AFMC - Inflation Fell But Prices Are Rising

2023-04-14 10:13:15 ET

Summary

- The definition of inflation as the year-over-year change in CPI is misleading. Inflation falls, but prices continue to rise.

- Higher prices are realized even if inflation rises slowly above 0%.

- Even if year-over-year inflation falls, over longer lookback periods inflation remains high and prices are rising, while consumer purchasing power is decimated and debt is rising.

- Since 1943, there have been only two periods when the US economy had a meaningful drop in prices and inflation.

- Rising price levels may cause financial instability. A period of deflation may act as a relief valve to higher price pressures. Increases in rates are required to remove excesses.

I know this article may generate backlash, but as authors, we should not always write about subjects that please the audience. The truth is more important than avoiding criticism from those who have an opposite view.

The mainstream media was excited after the recently announced drop in inflation. According to the Bureau of Labor Statistics:

The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.1 percent in March on a seasonally adjusted basis, after increasing 0.4 percent in February, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 5.0 percent before seasonal adjustment.

Summary

- The CPI rose 0.1 percent.

- YoY the CPI increased by 5 percent.

What was in the report that caused excitement in mainstream financial media? In reality, the report was another bad one: after a long period of higher price pressures, the CPI continued to rise. The YoY fell because of its rolling nature and the elimination of past higher rises in the index.

Before elaborating further on the thesis that inflation is rising at an alarming rate, I will attempt to answer the following question:

Why did the stock market rally?

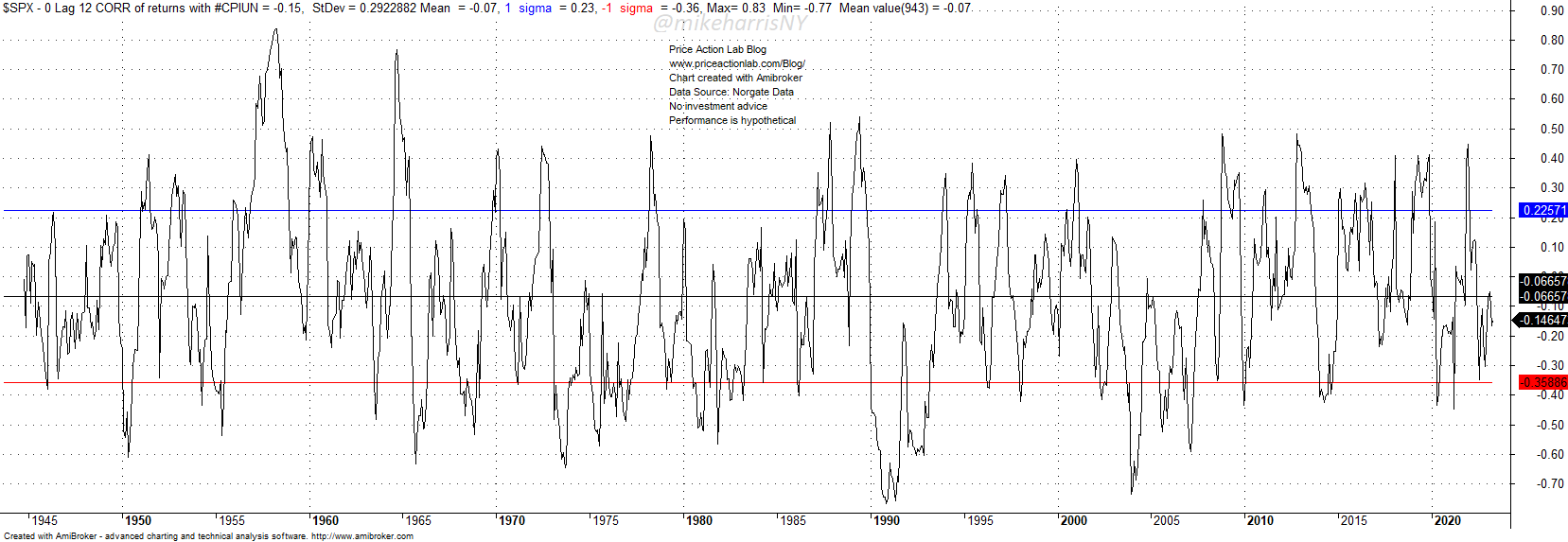

The answer may sound trivial: there is no clear long-term correlation between the stock market and inflation. Stocks can rise when inflation is falling and also when it is rising. The stock market direction depends on a large number of variables and it is a highly complex non-linear stochastic process. Let us look at the zero lag, 12-month correlation, between the S&P 500 index ( SPX ), and the CPI monthly returns.

Zero Lag, 12-Month Correlation of S&P 500 and CPI (Price Action Lab Blog - Norgate Data)

{kind=link}

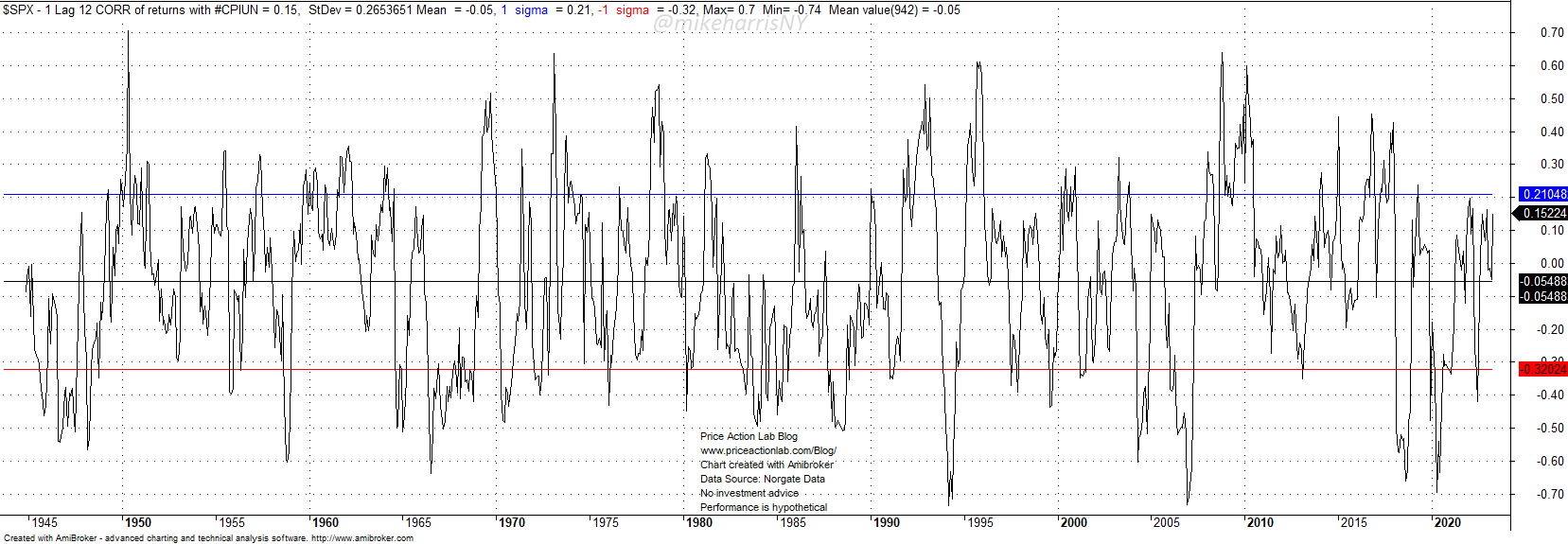

Although the correlation has been very volatile, over the long term the average is close to zero. The same is true when we look at the 1-lag, 12-month correlation.

1 Lag, 12-Month Correlation of S&P 500 and CPI (Price Action Lab Blog - Norgate Data)

{kind=link}

Analysts may identify a temporal correlation of stocks with inflation and attempt to make analogs, but the truth is the correlation is highly volatile and random with a long-term mean close to zero. Stocks do not care much about inflation levels. As an example, in an SA article about inflation parallels , I noted how by the mid-1980s stocks had made new highs although inflation was very high. As related to the current period, stocks may continue to rally even as inflation and rates rise. Forecasting the stock market direction is always an exercise in futility, especially during periods of high uncertainty.

Inflation is high, it is rising, and a period of deflation may be required

In August of last year I wrote an SA article, Taming Inflation May Require More Than A Recession . This was the main point of the article:

Taming inflation with rate hikes may not be sufficient. Elevated gold prices, despite a strong US dollar, indicate expectations for higher inflation. A recession may not be enough, and a deflationary spiral may be required to lower inflation.

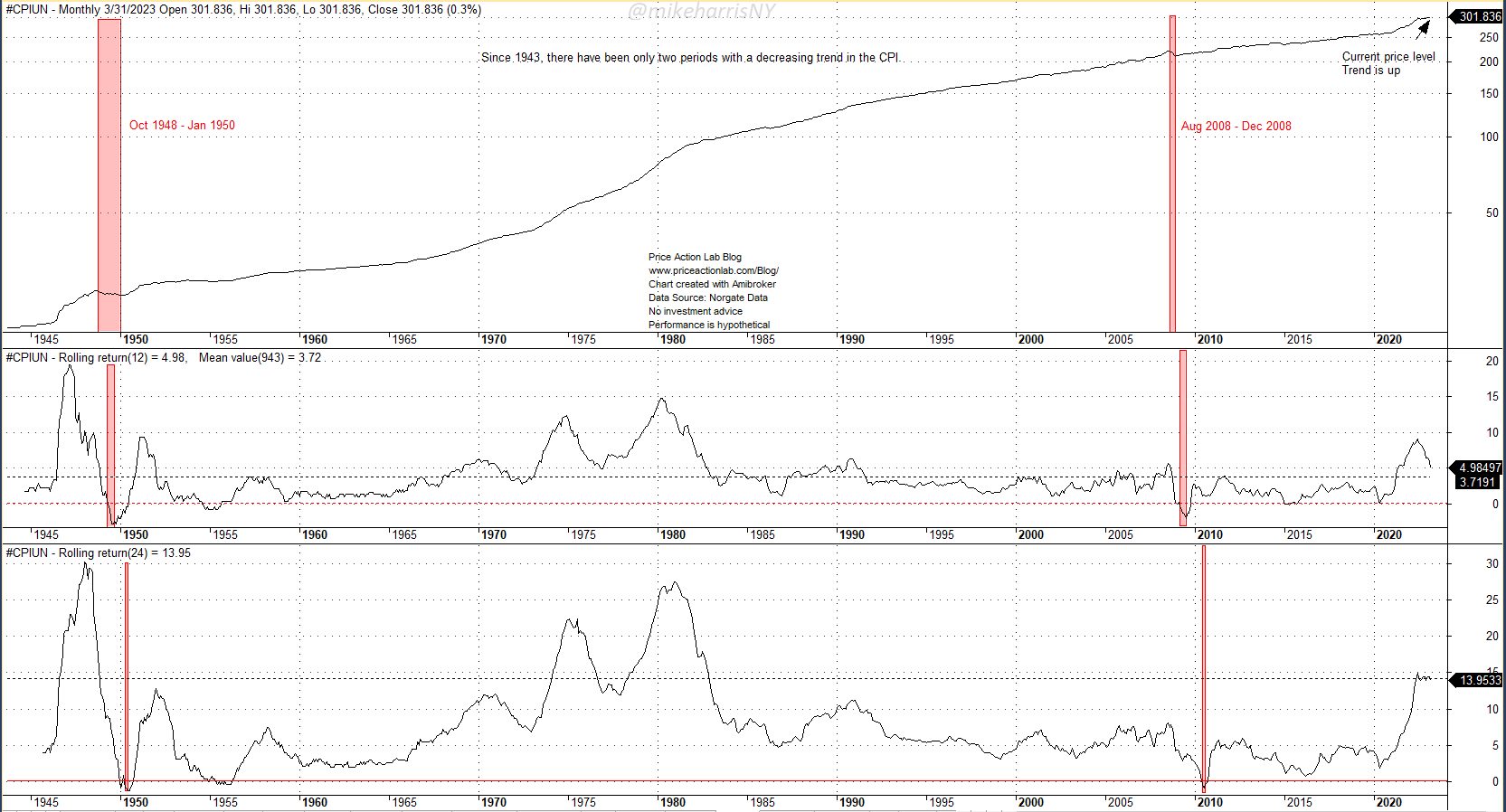

It is shown below that there have been only two periods since 1943 in the US with a meaningful drop in the price level, as measured by the CPI.

CPI Chart with 12 and 24-Month Rate Of Changes (Price Action Lab Blog - Norgate Data)

{kind=link}

From October 1948 to January 1950, the CPI fell by 3.7%. From August to December 2008, it fell by 4.1%.

The maximum monthly drop in the CPI was 1.9% in November 2008. The maximum YoY drop was 2.9% in August 1943.

The YoY inflation in March of this year was 5% and this rate-of-change of CPI is falling, but rate-of-change of a rate-of-change is a tricky notion.

If we consider the 24-month rate-of-change of CPI, and we define that as inflation also, then it is at a high level of 14% and not falling.

The YoY change as the inflation measure is an arbitrary convention. At the end of the day, consumers care about the level of prices, and from two years ago they are high and are not falling. Except, if we will demand consumers to forget what they paid two years ago and only have memories of the most recent year.

The GFC was an opportunity to tame inflation and the CPI but central banks elected instead to flood economies with money and create the conditions for rising inflation. For a while, inflation hid in financial markets in the form of excess liquidity chasing returns. During the pandemic, central banks flooded economies with money again and created conditions for long-lasting inflation.

It is evident even to those who are no experts, that a return to 2% inflation will require additional rate hikes, and possibly inflation will increase as competitors in the world respond with supply cuts. We saw that recently with the OPEC+ decision to reduce production.

Since GFC, the FED's actions have been driven by politics and short-term objectives. Prolonged inflation has the potential to create instability and even tail risk. Another deflation is required but without stimulus to remove the significant excesses from the economy and drive investment where there is real tangible value. It will be a painful process, the living standard will decrease, but financial chaos will be avoided. The current path of complacency and rush to print money whenever there is a crisis to appease the crowds will eventually lead to significant issues, some of which may be unknown unknowns.

Conclusion

There is no clear correlation between stocks and inflation.

At this point, inflation remains stubbornly high.

Additional rate hikes will be required but may not be enough.

Another period of deflation may be required to tame inflation.

If another deflation occurs, a stimulus will not be provided.

A deflation will clean excesses and drive investment to real value.

For further details see:

Inflation Fell But Prices Are Rising