ING - ING Groep: Solid Main Street Bank Trading At A 7.1% Dividend Yield

2023-03-30 11:12:11 ET

Summary

- ING Groep, a leading Dutch Main Street bank, experienced a significant sell-off following the U.S. banking turmoil.

- The Dutch banking system is highly concentrated, with only three major players.

- Eurozone banks have been slow to pass on higher interest rates, and ING's return on equity has been strong at 22%.

- The bank aims to achieve a 12.5% return on equity by 2025, which could lead to a re-rate and 28% upside outside of the dividend.

Shortly after the U.S. banking turmoil emerged, European bank shares experienced a big decline. This culminated in UBS ( UBS ) begrudgingly taking over Credit Suisse ( CS ). Deutsche Bank ( DB ) came under a lot of pressure as well. I've written more about that situation here . In this article, I wanted to highlight a relatively solid bank that I believe sold off alongside the industry. However, I think this readjustment by the market could be premature.

ING Groep ( ING ) is a leading Dutch Main Street bank. Dutch banking is one of the juiciest banking environments in Europe. The leading three banks hold 90% of all checking accounts. Most of the Eurozone, and specifically Germany, has a more dispersed banking system. The German system is more akin to the U.S. banking landscape. ING has a dominant position and has 40% of all checking accounts. The bank is also active outside of the Netherlands but lacks a dominant presence in those markets.

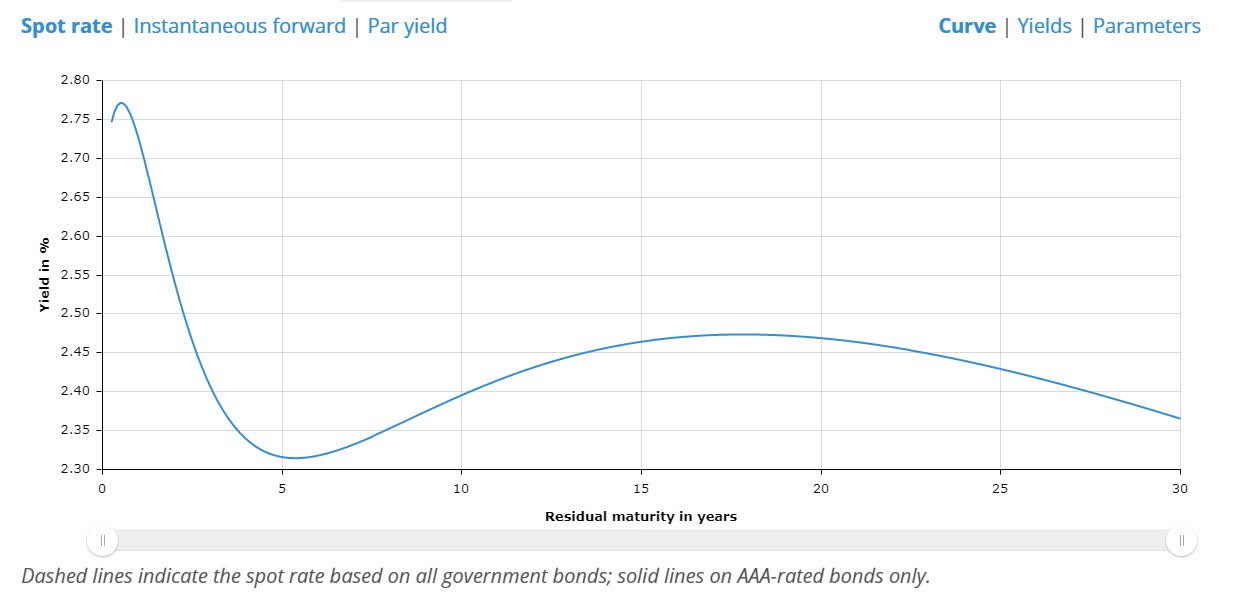

The ECB hiking rates benefitted ING and caused investors to start re-rating the shares until the recent crisis. I'll touch on this later, but ING has an unusually high share of checking accounts, it is just offering only 0.5% even on savings accounts. Its main competitors are doing the same thing. The yield curve is admittedly inverted in the Euro area:

{kind=link}

This tends to be challenging for banks, but consumers are so used to low-interest rate environments that there is not a lot of competitive pressure to offer rates commensurate with the short end. Taking deposits at 0.5% and investing them at the short end is the best type of business a bank will ever get.

Inverted yield curves in both the U.S. and Europe are likely to cause a recession in my opinion. If there is little apparent upside to investing money for the long term, it should over time lead to the investment being curtailed across the continents, which of course increases the likelihood of a recession. As the curves stay inverted longer and longer, this becomes increasingly likely (as per Central Bank's intention to cool off rates).

Meanwhile, the banking crisis's immediate effects have been dealt with. I don't see any evidence of much further contagion, although the failure of a large, well-known bank could easily lead to contagion effects accelerating again. A key concern for U.S. and European banking investors is whether the banking crisis has spurred depositors to look for safer places to park money that offer higher yields. I don't think this is happening in the Eurozone to the extent it is taking place in the U.S. In Europe, money market-type funds are generally less readily available, and the banking crisis isn't a hot topic outside of financial circles. I don't get a lot of questions about it, and few people seem concerned.

Over the past five months, customers moved €214 billion out of eurozone banks, with record outflows in February, as the European Central Bank reported . This downturn in deposits started after the ECB began raising interest rates last summer, and contrasts with the surge of money that flowed into banks during the pandemic. The trend seems to have started before the recent banking crises.

I can understand it if corporate depositors and high-net-worth individuals are alarmed, as the Eurozone hasn't implicitly guaranteed deposits like what happened in the U.S. with Silicon Valley Bank (SVB) ( SIVBQ ). Meanwhile, Eurozone banks have been slow to pass on higher interest. The ECB raised its deposit rate to 3% this month, but interest rates for depositors continue to fall far short of that rate.

In fact, on checking accounts, banks generally pay nothing and charge fees, while large banks like ING, ABN AMRO ( AAVMY ), and Rabobank offer only 0.50% on designated savings accounts .

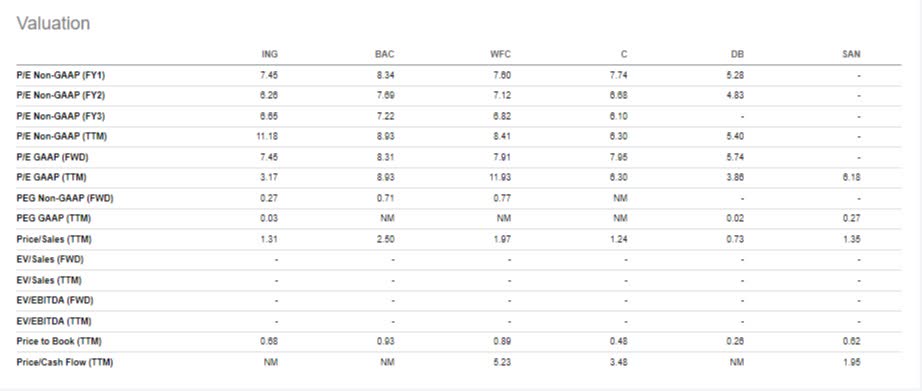

I've pulled up the valuations of several different banks. I included three well-known Main Street U.S. banks because readers know these entities. In general, valuations in Europe are a bit lower on banks as they are more regulatory-constrained, and it is more challenging to achieve the RoE that U.S. banks achieve.

Recently ING's return on equity has been exceptionally strong (22%), but over the past five years, it achieved around 7.70%. With that kind of return on equity, a bank should trade at a discount to book value, or shareholders don't see long-term returns commensurate with the risks associated with banking.

ING trades at 0.7x book value, which is a very large discount given its strong competitive position in its core market. Banks like Citigroup and Deutsche Bank trade at lower multiples to book, but these are typically not considered the best banks. ING also trades at the lower end of the forward P/E multiples.

Bank valuations U.S. and Europe (Seeking Alpha)

{kind=link}

No bank is ultimately completely safe from mass deposit withdrawals. I'd argue this type of bank is least vulnerable to the types of bank runs we've seen at Silicon Valley Bank and others.

The bank also has a very solid CET1 ratio of 14.5% (about average for the Euro area ), which it intends to bring down towards 12.5% over time. The CET1 ratio is a measure of a bank's financial strength and capital adequacy. It divides risk-weighted assets ((RWA)) by core capital. The regulatory minimum imposed on ING is 10.5%.

Of course, ING is exposed to interest-rate risk. It tends to get easier to capture a spread between bank funding and investments as interest rates rise. At the same time, as we're seeing right now, rapidly rising interest rates can cause pain on the asset side. ING has a lot of exposure to fixed-rate mortgages. However, banks tend to focus on 10-year mortgages. Very long-term mortgages are more likely to be issued and held by insurance companies.

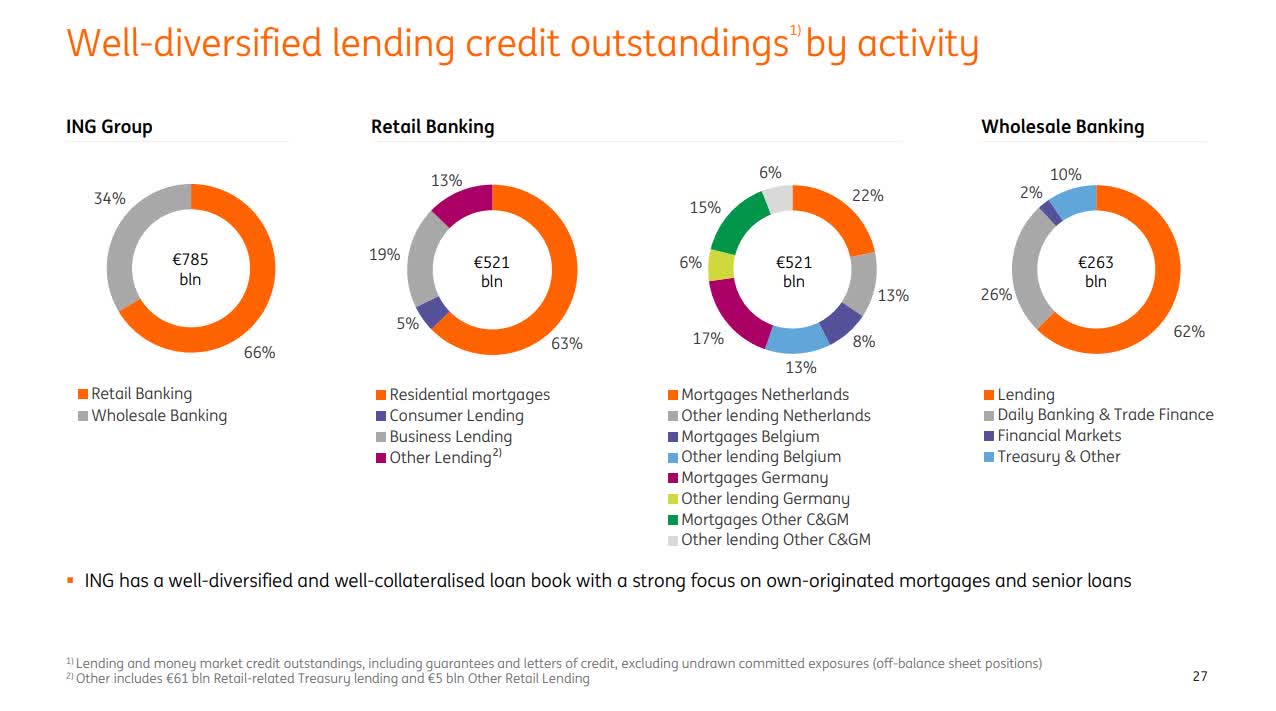

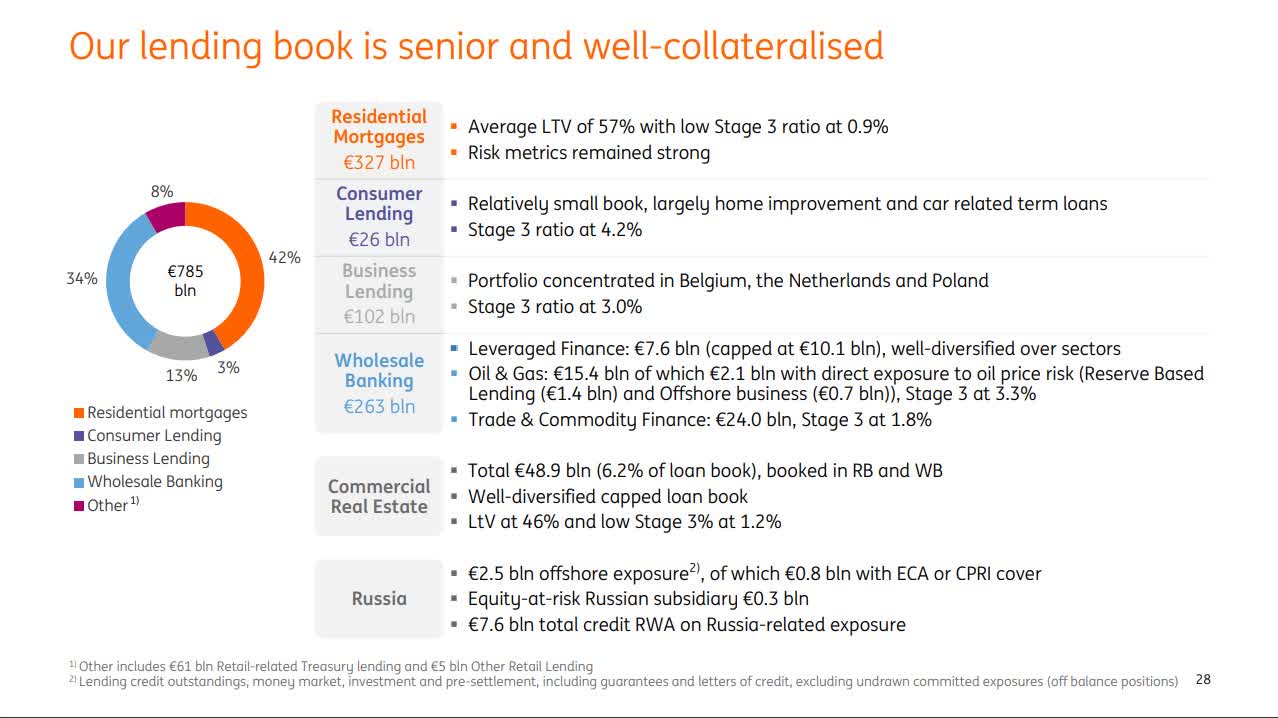

Here are two slides giving a high-level overview of the bank's lending profile:

ING credit positions (ING)

{kind=link}

ING lending book (ING)

{kind=link}

The bank holds a large number of mortgages. It is typically encouraged by banks to take out a mortgage that's covered by the Dutch National Mortgage Guarantee ((NHG)). This NHG provides insurance up to €405,000.

Mortgages and specifically Dutch mortgages make up a significant portion of ING's lending book. There is therefore some concentration risk to a downturn in the Dutch property market, although the government-backed guarantee of smaller mortgages does shield a meaningful portion of ING's mortgage book from credit risk. The insurance starts covering mortgage payments if the homeowner is no longer able to do so. For example, after remaining unemployed for a long time after losing a job. First, unemployment benefits kick in, which are relatively long periods (by U.S. standards) of cheques from the government after losing employment.

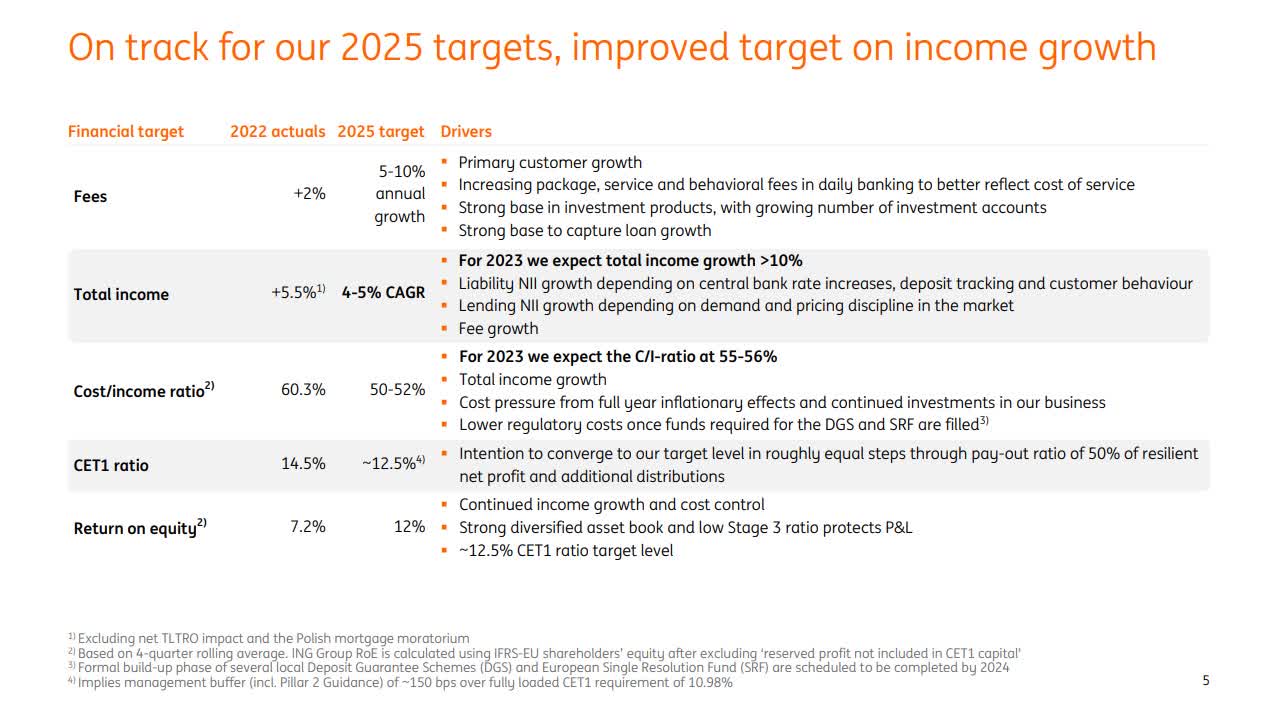

Meanwhile, the bank is ambitious to achieve 12% return on equity by 2025, and if it gets there sustainably, it should trade at a slight premium to book value.

ING 2025 targets (ING)

{kind=link}

I have doubts about whether ING can sustain that kind of return. However, if it falls short, it could still be fair to trade at or close to book value. If ING would trade at 0.9x book value in the future, there's a 28% upside from here. Meanwhile, at the current share price, the forward yield is 7.1% which is quite attractive in its own right. A yield that appears to be highly sustainable given the bank is so well capitalized and current profitability. Banks can always proactively choose to cut their dividend to strengthen their capital base, but the opposite scenario (rising shareholder returns) seems more likely.

For further details see:

ING Groep: Solid Main Street Bank Trading At A 7.1% Dividend Yield