ACI - Ingles Markets Still Has Room To Run

Summary

- Ingles Markets has been a solid play relative to the broader market, with sales and cash flows increasing.

- Profits have struggled a bit, but the overall health of the company looks to be intact.

- Add on top of this how cheap shares are, and the picture for investors looks great moving forward.

One of my favorite companies to write about, even though I don't own shares in it, is retail play Ingles Markets ( IMKTA ). This firm is a fairly small retailer with a market capitalization of only $1.85 billion and operations spread across only a few states. Because of its size, investors often overlook the company when evaluating potential opportunities. But following this approach has resulted in significant opportunity costs for those who are guilty. Driven by attractive revenue growth and generally improving bottom line results, combined with how cheap shares have been, the stock for the enterprise has performed quite well in recent months. Add on top of this how cheap shares still are and further upside seems to still exist for those who are patient enough to wait out market volatility.

A great play in retail

The last article I wrote about Ingles Markets was published in October of 2022. At the time, I was marveling at how well the company was performing compared to the broader market while also stating that shares seemed to offer even more upside for buyers. My enthusiasm around the company related not only to the company's revenue growth, but also to its cash flow data and how cheap shares were. All of this data coalesced into a reiteration of the ‘strong buy’ rating I had assigned to the company previously, a rating that reflected my view that shares should drastically outperform the broader market for the foreseeable future. Given the short amount of time that has passed since the publication of that article, I would say that the company has definitely delivered. While the S&P 500 is up 2.3%, shares of Ingles Markets have seen upside of 5.8%. This follows a trend of outperformance for the company. After all, since I first wrote about the firm in January of 2022, shares have generated upside for investors of 22.3% compared to the 15.1% drop experienced by the broader market.

{kind=link}

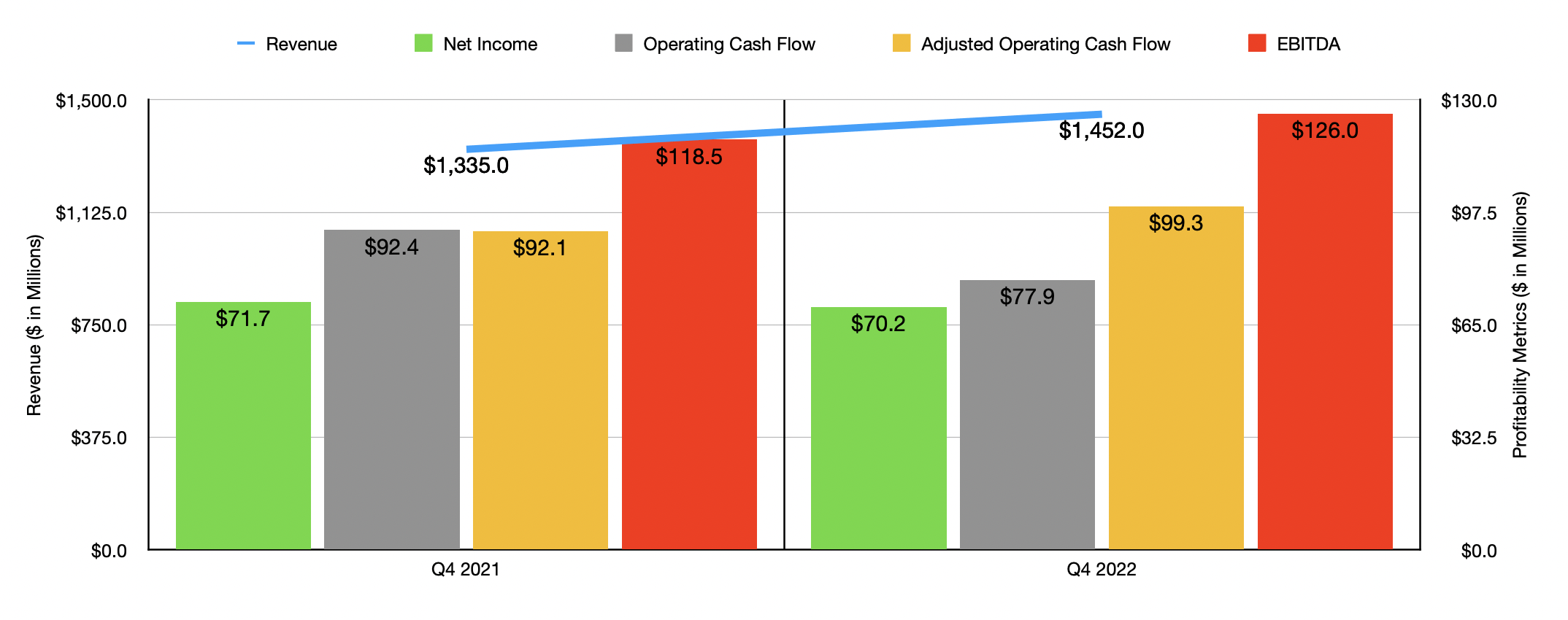

This return disparity really boils down to fundamental performance and share price. On the fundamental side, we do have data from the fourth quarter of 2022 to take into consideration. This is the only quarter for which new data is available that was not available when I last wrote about the business. Sales during that time came in at $1.45 billion. That represents an increase of 8.8% over the $1.34 billion the company generated the same time one year earlier. According to management, excluding the impact caused by gasoline sales, comparable store sales grew by 5.2% year over year. This was the leading driver behind the company's growth during that time.

On the bottom line, things were somewhat mixed. Net income, for instance, dropped from $71.7 million down to $70.2 million. Although revenue increased, the company's gross profit margin suffered, dropping from 25.6% of sales down to 25.1%. This decline may not seem like much, but when applied to the revenue achieved in the final quarter of last year, it would have translated to $7.3 million of additional bottom line results had margins remained flat year-over-year. Operating cash flow fared even worse, falling from $92.4 million to $77.9 million. But if we adjust for changes in working capital, it would have risen from $92.1 million to $99.9 million. And over that same window of time, EBITDA for the company also expanded, climbing from $118.5 million to $126 million.

{kind=link}

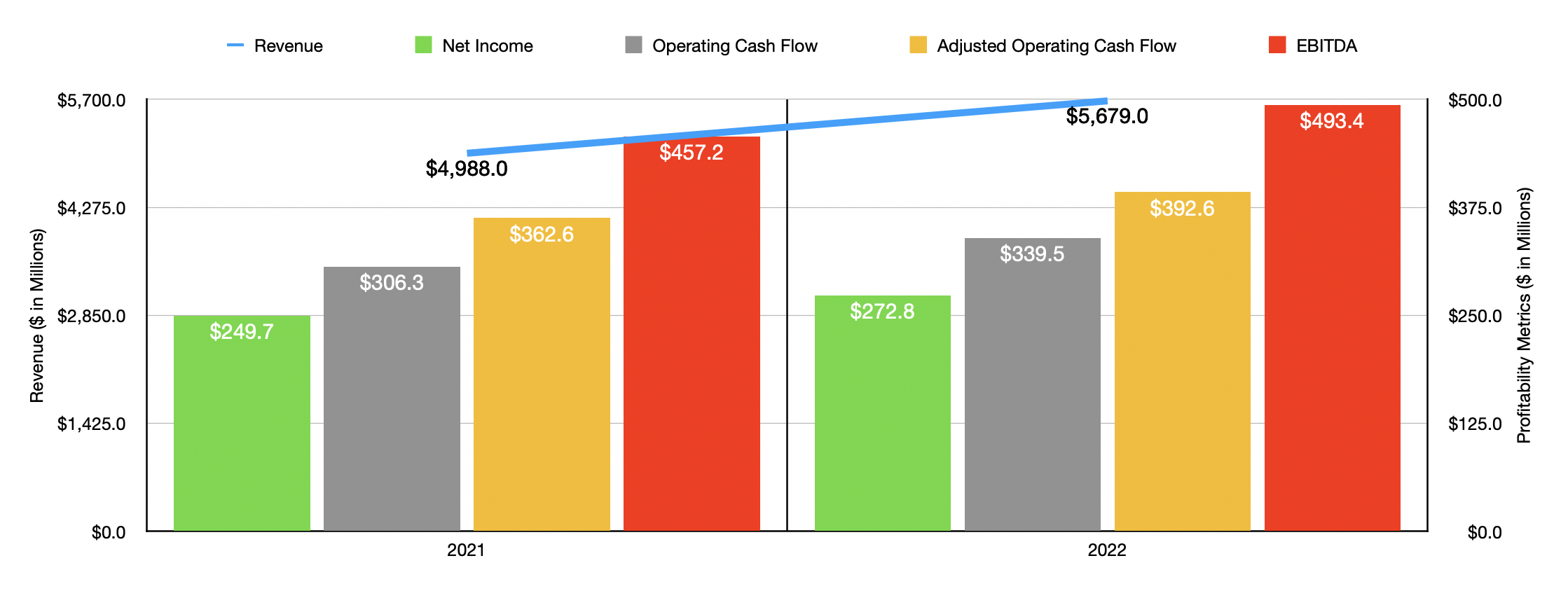

Thanks to the fairly robust financial results achieved in the final quarter, results for 2022 as a whole were quite positive. Sales for the year came in at $5.68 billion. That's 13.9% higher than the $4.99 billion reported for 2021. On the retail side of things, the largest increase came from comparable store sales growth, with revenue there shooting up $623.7 million year over year. New stores that were opened in 2021, net of those that were closed, contributed another $18.8 million to the company's top line. On the bottom line, things were quite impressive as well. Net income of $272.8 million beat out the $249.7 million reported one year earlier. Operating cash flow went from $306.3 million to $339.5 million. If we adjust for changes in working capital, it would have risen from $392.6 million to $362.6 million. And over that same window of time, EBITDA rose from $457.2 million to $493.4 million.

{kind=link}

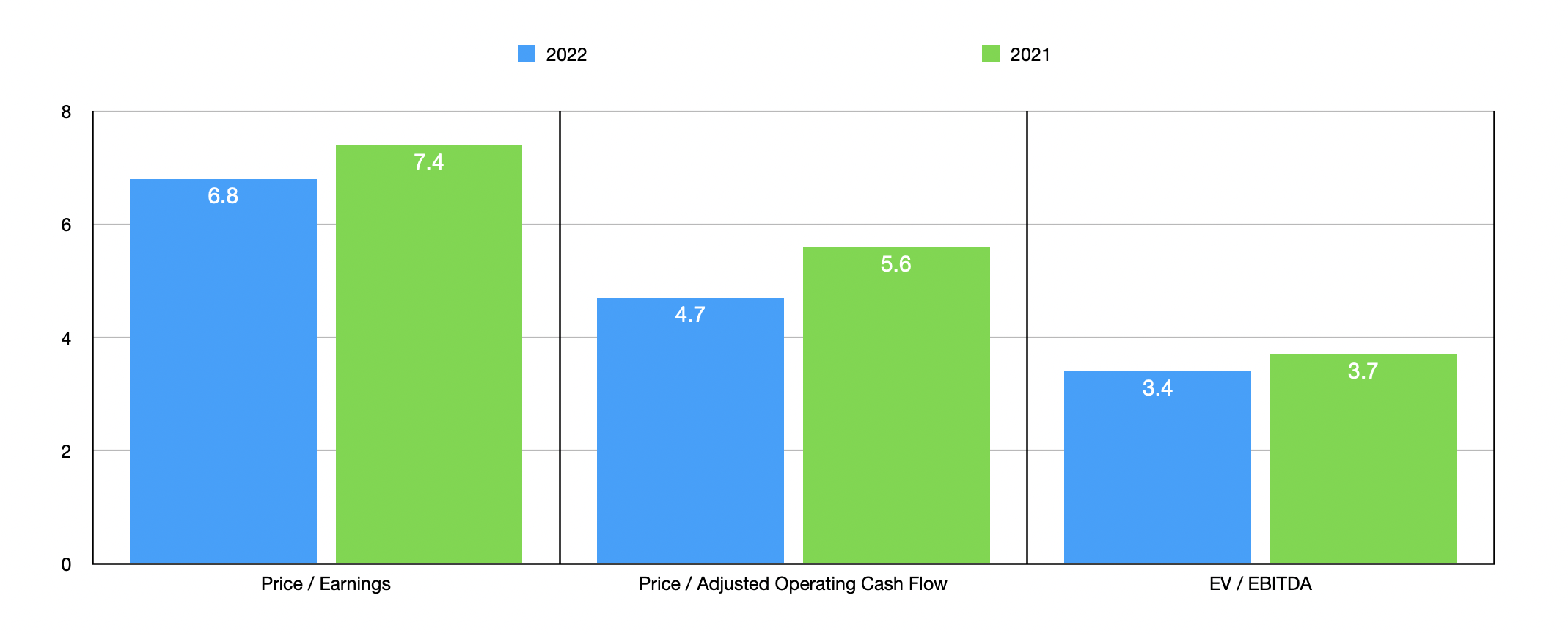

Using the data that management provided for 2022, I calculated that the company is trading at a price-to-earnings multiple of 6.8. This compares to the 7.4 reading that we get using data from 2021. The price to adjusted operating cash flow multiple should drop from 5.1 using data from 2021 to 4.7 using data from last year. Meanwhile, the EV to EBITDA multiple, driven by the company having cash in excess of debt in the amount of $176 million, comes in at only 3.4 compared to the 3.7 reading that we would get using data from one year prior. As part of my analysis, I also compared the company to five similar enterprises. On a price-to-earnings basis, these companies ranged from a low of 7 to a high of 51.6. In this case, Ingles Markets was the cheapest of the group. Using the price to operating cash flow approach, the range was from 3.8 to 17.6. And when it comes to the EV to EBITDA approach, the range was from 3.1 to 18.6. In both of these cases, only one of the five companies was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Ingles Markets |

| 6.8 |

| 4.7 |

| 3.4 |

| Grocery Outlet Holding Corp. ( GO ) |

| 51.6 |

| 17.6 |

| 18.6 |

| Natural Grocers by Vitamin Cottage ( NGVC ) |

| 10.3 |

| 5.5 |

| 3.7 |

| Casey's General Stores ( CASY ) |

| 20.0 |

| 10.1 |

| 20.4 |

| Sprouts Farmers Market ( SFM ) |

| 13.9 |

| 9.4 |

| 5.4 |

| Albertsons Companies ( ACI ) |

| 7.0 |

| 3.8 |

| 3.1 |

Takeaway

Even though I don't consider myself a fan of the retail space, I always enjoy looking at Ingles Markets. The company continues to grow at a nice pace. On top of this, bottom line results are mostly positive and shares look incredibly cheap on an absolute basis and relative to similar firms. I don't see anything besides broader economic concerns that could negatively impact the company in the near term. And I would make the case that shares deserve to be trading far higher than what they are trading for now. Because of all of this, I have no problem keeping it at the ‘strong buy’ rating that I had it at previously.

For further details see:

Ingles Markets Still Has Room To Run