IDCBF - Industrial and Commercial Bank of China: Trading At A Deep Discount With An 8% Yield

2023-04-24 13:38:12 ET

Summary

- ICBC's annual results disappointed again.

- But with the economy already picking up in Q1/Q2, there is light at the end of the tunnel.

- With the bank likely to navigate the upcoming regulatory changes unscathed, the current valuation discount seems unjustified.

- Investors get paid an attractive yield to wait for the re-rating.

Despite a challenging 2022, state-owned commercial bank Industrial and Commercial Bank of China or 'ICBC' ( IDCBY ) looks poised to benefit from the post-COVID reopening. While retail banks will probably gain the most upside near-term, corporate lending growth should eventually follow suit (albeit with a lag). And perhaps even more importantly for ICBC, a more robust economy and increased fiscal support reduce any asset quality risks from the property sector, a key exposure. In the meantime, ICBC stands out for its defensiveness, given its peer-leading capital buffer. As excess Chinese household savings are redeployed into the market, and foreign investment flows also move into low beta, resilient dividend payers ahead of a global slowdown, ICBC should re-rate from the current <0.4x P/Book.

Q4/FY22 Misses the Mark on Further NIM Weakness

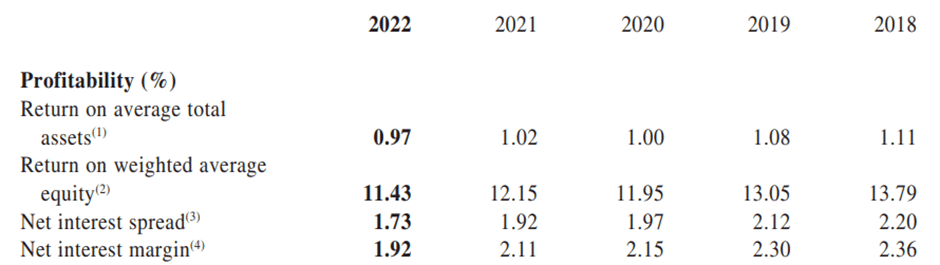

ICBC's full-year earnings report (HKEX filing dated 30th March 2023 here ) saw Q4 net profits of RMB95bn (down ~2% YoY), underperforming its major Chinese banking peers, all of which delivered positive YoY bottom-line growth. Digging deeper, much of the delta was down to ICBC's contracting net interest margins – a result of an overall decline in loan yields (not helped by the multiple Loan Prime Rate reductions in Q4), as well as a rise in deposit funding costs, mainly due to time deposit 'regularization.' Non-fee income performance didn't help either, declining significantly in Q4 due to exchange/exchange rate product losses.

{kind=link}

ICBC

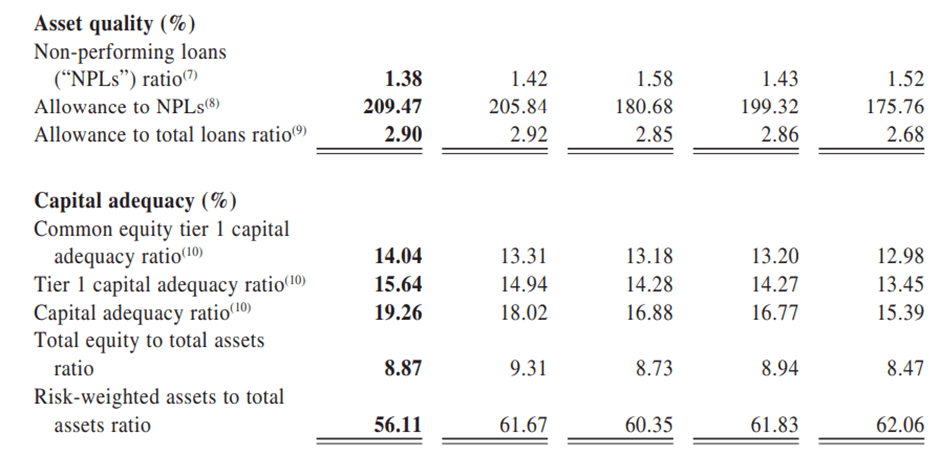

There were silver linings, however, on the asset quality side, which decelerated from the prior pace of NPL deterioration. This came despite a continued increase in property developer NPLs (+1.3%pt YoY to 6.1% in 2022), with lower NPL ratios elsewhere, including on the corporate side, providing a sufficient offset. The CET1 ratio was another bright spot, improving sequentially to ~14% in Q4, the highest among the major Chinese banks. So even with ICBC missing the mark at the pre-provision and net profit levels, the bank's resilient capital position offers it a great base to capitalize on a near-term recovery.

{kind=link}

ICBC

A Relative Beneficiary of Upcoming Capital Regulation Changes

There has been a wave of financial regulatory changes in China this year, chief among them a consultation draft on commercial bank capital management . The regulation, which will come into effect next year, categorizes banks according to their asset size; major SOE banks like ICBC naturally fall into the tier 1 group. Falling into the first tier comes with risk-weighting advantages, particularly on focus areas like small/medium businesses and high-grade corporates such as property developers and local governments.

In essence, the policy update creates a win-win situation. ICBC gains capital savings for deployment into new opportunities in return for accelerating growth in these areas while the government achieves its goal of providing support to the property sector and refinancing local government credit. As ICBC already adopts an internal-based rating approach to its risk-weighted asset calculations as well, the bank should outperform (on a relative basis) due to lower minimum requirements post-reform.

Limited Impact from the Property/Mortgage Fallout

After years of debt build-up, Chinese households have entered their deleveraging phase . While balance sheet repair typically comes with a challenging economic backdrop, this time around, the wide mortgage rate delta (i.e., between outstanding and new loans) amid the People's Bank of China's (i.e., the Chinese central bank) rate cuts and looser lending standards have been the key drivers. At first glance, deleveraging means margin pressures, as higher-rate mortgages and other loans are refinanced into lower-rate, shorter-term credit. Yet, unlike in prior years, when rate cuts led to a market-wide decline in existing mortgage rates, the 2019 ban on inter-bank mortgage transfers by regulators reduces the competitiveness across the banking sector. As each bank now has control over its issued mortgages, rates on outstanding debt are unlikely to come down as rapidly, shielding NIMs from further pressure.

Another key area of concern on mortgages is the dynamic adjustment rate mechanism for first-time home buyers by the PBOC and the China Banking and Insurance Regulatory Commission (CBIRC). This would certainly weigh on ICBC's NIMs and earnings, likely as soon as 2023. But the silver lining is the limited scale, which allows ICBC to partially offset any negative impact through its funding (i.e., deposit rates). It also eases the pressure on the property sector, in turn mitigating further property-related NPL risks for Chinese banks. Given ICBC's sizable property sector/developer loan exposure, it could end up being a net beneficiary instead.

A Heavily Discounted State-Owned Bank Offering an ~8% Yield

Having weathered a challenging 2022, the tide is turning for ICBC as the economy re-accelerates post-reopening. The initial wave of the recovery is consumption-led, and thus, retail-focused banking businesses have outperformed to start the year. But as we enter the second inning, ICBC should also come back into favor as property sector risks subside and corporate lending regains momentum. While Q4 NIMs disappointed amid the PBoC easing cycle, the pace of rate cuts is slowing, and with its core tier 1 ratio continuing to lead peers, the bank is in an excellent position for a profitability boost as well. Even if NIMs disappoint, the hefty ~60% discount to book means investors have an ample margin of safety here. And as we move into a global recession/slowdown scenario, ICBC's low beta/high dividend profile screens attractively as a destination for 'safe haven' flows. Investors willing to wait for the ICBC recovery story to play out get a well-covered ~8% dividend yield in the meantime.

For further details see:

Industrial and Commercial Bank of China: Trading At A Deep Discount With An 8% Yield