ILPT - Industrial Logistics: A Potential Value Trap

2024-01-10 17:39:13 ET

Summary

- Industrial Logistics owns and leases industrial and logistics properties across 39 states.

- Its portfolio is well-diversified and its shares are trading at a very large discount to NAV.

- Regardless, the REIT's high leverage, decreasing cash flow, and low dividend make it a highly speculative investment.

Industrial Logistics Properties Trust ( ILPT ), incorporated in 2017 and headquartered in Newton, MA, owns and leases industrial and logistics properties across 39 states.

The company's portfolio is one of the most attractive ones I have observed in the industrial REIT space and the current discount to NAV is very large. However, its high leverage, drying liquidity, decreasing cash flow, and very low dividend make an investment in this enterprise highly speculative in my view.

Portfolio

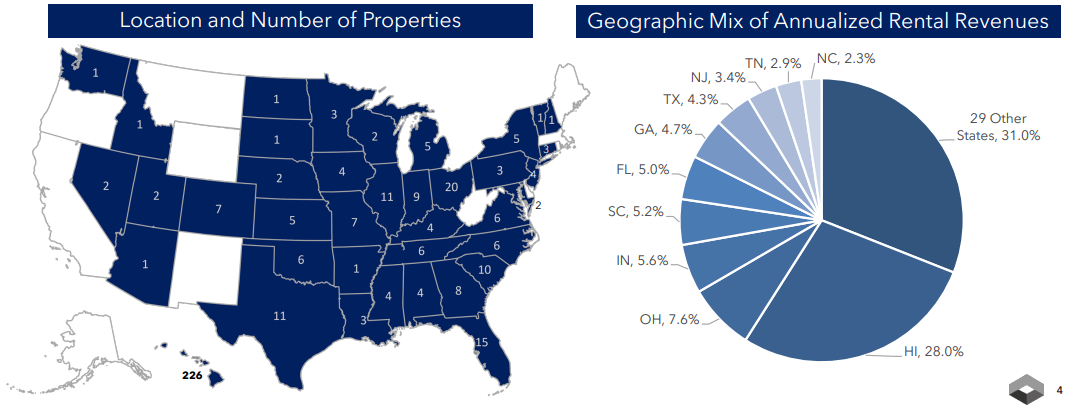

As of September 30, 2023, ILPT's portfolio consisted of 413 consolidated properties aggregating ~60 million rentable sqft located in 38 states and the island of Oahu, Hawaii. Below is the breakdown of the portfolio based on annualized rental revenue:

{kind=link}

For the REIT's current market cap, the portfolio is massive and impressively well-diversified. It's also further diversified based on property type with additional exposure to ground leases and light manufacturing:

Investor Presentation

And to top it all off, Industrial Logistics serves corporations belonging to industries other than transportation/shipping as is usual for industrial REITs. The breakdown looks pretty attractive here too:

Investor Presentation

The only area it falls short is its significant exposure to FedEx:

Investor Presentation

Performance

Regarding the REIT's long-term historical operating performance, the picture is mixed. Though a 162.5% revenue increase is decent in 6 years, operating income and cash flow performance have been underwhelming:

Arguably, this is a fairly young REIT and it might deserve some slack as expansion can be very expensive in the early years. However, more recent results give a similar picture; though rental revenue and NOI have been expanding, FFO has taken a deep dive.

Below, I present the difference between the average annual figures from the last 3 fiscal years and the latest quarterly figures annualized:

| Rental Revenue Growth |

| 53.22% |

| NOI Growth |

| 51.35% |

| AFFO Growth |

| -70.26% |

Not surprisingly, this issue is well reflected in the price performance:

That's a very large dip to simply attribute it to rising interest rates. However, the recent change in the dividend policy was likely the fuel of such a market reaction as we'll see shortly.

Leverage

Another problem with this REIT is the very high leverage it uses. With a debt-to-assets ratio of 76.38% and a debt/EBITDA ratio of 13.74x, the heavy reliance on debt and the low liquidity are evident.

Interest coverage is not accurately depicted above because of the inclusion of non-cash expenses before coverage is calculated, but the ever-decreasing ratio is useful to help us understand how liquidity has been drying up since incorporation. Additionally, the interest coverage before depreciation and amortization is 1.08x; still dangerously low.

On the bright side, its mortgages carry a weighted average interest rate of 5.5% which is low considering the REIT's substantial exposure to floating-rate debt and the current interest rate environment. Moreover, no significant maturities are approaching anytime soon. Assuming the REIT exercises its three one-year extension options regarding the principal payments coming due in 2024 (which is very likely), the next definite significant maturity would be pushed to 2027:

Investor Presentation

Dividend & Valuation

In July 2022, ILPT announced a dividend decrease from $0.33/share to $0.01/share per quarter; a distribution that results in a forward yield of 0.88%. Although the company was anticipating that it would be able to increase it back to or close to the previous distribution in 2024, this is highly unlikely as its leverage profile hasn't improved since, which was what the management claimed to be what they'd rather focus on.

A lot has already been said about the decision to cut the dividend to nearly nothing and what led to it. The only thing I would like to add is that even though AFFO has shrunk a lot lately, the payout ratio is 8.29% when it comes to the current dividend. True, anything close to $0.33 per share would quickly drive the REIT to insolvency. But there is plenty of room for a more respectable distribution, which ILPT refuses to use.

Now, largely because of this decision in my view, the shares are trading at an 8.08% implied cap rate, a very unusual level for such a diverse portfolio of industrial properties. Consider that the median implied cap rate for industrial REITs was around 5% recently and rates for such assets are forecast to average about 5% this year. So based on such a rate, the stock is trading at an 89.71% discount to NAV ($44 per share) right now.

Regardless, ~$28 per share is the highest the stock price has reached and there are no drivers in place for a fair valuation as far as I can see. I believe the market has lost faith in this enterprise and I find this sentiment justified until I see significant improvement with ILPT.

Risks

Apparently, the most important risk is related to that market sentiment. The current price may be historically very low, but I have no reason to think that the "storm before the calm" is near its end.

Another risk has to do with the REIT's biggest tenant which is responsible for one-third of its revenue. To be fair, FedEx is a big tenant and is unlikely to run into financial trouble. The most important risk here lies in the scenario it chooses to stop doing business with ILPT. Difficult, but I still need to note this risk.

Lastly, we need to be cautious regarding valuation. Right now, ILPT may not be a distressed seller, but that can change if it becomes insolvent in a high-interest environment. In such a case, our 5% cap rate assumption can prove very optimistic at best and completely out of touch with reality at worst.

Verdict

Therefore, I assign a hold rating on ILPT for now and urge investors to look elsewhere for value opportunities. No NAV discount is worth the risk that comes with investing in a highly leveraged REIT that recently decreased its dividend by 98% and has experienced a prolonged cash flow downtrend.

If you don't mind the low dividend yield, you might be interested in reading my recent analysis of Plymouth Industrial ( PLYM ) which is less risky and trades at a decent discount to NAV.

What's your take? Do you own ILPT or intend to? Why or why not? Leave a comment below and I'll get back to you soon. Thank you for reading!

For further details see:

Industrial Logistics: A Potential Value Trap