V - Inflation Got You Down? Buy These 3 Undervalued Dividend Growth Stocks

2023-10-27 06:54:30 ET

Summary

- Per the CPI, the purchasing power of the U.S. dollar has diminished by 3.6% in the past year.

- Visa, American Electric Power, and McDonald's have handed out dividend hikes ranging from 6% to 15.6% to shareholders in that time.

- Each company has a low payout ratio for its respective industry and enjoys an investment-grade credit rating from S&P.

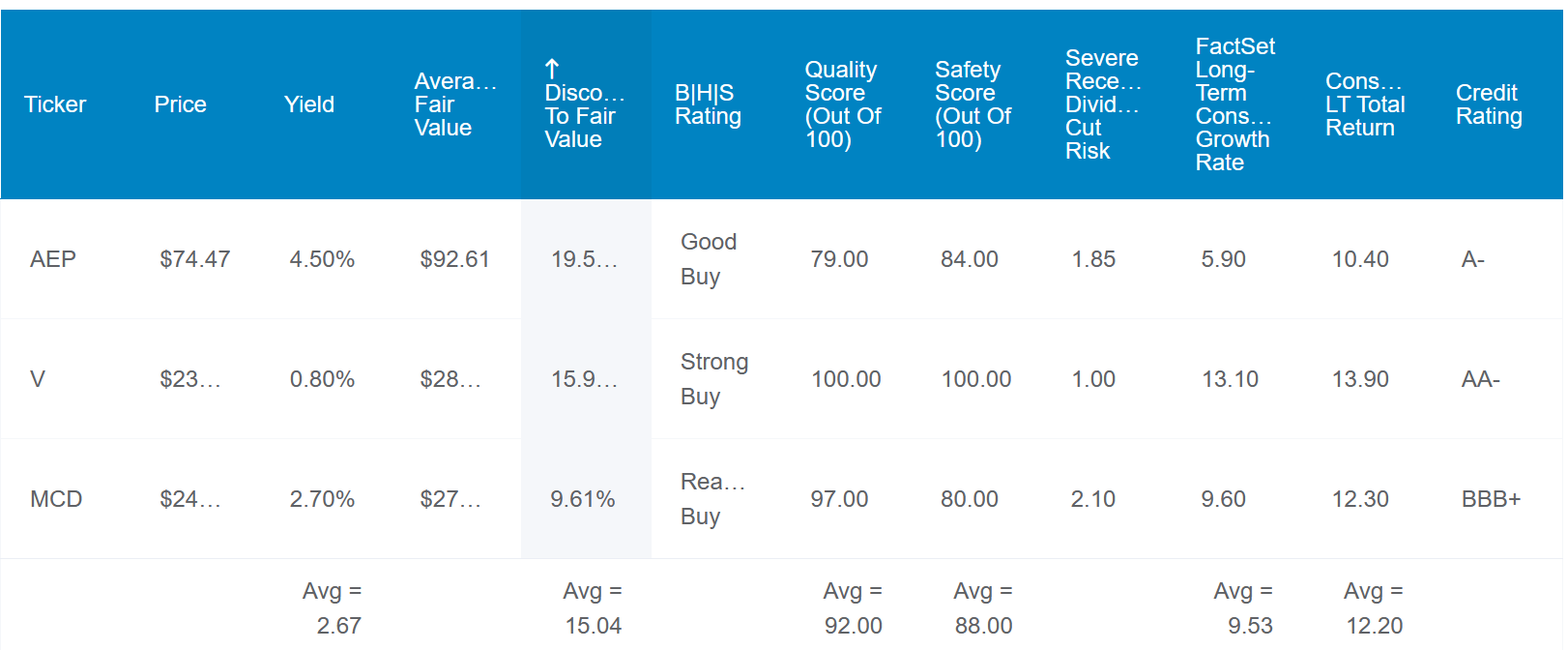

- The stocks vary from 6% to 26% discount relative to fair value.

- The trio of stocks could dramatically outperform the S&P 500 over the next 10 years.

It's a fact of life that the purchasing power of a U.S. Dollar (or any currency for that matter) steadily decreases year after year. From September 2022 to September 2023, the U.S. Dollar lost 3.6% of its purchasing power. Short of a Great Depression-like event causing debilitating deflation, this will continue to remain the case.

Since you and I don't have the power or influence to alter this reality, we must figure out how to adapt to it. My plan and proposal to others is to own world-class businesses.

This is because such businesses can consistently grow their revenue and earnings. That is what supports dividends that can grow above the rate of inflation over the long run.

What do I characterize as world-class companies? I mean businesses with solid growth prospects. I also mean businesses with payout ratios that are sustainable for their industry. Finally, companies that possess investment-grade balance sheets. Let's dig deeper into three companies that have handed out inflation-crushing raises over the past few weeks and average a 2.7% yield.

Visa: The World's Most Dominant Payments Company

{kind=link}

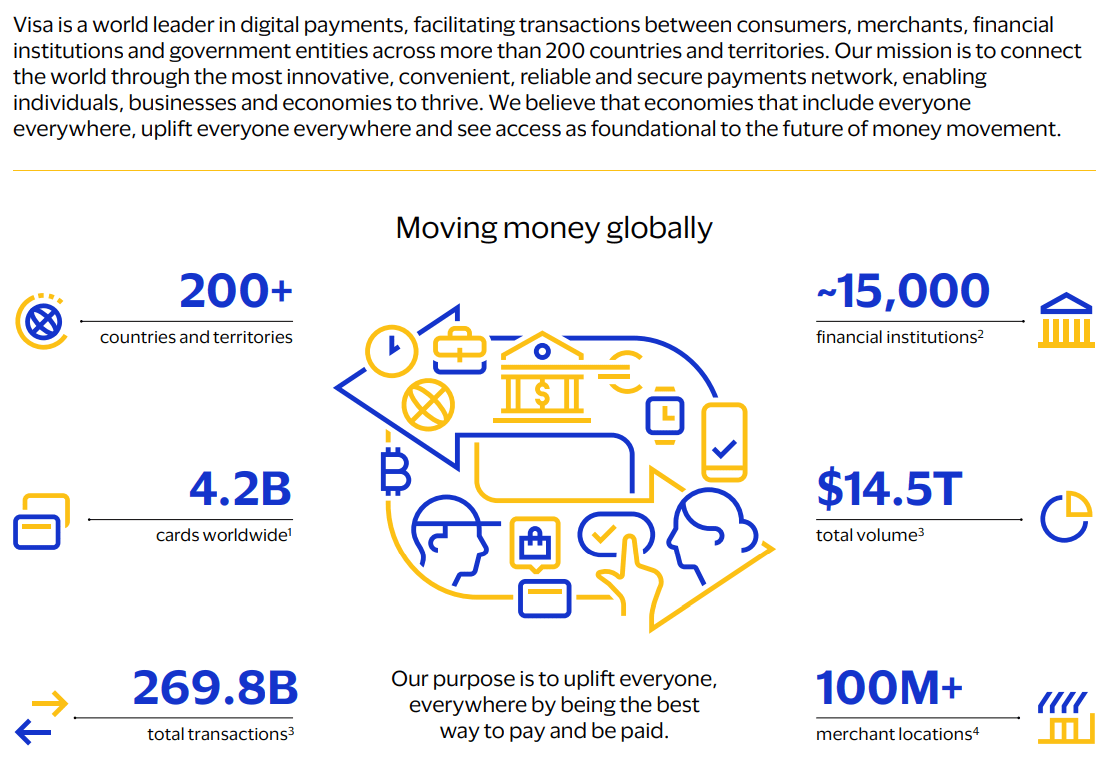

If you have at least one credit or debit card, the odds are quite high that Visa ( V ) is the company processing your transactions on its payment network. This is because Visa is accepted at over 100 million merchant locations around the world and processed nearly $15 trillion in total payment volume in the last four quarters. Such massive size and scale make it the largest payments company in the world.

Visa's 0.8% dividend yield doesn't jump off the page. But just recently, it hiked the quarterly dividend per share by 15.6% to $0.52 (and announced a $25 billion multi-year share buyback program). Since that dividend growth rate can double income every five years, Visa is an ideal pick for dividend growth investors who are younger like me.

For various reasons, the company should have little difficulty keeping up this dividend growth rate for quite a while longer. First, Visa's EPS payout ratio clocks in at just 21%. That is far below the 60% payout ratio that rating agencies consider to be safe. This gives the company a huge buffer to grow the dividend in line with earnings or even ahead of earnings for the foreseeable future.

Second, Visa's earnings growth prospects are robust. As credit/debit cards are adopted more in developing countries, an already huge addressable market should only get bigger from here on out. The unparalleled brand recognition and 4 billion-plus cards on Visa's network should lead to a virtuous cycle of more merchants adopting the payment method over time. That will drive more transactions and payment volume, which will fuel further net revenue and earnings growth for Visa. This is why the FactSet Research annual earnings growth consensus for the long term is 13.1%.

Finally, Visa's debt-to-capital ratio of 35% is less than the 40% that is viewed as viable by rating agencies for its industry. Among numerous other reasons, that is why the company possesses an AA- credit rating from S&P on a stable outlook. This means the company's implied 30-year bankruptcy risk is just 0.55%.

{kind=link}

Best of all, Visa's $232 share price is trading 26% below its updated fair value of $316 a share (as of October 26, 2023). That builds in a significant margin of safety for investors, which is what makes the stock a great buy for dividend growth investors.

American Electric Power: A Well-Established Electric Utility

AEP June 2023 Investor Presentation

{kind=link}

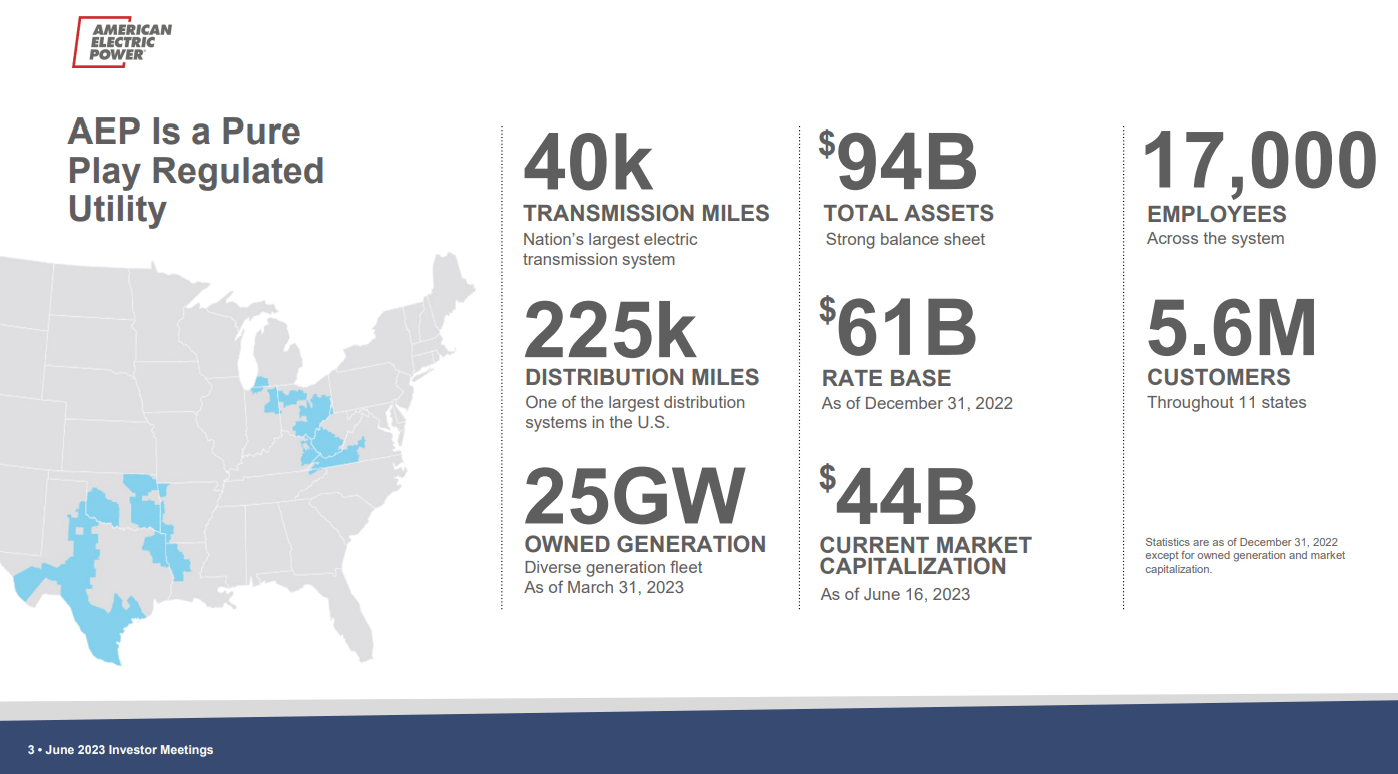

Operating in 11 states throughout the Southwest, Midwest, and Northeast, American Electric Power ( AEP ) is one of the largest regulated electric utilities in the country. Thanks to its 40K miles of transmission lines and 225K miles of distribution lines, the company provides 5.6 million customers with reliable and affordable electricity.

Even in this high interest rate environment, AEP's 4.5% dividend yield isn't too shabby. This is especially true when we consider that the company just upped its quarterly dividend per share by 6% to $0.88. Better yet, this level of dividend growth should persist in the years to come.

For one, AEP's EPS payout ratio currently stands at just 63%. That is well under the 75% payout ratio that rating agencies like to see from electric utilities. Not to mention that FactSet Research believes that AEP's earnings will rise by 5.9% annually - roughly in line with the company's 6% to 7% annual target.

The electric utility also is financially sound, with a debt-to-capital ratio of 55%. That's less than the 60% that rating agencies prefer for AEP's industry. This is why the company has an A- credit rating on a stable outlook from S&P. That carries with it just a 2.5% probability of bankruptcy by 2053. This excellent credit rating and manageable debt load should make AEP's $40 billion capital spending plan over the next five years attainable.

{kind=link}

Clinching the buy case for AEP, the stock's $76 share price is trading 20% below its updated fair value of $95 a share. This is a favorable valuation as an entry point for income investors.

McDonald's: It's Hard Not To Love This Dividend Aristocrat

With more than 40,000 locations in 100-plus countries throughout the world, McDonald's ( MCD ) has established itself as the heavyweight among fast food restaurant franchises.

The company just raised its quarterly dividend per share by 9.9% to $1.67, which was the 47th consecutive year that it increased its dividend. That's an attractive raise when coupled with McDonald's 2.7% yield. There are also plenty of reasons to believe similar payout growth can be maintained by the Golden Arches.

First of all, McDonald's EPS payout ratio of 58% is just below the 60% that is perceived as safe for its industry. This gives the company a realistic chance at serving up dividend growth in line with earnings growth moving forward.

Due to McDonald's burgeoning MyMcDonald's rewards program and franchised restaurant growth, the future is also bright. That is why FactSet Research is projecting 9.6% annual earnings growth over the long haul.

Perhaps the only thing to not love about McDonald's is its balance sheet. The company's debt-to-capital ratio of 114% is far higher than the 40% that rating agencies desire from its industry. The good news is that McDonald's isn't a very capital-intensive business since 95% of its restaurants are franchised, meaning franchisees bear startup costs. That is largely why even with its elevated debt load, the company still enjoys a BBB+ credit rating from S&P. This suggests just a 5% bankruptcy risk for the next 30 years.

{kind=link}

Lastly, McDonald's $257 share price is 6% less than its estimated fair value of $274 a share. The Dividend Aristocrat isn't a no-brainer buy, but it's arguably a classic case of a wonderful company at a fair valuation.

Summary: These Three Stocks Can Stave Off Inflation And Beat The S&P 500

{kind=link}

Visa, AEP, and McDonald's are fundamentally strong businesses that dividend investors should consider owning. Adjusting for Visa and AEP's higher fair values that aren't yet reflected in the Zen Research Terminal, the trio is trading at an 18% discount to fair value.

If growth transpires as expected and valuation multiples expand to fair value, the three stocks collectively could deliver the following annual total returns for the next 10 years:

- 2.7% yield + 9.5% annual earnings growth consensus + a 1.9% annual valuation multiple boost = 14.1% annual total returns or a 274% total return versus ~10% annual total returns or a 160% total return from the S&P 500 ( SP500 )

You can't ask for much more than high-quality businesses that are lower volatility and have greater total return potential than the S&P 500. That's why I like this trifecta of businesses quite a bit for the long term.

For further details see:

Inflation Got You Down? Buy These 3 Undervalued Dividend Growth Stocks