STM - Infineon Q3 Earnings: A Solid Quarter Unchanged Outlook And Massive SiC Investments

2023-08-05 10:36:46 ET

Summary

- Infineon continues to report strong growth while meaningfully expanding margins and heavily investing in capacity expansion.

- The company's strong competitive positioning in the semiconductor industry, particularly in automotive and industrial segments, is driving better-than-expected results.

- Infineon is increasing its investments in silicon carbide technology, a fast-growing semiconductor vertical, to maintain its market share and boost growth in power semiconductors.

- Infineon remains ridiculously undervalued after falling by 13% in the two trading days following its Q3 results.

Investment thesis

I maintain my strong buy rating on Infineon Technologies AG ( IFNNY ) and update my revenue and EPS estimates following the company’s Q3 results. The company delivered a quarter that aligned with its expectations, allowing it to reaffirm its FY23 guidance. Yet, despite the solid financial results, which beat my EPS estimate by 23%, the share price plummeted around 13% in the following two trading days.

As for my investment thesis, this is what I previously wrote and not much has changed since:

The excellent competitive positioning of the company makes it a winner in the semi(conductor) industry. Tailwinds from its automotive and industrial segments are driving better-than-expected results for this year and most likely also for the years after. Infineon even holds an impressive 31% market share in the power semiconductor market, a very important product for many different industries. These industries include automotive, renewables, datacenter, and IoT (Internet of Things). And Infineon is not just a player in these industries, but it holds a significant market share in these fast-growing markets with it holding the largest market share in automotive semiconductors at 12.4%, and its power semiconductors being responsible for powering 50% of currently installed solar and wind energy systems. The broad product portfolio of Infineon covers all verticals of the energy conversion and usage business and the automotive semiconductor industry, which positions it well for impressive above-average growth in the coming years.

Add to this a strong management team that knows exactly where it needs to steer the company and which segments it needs to invest in to boost growth, and we end up with an excellent opportunity for investors. Yet, this does not seem to be entirely recognized by the market. Also, with additional funding from the European Union and the US government to increase domestic semi production, Infineon is poised to benefit as it plans to increase manufacturing capacity in both regions.

One important development contributing to the bullish narrative explained above is the company's increased investments in Silicon carbide technology, one of the fastest-growing semiconductor technologies today. Infineon already has a firm market share in silicon carbide, which allows it to fully benefit from growth in this vertical, and through these new investments and long-term agreements with customers, it should be able to maintain its market share in this fast-growing industry and boost its overall growth.

In this article, I will take you through the latest developments and financial results and update my estimates and view on the company accordingly.

For a more in-depth analysis of the company’s fundamentals, products, and long-term growth drivers, I recommend reading my initial coverage of the company here . This article will primarily focus on the latest quarterly results and developments.

Investors have nothing to complain about as Infineon continues to execute close to perfection

Infineon reported revenue of €4.1 billion for its fiscal Q3, up 13% YoY, down 1% sequentially, and in line with its own guidance. Also, it performed roughly in line with my estimate, although it fell short by €71 million or about 2%.

Just like in the first half of the year, Infineon continued to see strong momentum in its decarbonization and automotive products. The secular tailwinds driving these industries, like electric vehicle growth, continued investments in ADAS, and the shift to green energy solutions like solar, remain strong. As a result, Infineon reported strong growth rates for its Automotive and Green Industrial Power segments, growing 25% and 30% YoY, respectively, while also reporting sequential growth.

In automotive, Infineon is seeing no weakness in demand at all, which also allowed the segment result margin to expand by 390 basis points and to come in at 27.4%, resulting in the segment result increasing 46% YoY as well. The continued semiconductor shortages in the industry give Infineon slightly more pricing power, which is what is boosting its margins. Yet, these shortages are easing so we might see a slight decline in automotive margins over the next several quarters, although nothing too extreme.

Important to note is that the automotive segment result margin was down from a record quarterly level of 31.1% in Q2 as this one saw several non-recurring positive impacts, and so this decline was expected.

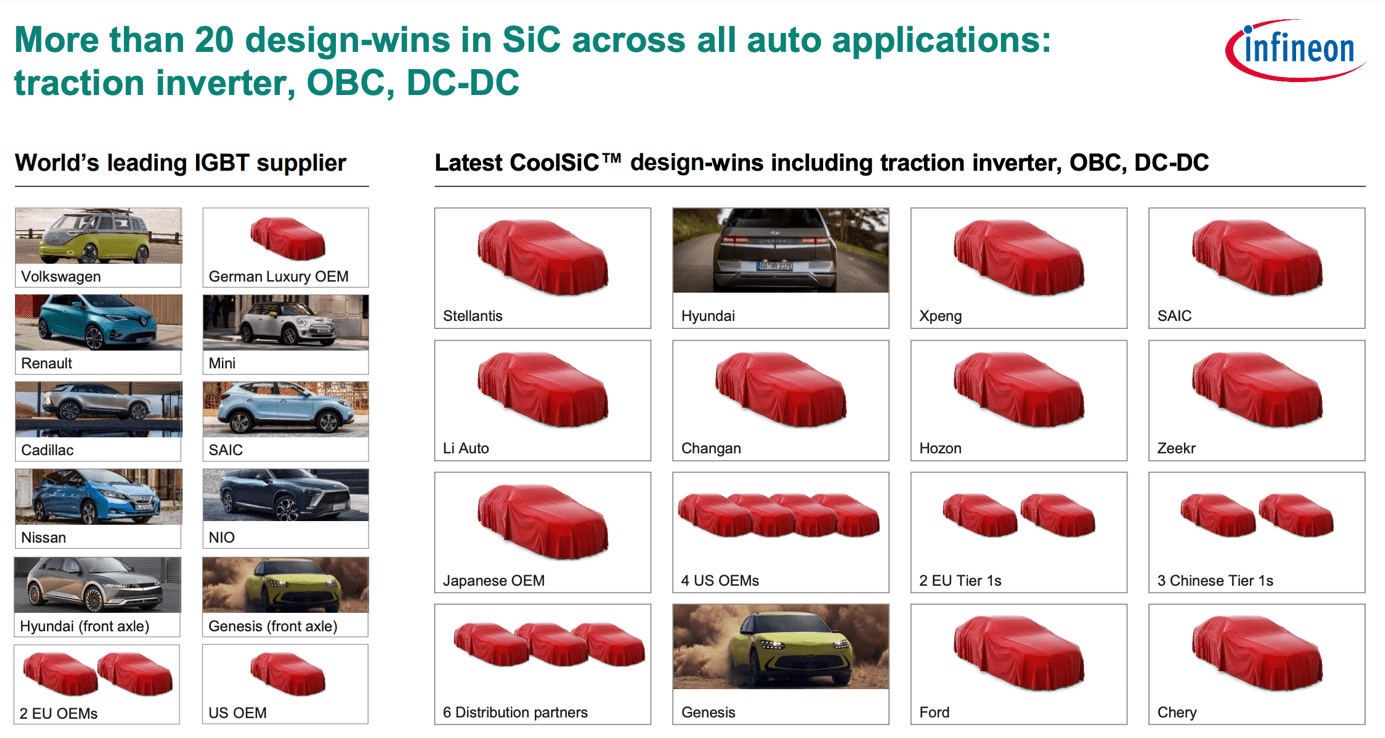

Infineon's automotive design wins (Infineon)

{kind=link}

Still, margins remain incredibly strong, driven by high demand, highlighted by the many new design wins. Infineon remains the global leader in automotive semiconductors with a 12.4% market share and continues to gain share every quarter. It is also the largest provider of automotive semiconductors in China, the largest and fastest-growing automotive market. Furthermore, as Infineon is seeing no easing in demand, I expect automotive to remain a growth driver in the fourth quarter and going into its fiscal FY24.

Automotive market share % (Infineon)

Looking at the longer term, Mordor Intelligence believes the automotive semiconductor industry will grow at a CAGR of 14.43% through 2028. With the segment now accounting for over 50% of Infineon’s revenue as of Q3, the strong growth in automotive will also be a crucial driver of Infineon’s overall growth. And whereas this kind of revenue exposure to a single end-market would generally be a reason for concern, the strong tailwinds and expected continued growth in automotive semiconductors for the foreseeable future make this exposure a crucial driver for Infineon and far from a negative. The company through this exposure is well positioned to benefit from this industry growth.

The second segment that is very much supported by these secular growth drivers is the Green Industrial Power segment, which is exposed mainly to decarbonization products. This segment also reported an excellent Q3 with revenue growing 30% YoY to €565 million, making it the fastest-growing segment for Infineon in Q3. Meanwhile, the segment result margin also remained excellent at 30.3%, making it the most profitable for Infineon. Demand for the decarbonization products continues to be driven by growing demand for renewable energy and power infrastructure. Regarding Infineon’s role in these energy supply shifts, this is what I wrote in my previous article :

To also put Infineon’s market position in this industry into perspective, as explained in my previous article, Infineon is responsible for powering 50% of the currently installed capacity in wind and solar energy. In addition to this, Infineon's power semiconductors are also used for 2/3 of the electricity grid infrastructure, including electric charging. Clearly, Infineon has great exposure to the decarbonization trend and is well-positioned to benefit from growth in green energy generation and electricity grid infrastructure growth going forward.

During the Q3 earnings call, management once more confirmed that it is by far the largest power semiconductor supplier for solar applications, with supply agreements for the solar end market alone amounting to over €3 billion. Crucial to this strong market position is the company’s leadership in silicon and silicon carbide power semiconductors as it continues to hold a market share of 32% in the power semiconductor market, far ahead of second place STMicroelectronics ( STM ) with a 20% market share. This strong market position should mean that Infineon continues to benefit from growth in solar applications.

Power semiconductor market share % (Infineon)

Meanwhile, the market environment for computing, consumer, and communication-related businesses is much more challenging as these are more exposed to the slowdown in IT and consumer spending. Still, Infineon is seeing a comparatively strong performance, highlighting its portfolio strength. Still, growth in Power & Sensor Systems and Connected Secure Systems came in much weaker as these reported a revenue decline of 10% and a very minimal increase of 4%, respectively.

The decline in Power & Sensor Systems is largely driven by an ongoing inventory contraction on the power side, which has a lot of exposure to electronic devices like smartphones and PCs. It is very well known that these industries have been struggling quite a bit and this also impacts Infineon, although the impact was less severe than anticipated by management as the sequential decline was limited to just 1%, indicating a possible underlying improvement. Nevertheless, this is expected to remain a drag on this segment over the next couple of quarters as well, with management seeing no quick recovery as customer inventory levels remain inflated. Also, despite diligently managing production capacities and inventories, the segment result margin dropped by 630 basis points to 20.8%, leading to a 31% decline in the segment result. Yet, this should not come as a surprise to investors or analysts. This weakness was long anticipated and is simply the result of cyclical weakness.

At the same time, the Connected Secure Systems segment saw quite a negative sequential development as revenue dropped by 14% after a record Q2 but was still up 4% YoY. The sequential decline was driven by a weaker development in predominantly Wi-Fi components and microcontrollers. As a result of the lower revenue base, the segment result margin fell 310 basis points but was still up significantly YoY and stood at 25.1%, which is really nothing to complain about. Furthermore, growth will most likely remain subdued over the next few quarters as demand for IoT devices remains low. Yet, to long-term investors, this does not have to be an issue as the long-term outlook for the segment remains impressive, driven by growth in IoT devices and the development of AI.

Moving to the bottom line, the segment result margin came in at 26.1%, roughly in line with management’s guidance of 26%. The gross profit margin was 44.5%, a solid improvement from the year-ago quarter. At the same time, this was down from Q2, but this was a tough comparison due to currency fluctuations and heavy investments. Therefore, I believe it is best to focus on the YoY development and take out any seasonal impacts. And looking at this, as an investor, I am happy with the 130-basis points margin expansion. As a result, EPS was up 39% YoY to €0.68, 23% above my €0.55 estimate.

Furthermore, free cash flow did improve from Q2 and came in at €326 million in Q3. Management used this cash flow to repay a €750 million bond, which also resulted in the cash balance on the balance sheet decreasing to €3 billion. Though, this is still a respectable level, especially considering that Infineon also only holds a total debt of €4.7 billion, resulting in a very healthy net debt position of €1.7 billion. The balance sheet remains in excellent health and should provide Infineon with plenty of cash to fund its investments and dividends.

Finally, Infineon continues to see its backlog decline to healthier levels after the inflated levels during the COVID-19 pandemic, in which demand for electronic products boomed. During the quarter, the backlog declined by €4 billion but still stood at €32 billion or 2x its annual revenue, providing the company with an impressive buffer to offset any negative demand impacts. Yet, one factor that also jumped out to me is the inventories as the reach went up from 143 days to 149 days, which right now is a normalization of the inventory levels, but it will be crucial to monitor these if demand drops further.

Infineon is massively increasing its SiC investments to benefit from industry growth

Most crucial to Infineon for maintaining its strong market position in power semiconductors for automotive and decarbonization applications is the development of silicon carbide (SiC) technologies, one of the fastest-growing verticals of the semiconductor industry. The SiC semiconductor industry is projected to grow at a stellar 23.8% CAGR through 2030. Without getting too much into technicalities, the technology is a superior solution compared to silicon and it is excellently suited for sustainability, electrification, and power semiconductors. As a result, the technology is in exceptionally high demand by automotive OEMs and industrial customers.

Infineon is massively increasing its efforts in this industry and continues to see impressive design wins in silicon carbide technology. It is seeing high demand for its industrial SiC solutions as this business grew 60% YoY in Q3. Both industrial and automotive are pushing demand for Infineon’s SiC products through design wins and monetary commitments. This is what management said during the earnings call regarding this massive market potential:

The market for power semiconductors continues to show accelerating growth driven by decarbonization. Within this market, silicon carbide shows impressive and unabated growth in automotive and in a broad range of industrial applications like solar energy storage systems, high-power EV charging and more to come.

For FY23, Infineon expects to report €500 million in silicon carbide sales as it is unable to supply more due to capacity constraints. This revenue level would mean that it currently holds a significant market share of approximately 31.5% , already above its earlier set goal of 30% by 2030. Furthermore, this would mean the company has to grow this to €2.8 billion by 2030 to maintain and reach its goal of a 30% market share, going by today’s SiC industry growth estimates.

Yesterday morning, Infineon set a very important step in achieving this as it announced the plan to build a new state-of-the-art 200-millimeter silicon carbide power fab in Malaysia. In 2022, the company already announced the build of a fab in Kulim, Malaysia, but it is now investing an additional €5 billion over the next 5 years to further expand this fab, which should make it the largest silicon carbide fab in the world and this should give Infineon a significant capacity boost and the potential to produce over €7 billion worth of silicon carbide semiconductors annually by 2030. This is what management said regarding the factory's potential:

With this site, we will be able to leverage our strong technological base like the best-in-class silicon carbide trench technology, broadest package and customer portfolio and deepest and widest application understanding together with an unprecedented scale and factor cost advantage. Together with our well diversified substrate supplier base, we are convinced that we are set up for a silicon carbide market leadership position.

Crucial to this decision to expand its fabrication plans is the €5 billion in design win volume and €1 billion in prepayments management already has for silicon carbide products from new and existing customers. Among these customers are six leading automotive brands, among which are three Chinese brands and industry giant Ford, with all of which Infineon has made long-term agreements, which secures a lot of the demand and future revenue potential. The certainty and value of these deals should not be underestimated. Furthermore, it has also made large deals with decarbonization giants like SolarEdge and three leading Chinese photovoltaic and energy storage systems companies, further boosting its revenue potential.

For 2025, management aims to report €1 billion in silicon carbide sales, double the expected FY23 result. This should be boosted by the first phase of the Malaysia fab being completed and operational in the second half of FY24.

Outlook & valuation

Management is not seeing a slowdown in decarbonization and automotive products for the remainder of the year. Yet, at the same time, the other two segments are seeing no immediate recovery with exposure to personal electronics and IT budgets. The result is that management guides for flat sequential growth in the fourth and final fiscal quarter of its FY23. Therefore, revenue is projected to come in at around €4 billion, with a segment result margin of around 25% as management further ramps up investments.

This means management maintains its FY23 outlook and expects revenues of around €16.2 billion, an adjusted gross margin of 47%, and a segment result margin of 27%. Meanwhile, FCF is expected to be slightly higher than anticipated at around €1.2 billion or €1.7 billion for adjusted FCF.

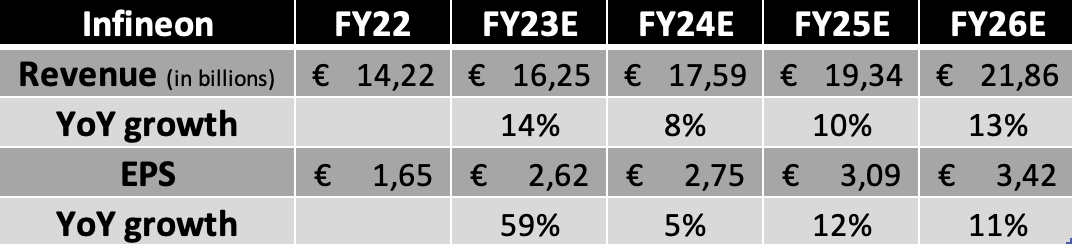

Following these Q3 results, the Q4 and FY23 guidance issued by management, and the promising developments in SiC products and capacity, I now expect the following financial results through FY26.

Financial estimates (By Author)

{kind=link}

(This includes Q4 revenue of €4.09 billion and EPS of €0.61)

Shortly explaining these estimates, I now expect Infineon to report FY23 revenue of €16.25 billion, slightly down from my previous estimate but still up 14% YoY. This represents my expectations of a very similar Q4 compared to the last quarter as growth in automotive and decarbonization remain strong while the other two segments continue to struggle for traction. Yet, I expect these two segments to start reporting a gradual recovery from the start of FY24 onwards, while growth in decarbonization and automotive will remain strong in FY24, although growing at a somewhat slower pace than we have seen this year. I expect these growth rates to sit in the high single digits for automotive and mid-double digits for decarbonization products, partly due to tough comparable FY23 quarters.

Investment firm Jefferies shares my bullish growth outlook for the company as it recently upgraded Infineon among others as it sees surprisingly strong demand for 2024 and 2025, driven by structural drivers like “AI, cloud computing, edge computing, IoT, EVs, ADAS, renewable energy, and VR/AR, amongst others”.

Also, I expect SiC revenues to start accounting for a more significant part of the revenue from FY25 onwards as production capacity gets boosted by the Malaysia fab. I see SiC as a great long-term growth driver, partly due to Infineon’s already strong market share and long-term agreements. Yet, these new SiC products will be replacing some of Infineon's legacy products, which is why growth will be somewhat limited.

As for EPS, I have upgraded this quite meaningfully for FY23 due to the impressive Q3 beat. I expect to see a slight sequential decline in EPS in Q4 due to increased investments, but this should continue to show strong YoY growth rates. Yet, this will make it hard for Infineon to keep up this growth in FY24, especially as margins in FY23 were incredibly high. I expect these to come down slightly as the demand environment, particularly in automotive, normalizes. Still, I have upgraded my long-term EPS estimates as I believe Infineon has strong pricing power compared to many of its peers, which should allow it to keep expanding margins. Overall, I think the company’s long-term growth targets should be easy to achieve.

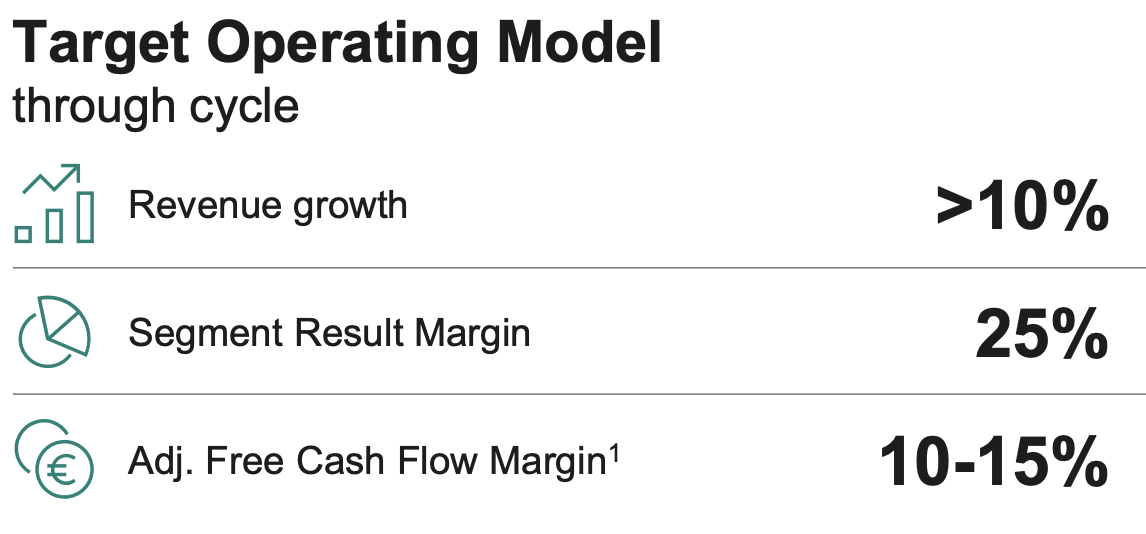

Infineon's long term targets (Infineon)

{kind=link}

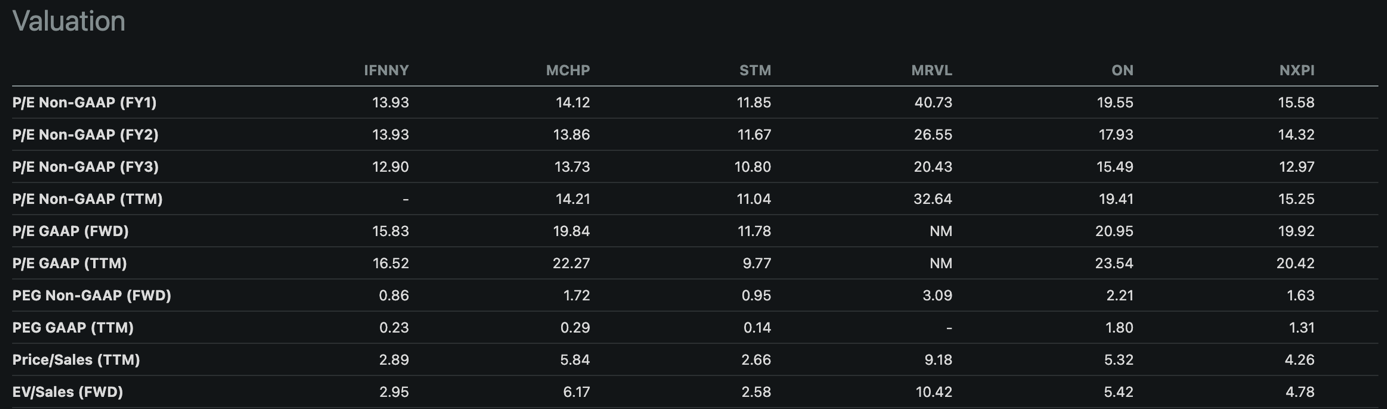

As for the valuation, following the massive drop in the share price following the Q3 results, which erased all the gains from the last couple of months, shares are now valued at a forward P/E of just 13x my FY23 EPS estimate. This means the company is now valued at a discount to almost all its peers despite holding one of the strongest market positions. Also, it is valued at almost 50% below its 5-year average.

No matter how you look at it, the company is incredibly undervalued and underappreciated as are most of its peers. These companies lack the incredible daily headlines we see from the likes of Intel ( INTC ), Nvidia ( NVDA ), or AMD ( AMD ), which causes them to often fall behind the rest of the semiconductor industry, completely unjustified.

Valuation peer comparison (Seeking Alpha)

{kind=link}

As discussed in previous articles, considering all aspects, Infineon should be valued at a forward P/E of at least 20x, which still sits below its 5-year average. The growth outlook remains excellent, and the company holds leading market positions across its segments. In my view, nothing has changed since my previous article, apart from the company’s increased investment plans in SiC semiconductors, which I view as a positive.

Based on this belief and my FY24 EPS estimate, I calculate a target price of €55 per share, up from a previous €50 due to an improved EPS outlook and leaving an upside of 60% from a current share price of €34,30.

Conclusion

Infineon reported very decent Q3 financial results, including no major surprises. Yes, the company’s performance weakened compared to Q2, but this was due to a number of factors that benefitted the company in the first half of the year. Therefore, I believe investors should be comparing the quarterly results on a year-over-year basis, and this is still looking very good with significant margin expansion and impressive growth in its leading segments.

With only a few adjustments needed to my investment thesis following this third fiscal quarter, I continue to be incredibly bullish on the company’s long-term potential and its short-term resiliency, driven by its exposure to secular drivers in the automotive and decarbonization markets, as well as silicon carbide technologies.

Considering the undervaluation of the shares and its potential for continued growth, I maintain a strong buy rating on the stock. With a target price of €55 per share, representing a 60% upside from the current price, Infineon offers an attractive investment case with a highly favorable risk-reward profile. The 13% share price drop following its earnings release is completely unjustified and presents a great opportunity to investors.

For further details see:

Infineon Q3 Earnings: A Solid Quarter, Unchanged Outlook, And Massive SiC Investments