VGSH - Inflation Undershoots Fed Projections

2023-12-25 05:30:00 ET

Summary

- After years of underestimating inflation, Federal Reserve officials now appear to be overestimating it.

- Given the most recent inflation data, the FOMC should probably begin cutting its target rate in January.

- Fed officials should avoid erring in the opposite direction now that inflation has come down.

By William J. Luther

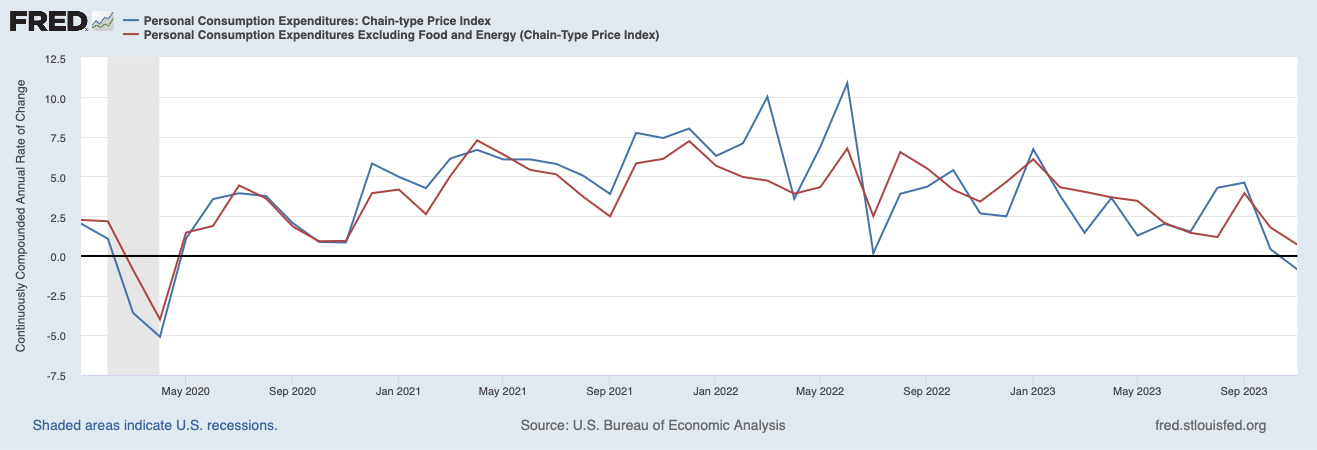

After years of underestimating inflation, Federal Reserve officials now appear to be overestimating it. The personal consumption expenditures price index (PCEPI), which is the Fed’s preferred measure of the price level, declined slightly in November. It was the first month of deflation recorded since April 2020.

Prices have grown at a continuously compounding annual rate of 2.6 percent over the last year, but much of the increase occurred in the first half of the period. Inflation has averaged 2.0 percent over the last six months and just 1.4 percent over the last three months.

{kind=link}

Core inflation, which excludes volatile food and energy prices and is thought to be a more reliable indicator of future inflation, is also low. Core PCEPI has grown at a continuously compounding annual rate of 3.1 percent over the last year. It has grown 1.9 percent on average over the last six months and 2.1 percent on average over the last three months.

Last week, Federal Open Market Committee (FOMC) members projected 2.7 to 3.2 percent PCEPI inflation for 2023, with a median projection of 2.8 percent. Actual inflation will almost certainly come in below that range. Prices have grown just 2.4 percent year-to-date. Prices would need to grow at an annualized rate of 3.1 percent or more in December 2023 to hit the low end of the projected range.

Those same officials projected inflation would remain above target over the next two years. Projections ranged from 2.1 to 2.7 percent for 2024, with the median FOMC member projecting 2.4 percent. They ranged from 2.0 to 2.5 percent in 2025, with a median projection of 2.1 percent.

Bond markets, in contrast, suggest inflation will be on target. After adjusting the TIPS spread to account for the average difference between the consumer price index (CPI) and PCEPI, I estimate the breakeven PCEPI inflation rate - that is, the rate bond traders are pricing in - at 2.0 percent over the five- and ten-year horizons. In other words, those putting their money where their mouth is expect inflation will be around 2 percent.

It is important that FOMC members accurately project inflation conditional on their monetary policies. When FOMC members underestimate inflation, as they did in 2021 and 2022 , they will tend to do too little to keep inflation down. When FOMC members overestimate inflation, as they appear to be doing now, they will tend to do too much - increasing the risk of a painful recession.

The FOMC changed course last week, foregoing a previously projected rate hike and projecting deeper rate cuts in 2024 than previously anticipated. But those rate cuts may come too late. The federal funds futures market is currently pricing in a 14.5 percent chance that rates will be lower following the Fed’s meeting in January. The FOMC looks unlikely to cut its target rate until March.

Given the most recent inflation data, the FOMC should probably begin cutting its target rate in January. Lower-than-anticipated inflation means that the real (i.e., inflation-adjusted) federal funds rate target is higher than FOMC members intended it to be.

Using last month’s core inflation rate (0.7 percent) as a proxy for expected inflation, I estimate the real federal funds rate target range at 4.55 to 4.80 percent. For comparison, the New York Fed estimated the natural rate of interest - the rate that would keep policy neutral - at 0.88 to 1.19 percent for Q3-2023. Even if the natural rate has risen somewhat in Q4, monetary policy looks very, very tight. A 25-basis point cut would not change the stance of monetary policy from tight to neutral or loose, but it would reduce the extent to which policy is tight - and might prevent the Fed from overtightening.

The Fed was very late to address rising inflation in 2021 . Inflation remained too high for too long as a consequence. Fed officials should avoid erring in the opposite direction now that inflation has come down.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Inflation Undershoots Fed Projections