IFNNF - Infineon Technologies AG: Higher Guidance To Price In

2023-06-08 14:25:02 ET

Summary

- Micron Technology is confident about the long-term earnings trend.

- Infineon decided to raise its 2023 guidance.

- Our buy rating target is confirmed. Equity research analysts should re-price Infineon.

Since our publication called Infineon ( OTCQX:IFNNY ) ( OTCQX:IFNNF ) Is A Screaming Buy released in early August 2022, the company delivered a total return of more than 34% (including its dividend payment).

Mare Evidence Lab's previous analysis

{kind=link}

I nfineon Technologies AG (was and still) is one of Mare Evidence Lab's top picks. Joking aside, the company benefited from multiple factors, starting from Micron Technology CEO who explained that he is confident about the long-term earnings trend and predicted that the memory chip sector will likely reach a peak in 2025 in market size. In the mind time, inventories are improving and Micron's CEO also foresees a better balance on supply/demand. In addition, Nvidia's data center business, which includes AI chips, has continued to grow, suggesting it could continue to benefit heavily from software projects. During the analyst call, Nvidia CEO said AI is at an " inflection point " prompting companies of all sizes to buy Nvidia chips to develop machine learning software. He also indicated that growth in data centers is expected to accelerate in 2023, and this has clear and positive implications for Infineon (and for the whole semis sector).

Having recently analyzed STMicroelectronics, German Infineon also lagged on stock price appreciation within the sector. In detail, the company underperformed the PHLX Semiconductor index by almost 50% (Fig 1) and we believe this is not justified.

Infineon and PHLX Semiconductor index YTD perf.

Source: Mare Evidence Lab's Analysis - Fig 1.

One of the main reasons for Infineon's buy rating is related to the EU Chip Act . The United States already carried out its Chips and Science Act , with a total figure of $52 billion, and the first works have already been performed on a few production plants. Semiconductor stocks were under pressure again as tensions between China and Japan. What we are living in is a real technological cold war between Beijing and other Western countries. Precisely to reduce the EU's dependence on Asian and U.S. semiconductors, following the problems in the supply chain that have damaged European companies, the Old Continent aims to relaunch the entire chip industry. The European semiconductor law was approved more than a year ago (February 2022), but only in the last month, there was the final green light. In detail, the EU chip act approved a €43 billion allocation to create the European supply chain of chip design and production. The goal is to double the production of semiconductors by 2030, building new factories, strengthening those already operating in the sector, and supporting companies and startups that develop software and hardware in the sector. The EU Commission calculated more than 1,000 billion chips were manufactured in the world in 2021, almost 140 for every person on Earth. Demand is also constantly growing. To date, if design and research are concentrated in the United States, production is in the Asian hands with 60% of the world's chips manufactured in Taiwan. This framework alone should support a re-price for the German chip lab.

Infineon's latest results

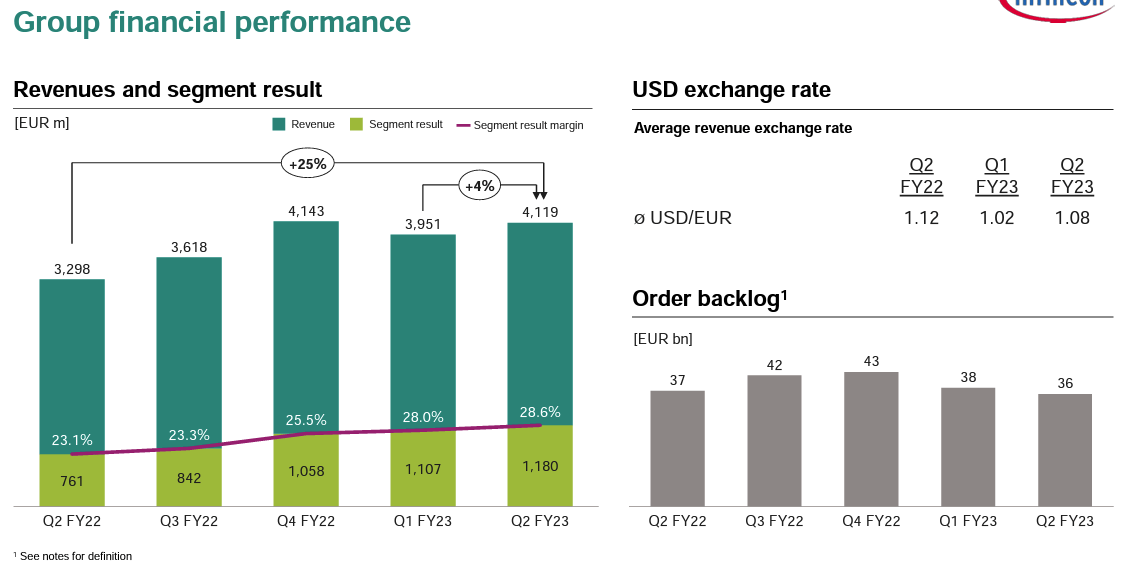

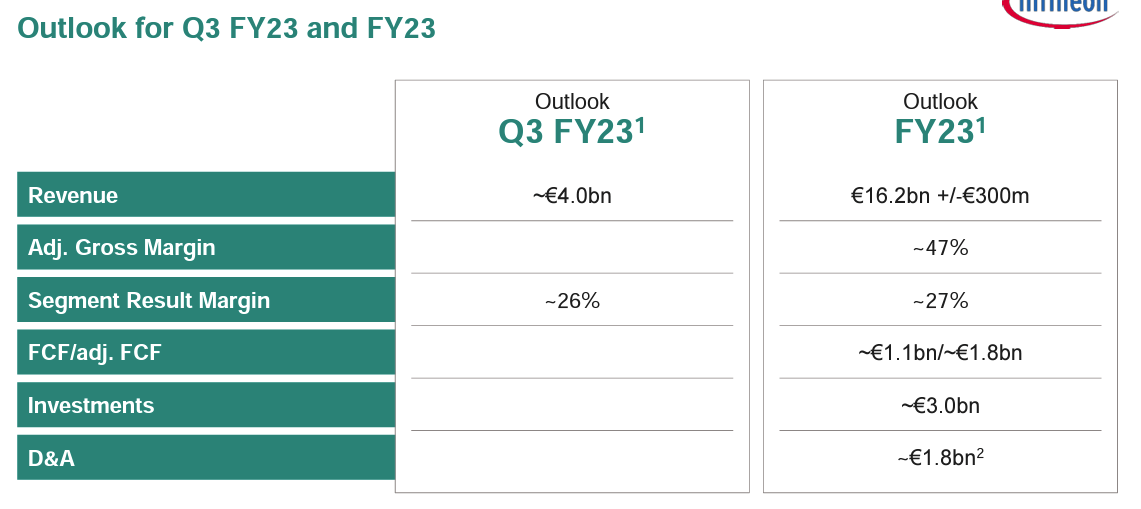

Infineon positively preannounced Q2 results and already raised the 2023 outlook before providing the usual update. Previously, guidance was provided in early February 2023. These positive results exceeded market expectations. In particular, the company reported sales of up to €4 billion (consensus estimated an average of €3.88 billion in sales) and a core EBIT margin of 28% (consensus estimated an average of 25% in operating profit). Therefore, the company managed to beat expectations by 4% and 16% respectively. Regarding the outlook, management raised its 2023 guidance indicating that, with a euro/dollar exchange rate of 1.05 in the second half, it expects a significantly higher level of sales to €15.5 billion (which was the previous guidance) with a corresponding positive effect on margins.

Infineon Q2 Financials in a Snap

{kind=link}

Source: Infineon Q2 results presentation

Regarding the segment result margin, we expect that Infineon will likely reach a high-twenties percentage thanks to stronger demand, positive MIX, and lower energy costs.

{kind=link}

Changes to our estimates

Based on the results, here at the Lab, we decided to:

- Keep our top-line sales estimates broadly unchanged and raised our Fiscal Year 2024-2026 revenue forecast by 5%;

- Increase our adjusted Earnings Per Share evolution in line with the revenue growth, continuing to see Infineon as a clear beneficiary of many secular trends. Therefore, we derive a 12-month EPS target at €2.5;

- Slightly increase our CAPEX forecast. In detail, the company obtained approval for a semiconductor plant for an investment of about €5 billion, with production scheduled for 2026. This would represent the largest CAPEX investment in its history and Infineon is seeking €1 billion in public funding, which would create approximately 1,000 jobs. The recent STM moves will support our decision ( China's new investment for a value of $2.4 billion and French new lab for $5.7 billion CAPEX);

- (We also suggest to our reader to check our STM latest publication called: " Positive EU Framework ").

Conclusion and Valuation

Q2 results are scheduled in early August, and we expect additional color on demand. Here at the Lab, we recently said that Infineon's post-Q1 2023 results were pricing significant caution this year, and we see upside potential . In addition, we also explained how our internal team was " ahead of the Wall Street estimates" . Well, this was a good call. Our conclusive paragraph clearly explained how "equity research analysts should re-price Infineon" . And, this is what is happening. We are still ahead of consensus estimates (for good reasons, have a look at our previous analysis ). Still related to our upside on the EU Chips Act , it is important to recall that Infineon got the go-ahead for a new chip fab in Germany. Therefore, we are still valuing Infineon with an FY P/E of almost 20x, including a 10% discount on higher rates (as we provided per STM), deriving a target price of €48 per share ($51 in ADR). Our risks include cyclical demand, logistic chain disruptions, and unfavorable €/$ FX moves.

{kind=link}

For further details see:

Infineon Technologies AG: Higher Guidance To Price In