IFNNF - Infineon: Trading At A Discount

Summary

- Infineon Technologies is a German semiconductor giant, mostly unknown among investors, while being one of the 10 largest suppliers of semiconductors.

- The company controls its whole supply chain through both frontend and backend production facilities.

- With exposure to many high growth industries, Infineon looks poised to show strong growth over the next decade. This was reason for management to upgrade its long-term targets.

- The company is currently trading 37% below its 5-year average and at a discount to the sector while reporting strong growth rates.

- Fair value for the company seems to be around $44 a share.

Introduction

I am very bullish on the semiconductor industry and believe semiconductor demand will increase significantly over the next decade. That I am not the only one with this opinion became clear when Qualcomm CEO Amon predicted that the production of semiconductors will need to double in the next decade as we will continue to see a digital transformation across every industry. He stated that the future of the economy is digital, and semiconductors will play a central part in this transition and digital future. While he might be talking to his own benefit, I do believe his statements are spot on. Digital trends such as AI, Cloud, and the Metaverse already are massive and will continue to grow at a rapid pace, driving demand for semiconductors.

There are even more secular growth drivers for the semiconductor industry and a major one is the transition toward EVs and self-driving. The number of semiconductors needed to drive all the systems of an electric car is already double that of the traditional ICE-powered car. Add to this the systems that allow self-driving features and the number of semiconductors in a single car increases even more. This all shows that the semiconductor industry is far from growing and Fortune Business Insights, therefore, expects the semiconductor industry to continue to grow at a 12.2% CAGR until 2029 to reach a total market size of $1.4 trillion.

(For a more in-depth analysis of the semiconductor industry outlook I would like to recommend this article .)

This secular growth story makes it a very interesting investment opportunity for investors. Yet, it is not so easy to find the right investment opportunities with the many high-growth companies still very highly valued, despite the significant drop in share prices during 2022. And whereas many investors tend to focus on the US, Taiwan, and maybe Korea for the most promising chip companies, it is Europe that also holds a few semiconductor gems such as ASM International ( ASMIY ), BE Semiconductor Industries ( BESIY ), and the very well-known ASML ( ASML ).

Within this article, I will take a deep dive into another one of these European semiconductor gems, namely Infineon ( IFNNY ). Infineon has exposure to many semiconductor growth industries while already reporting revenue of €14 billion for FY22 and not being as highly valued as some of its peers. Within this article, I will go through the company fundamentals, FY23 outlook, growth drivers & expectations, risks, and valuation in order to determine whether you should buy this European semiconductor giant at its current price of around $34 per share.

Let’s get to it!

Infineon Technologies AG

Infineon is a German semiconductor manufacturer headquartered in Neubiberg, Germany. The company used to be a division of industry stalwart Siemens AG ( SIEGY ) but was spun off in 1999. To give you an idea of its size, Infineon employs over 56,000 people and is one of the 10 largest semiconductor manufacturers in the world. Yet, it is still largely unknown among investors, or at least in my experience.

Importantly, Infineon is not a fabless semiconductor manufacturer but has multiple production facilities across several continents. Where this drives margins lower for Infineon compared to fabless peers like Nvidia ( NVDA ) or AMD ( AMD ), it gives them the flexibility to change production to their needs and they are not dependent on a third party like TSMC ( TSM ), Samsung ( SSNLF ), or Intel ( INTC ) to produce its chips. Infineon controls all the main stages of the semiconductor value chain itself. This includes the development and design of the semiconductors via frontend and backend manufacturing. The company also increasingly focuses on software and other services to control its semiconductor solutions.

The quote below from the investor presentation of Infineon should give a better idea of just how this supply chain is set up.

In frontend manufacturing, the wafers are processed. Optical, physical and chemical methods are used to create transistors and their interconnections, thus determining the function of the chip. The wafers are transferred from the frontend site to a backend site, where the remaining processing steps take place in backend manufacturing. These steps include sawing the wafer into individual chips as well as assembly and testing. Following the backend manufacturing, the chips are sold to customers via regional distribution centers.

{kind=link}

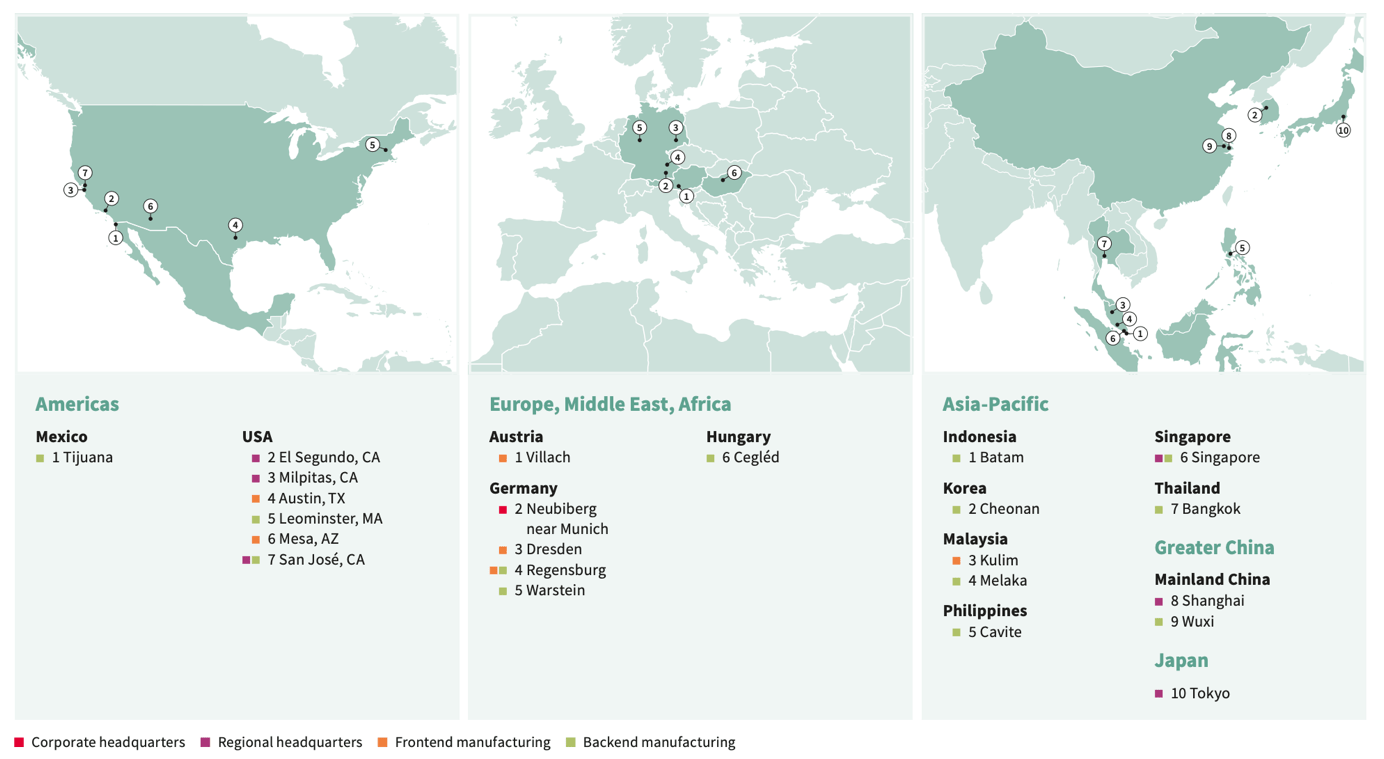

Infineon has manufacturing and offices all over the world including multiple backend and frontend manufacturing facilities in the US. This large exposure to Europe and the US regarding chip manufacturing also positions Infineon in a good way to benefit from tax incentives regarding domestic chip manufacturing. Both the US and Europe passed new laws over the last couple of years offering tax incentives to the domestic semiconductor market. The Chips and Science act in the US invests $280 billion into domestic semiconductor manufacturing and boosts R&D. The European chips act will address semiconductor shortages and strengthen Europe’s technological leadership. It will mobilize more than €43 billion of public and private investments and offers a strong tailwind for local manufacturing. With Infineon located across both continents, it will most likely benefit from these incentives. This report in the Austin Business Journal already mentioned that Infineon has tax breaks in hand for its factory expansion plans in Austin. This would reportedly save the company millions of dollars over a 10-year basis. In the end, this means Infineon can either lower its investment expenses or increase its expansion while spending the same amount of cash.

Infineon locations (Infineon Technologies)

{kind=link}

In addition to this, Infineon plans to invest $3.5 billion until 2027 into major frontend buildings. Infineon should have absolutely no problems funding these plans as the company expects operating cash flow growth to still outpace investments. Even after excluding high investment plans, Infineon continues to expect an adjusted free cash flow margin of 10-15%.

In fact, after its latest FY22 earnings report, Infineon decided to renew and increase its long-term targeted operating model. Infineon now targets long-term revenue growth of above a 10% CAGR, target margins of 25% (19% previously), and an adjusted free cash flow margin of a very solid 10-15%. Also, Infineon has very ambitious sustainability goals and wants to make itself an example of how sustainable a semiconductor company can be. Therefore, Infineon targets to be CO2 neutral by 2030.

In addition to having manufacturing facilities across the world, Infineon also has an excellent product and customer exposure to all regions. Below you can see that Infineon has revenue exposure to all regions and that revenue is generally very well split. China is the largest revenue contributor for Infineon, followed by the EMEA including Germany with a 24% share.

I am not very enthusiastic about the massive revenue exposure to China as this brings with it many risks. The increasing tension between the US and China for example is not making things a lot better. I would prefer Infineon to focus its efforts on the EMEA and Americas for a more reliable and riskless revenue stream. Still, as long as there will be no sanctions on products of Infineon (and there is no risk of such a thing) China can also turn out to be a large growth driver as its economy generally grows a lot faster than western economies. For now, with China representing less than 30% of revenue, I am not overly worried, and I don’t think other investors should be either.

{kind=link}

Now, Infineon reports its revenues split over four categories. To get a better picture of the company and its products, I will discuss these shortly.

Automotive ((ATV))

This segment is responsible for 45% of FY22 revenue and is the largest segment for Infineon. While being the largest, it is also the fastest-growing segment for Infineon with the segment growing 35% YoY for FY22. This will not be a surprise to many as the transition to EVs and autonomous driving trends are major tailwinds pushing digital growth for the automotive industry. Infineon is in an excellent position with almost half of its revenues coming from this high-growth industry.

In short, the products Infineon offers to the automotive industry target to make cars clean, safe, and smart. This is what the Infineon investor presentation added to this:

We cover all application areas in the vehicle: powertrain and energy management, connectivity and infotainment, body and comfort electronics, safety and data security. Our range of products and solutions helps to navigate the transition from internal combustion engines to hybrid or electric drives, enabling an ever-increasing degree of automated driving, electric-electronic (E/E) vehicle architecture, greater connectivity and digitization, and a higher level of data security in vehicles.

Infineon also focuses on innovative solutions in areas such as digital cockpit, infotainment, and lighting technology. All of this makes Infineon a market leader in semiconductor solutions for cars through its sensor, microcontrollers, and software solutions.

Industrial power control ((IPC))

This segment is responsible for 13% of FY22 revenue and is therefore one of the smaller segments of Infineon. The segment recorded strong double-digit growth for FY22 as the segment grew by 16% YoY.

This segment focuses on semiconductor solutions for intelligent management and efficiency of electric energy along the entire value chain. This is what the Infineon investor presentation added:

The product portfolio comprises mainly IGBT power transistors and the driver ICs to control them, as well as power semiconductors based on SiC. We offer products in the Industrial Power Control segment, whether Si-based or SiC-based, in various form factors and with different levels of functionality.

This segment has a very broad application spectrum and includes motor control units for industrial manufacturing and building technology, but also inverters for solar panels and wind power systems. The solutions offered by Infineon can be used in pretty much all electrical devices and increase durability, efficiency, and offers intelligent management applications.

By offering strong capabilities to green energy solutions such as solar energy systems, wind energy systems, electric vehicles, energy storage, and charging infrastructure, this segment is growing significantly by riding the green energy trend and this is expected to continue over the next decade as green energy adoption increases.

Power & Sensor systems ((PSS))

This segment is responsible for 29% of FY22 revenue and is the second largest segment for Infineon. Like the other segments, this one saw strong YoY growth in FY22 as the segment grew by a solid 25%.

The title of this segment could already give an idea of what this segment is about. Infineon develops and designs power semiconductors and sensors for use in products like power supplies, lighting systems, and mobile devices. The products of Infineon help make these products smaller, lighter, and more energy efficient while also developing new functionalities.

We are drawing on the next generation of new, innovative solutions based on Si, SiC and GaN for applications in the areas of 5G, data centers, power supplies and adapters, battery-powered devices, and renewable energy. Our portfolio of products for power supplies, comprising control ICs, drivers and MOSFET power transistors, addresses the two key requirements of the market: efficiency and power density.

As mentioned above, this segment gives Infineon exposure to other high-growth industries such as 5G, data centers, and renewable energy. It is therefore no surprise that also this segment managed to display very strong growth for FY22.

Connected secure systems ((CSS))

This segment is responsible for 13% of FY22 revenue and therefore is one of the smaller segments for Infineon. Still, this segment was the 2nd fastest growing segment as it saw growth of 30% for FY22.

This segment of Infineon is all about supplying microcontroller solutions, Wi-Fi and Bluetooth solutions, and combined connectivity solutions. Infineon also supplies hardware-based security technologies and software for the programming of all components that cover many application areas. Appliances involve the following options:

These include devices for IoT applications, connected home appliances and smart home appliances, IT equipment, consumer electronics, cloud security and connected vehicles, as well as credit and debit cards, electronic passports and national identity cards. With our technologies in the areas of computing, connectivity and security, we are contributing significantly towards ensuring that current and future connected systems are reliably protected.

Looking at these possible appliances it is not surprising at all that this segment is witnessing solid growth. Increased connectivity due to the increase of IoT applications and an increased focus on security is driving growth for this segment and will most likely continue to do so as the IoT market is expected to grow at a 26.4% CAGR .

Infineon Technologies

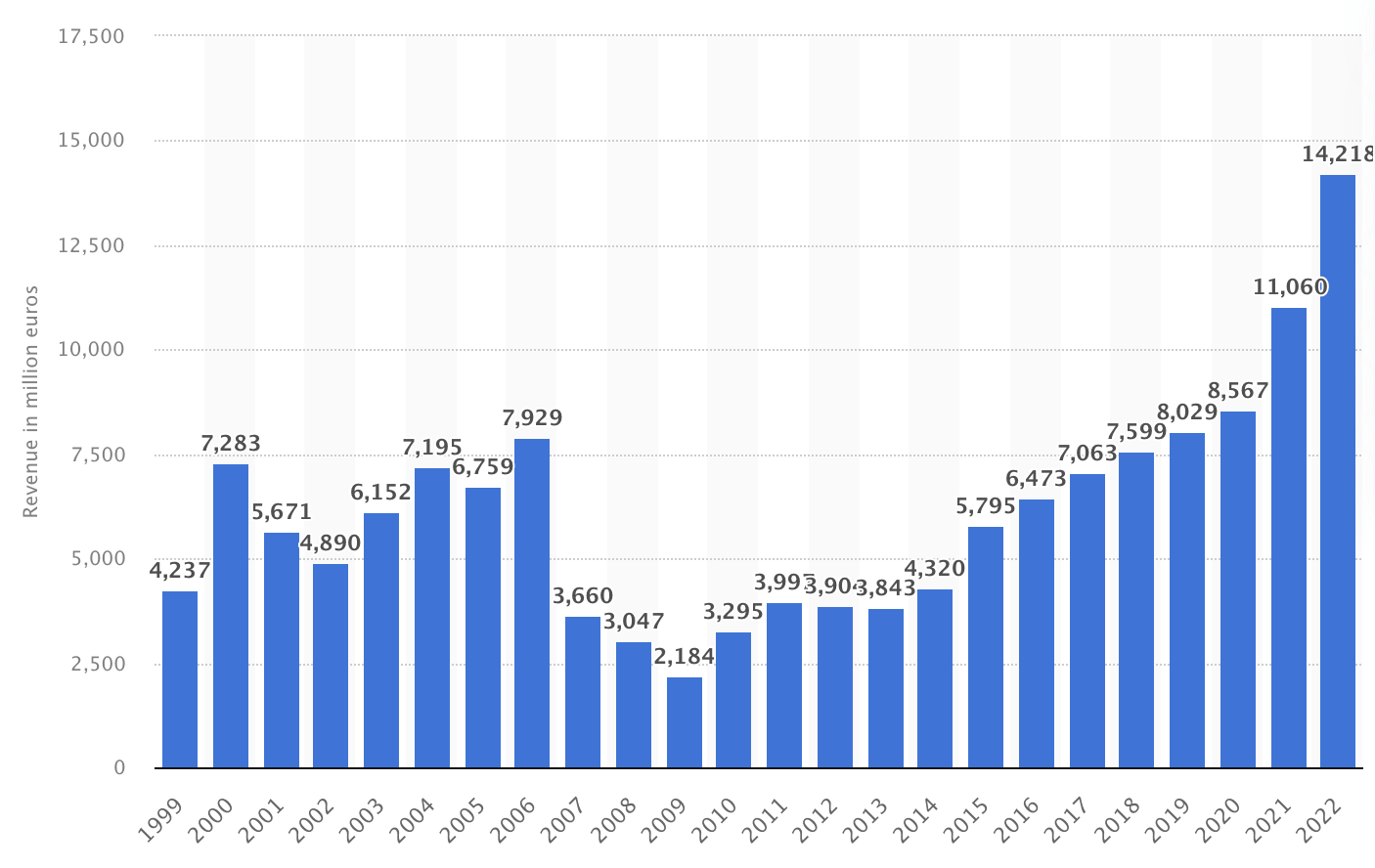

Overall, Infineon had a very solid 2022 in which it reported impressive growth of 29% YoY and revenue of over €14 billion. This was one of the strongest years for Infineon driven by growth from all segments. For FY23 , Infineon expects to report revenue of €15.5 billion +/- €500 million with an adjusted gross margin of 45%. Adjusted free cash flow is targeted to be around €1.5 billion with investments of €3 billion.

This would represent another impressive year from Infineon and record revenue despite economic worries. The graph below shows the impressive revenue growth from Infineon over the years, with constant growth from 2016 until today. The jump in revenue from 2020 to 2021 was mainly due to the acquisition of Cypress. Though, more interesting to investors will be growth going forward. So, what will be driving growth for Infineon?

Infineon revenue growth (Statista)

{kind=link}

Growth drivers

Infineon itself identifies 5 main growth drivers for the next decade and expects these to drive 60% of growth. These are the following:

- E-mobility (automotive)

- Renewables

- ADAS (autonomous driving)

- Data center

- IoT

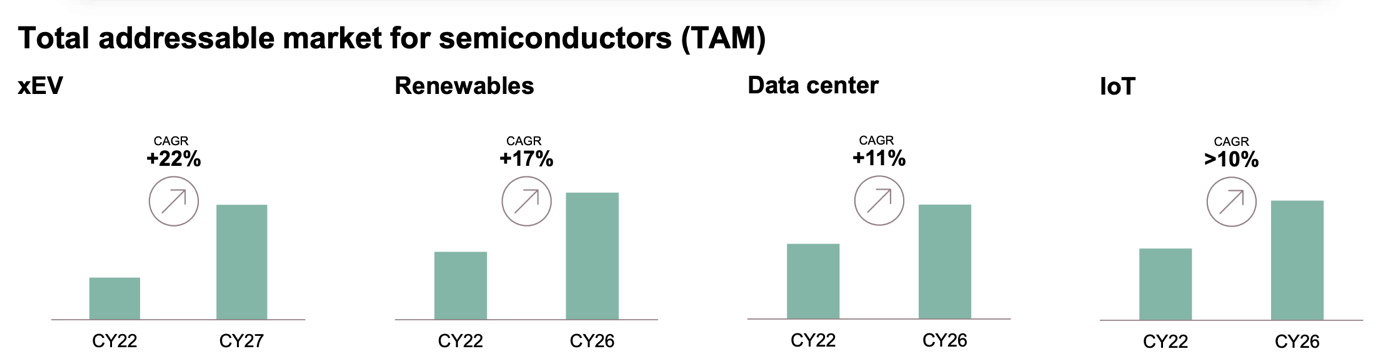

Overall, Infineon expects over 10% growth for all its segments and so believes it has no weak links.

Infineon TAM growth (Infineon Technologies)

{kind=link}

The graph above shows just how Infineon views growth for its TAM, and we can see that all are expected to grow at solid rates until 2026. Most of these are exposed to secular trends. Now, let’s discuss what I view to be the main growth drivers for Infineon.

Renewables

Infineon power systems solutions will play a crucial role in the entire power transformation chain. This starts at the generation through solar and wind energy systems where approximately 50% of currently installed capacity is powered by Infineon power systems products. This shows the importance and exposure of Infineon to the green energy transition. And it does not end at just renewable energy generation as Infineon power solutions are also used for 2/3 of the electricity grid infrastructure, including electric charging. Add to this that Infineon is also offering the broadest portfolio, covering all verticals of the energy conversion and usage business, and we can see Infineon plays an incredibly crucial role in the energy transition. Finally, Infineon power solutions are also the number one choice for vehicle electrification.

Convinced yet? Of course, it is not just that simple, but the incredible exposure and importance of Infineon to the shift towards green energy is massive. This also puts Infineon in a great place to continue riding this green energy wave over the coming decade(s) as solar and wind energy should replace fossil fuels in the future.

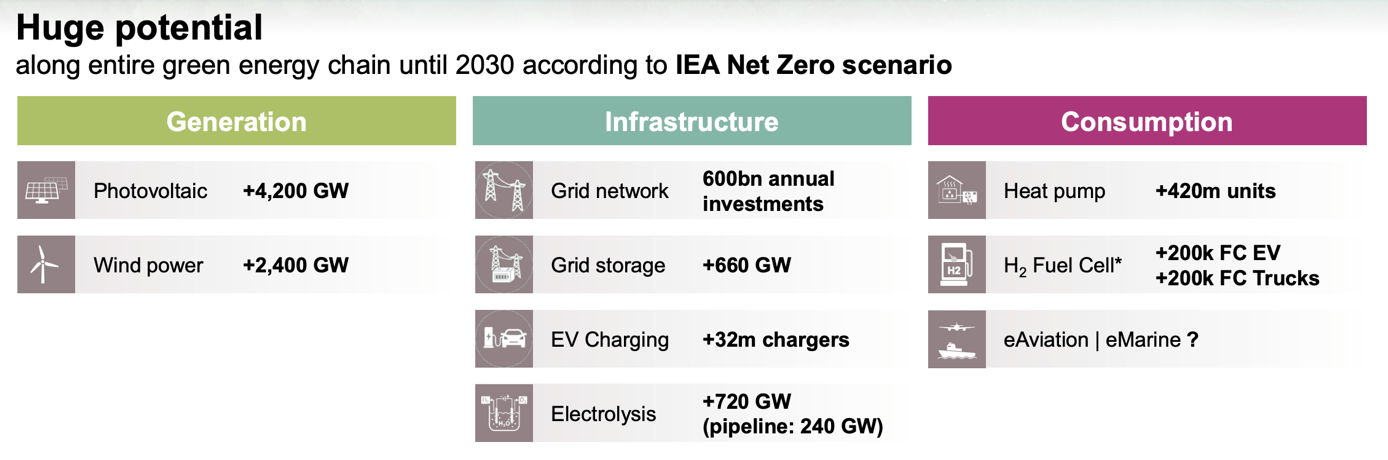

The PSS segment will most likely see strong continued growth due to product dominance and exposure to the green energy trend. The strong presence of Infineon across the whole power transformation chain has it set up well for future growth. According to the IEA , the momentum behind the green energy shift is increasing as a result of the Russia-Ukraine war and power capacity is now expected to grow by 2400 GW by 2027. As this number will most likely not mean much to you – this is equal to the entire power capacity of China today. As a result, it is expected that renewables are set to account for over 90% of global electricity expansion over the next 5 years, overtaking coal. Most of this expansion will be coming from solar and wind energy systems and as Infineon has a 50% market share in the power solutions industry for renewable energy generation, this is looking very, very good. In addition to this, pictured below you can see the IEA expectations for 2030 and it looks very promising! Wind energy generation is expected to increase at a 19% CAGR until 2030 and solar grows at an even faster 22% CAGR.

In short, this means Infineon is well positioned through its strong presence and market share in the power systems of green energy solutions to continue benefitting from the increasing adoption of both solar and wind power solutions. This will be a solid growth driver over the next decade.

{kind=link}

Automotive

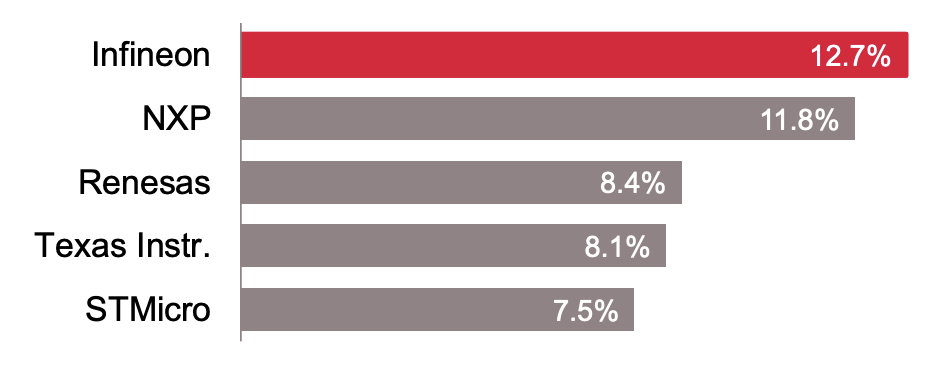

Infineon also continues to be very bullish on its automotive exposure and rightfully so. The company has been increasing its market share in the automotive industry for many years now. In 2019, it was only the second largest and behind NXP with a 9% market share in car semiconductors. In 2019 Infineon massively increased its market share with the acquisition of Cypress to 11.2% , still trailing NXP ( NXPI ) with an 11.3% market share. In FY21 Infineon than finally managed to overtake NXP and became the largest supplier of automotive semiconductors with a 12.7% market share. Its dominance in this industry is yet again thanks to its strength in power semiconductors. For this specific category in the car semiconductor market, Infineon even has a 31.7% market share as can be seen below.

Its strong market share in the car semiconductor industry (and increasing) means that Infineon will be the main beneficiary of industry growth. This industry was valued at $41.78 billion in 2020 and is expected to grow at a 6.2% CAGR until 2028. Infineon has been steadily increasing its market share over the past few years and I see no reason why this would stop now. This is shown by recent design wins with Stellantis ( STLA ) for example. I believe we will see the automotive segment of Infineon grow at a slightly faster pace than the overall market. Also, this projection does not seem to include sensors for ADAS systems which is also an important business part for Infineon.

Market share in automotive semi industry (Infineon Technologies)

{kind=link}

Infineon market share (Infineon Technologies)

{kind=link}

The automotive semiconductor market reached a market size of $46.7 billion for FY21 as it grew by 31.5% and reached an all-time high, beating the previous high reached in 2018. The covid years were tough for the market as car demand massively dropped and so did the demand for its semiconductors. Still, the renewed growth as the result of the push towards more semiconductor-heavy EVs and ADAS, caused for the industry to quickly recover. Infineon also acknowledges that this growth seems to be in part driven by content-per-car growth.

Another automotive growth area for Infineon is the increasing popularity of ADAS and self-driving systems. These systems need strong sensor and Lidar solutions and as a result, the number of radar systems worldwide is expected to increase at a 24% CAGR due to low penetration and new applications. Infineon has a strong market share in the radar semiconductor solutions segment and has many OEM clients such as Volkswagen Group ( VWAGY ) brands, GM ( GM ), Honda ( HMC ), Mercedes ( MBGAF ), Toyota ( TM ), Stellantis, and even Alphabet-owned Waymo ( GOOGL ).

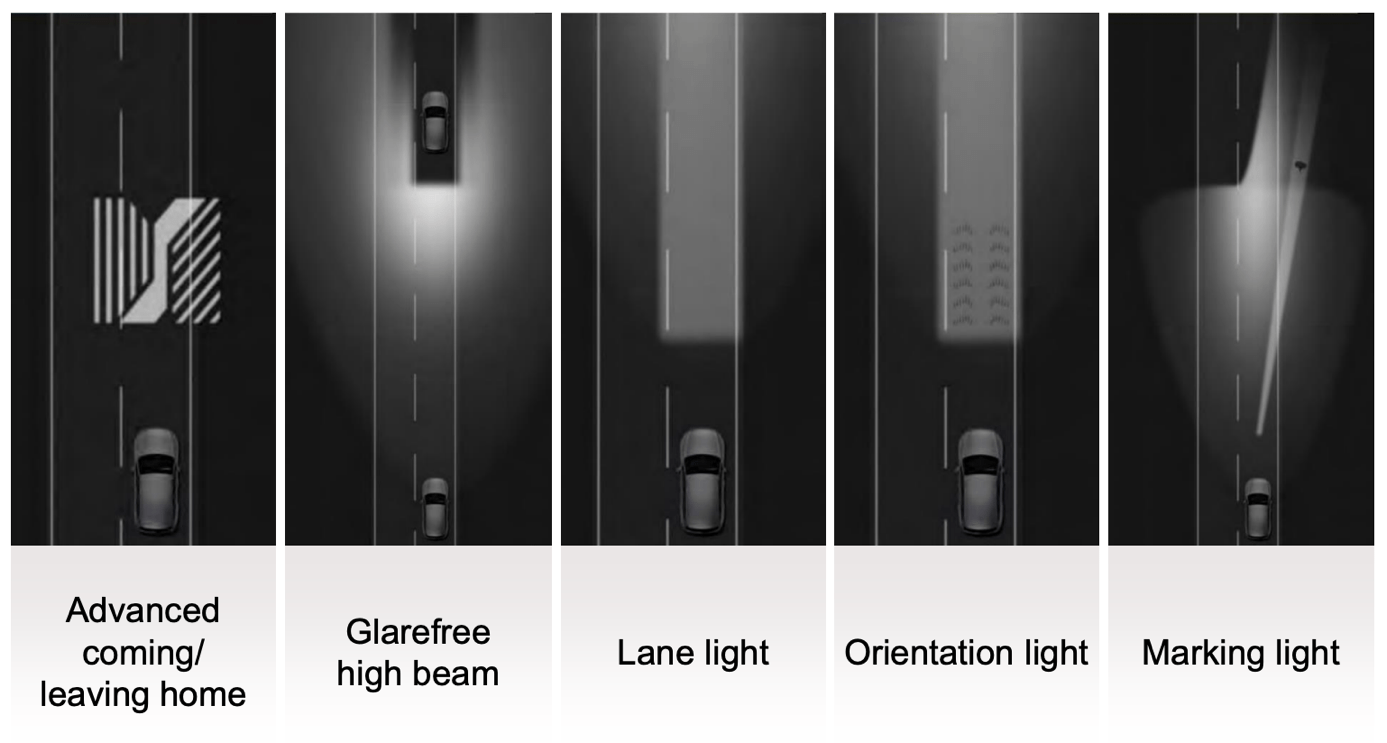

With electrification and ADAS systems increasing in penetration, cars are increasingly becoming more software-defined and Infineon offers the full stack of solutions. This ranges from head-up display functionalities, noise canceling for your car, infotainment systems, complete car control, heated seats, and advanced lighting capabilities as shown below. Due to the car more and more becoming a computer, Infineon expects to increase its MCU revenue from €1.6 billion in 2022 to €4 billion by 2027, a significant increase and a 20% growth CAGR.

Infineon light solutions (Infineon Technologies)

{kind=link}

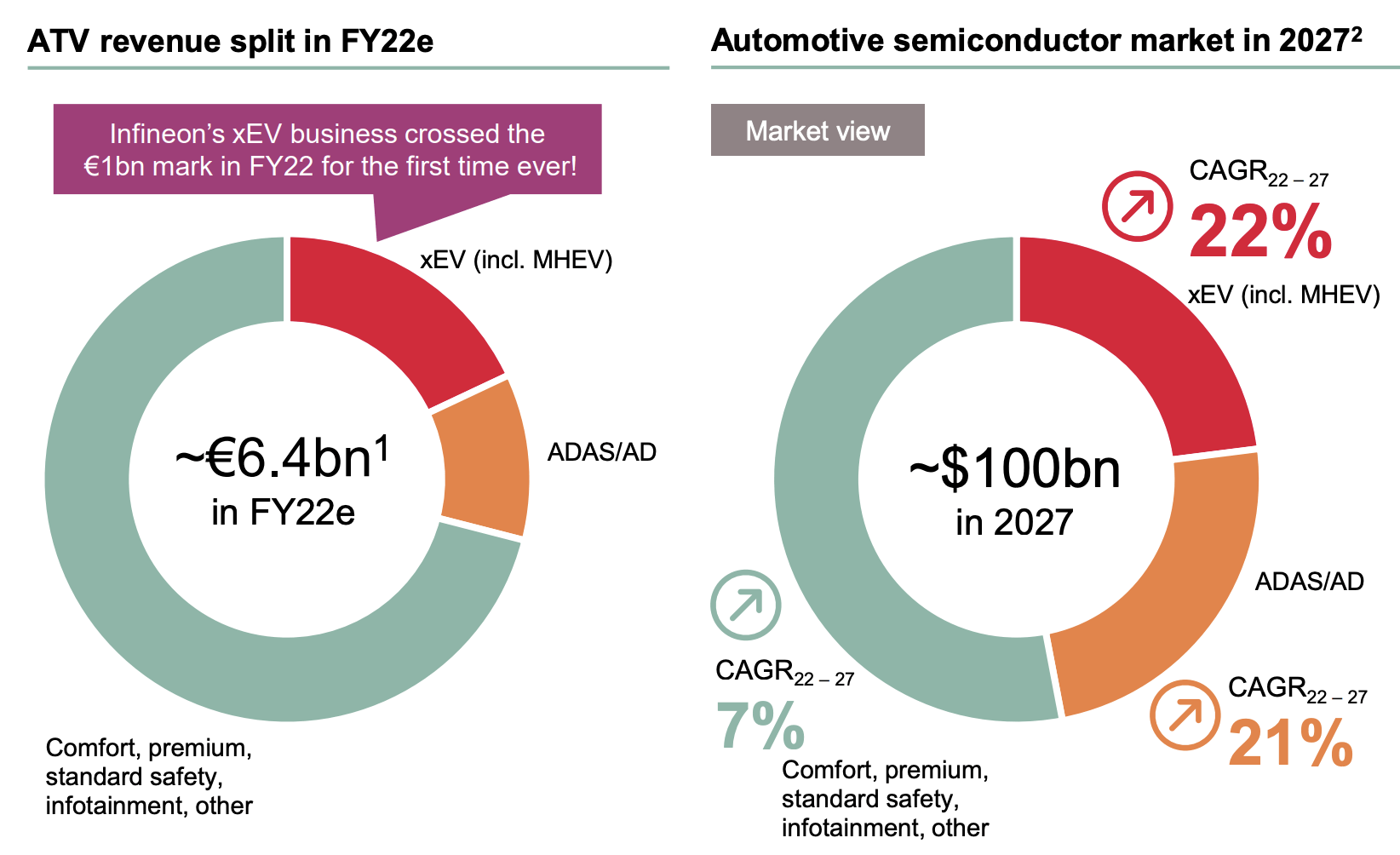

Overall, Infineon expects strong growth from the automotive industry and has positioned itself in a sweet spot. The automotive operating segment ((ATV)) recorded €6.4 billion in revenue for FY22 of which the transition towards EV contributed only €1 billion and ADAS even less. Currently, most of the automotive revenue for Infineon comes from its power semi-solutions and traditional automotive applications. By 2027, Infineon believes the TAM for the automotive semi market to reach $100 billion, from a little under $50 billion today, as mentioned before. Electrification and ADAS are expected to lead the way and increase their share of the market. The graph below shows the transition.

Infineon will likely see this segment continue to grow strong, but with the majority of revenue still coming from traditional automotive semis, a possible slowdown in car sales could hit the business segment in the short term. Despite this, I believe the automotive segment will be a revenue driver and become a larger share of total revenue for Infineon. With EV penetration increasing over the next decade, and ADAS and further self-driving still in their infancy, I do not believe increased exposure to this industry will be a bad thing for the decade ahead.

{kind=link}

Power semiconductor dominance

I have mentioned the term “power semiconductors” many times in this article already as Infineon has a strong market share in this product category, but without a technical background, it might not be totally clear what these do. And actually, the basics are not very complicated.

Power semis are used to regulate the flow of electrical power and can be used in all types of systems. As mentioned already, this is primarily for high-power applications like electric vehicles, industrial machines, and renewable energy. These semis allow for very precise control of the power being supplied to a system. These are very crucial parts in many modern systems as without them, these systems would not function properly and would be way less efficient. As the world is moving towards more sustainable and efficient solutions, the use of these power semis is expected to grow further over the next decade.

Power semi applications (Infineon Technologies)

{kind=link}

As Infineon has a leading position in both the MOSFETs and power semis, it can greatly benefit from trends that require an increasing number of these solutions. One of these trends is the shift towards the cloud and, therefore, the increasing demand for server capacity. Power ICs can help to improve the efficiency, reliability, and performance of servers, by providing precise control over the power consumption and management of server components, and they, therefore, play an important role in maximizing the abilities of these servers.

Server capacity is expected to grow at an 8% CAGR until 2027 and provides another tailwind for Infineon. This products segment gets an additional boost from the transition to 5G as it drives higher demand for power semiconductors for antennas and power supplies.

In summary, the excellent market position of Infineon allows it to benefit from the increasing demand for power semi-solutions from several high-growth industries and trends and should see strong continued growth over the next years as well.

Summary

Now, to summarize, it is clear why Infineon increased its long-term goals. With its current market strength, product dominance, and exposure to several high-growth industries and trends, growing over 10% a year seems definitely achievable. The company has a very strong position in the automotive semi-market, a strong market share in power semis, and several other product categories in which it dominates or sees high growth potential. Through this, it gets solid exposure to growth trends like xEVs (all types of electric vehicles), green energy, datacenters, and 5G. All of these will drive solid growth for this German semiconductor giant.

Balance sheet & dividend

At the end of its fiscal FY22 Infineon held €3.7 billion in cash on the balance sheet with €5.7 billion in debt. This means Infineon currently has an acceptable net debt position of €2 billion. While the company is expecting to invest a significant amount of cash in new factories or factory expansion, it also believes it will continue to generate a significant amount of free cash flow. The cash position allows Infineon to invest in new facilities while its cash generation is strong enough to cover the debt burden. Whereas I prefer tech companies to hold a net cash position with not too much debt, I believe the current situation for Infineon is acceptable and should be of no worry to investors.

Infineon also pays a small dividend to investors. Its forward dividend yield currently stands at 0.97%, which is not all that high, but a nice bonus on top of strong growth. Infineon has been growing its dividend at a 5.68% CAGR over the last 5 years, but this growth has not been as steady. The company did not grow its dividend during covid but made a significant increase last year when it announced an 18.52% increase. Infineon has been paying a dividend for 7 straight years.

Dividend safety is looking very good for Infineon as the payout ratio stands at just 18%. As a result, the dividend should not be at risk if growth would stall. If Infineon manages to keep growing according to plan and current projections, the dividend has plenty of room to grow in the future.

While not the ideal pick for a dividend (growth) investor, the dividend is a nice bonus on top of share price growth.

Valuation and Outlook

Infineon is currently valued at a forward P/E of 15.71 which is almost 20% below the information technology sector and over 37% below its 5-year average. With growth prospects looking better than over the previous 5-years I believe Infineon should trade much closer to its 5-year average, even when factoring in a potential recession and global slowdown.

With Infineon guiding for revenue to grow at an above 10% CAGR, the growth outlook looks strong, and considering everything discussed above, this seems very achievable. Infineon management has projected for revenue to grow around 11% for FY23, but historically management’s expectations have been rather conservative. It is therefore no surprise that analysts’ expectations are slightly higher and guide for revenue to grow slightly over 12% for the year ending in September 2023. Surprisingly, current analyst estimates guide for revenue growth to drop below 10% for both FY24 and FY25 with expected growth rates of 6.99% and 9.39%, respectively. As a result, I would say analyst expectations also look rather conservative and seem to price in a slowdown as the result of a severe recession. Although this is still highly unpredictable, economic conditions remain strong and unemployment is well under control, so a soft landing still seems possible. Yet, even if we would enter a severe recession, I expect Infineon to perform better than current analysts’ estimates for FY24 and FY25 as the company still has a solid backlog of almost 3x FY22 revenue. This should offer the company enough downside protection if a severe slowdown would occur. The backlog has been increasing rapidly as shown below. I do expect the backlog growth to slow or even decrease as this build-up has been mainly due to a chip shortage in the automotive sector.

Infineon backlog (Infineon Technologies)

{kind=link}

I believe analyst estimates should be revised upwards for both FY24 and FY25 as growth will most likely come in closer to a 10% growth rate for both years as strong secular trends such as the transition to green energy, car electrification, ADAS, and datacenter expansion will continue growing at a strong pace. As a result, I expect FY24 and FY25 revenue of closer to 9% and 12%, respectively.

Infineon analysts' revenue expectations (Seeking Alpha)

{kind=link}

Seeking Alpha does not provide much information regarding EPS estimates as it only shows 2 analyst projections. Infineon has been increasing margins over the last several years and plans to increase these even more over the next couple of years. If we would assume EPS to grow slightly faster than revenue with growth rates of 12% for FY23, 10% for FY24, and 12% for FY25, this would result in the following EPS estimates:

- FY23 EPS of $2.17

- FY24 EPS of $2.39

- FY25 EPS of $2.67

If the stock were to revalue to a P/E of 18x (still much below its 5-year average of 25) this would result in an FY25 share price of $48 or a growth CAGR of 12% from current prices of around $34. Considering these are still very conservative growth projections, it is safe to say that the stock is trading very cheaply.

According to Tipranks , wall street analysts have an average moderate buy rating on the company with a price target of $44.08 based on a 21x P/E. This represents a 27% upside potential and seems like a fair price target for the next 12 months.

Risks to the outlook

Despite the company's excellent positioning and product dominance, an investment in the company is not without risks. Let’s discuss several of the most important risks that could impact the financial performance, business outlook, or valuation of Infineon.

Recession

The risk of a potential recession will continue to weigh on the valuation of Infineon. Infineon has high exposure to the very cyclical automotive industry and a potential slowdown as a result of high-interest rates could weigh down on demand and growth for the automotive segment of Infineon. In addition to this, Infineon also has exposure to consumer electronics which has already seen a significant slowdown. This might not be a large part of Infineon’s business, but a slowdown can turn out to be a drag on revenue growth.

In the end, a severe recession would also be reflected in revenue growth. Infineon does have a strong backlog that protects it from many downsides, and as a result, I believe the company is protected against a severe slowdown.

Loss of market share

Like many companies operating in competitive industries, Infineon needs to protect its market share and technological expertise. If Infineon were to lose market share, this would impact the long-term outlook and revenue growth would be lower than expected.

Infineon has been increasing market share over the last couple of years at a rapid pace across several business segments and I do not expect this to reverse against them any time soon. Still, this is something to guard against as an investor. Within the semiconductor industry, technical dominance and market share are crucial.

Dependence on certain growth areas

As management itself acknowledges, Infineon has several growth drivers that are expected to account for 60% of future growth. The main two are automotive exposure which includes several trends like ADAS/radar and electrifications, and the transition towards green energy in the form of both solar and wind. These two will most likely account for 50% of growth for Infineon and this makes the growth outlook somewhat sensitive to setbacks.

If, for example, the green energy transition were to slow down and result in disappointing growth, this would have serious implications for Infineon as well. The company is heavily invested in this ongoing trend. The same goes for the electrification of cars and autonomous driving systems.

Conclusion

Infineon is a fascinating and mostly underappreciated semiconductor giant located in Germany with facilities across the world. The company is well-positioned to benefit from government incentives and has already announced that it has ambitious plans. Infineon is set to expand the business and the company backlog proves that demand is high for its products.

With excellent exposure to high-growth industries and trends like renewable energy, electrification, ADAS, and datacenters the company is well-positioned for continued growth over the next decade. Management recently upgraded its long-term goals and now aims to grow revenue at an above 10% CAGR, achieve 25% margins, and a 10-15% free cash flow margin.

I am expecting significant growth over the next decade for Infineon and from current low valuations believe the company can be a significant outperformer for investors. With the stock currently valued 37% below its 5-year average, the stock is priced at a discount and all downside from a potential recession seems to be more than priced in. In fact, I believe analysts’ estimates should be revised upwards for both FY24 and FY25.

I agree with analysts on a 12-month price target of $44 per share. This means the stock has approximately 27% upside potential from current prices of around $34 per share. Combined with a strong growth outlook, complete control of its supply chain, and conservative management, I believe the stock is a no-brainer at current levels and is a strong buy for any investor.

For further details see:

Infineon: Trading At A Discount