IFNNF - Infineon Is Still A Buy!

Summary

- Infineon should benefit from the currency development.

- The CEO announced that they are looking for inorganic acquisitions.

- Infineon is still benefitting from the chip shortage. The 2022 revenue target has been revised upwards. Our buy target is confirmed.

Here at the Lab, today we are back to comment on Infineon Technologies AG's ( IFNNY ) ( IFNNF ) latest development. We still believe that the company is a Long-Term Winner based on five criteria:

- Its leading position in electric vehicle production,

- Our MACRO call based on the fact that more semiconductors are going into our everyday life,

- The EU Chips Act which will support the European Union dependency on semi imports ( as a reminder , the EU chip production accounts for only 8% of the total global capacity and is down on a yearly basis since 2000 ),

- On the MICRO level, Infineon is a well-diversified company both in terms of end-clients (none exceed 10% of the company's total turnover) and in terms of geographical exposure,

- Its solid order backlog.

In Q1 2022, when we initiated our coverage of the company, its backlog was three times the revenue line and stood at €31 billion, after three quarters, Infineon's backlog reached €43 billion (with 3.1x our 2023 revenue projection).

In addition, the company outperformed Wall Street's consensus estimates in seven of the last eight quarters. However, today, we are not commenting on the latest financial results (we already did and were impressed - Q3 results too ), but we focus on the latest news released by the company CEO Jochen Hanebeck.

In an interview published on Wednesday, 28 December by the German newspaper Frankfurter Allgemeine Zeitung, Infineon's CEO said that the German chipmaker is constantly " looking " for inorganic M&A. We never really talked about M&A optionality for Infineon but this is an optionality to price in.

What Infineon is looking for?

It is true that Infineon already has a strong position in the field of semiconductors, but according to the CEO, nothing is so good that it cannot be improved . In particular, the company aims to grow in data centers, renewable energy, autonomous driving, electromobility, and IoT, in which objects are connected to other communication networks or the Internet. Therefore, " there are a whole series of fields that we have defined and in which we are actively looking to further expand our portfolio ", concluded the top manager. The CEO said that they are looking also at the start-up level; however, Hanebeck did not mention individual potential acquisition targets.

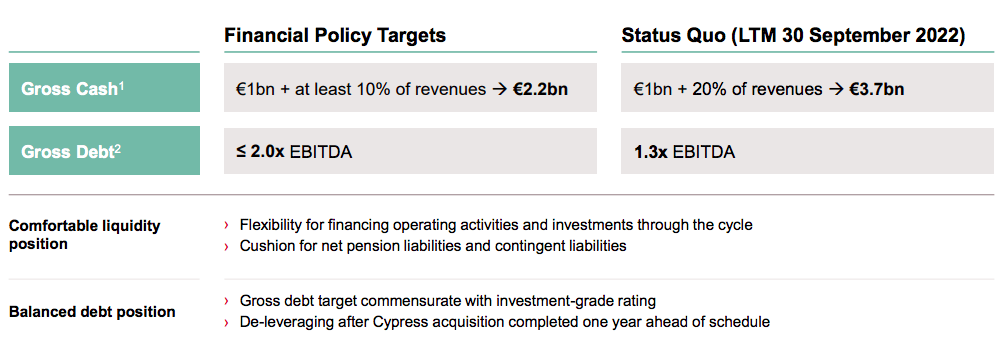

Currently, Infineon has a solid cash generation (just in Q4, free cash flow reached €709 million). In the fiscal year that ended in September 2022, the company reported a profit of €2.18 billion, up from €1.17 billion compared to the previous year, and revenues of €14.2 billion from €11.1 billion. The German chipmaker is willing to spend up to a few billion on the right M&A target, and this can also be financed by debt. Indeed, the company has a solid balance sheet with a gross financial debt that decreased on a quarterly basis and also on a yearly basis. Infineon's pension is almost fully funded and there is financial flexibility on the company's investment grade rating through the cycle.

Infineon Debt Ratio (Infineon Q4 Results Presentation)

{kind=link}

Aside from the M&A optionality, like its competitors, Infineon benefited from the global semiconductor shortages, but several chipmakers have recently warned that demand is easing. With rising energy costs and interest rates, product demand has recently weakened; however, we believe that the leading microchip supplier to the automotive industry will continue to outperform thanks to the important supply-demand imbalance in the EU. We also believe that we should price the $/€ exchange rate. As a result, based on a 1.05 rate, Infineon might increase its 2022 revenue estimate by €500 million and reach approximately €14 billion with an operating margin of over 23% (consensus is estimating a 22.4% margin). According to our analysis, approximately €140 million of the €500 million upgrades of the turnover guidance derive from the exchange rate improvement. Here at the Lab, we estimate that the new guidance implies an upgrade of the 2022 EBIT consensus estimate of around 8-9%.

Conclusion and Valuation

Since the beginning of the year, the stock is down over 33%, but in the last three months, it has recovered 22.7% of its market value. We continue to be ahead of the Wall Street estimates, and we reiterate our buy target at €48 per share. We still believe that equity research analysts should re-price the German chipmaker. Last time, we lowered our PE ratio (now in line with the company's last three-year average), and by valuing the company with a 2024 EPS of €3, we decide to maintain our overweight and then confirm our valuation.

For further details see:

Infineon Is Still A Buy!