CTSH - Infosys' Agile Adaptability In A Volatile Market

2023-04-19 01:41:42 ET

Summary

- The company's focus on cost control and efficiency, as well as trimming fat and tidying vendor relationships, could improve profitability and drive revenue growth.

- Infosys' pipeline of deals is jam-packed and potential mergers and acquisitions add to its strategic belt.

- Infosys has displayed adaptability to shifting circumstances and has consistently hit annual revenue and margin guidance, but risks and headwinds remain.

Thesis

As Infosys (INFY) faces a range of challenges, including cancelled and terminated projects, vendor consolidation agreements, and economic instability among its client base, investors like myself have become increasingly wary of the company's future prospects. In this article, I will explore the risks and headwinds that are impacting Infosys' growth trajectory as well as potential strategies for mitigating these challenges to improve profitability.

Infosys's Agile Adaptability

From my perspective, Infosys' display of resolute pluck in maintaining its tightrope of growth and profitability, while deftly navigating the precarious economic landscape, could very well be considered nothing short of remarkable (if we ignore the risks and headwinds noted below). The company's chameleon-like adaptability to shifting circumstances has allowed them to consistently hit the mark on their annual guidance for revenue and margin, even in the face of life's little surprises.

In my estimation, Infosys' ironclad guidance for the upcoming quarter predicts a growth range of 4-7% , demonstrating their confidence in navigating the current economic quagmire. Their bulging war chest of hefty deals could very well catapult the company toward the upper echelons of growth expectations. To my mind, the company's unwavering focus on cost control and efficiency has them reaching for the stars, with higher margins gleaming tantalizingly on the horizon. As I see it, Infosys's strategic pivot and their laser-like focus on trimming the fat and tidying up their vendor relationships could potentially set a stage to jolt revenue growth into overdrive in the coming year. My assessment is that the company's pipeline is so jam-packed with sizable deals that it's practically bursting at the seams. And, if that wasn't enough, the potential for mergers and acquisitions adds yet another notch to their already impressive strategic belt, a prospect that should have shareholders grinning from ear to ear.

So from my point of view, Infosys's Herculean balance sheet positions them rather cozily to seize any golden opportunities that come knocking if it weren't for those pesky risks. The company's performance in FY '23 is a veritable smorgasbord of success, with a healthy serving of growth across various business segments, and most reaching the coveted double-digit mark. Upon further examination, the digital business soared by 25.6%, while core services witnessed a 1.9% uptick. This paints a picture of Infosys straddling the dual realms of digital transformation and cost efficiency, automation, and consolidation with aplomb—all key ingredients to their growth recipe. The way I see it, with a rock-solid operating margin of 21% and $2.5 billion in free cash flow, Infosys has a slight glimmer of hope in becoming a shining beacon of financial stability in a tumultuous technical world.

Peer Evaluation and Dividend Status

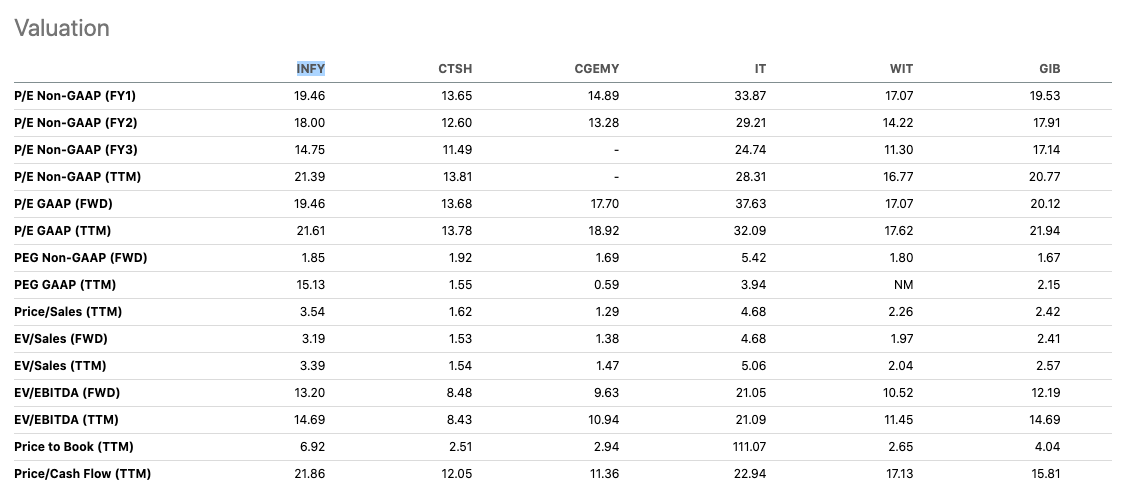

Unfortunately, upon examining Infosys, it appears that the firm's valuation stands at a premium relative to its industry counterparts. The evidence for this assessment can be found in several key financial ratios:

{kind=link}

Forward Price-to-Earnings Ratios: With a ratio of 19.46, INFY's forward P/E exceeds that of the majority of its competitors ([[CTSH]], [[CGEMY]], [[WIT]], [[GIB]]), save for IT, which sports a considerably higher figure of 33.87. This suggests that market participants are attributing a higher value to INFY's earnings per share, rendering the company comparatively more costly.

Forward PEG Ratios (non-GAAP): At 1.85, INFY's forward PEG ratio also outstrips most of its peers, again barring IT, which boasts an even loftier 5.42. This heightened ratio implies that INFY's equity valuation may not align with the firm's earnings growth trajectory, raising the specter of overvaluation.

Forward EV/EBITDA Ratios: Similarly, INFY's forward EV/EBITDA ratio of 13.20 surpasses that of its peers (CTSH, CGEMY, WIT, GIB), with only IT exhibiting a higher figure of 21.05. This metric intimates that the company's enterprise value may not be commensurate with its earnings before interest, taxes, depreciation, and amortization, further pointing to potential overvaluation.

Price-to-Book Ratios ((TTM)): INFY's price-to-book ratio of 6.92 is substantially greater than all its industry peers (CTSH, CGEMY, WIT, GIB), with the notable exception of IT, which registers a staggering 111.07. A higher price-to-book ratio signals that the firm's stock price may not reflect its net asset value accurately, hinting at overvaluation.

{kind=link}

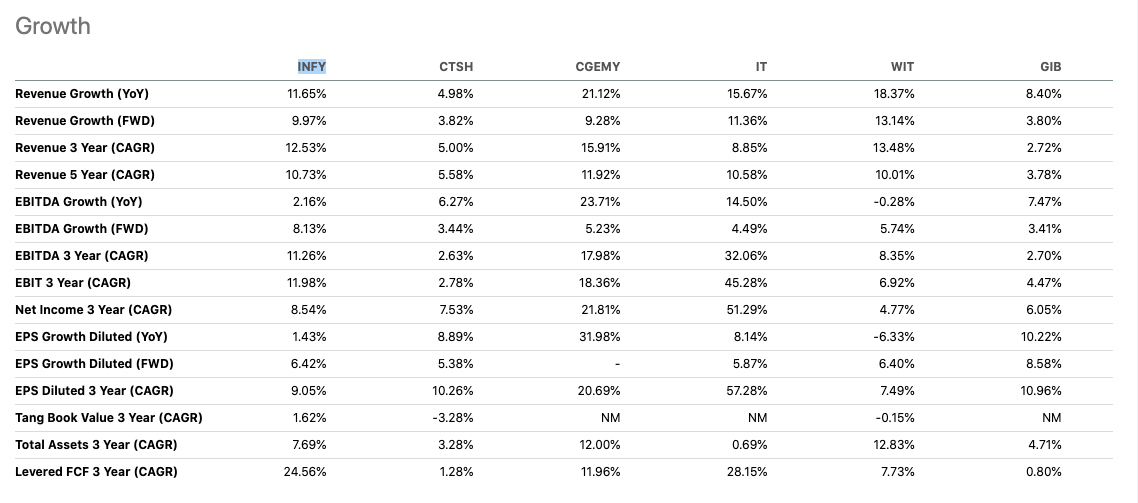

Nonetheless, it is crucial to acknowledge that INFY has demonstrated more robust revenue growth rates (YoY, FWD, 3-year, and 5-year CAGR) than most of its peers, potentially providing a partial rationale for the elevated valuation ratios. However, the company's mixed profitability metrics (gross profit margin, EBIT margin, net income margin) and return ratios (return on equity, return on assets) render it challenging to justify the heightened valuation ratios based solely on growth and profitability factors.

{kind=link}

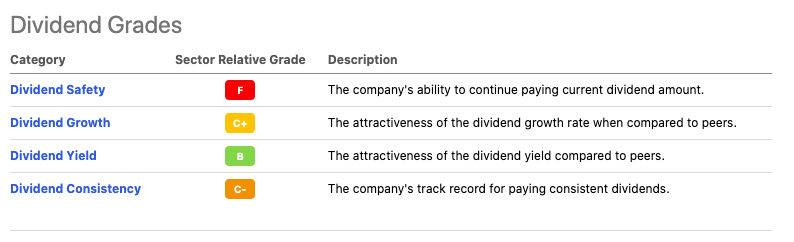

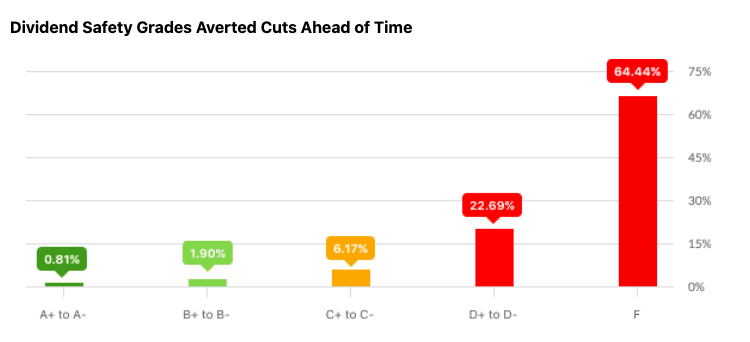

Finally, INFY stock currently boasts an underwhelming Dividend Safety Score of F . Essentially, what that indicates as that over the past 11 years, an astonishing 64.4% of stocks with similar ratings have taken a swift nosedive in their dividends. Now, this little nugget of wisdom is nothing short of disastrous for those investors who cling to their dividends like a life raft in a sea of uncertainty.

{kind=link}

If history is any indication, Infosys could be on the precipice of leaving them high and dry, frantically searching for a new steady stream of income. Therefore, If you are looking for alternatives to Infosys as far as dividends are concerned, you might want to check out a list of " Top Rated Quant Dividend Stocks" .

Risks and Headwinds

From my perspective, Infosys is grappling with the disconcerting reality of abruptly terminated and cancelled projects. It came to my attention that this predicament could signal a broader economic instability gnawing away at the firm's client base. As a result, these vulnerabilities may drive Infosys into fierce price negotiations, potentially stifling their growth trajectory. The sudden evaporation of projects also raises concerns about their discretionary nature and the potential for vendor consolidation agreements that could put Infosys at a disadvantage.

In my estimation, Infosys' recent 3.2% decline in revenue is far from reassuring, and the puzzling "one-off client issue" only intensifies investor apprehension. During the Q4 earnings call, CFO Nilanjan Roy tried to shed light on the issue.

Yes. So like I said earlier, this is a one-off client revenue issues, and there are a number of clients -- it's a mixture of clients, and some of it is a provision against them. Some may come back, some may not come back. And some of it is also due to cancellations, right, because the revenue impact also beyond the volume impact of cancellations. Yes, I mean, it is -- there is a mixture of clients there.

Meanwhile, the 10% drop in the US telecom sector is another red flag, indicating potential headwinds. Although Infosys seems to have achieved an acceptable margin walk, there's no denying the likelihood of deferred costs emerging in the coming quarters, eroding profitability. To my mind, the wide range of Infosys' growth predictions for the next quarter suggests an unpredictable landscape. Granted, they've embarked on a cost-cutting and efficiency-enhancing endeavor, but the long-term effectiveness remains to be seen, especially with impending salary increases. Furthermore, Infosys' proclivity for M&A activities could encounter obstacles in identifying suitable targets that align with both strategic and cultural criteria, leading to slow capital deployment.

Takeaway

In summary, from where I stand, there's reason to be skeptical about Infosys' capacity to expand and maintain profitability in the current, volatile market. A pipeline of significant deals might be in the works, but industries like financial services, telecommunications, and retail are taking the hardest hit, causing delays in decision-making and unpredictability in spending. Add to the mix a few departures of top executives, and Infosys' leadership may face even greater challenges this year. So overall, it's a tough call. On one hand, I think it's fair to say that Infosys deserves a "sell" rating; however, in light of the oversold technical indicators (a weekly RSI of 31 and a daily at a significantly oversold indicator of 23) I believe that the bad news has been priced in and therefore, a "hold" rating is a far more judicious strategy.

For further details see:

Infosys' Agile Adaptability In A Volatile Market