IDEXF - Industria de Diseño Textil S.A.: Defying The Headwinds With Another Strong Update

Summary

- Inditex outperformed its European retail peers yet again in Q3, delivering a double-digit % increase in sales despite the headwinds.

- Gross margins were the only blemish, but decelerating inventory growth provides a tailwind into Q4.

- With the company also maintaining cost discipline while driving overall growth, the near-term setup is compelling.

Inditex SA ( OTCPK:IDEXY ) yet again defied the challenging operating conditions with a solid Q3 update . Of note, revenue and EBIT numbers beat consensus expectations across the board, with Q4 numbers showing signs of further improvement. The key reason for Inditex’s through-cycle outperformance remains its highly differentiated retail model and channel integration, allowing for continued best-in-class lead-time sourcing amid the supply chain disruptions. Fundamentally, Inditex has translated its competitive advantages into consistent growth and cash generation as well, with margin-accretive online growth set to drive further EPS upside in the coming years. The stock isn’t optically cheap at ~20x P/E, but quality rarely is; relative to the underlying growth potential and the mid-single-digit % fwd dividend yield (ordinary + special), Inditex is worth a look, in my view.

Riding the Sales Momentum in Q3/Early Q4

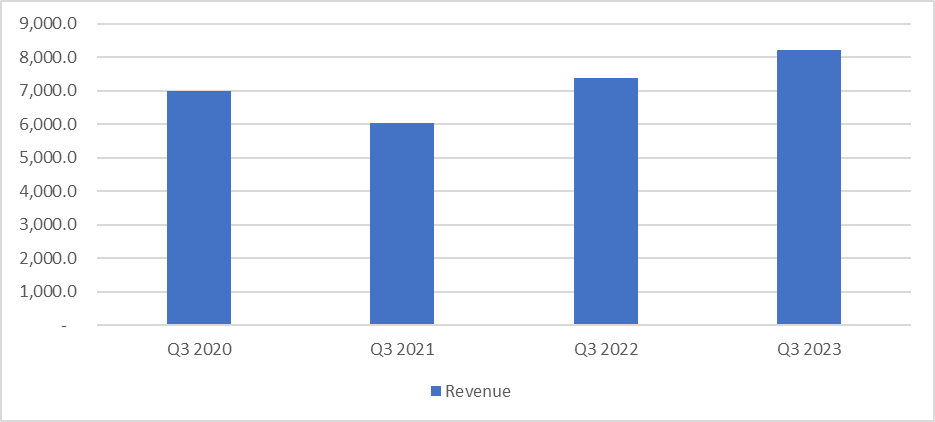

The key highlight from the Inditex Q3 update was its strong sales growth, which was broad-based across all regions and channels to market. Relative to its other retail peers in Europe (see my coverage of H&M’s trading update for the corresponding period here ), the differentiated appeal of Inditex’s ‘high fashion’ offerings is shining through a challenging backdrop. To recap, Q3 sales were up 11.1% YoY to EUR8.2bn, while sales in the initial weeks of Q4 (November to 8 th December 2022) were up ~12% YoY on an FX-neutral basis. In both cases, Inditex is pacing well ahead of expectations.

{kind=link}

Inditex

Perhaps most impressively, though, the strong sales numbers have come despite a decline in square footage due to closures in the Russia/Belarus/Ukraine region. This implies higher like-for-like sales growth than suggested by the headline numbers. Combined with a weaker Q4 base due to last year’s omicron wave, this likely means more upward revisions to earnings on the horizon.

Inventory Headwinds Fading

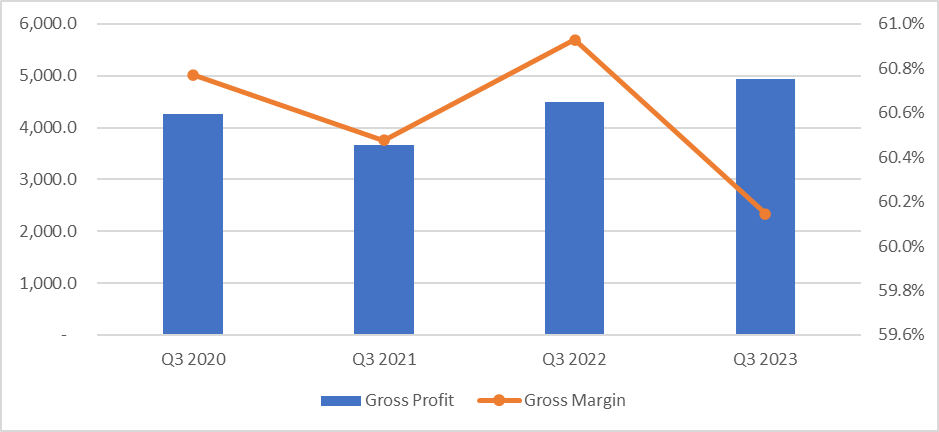

Gross margins were less impressive at -80bps YoY, amid inventory growth of +27% YoY, as Inditex prioritized product availability to buffer against supply chain disruptions. While bears will point to possible discounting ahead based on this metric, some context is needed. Recall that in Q2, the company had seen elevated levels at +43% YoY before falling to +33% in the last trading update (six weeks ending 11 th September). Given Q3 typically represents a seasonal high for inventory levels, the deceleration in inventory growth to +15% YoY in Q4 to date is a positive. And relative to the double-digit % revenue growth, this isn’t a major concern, in my view. With the YTD gross margin up to a solid ~59% (+30bps YoY) and inventories normalizing, the reiterated +/-50bps YoY guidance could prove to be a low bar.

{kind=link}

Inditex

Importantly, Inditex’s short-lead-time production model allows for a key competitive advantage with regard to inventory risk. As the company can hold less inventory as a % of sales, it is, thus, also unlikely to suffer markdowns should consumer demand fall short of expectations. Additionally, a lower % of Inditex’s variable cost line is denominated in USD vs. peers, so it doesn’t need to push through price increases to maintain margins.

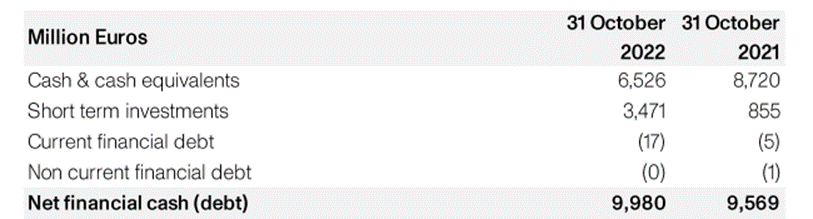

Further alleviating the P&L risks is the increased net cash position at ~EUR10bn. Given the ~EUR0.8bn increase from H1 2022 came despite a double-digit % increase in inventories, a deceleration in Q4 inventory growth will be a tailwind to cash generation.

{kind=link}

Inditex

Opex Levers Insulating Margins

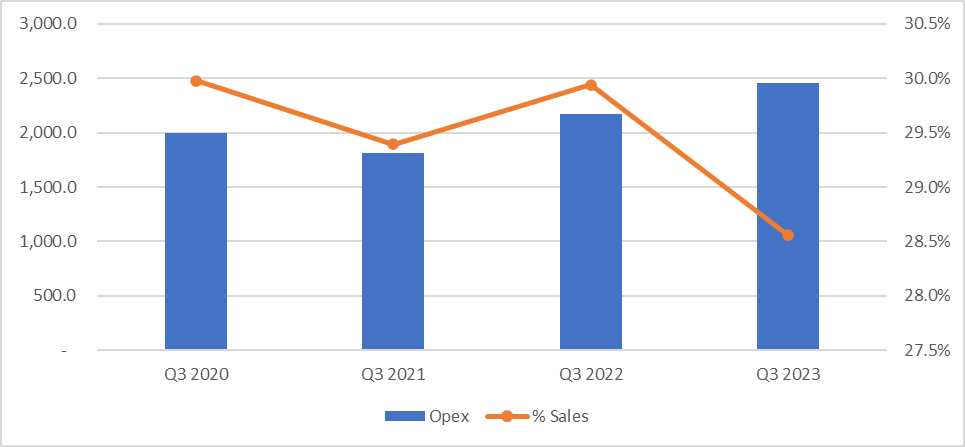

Despite the transitory headwinds at the gross margin level, operating margins have remained strong, helped by continued opex discipline for yet another quarter. While headline opex was up ~13% YoY, underlying inflation was lower at ~10% after adjusting for depreciation and amortization and well below sales growth. Given Inditex has been contending with an inflationary backdrop and investing in online penetration, the opex result is commendable, in my view. Plus, if we were to benchmark against pre-COVID levels, the opex ratio (including rent) would have improved by an impressive ~60bps. This is better than many of its peers, highlighting the effectiveness of the Inditex model and best-in-class channel integration in navigating a downcycle.

{kind=link}

Inditex

Defying the Headwinds with Another Strong Update

Inditex is coming off another strong quarter, with Q3 sales up ~11% and the momentum continuing into Q4 as well at +12% FX-neutral (albeit helped by an easier YoY comp due to the omicron wave last year). Margins were also resilient despite a YoY gross margin % decline, as exposure to the challenging market environment was more than offset by opex discipline and operating leverage benefits.

More broadly, Inditex’s outperformance relative to the rest of European retail reinforces its differentiated operating model, which allows for a clear advantage in lead-time sourcing and logistics. In the near term, the company looks poised to ride out any challenges in FY23, while over the long run, the best-in-class operating platform should continue to translate into superior free cash generation. The stock isn’t cheap, but relative to the through-cycle growth and attractive mid-single-digit % dividend yield on offer (including specials), Inditex is worth a look, in my view.

For further details see:

Industria de Diseño Textil, S.A.: Defying The Headwinds With Another Strong Update