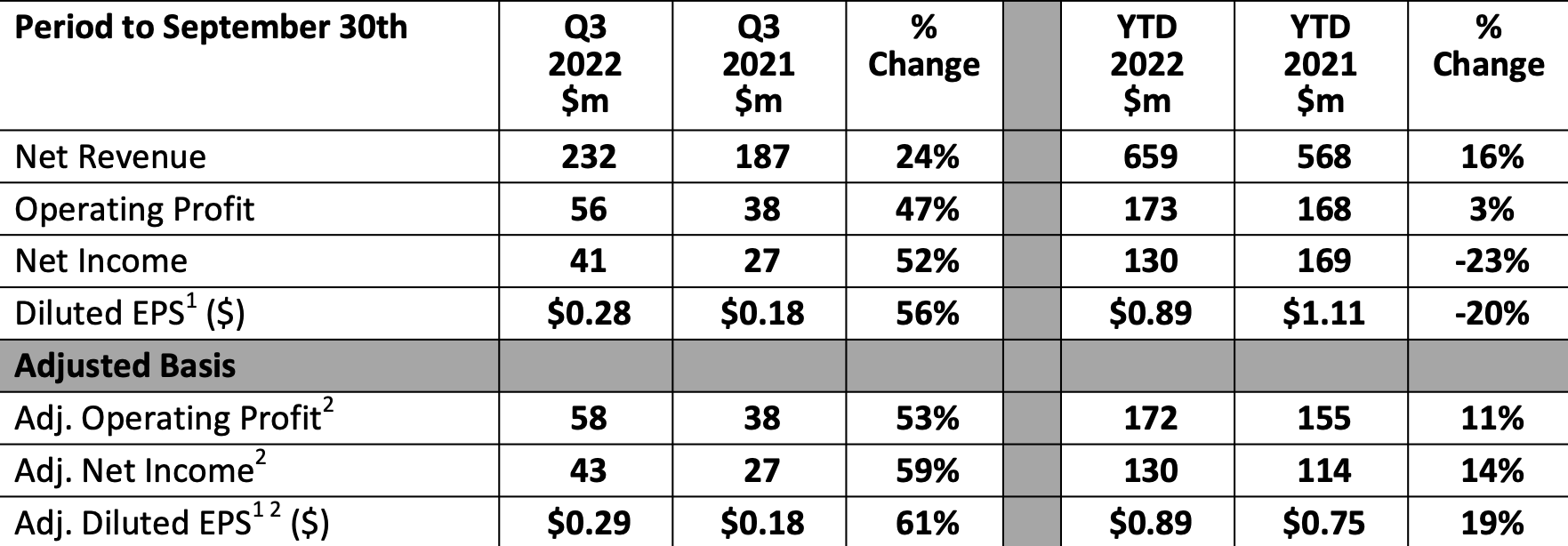

Its top line grew by 24% in the third quarter of 2022 (Q3 2022), with Sublocade, which treats opioid disorders, seeing a revenue rise of 66%. Its revenue increase over the first nine months of 2022 (9M 2022) has been less strong at 16% but that has hardly been a deterrent for the company from raising its guidance. Probably because the guidance still looks quite conservative with an expectation of a 14% increase compared to a 10% increase expected earlier. Or, it can mean that the company expects a slowing down in growth in Q4 2022.

If the second is the case, then I’d look out for a geographical breakdown of its figures in the next quarterly figures. While its biggest market, the US which has an over 80% share in revenues, is still growing at a fast clip, sales have shrunk by 10% in other markets. This would be a relief to hear if it's on account of a genuine reduction in demand for its treatments. But the fact is this is only trivially due to that. Much of it has to do with currency translation, with a decline in revenues from the rest of the world by just 1% in constant currency terms as the US dollar saw a particularly strong last year. In fact, in Q3 2022, sales ex-US grew by 9% even at constant currency.

Exceptionally high margins

The company’s gross profit margin is also exceptionally strong at almost 83%. These are near unbeatable margins by any standards, but for context, they are even slightly higher than those for the cancer treatment provider AstraZeneca ( AZN ) at 81.4% as of the latest quarter. At 25% its operating margins are also quite healthy. Indivior expects a modest increase in its adjusted operating profit this year compared to 2021, which is positive in itself, but it might or might not translate into an even better operating margin.

{kind=link}

The reason is a rise in both the cost of revenues and operating expenses. Cost of goods sold rose at the fastest pace in the year in Q3 2022 at 53.8% year on year (YoY), similarly operating expenses grew by 28.8%. While it doesn’t mention anything about the cost of sales, it does say that operating expenses are up due to higher marketing expenses as well as exceptional consulting costs resulting from Indivior’s plan to get listed on a major US exchange. At present, it’s listed on the London Stock Exchange and it's tradable in the US via OTC Pink. To come back to the main point though, even with higher costs, its margins look firm. With inflation expected to remain high through 2023, costs can continue to rise further, but so far it seems unlikely that it will impact the margins dramatically.

A 23% decline in net income for 9M 2022, however, sits oddly against the rest of the robust report, but this is down to an increase in taxes. In 2021, the company received a tax benefit that bumped up its net earnings. This is a feature of the first half of the year, though, with Q3 2022 net earnings up by 52%. Also, the company’s adjusted net income is up by 14% YoY.

Market multiples indicate further price rise

This takes me directly to its price-to-earnings (P/E) ratio, which is at 21x. While a decline in net earnings has the logical effect of increasing the P/E, in this case, it’s not out of line. The S&P 500 ( SP500 ) is trading at around these levels right now. Moreover, compared to the healthcare sector at 25.3x, it doesn’t look pricey at all. Given the fact that this is most likely to be a year that favors defensives, on account of unsupportive macroeconomic conditions, healthcare stocks as such could be well placed. A company like Indivior with strong growth and robust margins can look especially attractive. So a 20% upside indicated by the higher valuations for the sector, looks achievable to me. It’s already up by 55% over the past year.

Not without risks

But when we look at its longer-term price history, an 11% decline over the past five years is unmissable. And that’s because it’s not a company without its risks despite all that’s going for it. In fact, much has ensued in the past few years that have shaken investor faith in it. Not the least of these includes allegations of false information regarding how safe or not its opioid addiction treatment was, which resulted in its former CEO Shaun Thaxter being jailed for six months in 2020. Reckitt Benckiser, from which Indivior was spun off, also slapped a lawsuit on it for damages from the misleading marketing scheme. It was later withdrawn. This is in addition to the company’s uneven growth over the past decade. At the end of 2021, its revenue was only 60% of where it was in 2012. In other words, its growth can’t be taken for granted.

What next?

For now, though, Indivior appears to have sorted out both its legal and financial challenges. It’s a Buy for me at present, but I would be willing to sell it at the hint of any more legal trouble.

For further details see:

Indivior: Healthy Defensive In A Difficult Economy