EUFN - ING Groep: A European Dividend Standout Buying Back Stock

2023-12-24 09:00:00 ET

Summary

- European stocks offer a potentially better value compared to the US market, with the Euro Area trading at just 12.3 times NTM EPS estimates.

- ING Groep is a European bank that has performed well recently, with strong Q3 earnings, a 2.5 billion euro buyback program, and a yield north of 5%.

- ING has attractive valuation metrics, with a high dividend yield and potential for future growth. Technical indicators suggest a bullish breakout potential.

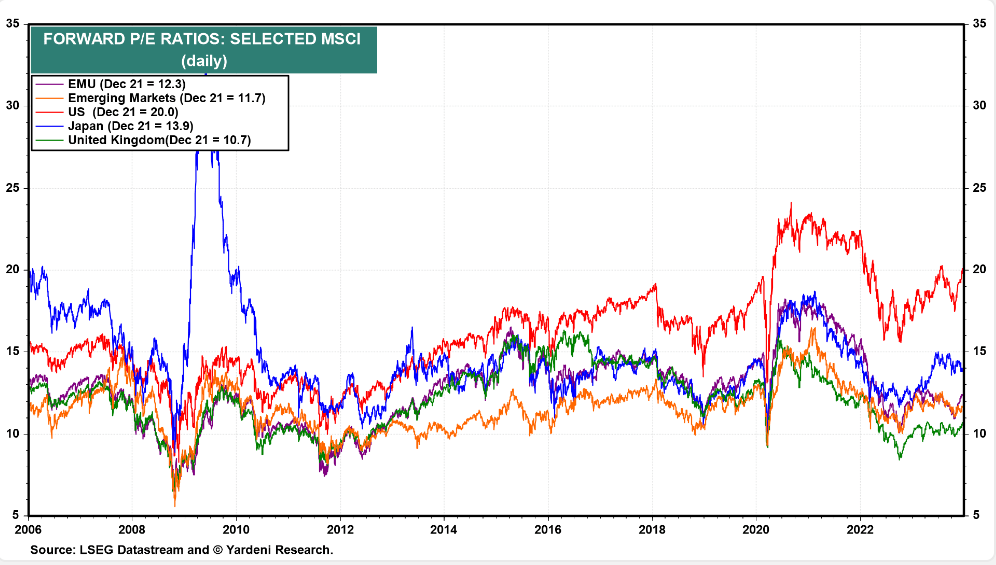

European stocks remain a tremendous value compared with the domestic equity market. It was just a few months ago that pundits were clamoring in favor of US small and mid-cap stocks due to their low-teens forward price-to-earnings ratios. Given a more than 20% rally off their October lows, the SMIDs now sells for about 15x 2024’s expected per-share profits – not quite the steal of a deal they once were. You can still find big value overseas, however. The Euro Area is inexpensive at just 12.3 times NTM EPS estimates – that is an earnings yield of more than 8%. Let’s take a look at a European bank that has performed well recently.

I reiterate my buy rating on ING Groep N.V. ( ING ). I see shares as significantly undervalued, while investors are paid a high dividend yield to wait for shares to appreciate.

Global Equity Valuations: Cheap Stocks in Europe, 12.3x P/E

{kind=link}

According to Bank of America Global Research, ING Group is a global financial institution (Dutch origin), offering banking services. Following the sale of its remaining stakes in insurance operations, ING will become a pure bank with a European retail focus combined with a global Commercial Banking activity.

The Amsterdam-based $50.5 billion market cap Diversified Banks industry company within the Financials sector trades at a low 7.1 forward non-GAAP price-to-earnings ratio, and it pays a high 5.4% trailing dividend yield. Ahead of its Q4 2023 earnings due out in early February, shares trade with a low 19% implied volatility percentage, while short interest on the stock is modest.

Back in November, ING reported an adjusted net profit of 2.1 billion euros in the third quarter, topping estimates. Profit before taxes jumped significantly to 2.9 billion euros, while its CET1 ratio rose to 15.2%. Total income surged 32% compared to year-ago levels, and its net interest margin improved a basis point to 1.57%. Strong top-line performance and some cost-cutting drove the beat. Its net interest income climbed 21% YoY, driven by stable liability margins and easing lending margin pressure.

From a shareholder’s perspective, ING announced a 2.5-billion-euro buyback program in early November, too. The stated goal was to converge its CET1 ratio towards its 12.5% target, and since the rate was well in excess of the objective, repurchasing shares was a way to reward stockholders. Reducing the share count also lowers the equity portion of a firm's capital structure. The stock has risen by more than 10% since that announcement . Not surprisingly, analysts at J.P. Morgan have ING on their list of top picks with dividend yields above 4%.

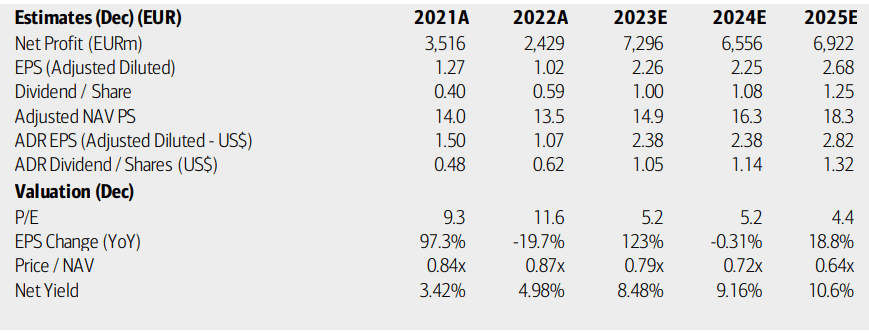

On valuation , analysts at BofA see earnings rising to $2.38 this year, but then stalling at that level in 2024. Per-share profits are then expected to return to the upswing by 2025. The current consensus figures, per Seeking Alpha, reveal normalized EPS expectations between $2.10 and $2.20 while top-line numbers hold steady around $25 billion annually.

Dividends, meanwhile, are forecast to rise at a fast pace over the coming quarters, with a net yield perhaps surpassing 10% in the out years, so says BofA. While profit growth is not all that impressive, ING’s very cheap earnings multiple and with a price-to-book ratio that is under 1, value investors must at least be intrigued by this rebounding bank.

ING: Earnings, Valuation, Dividend Yield Forecasts

{kind=link}

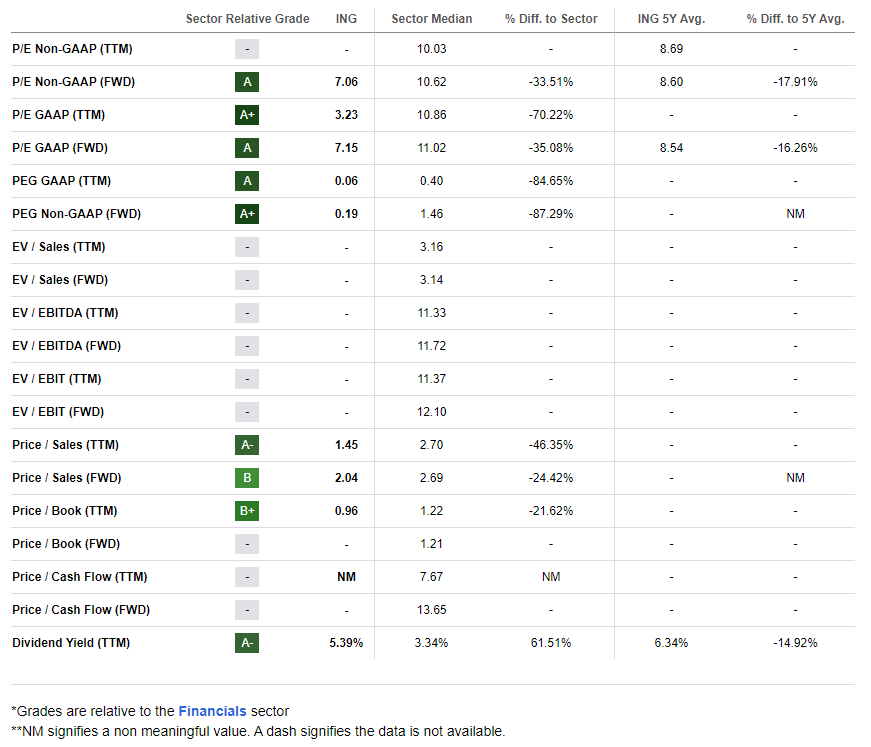

If we assume normalized EPS of $2.15 and apply a mere 10 forward non-GAAP P/E ratio (below the sector multiple), then shares should be $21.50. What’s more, if we give ING a typical price-to-book multiple of 1.22, then the stock should be about $19. Consider that the stock pays a high 5.4% yield, and there is much to like from a valuation perspective for prospective shareholders.

ING: Attractive Valuation Metrics

{kind=link}

Compared to its peers , ING features a best-in-class valuation rating while its growth figure is also stout, though its near-term outlook is to the dim side. While the firm has a weak profitability rating, that is due to some margin figures not flowing through to the data page – ING recently reported better than 14% return on tangible equity, which is impressive for a stock trading with a low to mid-single-digit P/E. Share-price momentum has improved recently, and I’ll detail key price levels to watch later in the article. Finally, EPS revisions are nothing to weigh too heavily on since there have been just two recently, though the company has topped earnings estimates in the past four quarters.

Competitor Analysis

{kind=link}

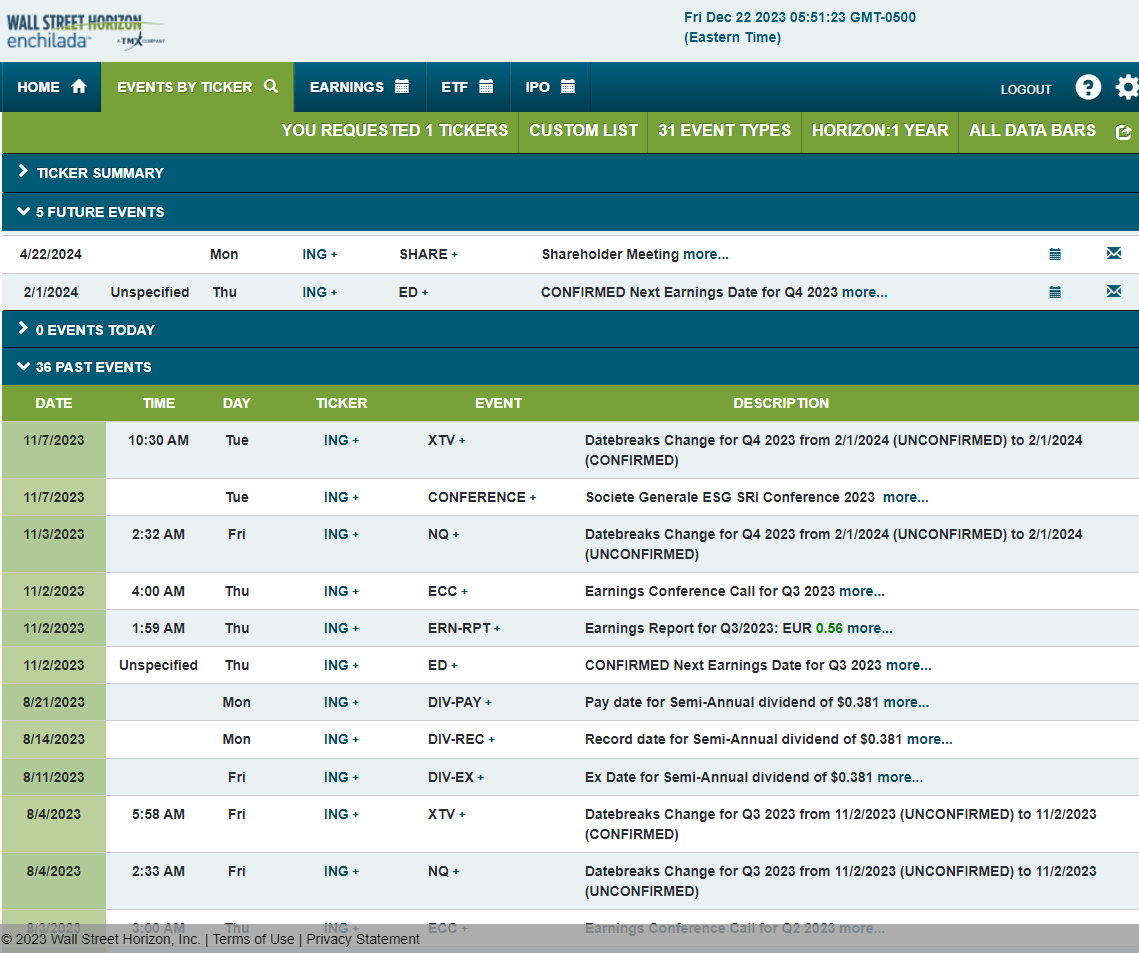

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2023 earnings date of Thursday, February 1. Keep your eye on ING’s annual shareholders’ meeting slated to take place on Monday, April 22, 2024.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

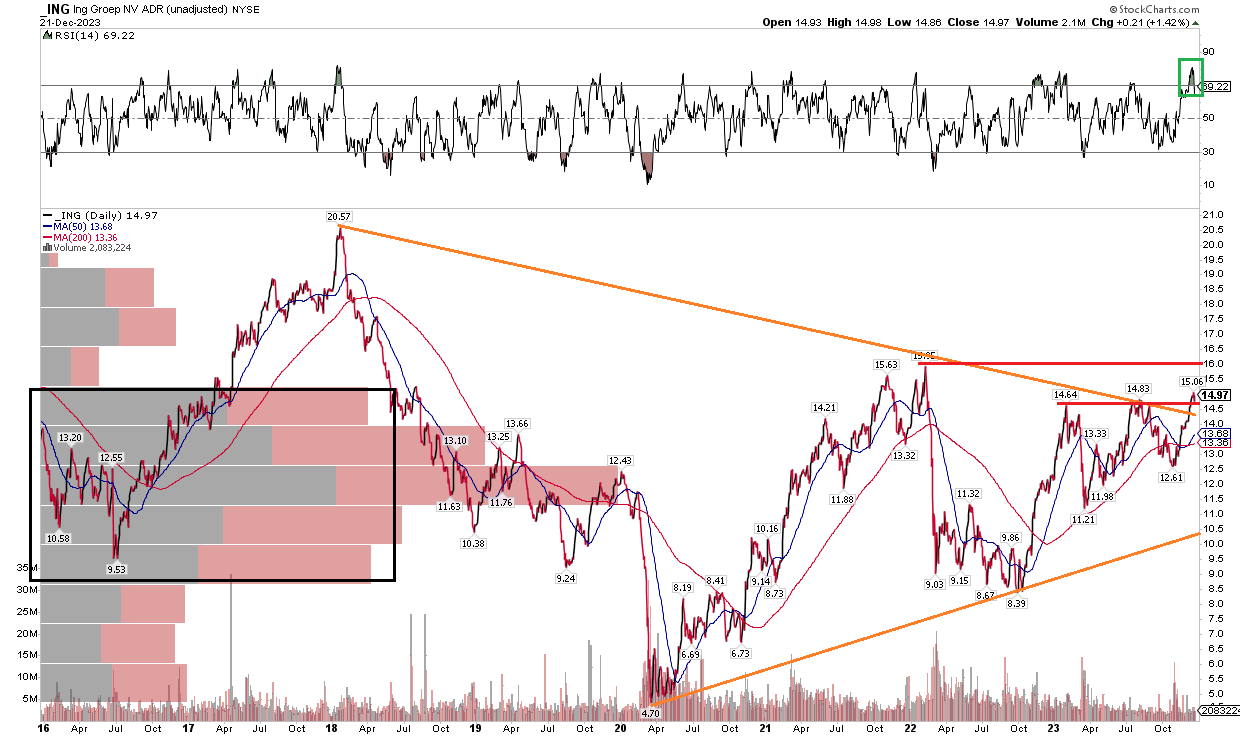

I first reviewed ING in Q4 last year. Shares wobbled, but have turned higher in a significant way over the last two months. Notice in the chart below that ING has also possibly broken out from a years-long consolidation pattern. A symmetrical triangle of lower highs and higher lows was the theme since ING peaked in January 2018 above $20. It went on to notch a March 2020 low under $5 before rebounding to near $16 early last year. With shares now almost having doubled off its Q4 2022 nadir, the bulls might wonder how much is left in the stock.

I assert that a breakout above $16 could help confirm the move out of the consolidation. If so, then a major price target into the upper $20s would be in play. For now, $16 is the first hurdle and the 2018 high is the next resistance. What is encouraging is that there’s a high amount of volume by price from the current price all the way down to $9 – that is a lot of support on pullbacks. There is little overhead supply above $15, too. With a long-term 200-day moving average that is now moving higher and as the RSI momentum oscillator works off overbought conditions, I see upside potential for ING shares. Support is near $12.60.

Overall, I see ING as potentially breaking out, while longer-term and broader technical readings suggest more gains are ahead.

ING: Bullish Breakout Potential, Working Off Overbought Conditions

{kind=link}

The Bottom Line

I reiterate my buy rating on ING. I see the Financials sector stock has significantly undervalued, while the technical situation is encouraging.

For further details see:

ING Groep: A European Dividend Standout, Buying Back Stock