VNQ - INDUS Realty: Overvalued In A Growth-Hostile Environment

2023-03-24 08:00:00 ET

Summary

- INDUS Realty Trust has only been a REIT for 2 years.

- The company's growth in revenue and cash flow has been impressive in its short history. Whether they can keep up the pace is another question.

- This article examines the growth, balance sheet, dividend, and valuation metrics for this tiny up-and-coming Industrial REIT.

After a disappointing 2022, in which they lost (-30.2)% and finished below even the dismal REIT average of (-26.2)%, Industrial REITs are off to a relatively good start in 2023. Industrials are one of only two REIT sectors in positive territory YTD, and trail only Self-Storage REITs for total return.

Hoya Capital Income Builder

Among the herd of more than 10 companies is a relative newcomer, INDUS Realty Trust, which is standing out from the pack with a return of 3.16%.

{kind=link}

What is going on with this company? Will its outperformance continue?

Meet the company

INDUS Realty Trust

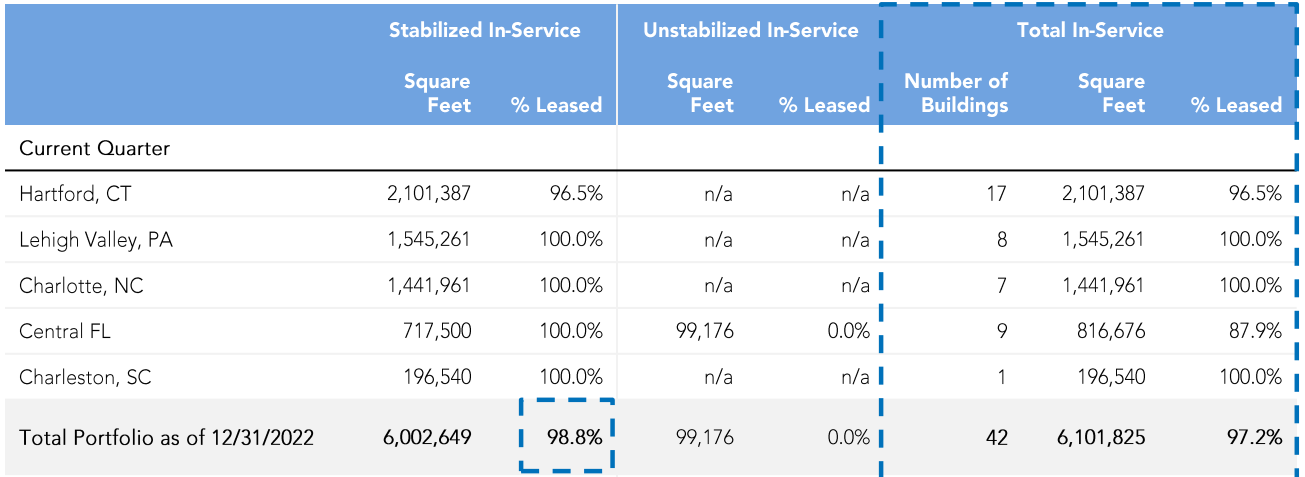

Headquartered in New York City, and formerly known as Griffin Industrial Realty , INDUS Realty Trust ( INDT ) converted to a REIT in January, 2021. This small-cap focuses on mid-size industrial properties (75,000 to 400,000 square feet) in high-growth, supply-constrained markets in the eastern U.S, with strong transportation infrastructure. The portfolio consists of 42 buildings totaling 6.1 msf (million square feet) in 4 geographic areas:

- Lehigh Valley (eastern Pennsylvania)

- Charlotte-Charleston

- Central/Southern Florida

- Hartford, Connecticut

The company also has 295 acres of undeveloped land in Massachusetts, according to its annual report , and is establishing a toehold in Nashville.

Company Q4 Supplemental

The average building measures about 145,000 square feet, and 13 years of age. The portfolio is 97% leased, with a weighted average lease term of 4.7 years.

{kind=link}

The tenant base is not yet fully diversified, as the top 10 tenants contribute 45% of ABR (annual base rent).

Company Q4 Supplemental

For such a small company, the tenants are nicely diversified across a variety of industries, with third-party logistics and trucking companies leading the way.

Company Q4 Supplemental

The company faces significant lease expirations in 2025 - 27, with 18 - 22% of ABR and square footage expiring in each of those three years.

{kind=link}

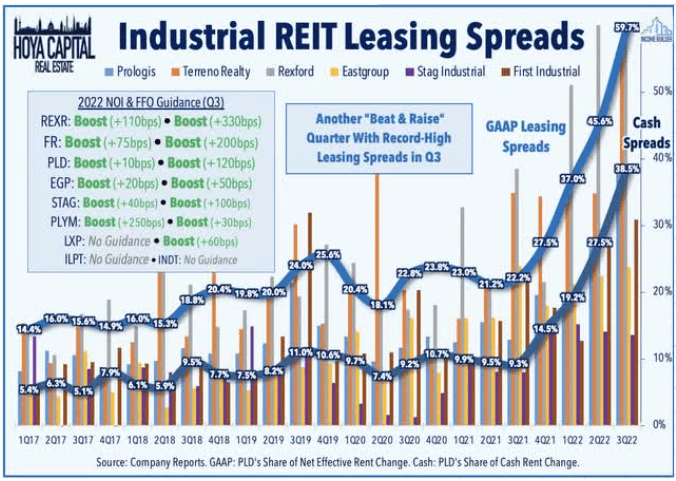

Amid a nationwide shortage of industrial space, INDT enjoyed eye-popping rent spreads of 38% on new leases, and 27% on renewals for the full year 2022. This was not at all uncommon for Industrial REITs.

{kind=link}

INDT has contracts to acquire 5 more buildings (including 2 in Nashville), totaling 0.96 msf, for a total purchase price of $106 million. It also has one new development in progress in Pennsylvania, that will be 0.21 msf, and has purchases or contracts to purchase 4 land parcels that will support up to 9 buildings and 1.35 msf, at a total cost of $31 million. At the same time, it is disposing of 427 acres for proceeds of $26.7 million.

Growth metrics

Like many REITs in their early stages of development, INDT benefitted from relatively easy comparables in 2022, so their growth figures look very impressive.

| Metric (millions) |

| 2022 |

| 2021 |

| Change |

| Rental revenue |

| $49.2 |

| $40.2 |

| 22.4% |

| Expenses |

| $41.8 |

| $36.5 |

| 14.5% |

| Net operating income |

| $38.1 |

| $30.0 |

| 27.0% |

| FFO |

| $24.6 |

| $7.7 |

| 219.5% |

| FFO per diluted share |

| $1.85 |

| $0.95 |

| 94.7% |

| Core FFO from continuing operations |

| $20.0 |

| $12.7 |

| 57.9% |

| EBITDA |

| $25.3 |

| $13.6 |

| 86.0% |

| Cash from operations |

| $19.0 |

| $10.9 |

| 74.3% |

Source: Company 10-K

The company's growth in revenue and cash flow has been impressive in its short history. Whether they can keep up a similar pace over 3 or more years is another question.

Meanwhile, here is how the stock price has done over the past twelve months, compared to the REIT average as represented by the Vanguard Real Estate ETF ( VNQ ).

| Metric |

| 2021 |

| 2022 |

| 1-yr CAGR |

| INDT share price March 21 |

| $74.77 |

| $66.11 |

| -- |

| INDT share price Gain % |

| -- |

| (-11.6)% |

| (-11.6)% |

| VNQ share price March 21 |

| $105.75 |

| $81.11 |

| -- |

| VNQ share price Gain % |

| -- |

| (-23.3)% |

| (-23.3)% |

Source: MarketWatch.com and author calculations

INDT shares have strongly outperformed the VNQ, even while losing (-11.6)% of their value.

Meanwhile, INDT has also outperformed its much-larger and better-established Industrial REIT peers, even while posting a total return of (-10.6)%.

Balance sheet metrics

INDT has an extremely tidy little balance sheet. Industrial REITs on average have stronger-than-average balance sheets, and INDT significantly outshines even its fellow Industrials in liquidity, debt ratio, and debt/EBITDA.

| Company |

| Liquidity Ratio |

| Debt Ratio |

| Debt/EBITDA |

| Bond Rating |

| INDT |

| 2.99 |

| 12% |

| 1.1 |

| -- |

Source: Hoya Capital Income Builder, TD Ameritrade, and author calculations

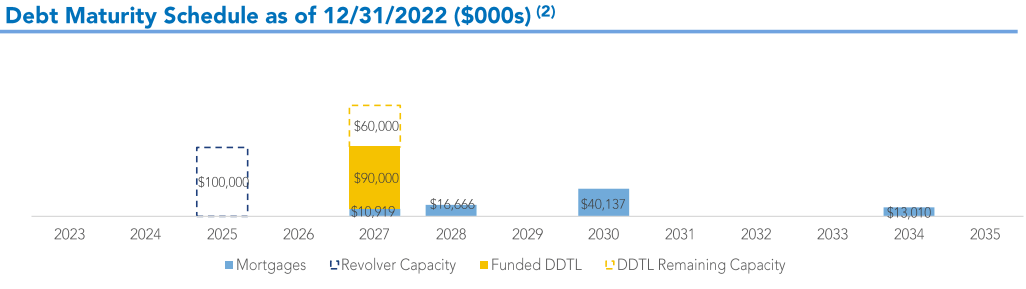

As of December 31, INDT had $52.4 million in cash and equivalents, and $150 million of unused revolver credit, over against $330.7 million in debts. The company also has $100 million in ATM equity issuance authority.

INDT faces very little in the way of debt maturities until 2027, when $160.9 million comes due, which is nearly half its total indebtedness. Between now and then, it faces only $100 million due on its revolver, in 2025.

{kind=link}

If INDT is able to keep up double-digit growth in revenue and cash flow, and maintain this strong balance sheet, within two years it could qualify as a bona fide FROG . In the meantime, however, considering its small market cap of $0.67 billion, and its brief history, it is best thought of as a Tadpole.

Dividend metrics

Industrial REITs are typically low-yielding, but grow their dividends more rapidly than the average REIT. INDT yields even lower than its Industrial peers, and thus far, has not proven itself as a dividend grower, so it earns a pathetic Dividend Score of 1.41. Meanwhile, its dividend is much too safe at A+.

| Company |

| Div. Yield |

| 3-yr Div. Growth |

| Div. Score |

| Payout |

| Div. Safety |

| INDT |

| 1.09% |

| 9.1% |

| 1.41 |

| 40% |

| A+ |

Source: Hoya Capital Income Builder, TD Ameritrade, Seeking Alpha Premium

Dividend Score projects the Yield three years from now, on shares bought today, assuming the Dividend Growth rate remains unchanged. Since INDT is only 2 years old, I simply assumed its 3-year dividend growth rate would match its 1-year rate, for the sake of this comparison.

Valuation metrics

Because of their superb growth characteristics, Industrial REITs usually sell at a higher Price/FFO multiple that most other REITs, and that premium is well-deserved. But INDT is currently selling at a dramatically higher multiple than even the average Industrial REIT, and I personally can't see why the price deserves to be so high.

| Company |

| Div. Score |

| Price/FFO '22 |

| Premium to NAV |

| INDT |

| 1.41 |

| 35.7 |

| (-10.1)% |

Source: Hoya Capital Income Builder, TD Ameritrade, and author calculations

Hoya Capital Income Builder seems to agree, estimating that INDT is about 50% overvalued. Meanwhile, INDT's discount to estimated NAV is typical of an Industrial REIT, and much less tempting than the average REIT.

What could go wrong?

INDT's portfolio is geographically concentrated in just 4 relatively small areas, which causes it to be especially susceptible in the event of adverse developments in those markets. As a small company in a sector of giants, there is the possibility of larger and more experienced companies moving into INDT's 4 markets, which could increase acquisition costs and drive rents down.

Growth has gone out of style. Despite a 3-year growth rate that is 50% better than the REIT average (13.2% versus 8.8%), stronger balance sheets , and stellar operating performance across the board in 2022, Industrial REITs underperformed the REIT average last year, posting an average loss of (-30.2)%, compared to the REIT average loss of (-26.2)%, according to Hoya Capital Income Builder. Times of high inflation and rising interest rates are not good times to invest in growth stocks.

Even more importantly for Industrial REITs, according to Hoya,

discounts have narrowed following a rally from stellar earnings results and retreating interest rates, so selectivity has become critical.

Thus, while some Industrial REITs remain a bit undervalued, there are several that are dramatically overvalued now, and INDT unfortunately appears to be one of them.

Investor's bottom line

It is not unusual for a company with excellent growth prospects to be priced richly, despite yielding at or near zero. So if we look at INDT as a growth stock, its valuation makes a certain amount of sense. Nevertheless, INDT's growth prospects do not exceed those of its well-established and much larger Industrials running mates, so the company does not seem to warrant its extraordinary price multiple. Even if I considered INDT a prudent Buy at this time, its small size and brief history would argue strongly for a very small allocation.

Over the next 2-5 years, INDT may do quite well, so if I had a small position I would probably Hold. However, I think there are numerous Industrial REITs that will do considerably better over the same time frame. If I had a large allocation in INDT, however, I would definitely sell part of it at this favorable price and take profits, either to invest in a better Industrial REIT, or hold the cash for a better price on INDT in the future. So my verdict is a mild partial Sell, while holding part of any existing position for the long term.

Seeking Alpha Premium

The Street sees INDT as a Hold, as does the Seeking Alpha Quant ratings system. TipRanks agrees, with a Neutral rating. So do 4 of the 5 Wall Street analysts covering this firm. The other rates it a Strong Buy. The average price target is $68.25, implying only about 3% upside. Revisions-sensitive Zacks has no rating for this company.

However, as always, the opinion that matters most is yours.

For further details see:

INDUS Realty: Overvalued In A Growth-Hostile Environment