INGVF - ING Groep Is Another Buy Opportunity

2023-06-22 07:29:24 ET

Summary

- ING Groep reported solid profit thanks to net interest income development, lower regulatory costs, and low provisions.

- The bank announced a €1.5 billion buyback, but we are forecasting a higher share repurchase program.

- We see solid progress towards ING's 2025 financial targets. The company is now a buy.

Here at the Lab, we decided to move on with another coverage in the Dutch region. Since 2020, our internal team has provided updates on KBC Group (KBCSF) (KBCSY) (neutral rating target price), and today, we started to analyze ING Groep N.V. ( ING ). Following our macro update on Deutsche Bank Aktiengesellschaft (DB), it is important to recap a few key takeaways on why we support the EU banking sector. Our macro buy case is supported by the following: 1) core inflation, excluding energy and food, which has been revised upwards following the 15 June ECB meeting ; therefore, we expect an additional 25 basis point rate hike in the EU area (in July 2023); 2) European banks' Q1 results were excellent; 3) deposits are stable, and there are no signs of credit stress, 4) capital return is positive, and 5) the EU banking sector valuations are near historical lows, in detail, the tangible book value and RoTE are at 0.7x and 12.5%, respectively.

Following the developments involving the regional banks in the United States, we have long argued that Wall Street is too pessimistic towards European banks. Although the scenario is very optimistic, with rising earnings and subdued valuations, the sector has performed lackluster year-to-date. Nonetheless, we do not believe there will be an impact in Europe, and the outlook for the industry remains positive. An active bottom-up stock selection is critical, and ING Groep N.V. positively scores in almost every ratio. ING is a Dutch financial institution that offers banking services focusing on the Benelux area at B2B and B2C levels.

ING Groep Upside and Changes in Estimates

According to our team, we calculated that every 25 basis points of additional interest rate hikes add, on average, 2.4% to ING's earnings per share. Current funding and liquidity concerns, including the recalibration of the Liquidity Coverage Ratio calculation and the revision of deposit limits, are exaggerated for European banks. Here at the Lab, we expect higher interest margins and, therefore, better earnings which will surprise Wall Street to the upside (thanks also to lower-than-expected betas on deposits). Our internal team usually focuses on national champions bank, and ING is one of them. Thanks to organic capital generation, the ability to hold deposits with a lower beta than competitors, and a supportive asset mix with a solid franchise, ING is well positioned in the event of asset quality deterioration.

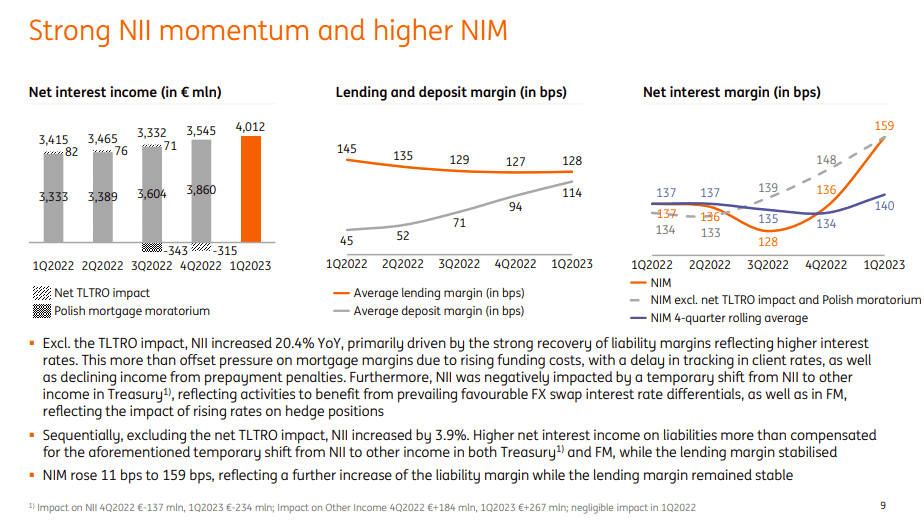

Very briefly, in Q1, the bank delivered a profit of €1.59 billion compared to a consensus estimate of €1.1 billion. Multiple factors drove this 1) a 7% top-line sales beat thanks to higher net interest income (NII - Fig 1), 2) a 1% beat on ING's cost basis, and 3) extremely low provision.

To support our investment thesis, the CEO continues to see positive evolution from higher interest rates while loan demand will deteriorate given the economic uncertainty. Going to our main ratio development, here are our main takeaways:

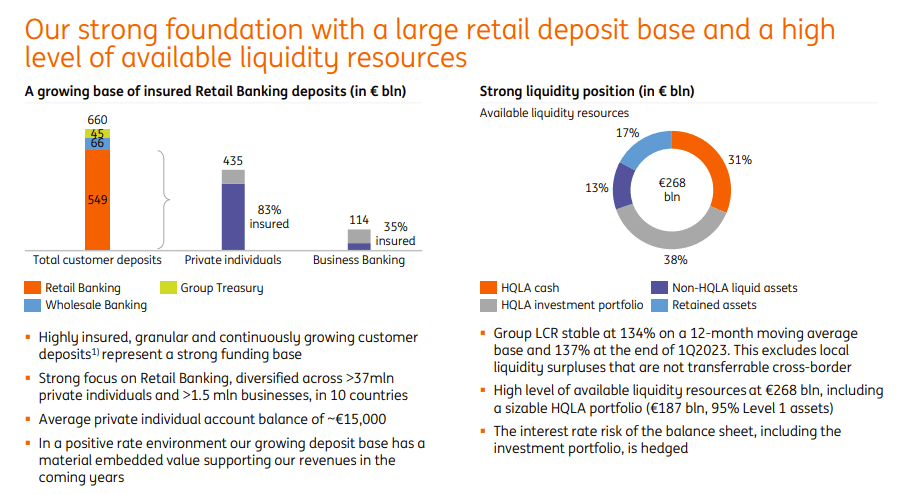

- Deposits are stable, and the liquidity cover ratio is at 134% (in line with EU banks) (Fig 2);

- Opex was slightly higher than anticipated and was negatively impacted by German payments to staff, legal provisions for €27 million, restructuring costs in Benelux for €16 million, and hyperinflation in Turkey for €4 million. Regulatory costs were down; the 58% cost/income ratio achieved is not the 2023 floor. In our estimates, we are forecasting a cost/income ratio at 55% for 2023, mainly thanks to lower regulatory costs;

- Provisions reached only €152 million (equal to 9 basis points). In our estimates, we are forecasting 25 basis points. ING's Russian exposure still stands at €2.3 billion;

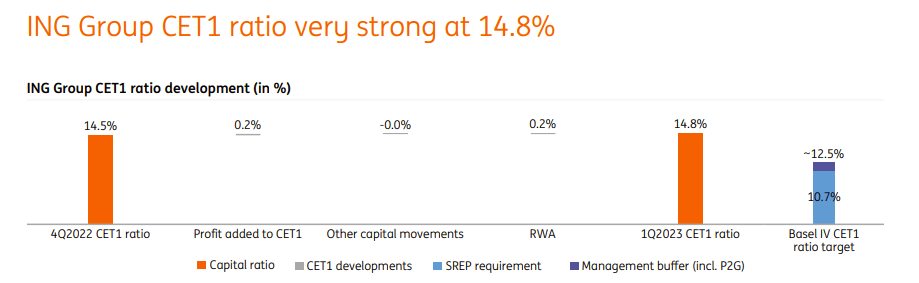

- The CET1 ratio reached 14.8% and was up 0.3% on a quarterly basis, beating consensus estimates at 14.5% (Fig 4);

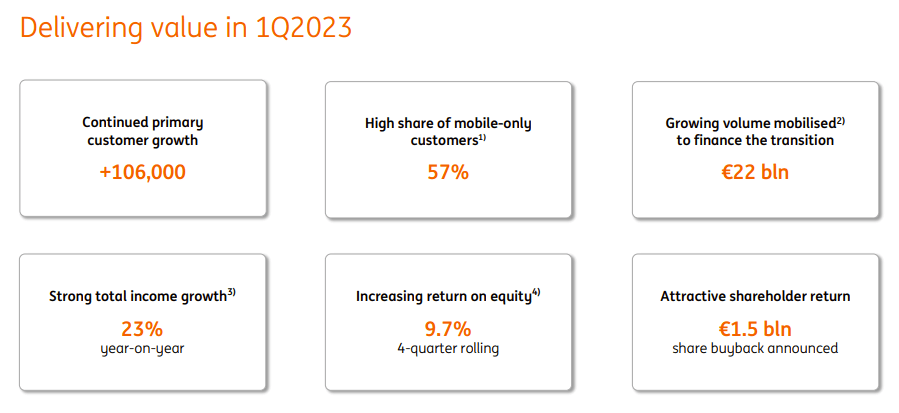

- The bank announced a €1.5 billion share buyback program in mid-May that should be completed by 2023 Q3 (Fig 3). Here at the Lab, we are forecasting a buyback for €2.5 billion this year, which aligns with ING's latest comment.

{kind=link}

Fig 1

{kind=link}

Fig 2

{kind=link}

Fig 3

{kind=link}

Fig 4

Conclusion and Valuation

Looking at the 2023 level, we believe that net interest income might reach €16.8 billion, and we are also forecasting an NII at €17 billion for 2024 (for both years, we are above consensus estimates). For this reason, we raise earnings per share estimates by 15% and 5% in 2023 and 2024, respectively, and our target price is set at €16 per share, confirming a clear buy rating. At this price, ING will trade at a 0.8x tangible book value with a RoTE of 13% and align with the current EU banking environment. Risks to our target price include interest rate development, higher risk costs, Russia/Ukraine exposure, inferior asset quality, and lower shareholders' remuneration.

For further details see:

ING Groep Is Another Buy Opportunity