ILPT - Industrial Logistics Properties: Deep-Value REIT With Significant Upside Potential

2023-10-25 03:41:59 ET

Summary

- Industrial Logistics Properties is a deep-value industrial REIT, offering a significant margin of safety at its current stock price.

- The recent dividend cut and the looming wave of maturing debt in 2024 have contributed to the stock's decline. However, ILPT has the option to extend the debt maturities to 2027.

- Potential catalysts for improving ILPT's financial position include reducing debt through asset sales, refinancing debt on more favorable terms, or divesting the over-leveraged properties through spin-offs.

- Creates a path for management to unlock value inherent in the Hawaii assets, which offer stable, long-term cash flows with future rent growth potential and minimal recurring capex needs.

Editor's note: Seeking Alpha is proud to welcome MJM Value Investments as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

Industrial Logistics Properties Trust (ILPT) is a deep-value industrial REIT and the current stock price offers a significant margin of safety. In 2022, the company financed a large acquisition with too much floating rate debt . Assuming they default on their floating rate loans and lose the properties offered as security, a conservative estimate of the remaining net asset value ("NAV") is $13.22 per share.

Background

ILPT is an industrial REIT with 60 million square feet ("sf") of class A distribution and logistics facilities located across the U.S. ILPT's properties play a critical role in helping e-commerce companies deliver goods to their customers. The portfolio consists of 318 wholly-owned properties, a 61% interest in 94 properties held in a consolidated joint venture ("Mountain JV"), a 22% interest in 18 properties held in an unconsolidated JV, and a 67% interest in one property.

ILPT's most valuable assets are its 226 wholly-owned properties situated in Honolulu, Hawaii. These properties have consistently delivered long-term, predictable cash flow since 2003, maintaining a 96% occupancy rate. Currently, the portfolio is 98.4% occupied, closely mirroring the broader Honolulu industrial market, which stands at 99% leased. Notably, the potential for future rent growth remains high due to the limited availability of land suitable for industrial use. Rent adjustments have averaged an impressive 26% since 2017, and management has recently expressed expectations for rent increases in the range of 30-40% moving forward . Furthermore, the need for ongoing capital expenditures is minimal, as the vast majority of the properties (93% of total square footage) consist of land leased to industrial tenants.

Data from ILPT Q2-23 investor presentation; analysis, assumptions, and table produced by author.

{kind=link}

In February 2022, ILPT closed the acquisition of Monmouth REIT ("MNR"), a 99% leased portfolio of class A industrial properties containing 26 million sf, outbidding Equity Commonwealth (Sam Zell) and Starwood Capital (Barry Sternlicht). ILPT paid $4 billion ($154 per square foot "psf") representing a 4.0% cap rate on in-place net operating income ("NOI").

After the MNR acquisition, ILPT's consolidated net debt to adjusted EBITDA reached 13x. Attempts to reduce leverage by selling assets and equity interests have been unsuccessful so far. With rising interest costs eroding cash flow, ILPT cut its dividend by 97% to $0.01 per share. Recently, the stock was removed from the S&P small-cap 600 index , which sent the shares to a new 52-week low.

Industry

Fundamentals in the U.S. industrial real estate sector are robust . According to data from Cushman & Wakefield, the national vacancy rate in Q2-23 was 4.1%. The U.S. market is on pace for 490 million sf of new deliveries in 2023 against 195 million sf of net absorption (i.e., 295 million sf of inventory that remains unleased). Vacancy rates could tick up slightly if the excess inventory is not fully absorbed. The rising cost of land, material, labour, and financing have led to a 65% drop in new development starts from peak levels, which should support strong occupancy levels over the medium term. Higher interest rates are forcing companies to dial back growth plans, however, the secular drivers of demand for logistics properties remain in place. In a recent investor call, the CEO of Prologis, the largest pure-play industrial REIT, stated that "the thing that encourages me and we will have to see… is that companies are not shutting down their dialogue with us in terms of their long-term needs." Given the robust supply-demand dynamics in the industrial real estate sector, Prologis is forecasting market rent growth of 7% in 2023.

The replacement cost of industrial properties has significantly risen and continues to stay high, which will serve as a basis for future rent increases. To illustrate, if it costs $150 psf to construct a standard logistics facility, developers must secure lease agreements with net rents exceeding $10 psf to meet their return targets (assuming a 7% developer's yield). This compares favourably to ILPT's in-place rent of approximately $7.20 psf.

During 2022, cap rates for top-tier industrial properties ranged from 3% to 4%. Subsequently, they have widened due to the uptick in the U.S. 10-year yield. Nevertheless, cap rates for high-quality properties with rents below market rates now fall in the range of 4-5%, representing an increase of only 100 basis points, in contrast to the 200-300 basis point shift in the 10-year yield. In June 2023, Prologis paid $3.1 billion ($221 psf) to acquire a 14 million sf industrial portfolio from Blackstone , which represented a 4% cap rate on in-place NOI but a projected 5.75% cap rate when adjusting to today's market rents. At the current stock price, ILPT is valued at a 7.5% cap rate on in-place NOI ($75 psf). ILPT increased rents by 47% in 2022 and management expects to mark-to-market lease expirations by at least 20% in 2023. This would imply an average market rent of $8.65 psf for their portfolio, which is equivalent to a 9.0% cap rate on forward NOI (assuming ILPT can rollover expiring leases at market rents).

Financials

To finance the MNR transaction, the Mountain JV took out a $1.4 billion floating rate loan secured by 82 properties. Additionally, ILPT took out a bridge loan subsequently refinanced in Q3 2022 by a $1.1 billion floating rate loan and $135 million mezzanine loan secured by 104 wholly-owned properties ("2024 Loan"). Interest rate caps have effectively fixed the interest rates on both loans at ~6.15% until their initial maturity dates in March 2024 and October 2024. ILPT must purchase new interest rate caps, likely with $72 million of unrestricted cash on the balance sheet, in order to exercise the loan extension options to 2027.

When analyzing an over-leveraged company, it's critical to evaluate the quality of the underlying assets to determine whether they can service the debt. ILPT's industrial properties generate stable, long-term cash flows. The portfolio is 99% leased with a weighted average lease term of 8.4 years and 77% of their revenue comes from investment-grade tenants (FedEx (FDX), Home Depot (HD), Amazon (AMZN)). Moreover, ILPT benefits from net lease contracts that offer some protection from rising operating costs and include annual rent escalators, which are likely to rise to 3-4% per year if inflation remains above target.

At Q2-23, LTM cash available for distribution, a proxy for free cash flow to equity, was equal to $33 million and ILPT had $139 million of restricted cash available to fund future capex (4.8x LTM capex). If interest rates on their floating rate debt reset near today's market rates of approximately 8.00% (300 bps spread over 500 bps SOFR), annual interest expense would increase by $53 million. The resulting cash flow shortfall would be mostly offset by an estimated $15-20 million increase in annual cash NOI as 2022-24 lease maturities are marked-to-market. In Q2-23, ILPT successfully refinanced four properties within the Mountain JV, locking in a fixed rate of 6.25% on an interest-only basis for a 7-year term. This development suggests that ILPT could potentially secure refinancing for their floating rate loans at an interest rate lower than 8.00%.

Valuation

Let's examine a hypothetical scenario if ILPT were to default on both floating rate loans. They are non-recourse to ILPT, with certain exceptions related to environmental indemnities, fraud, misrepresentations, and willful misconduct ("Bad-boy Carveouts"). Therefore, any borrower liability is limited to the real property offered as security for the floating rate loans (a common structure for commercial real estate loans). Assuming ILPT and the Mountain JV default on their floating rate loans, but don't trip any of the Bad-boy Carveouts, ILPT would lose its 100% interest in 104 wholly-owned properties (including 35 properties located in West Oahu) and its 61% interest in 82 properties in the Mountain JV.

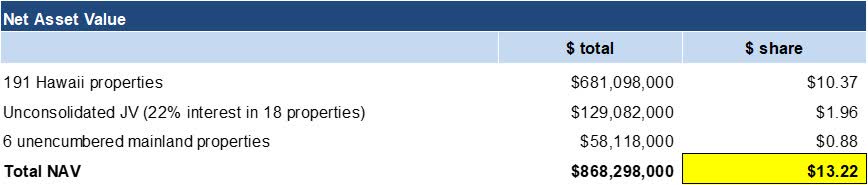

The estimated NAV for the remaining assets ("Leftover Portfolio") is as follows:

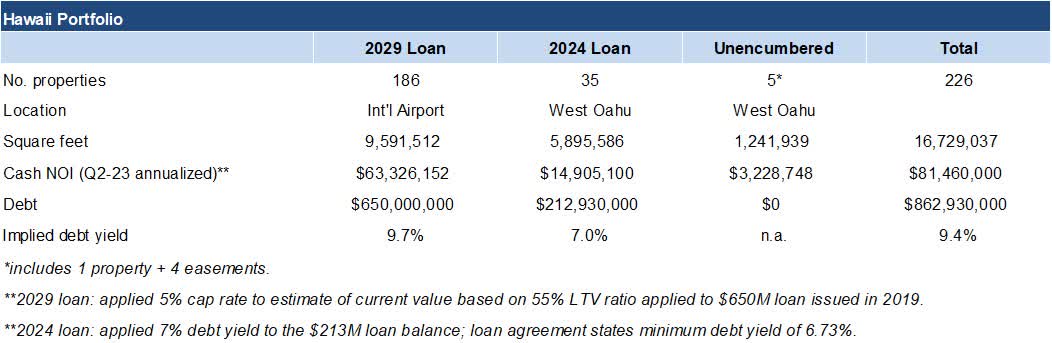

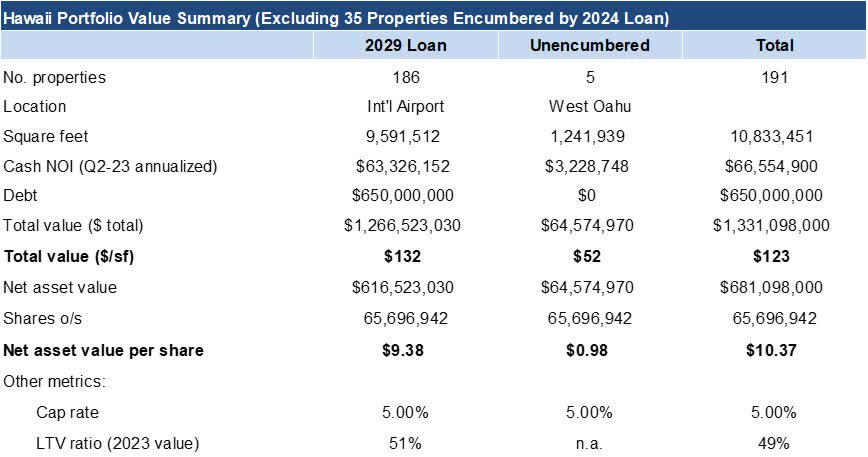

191 Hawaii Properties

186 properties comprising 9.6 million sf are located in close proximity to the international airport in Honolulu. These properties are encumbered by $650M of fixed rate debt (4.31%) , which is set to mature in 2029 ("2029 Loan"). The loan was issued in January 2019 by a syndicate of banks including Morgan Stanley (MS), Citi (C), UBS (UBS), and JPMorgan (JPM). Assuming a loan-to-value ratio of 55%, which falls within the mid-range of a 50-60% LTV, the implied value of the portfolio in 2019 was $1.08 billion. Factoring in a 3% nominal growth rate over the 5-year period from the start of 2019 to the end of 2023, the present value of the portfolio amounts to approximately $1.3 billion ($132 psf). An industrial broker working for Colliers International in Hawaii stated that industrial land parcels within a 5-mile radius of the international airport currently trade for $175-$200 psf. In 2020, Amazon acquired a 14-acre industrial site near the international airport for $205 psf. Deducting the outstanding $650 million loan, the resulting NAV is $617 million . At a 5% cap rate, the estimated annual cash NOI is $63.3 million (78% of annualized Q2-23 cash NOI for the entire Hawaii portfolio).

1 property (plus 4 easements) located in the West Oahu industrial submarket is a land lease that totals 1.2 million sf (28.5 acres). The property is unencumbered and the NAV is $64.6 million ($52 psf) based on a 5% cap rate applied to estimated annual cash NOI of $3.2 million. The same industrial broker stated that land parcels in West Oahu currently trade for $50-$60 psf.

Data from ILPT Q2-23 investor presentation; analysis, assumptions, and table produced by author.

{kind=link}

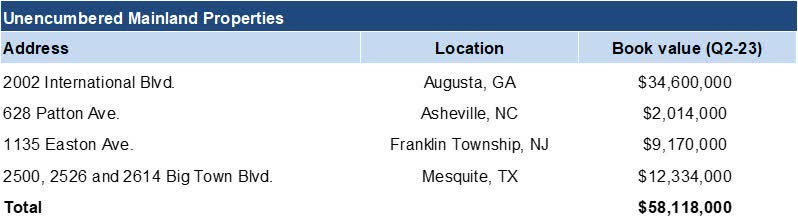

23 Mainland Properties

Attributing no value to the 17 encumbered by $700M of fixed rate debt maturing in 2032. Based on book value, the NAV of the 6 unencumbered assets is $58 million. These assets appear to be properties under construction or slated for redevelopment.

Data from ILPT Q2-23 quarterly report; table produced by author.

{kind=link}

61% interest in 12 Properties (Mountain JV)

Attributing no value to these assets (portfolio was purchased at a 4% cap rate). Properties are encumbered by $350 million of fixed rate property-level debt maturing between 2030 and 2038.

22% interest in 18 Properties (Unconsolidated JV)

Based on book value, NAV of $129 million ($93 psf). Includes write-downs totaling $48M in 2021-22. These assets total 11.7 million sf and are 99% leased with 6.5 years of weighted average lease term. Portfolio encumbered by $504 million of debt or $111 million at ILPT's 22% share.

67% interest in one New Jersey property

Attributing no value to this property.

To summarize, the NAV of the Leftover Portfolio is estimated to be approximately $868 million or $13.22 per share.

{kind=link}

Key Risks

Management's failure to uphold its fiduciary duty and make rational decisions to protect shareholder value. ILPT is externally managed by RMR Group, which provides both business and property management services. The reputation of RMR Group is mixed, raising the possibility that they may attempt to salvage the over-leveraged properties at the expense of the equity value in the Leftover Portfolio. While it's worth noting that RMR Group is incentivized through management fees tied to stock price performance, there remains a potential risk.

Industry downturn caused by an economic recession. Market rents fell 15-20% during the GFC when industry fundamentals were much weaker. ILPT's high occupancy rate, investment-grade rent stream, and below-market rent should offer some protection.

Tenant concentration is a risk, given that FedEx (S&P: BBB) contributes approximately 30% of the total revenues. FedEx does not have any imminent lease maturities, and its average lease maturity extends to 2027. In the past, ILPT has achieved a 90% tenant retention rate. Even in the event of FedEx vacating some properties prematurely, ILPT has a proven track record of re-leasing vacant properties within a quarter or two.

Catalysts

Debt reduction via proceeds from asset sales / new joint ventures.

Refinance the floating rate loans with long-term, fixed-rate debt.

Spin-off of heavily indebted properties.

Conclusion

While uncertainty surrounds ILPT's management of floating rate loans in the short term, they have ample cash on hand to purchase interest rate caps and extend maturity dates to 2027. I expect them to secure favourable loan refinancing terms, thanks to strong industry fundamentals, and future rent growth should help offset higher debt service costs. Despite the current stock price suggesting financial distress, the company can navigate these challenges through asset sales or improved asset refinancing. I believe the current price provides investors with downside protection and represents an attractive entry point to invest in a valuable class A logistics property portfolio offering significant upside potential.

For further details see:

Industrial Logistics Properties: Deep-Value REIT With Significant Upside Potential