III - Information Services Group: Competition Will Limit Any Progress

2023-12-27 16:50:22 ET

Summary

- Despite rapid technological development, III has struggled with growth, only achieving a CAGR of 4%. We believe the business struggles with competition relative to its much larger peers.

- III is positioned to succeed but is lacking scale and expertise required to outperform. The industry is highly attractive but we see limited reason for clients to choose III.

- Its mild growth and competitive position have limited margin appreciation, further compounding its weakness. When compared to its peers, the company significantly underperforms.

- Recent performance has been strong, as macroeconomic tailwinds are not sufficient to offset the broader industry strength. We expect healthy growth to continue, although III’s ability to partake will be limited.

- III’s valuation does suggest upside, particularly with an NTM FCF yield of ~12%, but we are not convinced. Buying a subpar business at a time when equities are depressed is not preferable.

Investment thesis

Our current investment thesis is:

- III operates in a highly lucrative industry that is growing well and appears well-positioned for long-term success. This said, the company has struggled to gain a material footing, with poor/volatile growth, limited margin gains, and minimal commercial development. It faces competition from significantly larger peers, many of whom are categorically superior through wide moats, implying III will continue to see subpar growth.

- We are not in the business of buying weak businesses unless we see a compelling opportunity for upside. This is not the case with III. It is only trading at a moderate discount to its historical average, which does not suggest a material upside given the limited development.

Company description

Information Services Group, Inc. ( III ) is a leading global technology research and advisory firm, specializing in digital transformation services. ISG provides innovative solutions to help businesses navigate the complexities of the digital world and make informed decisions.

Share price

III’s share price performance has been very underwhelming during the last decade, returning a meager ~15% while the wider market has comfortably exceeded 150%. This is a reflection of its poor financial development and commercial challenges faced, restricting the scope for future upside.

Financial analysis

{kind=link}

III Financials (Capital IQ)

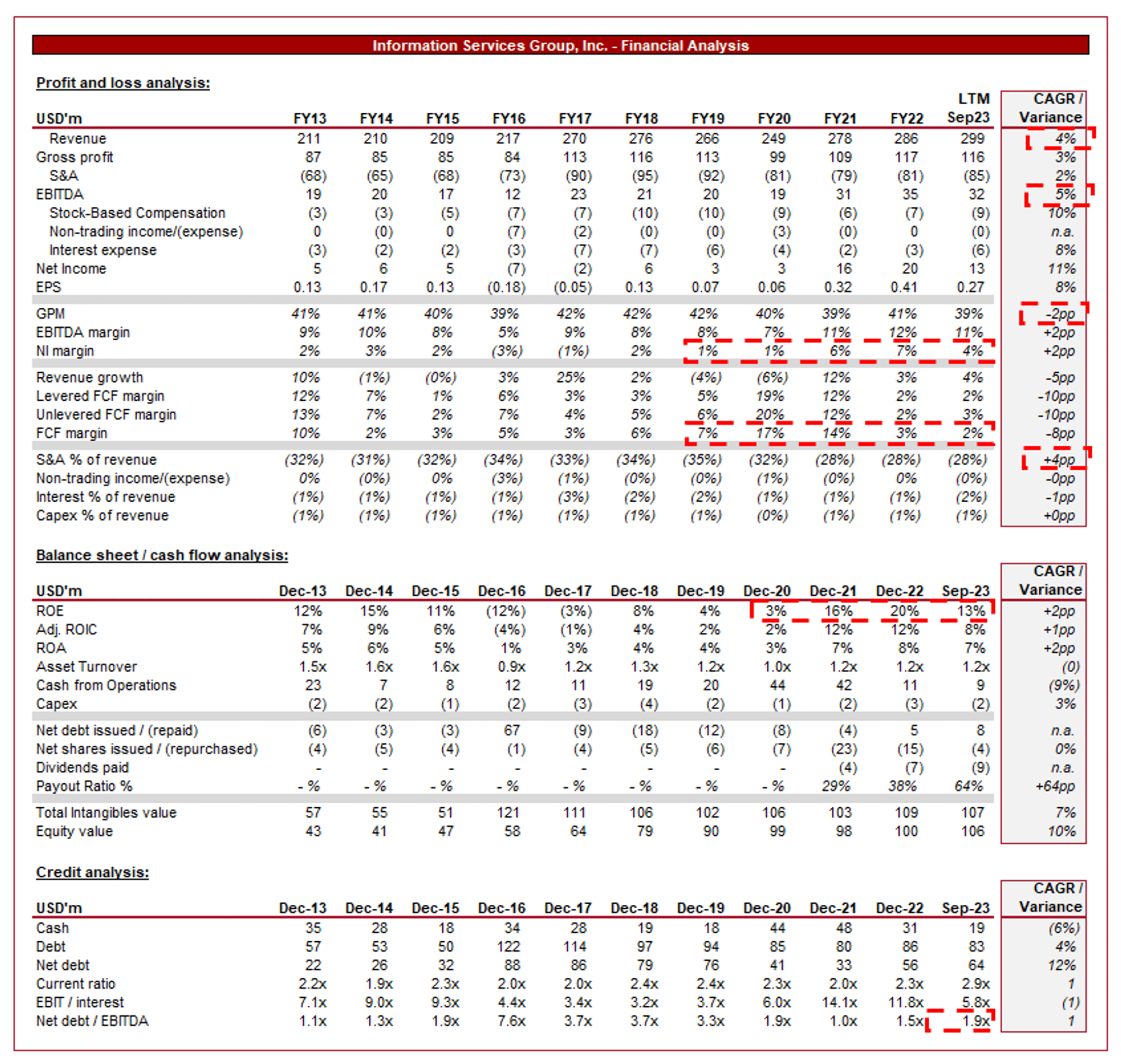

Presented above are III's financial results.

Revenue & Commercial Factors

III’s revenue has grown mildly during the last decade, with a CAGR of +4%. EBITDA has broadly matched this at +5%, which many will likely consider as disappointing given the rapid acceleration of technological development and adoption.

Business Model

{kind=link}

III

III primarily offers advisory services to businesses looking to navigate digital transformation, technology adoption, and outsourcing strategies. This includes providing insights, research, and consulting services to help clients make informed decisions.

The company conducts and collates extensive research on emerging technologies, market trends, and industry best practices. This research forms the basis for the advice, data, and recommendations provided to clients. With the increasing importance of digital transformation, III’s services have been increasingly relied upon on an ongoing basis. Further, ISG also has a focus on outsourcing advisory services, helping clients optimize their outsourcing strategies.

III operates globally, allowing it to serve clients across different regions. This global presence is essential for understanding regional nuances and regulatory environments to support multinational clients.

III operates a subscription-based model for its research. This model provides a recurring revenue stream for the company and establishes long-term partnerships with clients, creating the scope for up/cross-selling over time and reducing revenue growth volatility.

III has served many leading multinational to varying degrees over its historical period, although its size and expertise has limited the breadth of its scope. Most of these businesses are working with a range of other firms to encompass all of their needs.

{kind=link}

III

Competitive Positioning and Industry

The global service industry is estimated to be a $1t industry, alongside the sourcing industry which is a further $100b. The industry is highly competitive, with a range of consulting and data firms competing in various verticals.

We believe III competes alongside Gartner ( IT ), Forrester Research ( FORR ), Cognizant ( CTSH ), the big 4 audit firms, Capgemini ( CAPMF ), Accenture ( ACN ), IBM ( IBM ), in particular. Management believes it is well placed because “ no one competitor has the breadth of ISG offerings ”. This is an interesting claim. It may be strictly factual in that it is rare to see a fully capable consulting firm with proprietary research but this is a major stretch. We would suggest the opposite. III’s shortcomings mean its potential clients are more likely to get their research from a specialist, such as Gartner (better capabilities and larger data repository), and its consulting from a specialist, such as Capgemini (greater scale, expertise, and track record).

We believe the following are also key factors impacting growth:

- Market Saturation: The market for technology advisory services has become increasingly competitive and, in some segments, saturated. This will make it incredibly challenging for ISG to capture new clients and expand its market share.

- Technological Disruptions: While ISG advises clients on embracing technological disruptions, it must ensure it is consistently developing its understanding and capabilities to be at the forefront of new discoveries. Its lack of scale relative to its peers will inevitably increase its go-to-market timing.

- Long Sales Cycles: Advisory services often involve long sales cycles, especially when dealing with complex outsourcing contracts or significant digital transformation initiatives. For this reason, it can be difficult for smaller firms to pitch against larger ones, lacking the perceived expertise and resources to deliver.

- AI, Cybersecurity, and Cloud capabilities: These three technologies will be the driving force of growth in the coming years. III boasts capabilities in these areas, ensuring that it is at least “in the game”.

Margins

{kind=link}

Margins (Capital IQ)

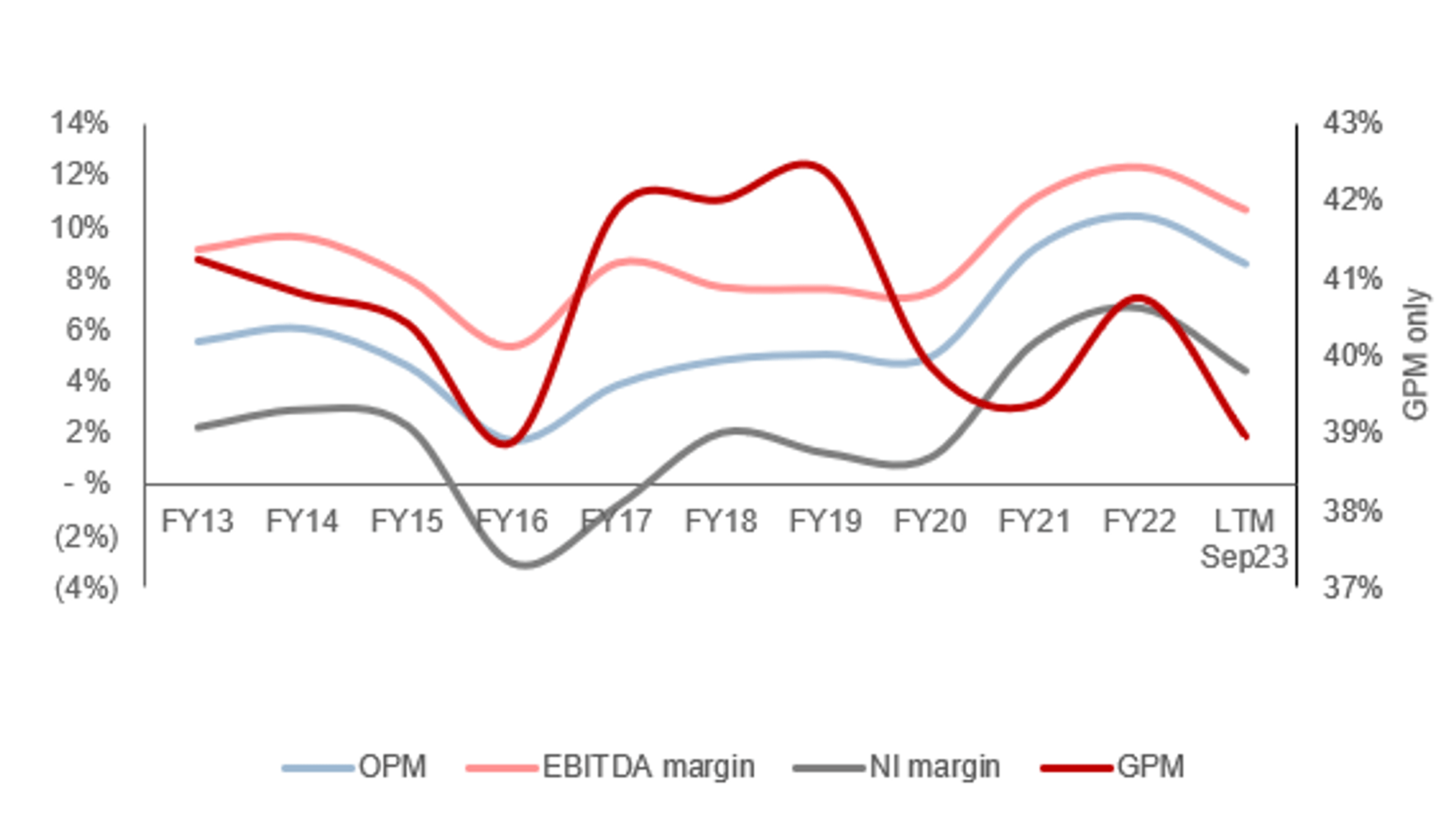

III’s margins have lacked material improvement during the last decade, although are broadly ahead of its FY13 level. This improvement is a reflection of operating cost leverage, as S&A spending has declined from 32% of revenue in FY13 to 28% in the LTM.

The challenge within this industry is achieving persistent margin improvement outside of non-labor-intensive solutions. As employees are the value drivers, the expectation is for compensation to broadly track any increases in fees, limiting margin improvement. This is likely why III’s GPM has stayed flat between 39% and 42%. Further, this illustrates that its SaaS / recurring revenue growth has not been sufficient to have a meaningful profitability impact, or at least not an accretive one (theoretically could be offsetting a decline in other areas).

For these reasons, we are not overly positive about margin appreciation in the coming years, although the company has shown an ability to maintain its existing level with soft growth.

Quarterly results

III recent performance has been healthy, with top-line revenue growth of +6.6%, +8.2%, +5.5%, and +4.3% in its last four quarters. In conjunction with this, margins have remained broadly flat, although slightly lower than its FY22 level.

This strength is partially a reflection of lower comparable periods. With elevated interest rates and inflation, businesses have sought to cut costs as they have experienced supply-chain issues and softening demand. This has contributed to slower decision-making regarding capital allocation and stretched spending over longer periods of time. Management teams are currently cautious, and rightfully so, and this will only continue with geopolitical tension and the rising fears of a recession again.

This said, the company is positioned well for resilient demand. With a growing recurring revenue base and a supportive services suite, businesses are unlikely to make short-term decisions to cut costs to the detriment of their long-term success. The issue will be with new business origination.

Balance sheet & Cash Flows

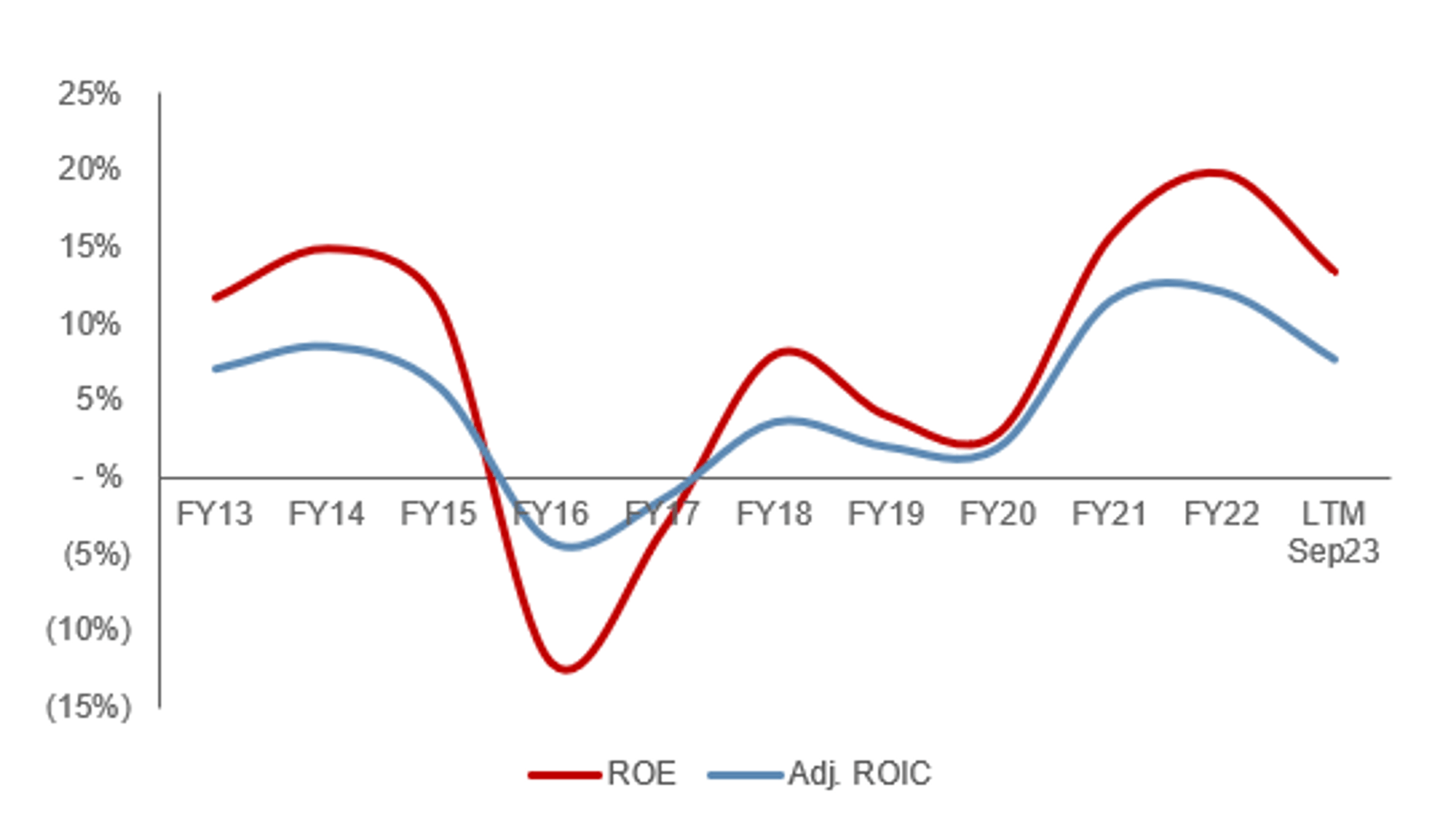

III is conservatively financed, with an ND/EBITDA ratio of 1.9x. This has allowed Management flexibility over its capital allocation, choosing to repurchase shares and conduct periodic M&A. This has allowed for an attractive ROE, although appreciating its volatility.

We would like to see the company increase its M&A activity, as this has the scope to develop its technical capabilities and competitive position. Most recently, III acquired Ventana Research, bolstering its Software Advisory capabilities.

{kind=link}

Returns (Capital IQ)

Outlook

{kind=link}

Outlook (Capital IQ)

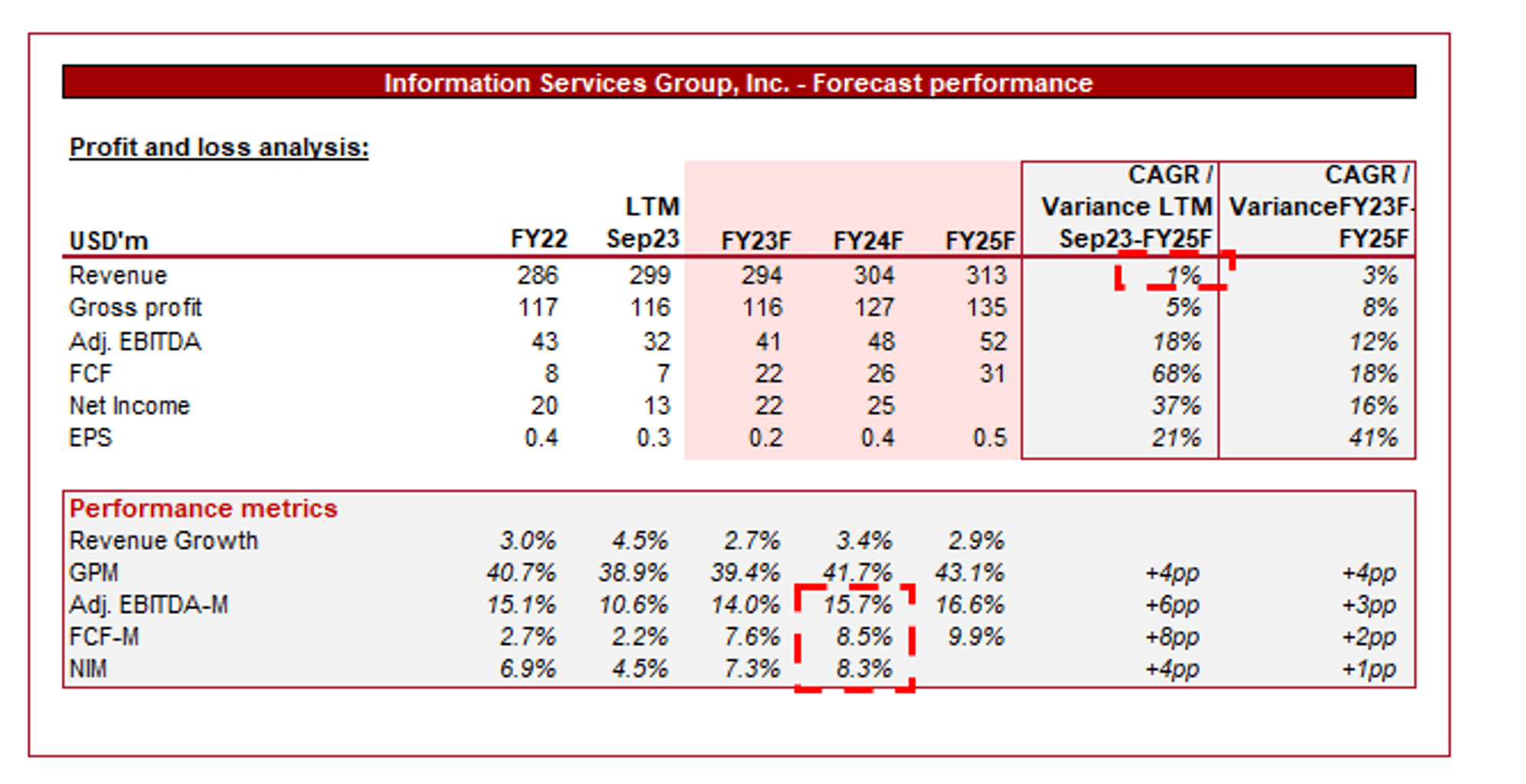

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a continuation of its mild growth, with a CAGR of 3% between FY23F and FY25F. In conjunction with this, margins are expected to sequentially improve, reaching an adjusted EBITDA-M of 16.6% in FY25F.

We are broadly aligned with these assumptions. The company is not overly competitive, at least to the extent it can gain market share, leading to the expectation of a persistent underperformance. Given ~4% has been achieved historically, we expect this to continue in the coming years (alongside the near-term impact of softening spending).

Further, although we have seen limited improvement thus far, theoretically the company should achieve margin appreciation through growth in its recurring revenue streams, which continue to outperform the wider company.

Industry analysis

{kind=link}

Seeking Alpha

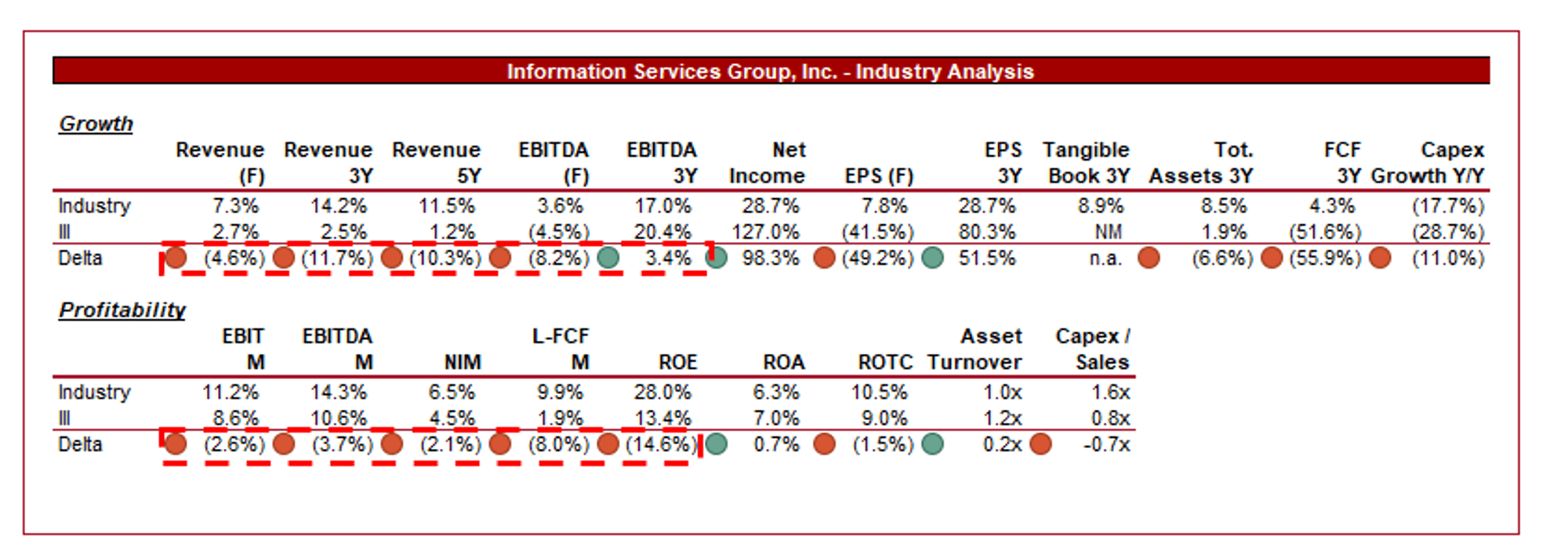

Presented above is a comparison of III's growth and profitability to the average of its industry, as defined by Seeking Alpha (27 companies).

III disappoints relative to its peers. The lack of revenue growth is a direct reflection of its competitive position, with its peers providing a superior offering, limiting III’s ability to gain market share. The lucrative nature of the industry makes it hotly contested, with industry recognition and reputation a major driver of new business.

Further, its lack of scale, product mix, and material SaaS/recurring offering contribute to a below-average margin profile.

Valuation

{kind=link}

Valuation (Capital IQ)

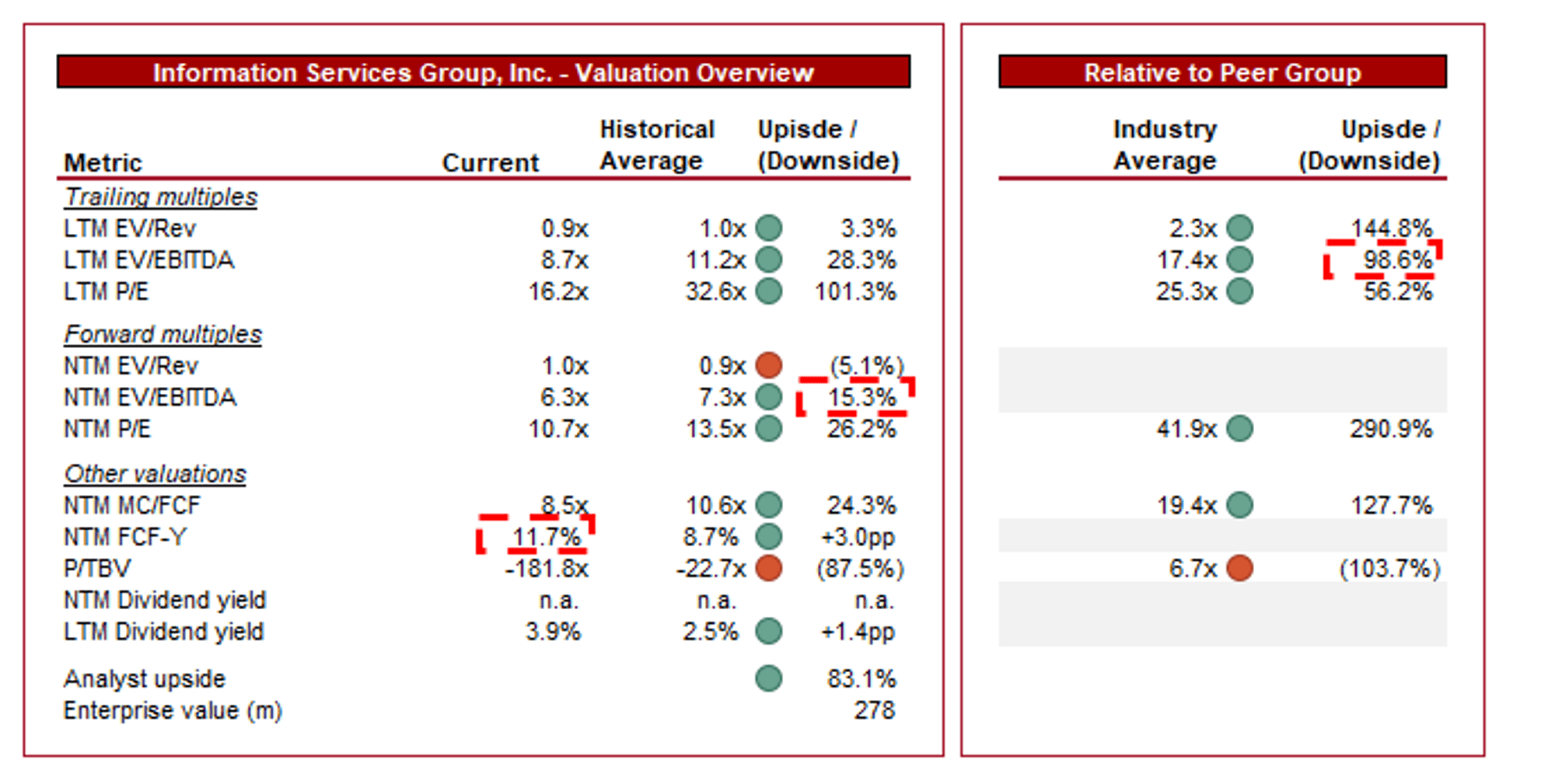

III is currently trading at 9x LTM EBITDA and 6x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view, primarily due to the limited financial development achieved, underpinned by a weakening commercial position. At a 15-28% discount on an EBITDA basis, we believe the company is well-priced.

Further, the company is trading at a significant discount to its peers, ~98% on an LTM EBITDA basis and ~290% on an NTM P/E basis. This is inevitably partially reflective of its poor financial performance and limited development relative to its peers. This said, the degree of discount does appear excessive.

At an NTM FCF yield of 12%, the business does appear undervalued. The key question is whether its business model is sufficiently sustainable to allow investors to enjoy this. We are skeptical, although not materially so.

{kind=link}

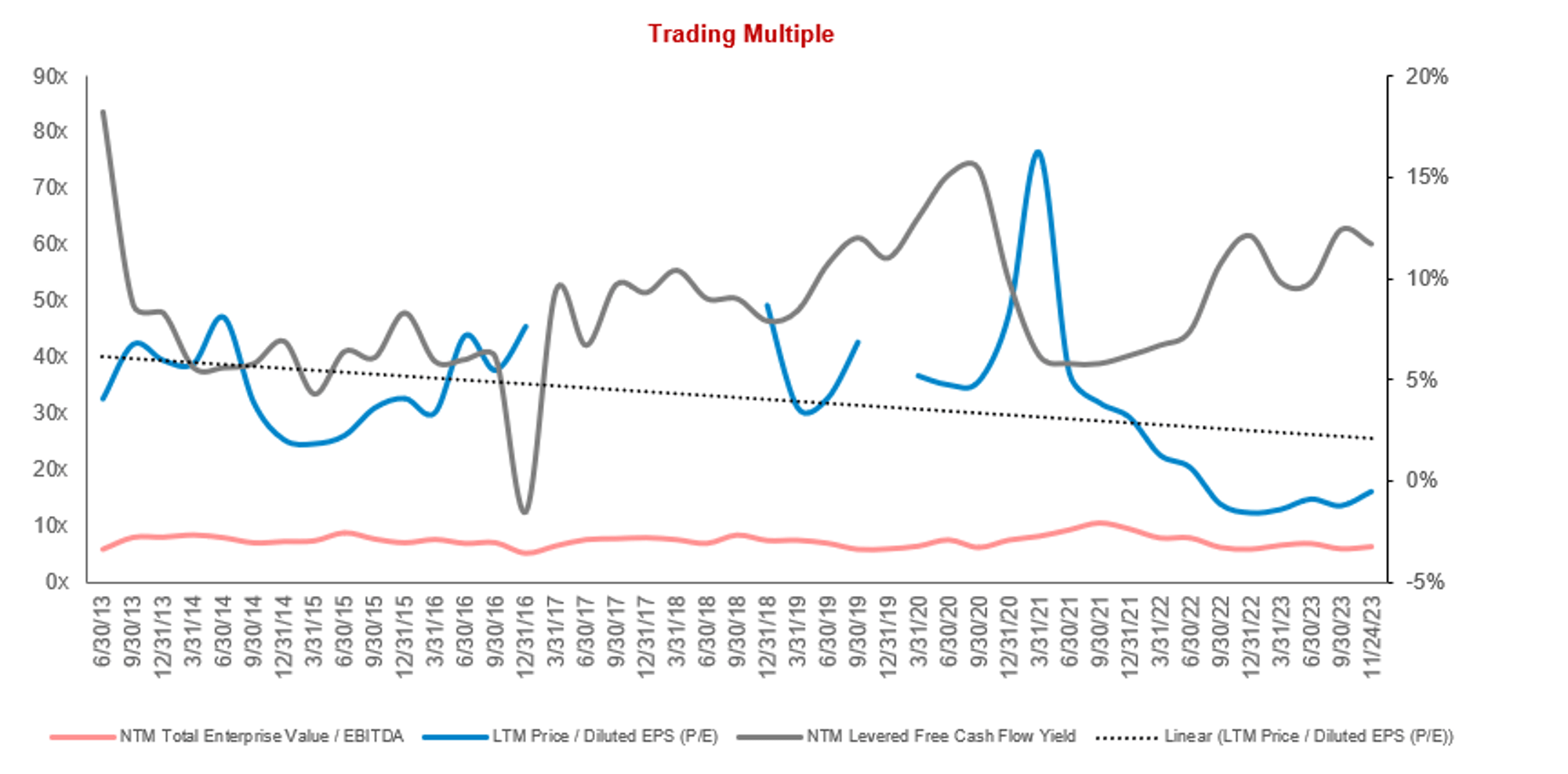

Valuation evolution (Capital IQ)

III does represent a potential takeover target, with a larger consolidator acquiring its expertise, while synergistic benefits and cross-selling opportunities contribute to an improvement in financial performance. The concern with this is again its competitive position and also how far margins can improve. No competitor will accept material dilution.

Key risks with our thesis

The risks to our current thesis are:

- Successful adaptation to emerging technologies.

- Strategic partnerships driving an increase in market recognition.

- Economic downturn impacting corporate spending.

- Failure to keep up with rapid technological changes.

Final thoughts

III’s ability to achieve growth is commendable given the level of competition it faces, yet we are not supportive of this being an attractive investment. The company is a weaker participant and lacks any material characteristics that can improve its fortune. Realistically, its growth will continue to lag behind its peers and the risk of client departures increases as its peers out develop it. This is why, despite hints of it being undervalued, we do not suggest the stock is a buy.

For further details see:

Information Services Group: Competition Will Limit Any Progress