INGR - Ingredion: Earnings Growth Slowing Down

2024-01-17 02:56:16 ET

Summary

- Ingredion is a global producer of sweeteners, starches, and other specialty food ingredients.

- INGR's stock has performed well in 2023, as earnings estimates grew at a 20%+ rate, driving the shares higher.

- However, with earnings growth expected to moderate in the coming quarters, the risk/reward is more balanced.

My my, time does fly. It has been over a year since I last wrote about Ingredion Inc. ( INGR ) in November 2022. At the time, I rated Ingredion a buy, as the stock was trading at a discount to peer Consumer Staples companies, while management was implementing a turnaround plan to reignite sales growth through specialty ingredients.

Since my article, INGR has performed well, delivering 22% in total returns, and keeping pace with the S&P 500 Index (Figure 1). This was no easy feat, as the markets had been driven higher by technology megacaps like Apple and Microsoft.

Figure 1 - INGR shares have performed well (Seeking Alpha)

As we begin 2024, let us review Ingredion's operational performance so far in 2023 and whether the stock still deserves a buy at this time.

Brief Company Overview

Ingredion is a leading global producer of sweeteners, starches, and specialty ingredients. Historically, commodity sweeteners like high fructose corn syrup ("HFCS") made up 1/3 of the company's sales while starches contributed 45%, with other co-products like refined corn oil and corn meal making up the rest.

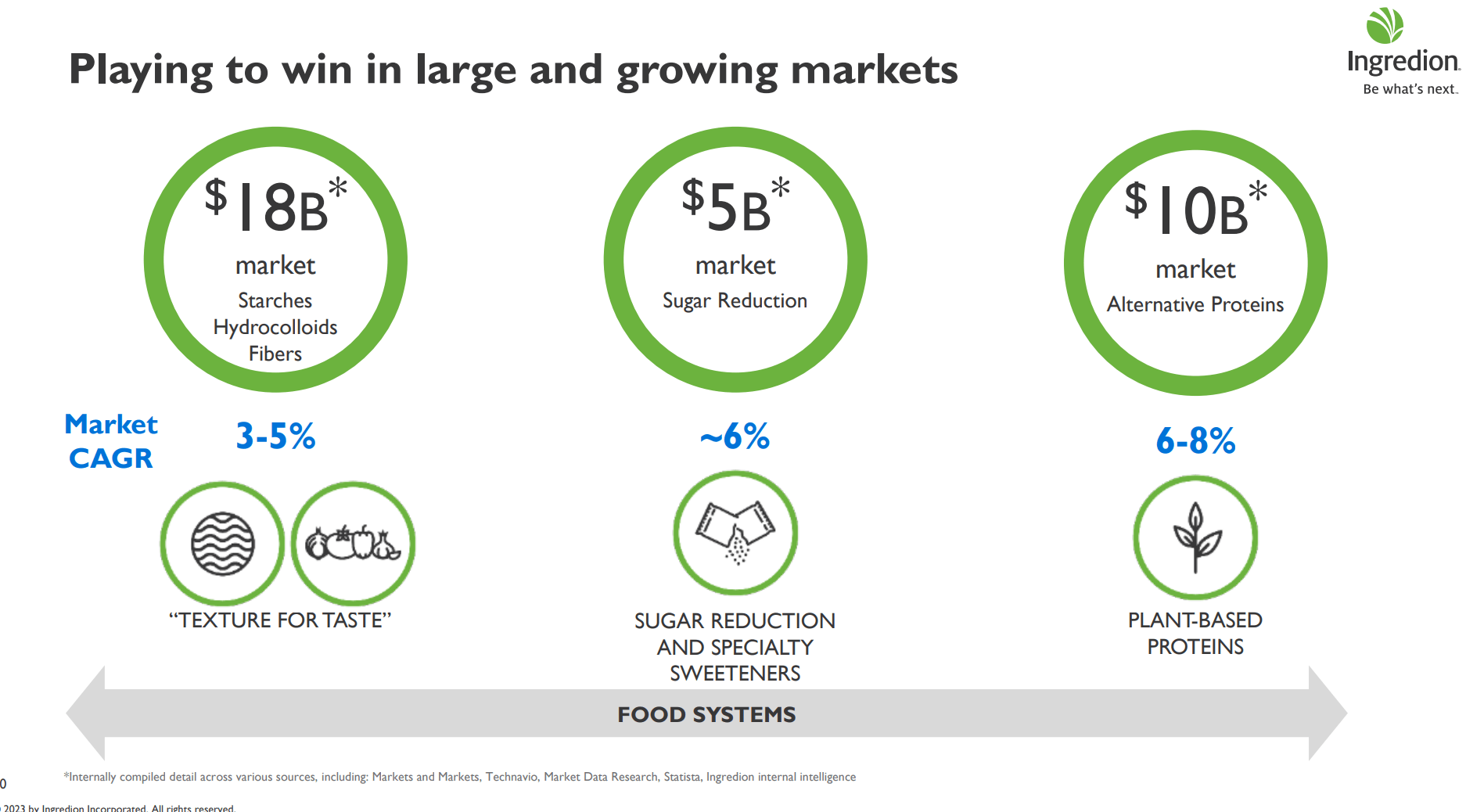

In recent years, Ingredion has been investing heavily in specialty ingredients like sugar-reduced sweeteners and plant-based proteins in order to reignite topline growth (Figure 2).

Figure 2 - Ingredion has been investing in specialty ingredients to spur growth (INGR investor presentation)

{kind=link}

Reached 2025 Goal 3 Years Early

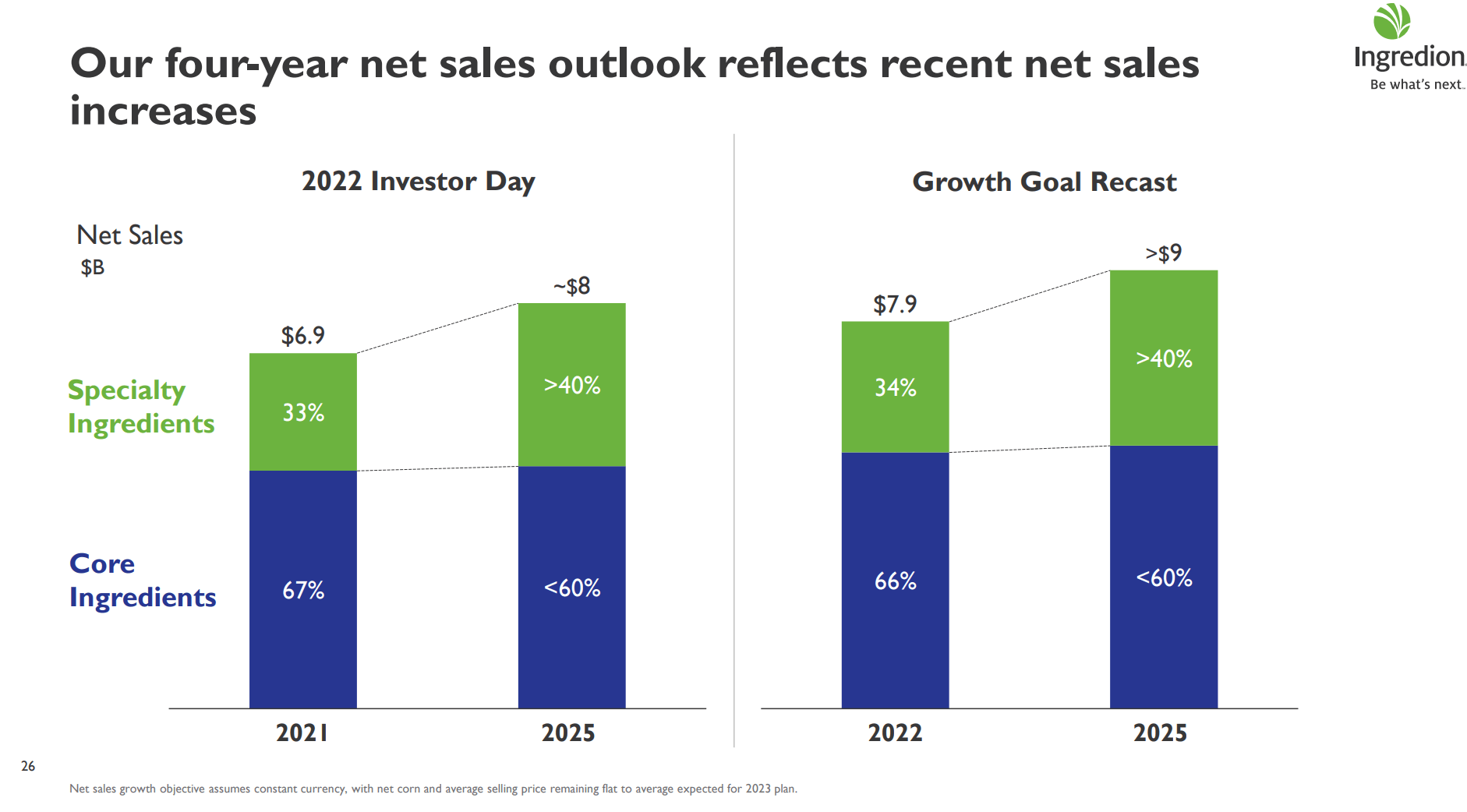

In my last article, I noted that Ingredion's strategic plan was to reach $8 billion in revenues by 2025 with specialty ingredients contributing over 40% of net sales and operating margins of 11-12% (Figure 3).

Figure 3 - INGR 3-year plan from 2022 (INGR investor presentation)

Due to commodity price inflation, Ingredion was actually able to reach its ~$8 billion topline sales goal 3 years early, with $7.9 billion in sales in 2022 (Figure 4). Management therefore bumped the company's growth goals to over $9 billion in revenues by 2025, with the same goal of generating over 40% of revenues from specialty ingredients.

Figure 4 - Growth plans bumped up following strong 2022 performance (INGR investor presentation)

{kind=link}

2023 On Track To Reach Management Goals

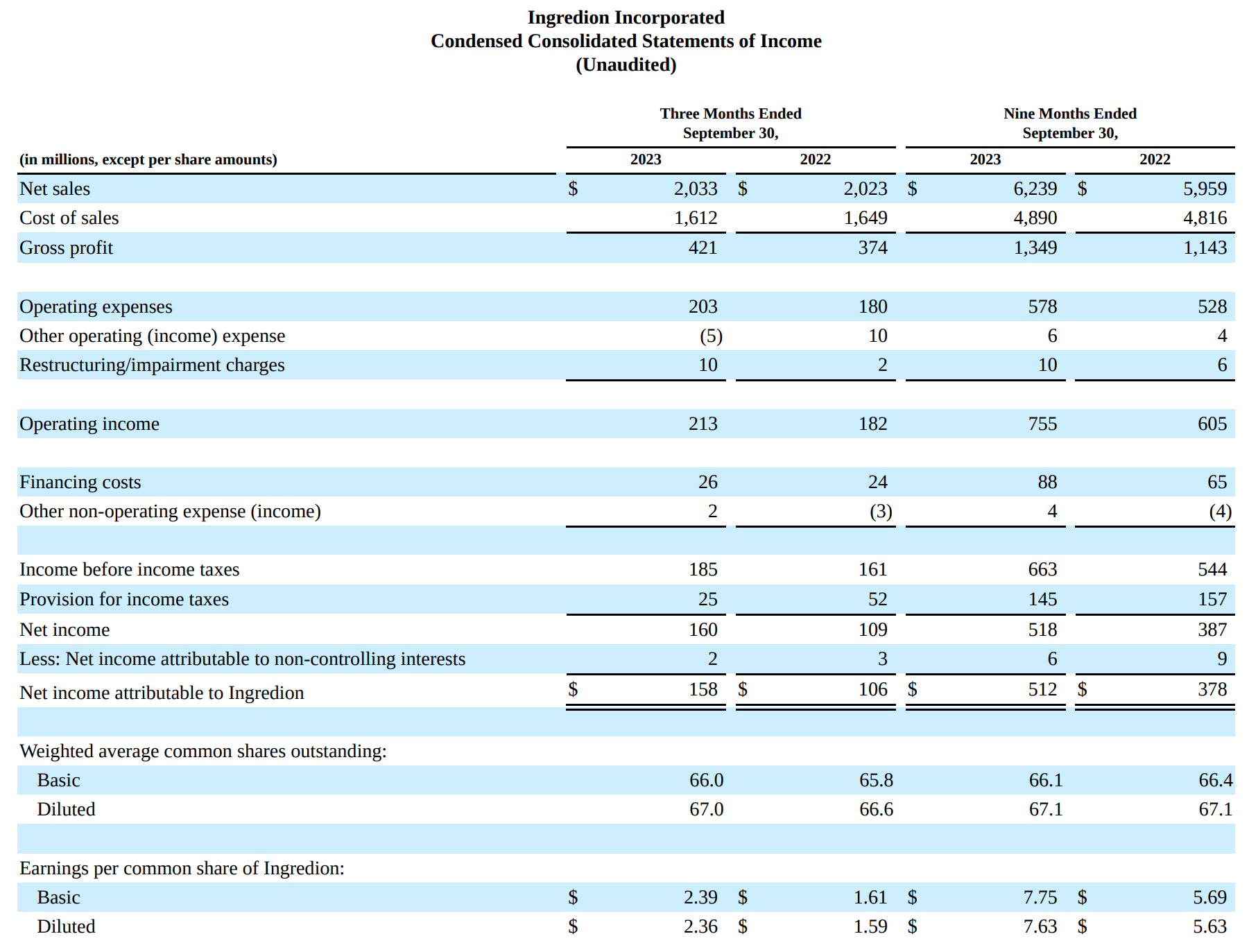

So far, Ingredion's 2023 results appear to be developing according to management's plan, with YTD revenues of $6.2 billion (+4.7% YoY) and operating income of $755 million (+24.8% YoY) (Figure 5). Operating margin was 12.1%, surpassing management's 2025 goal of 11-12%.

Figure 5 - INGR's strong momentum continued in 2023 (INGR Q3/2023 10Q report)

{kind=link}

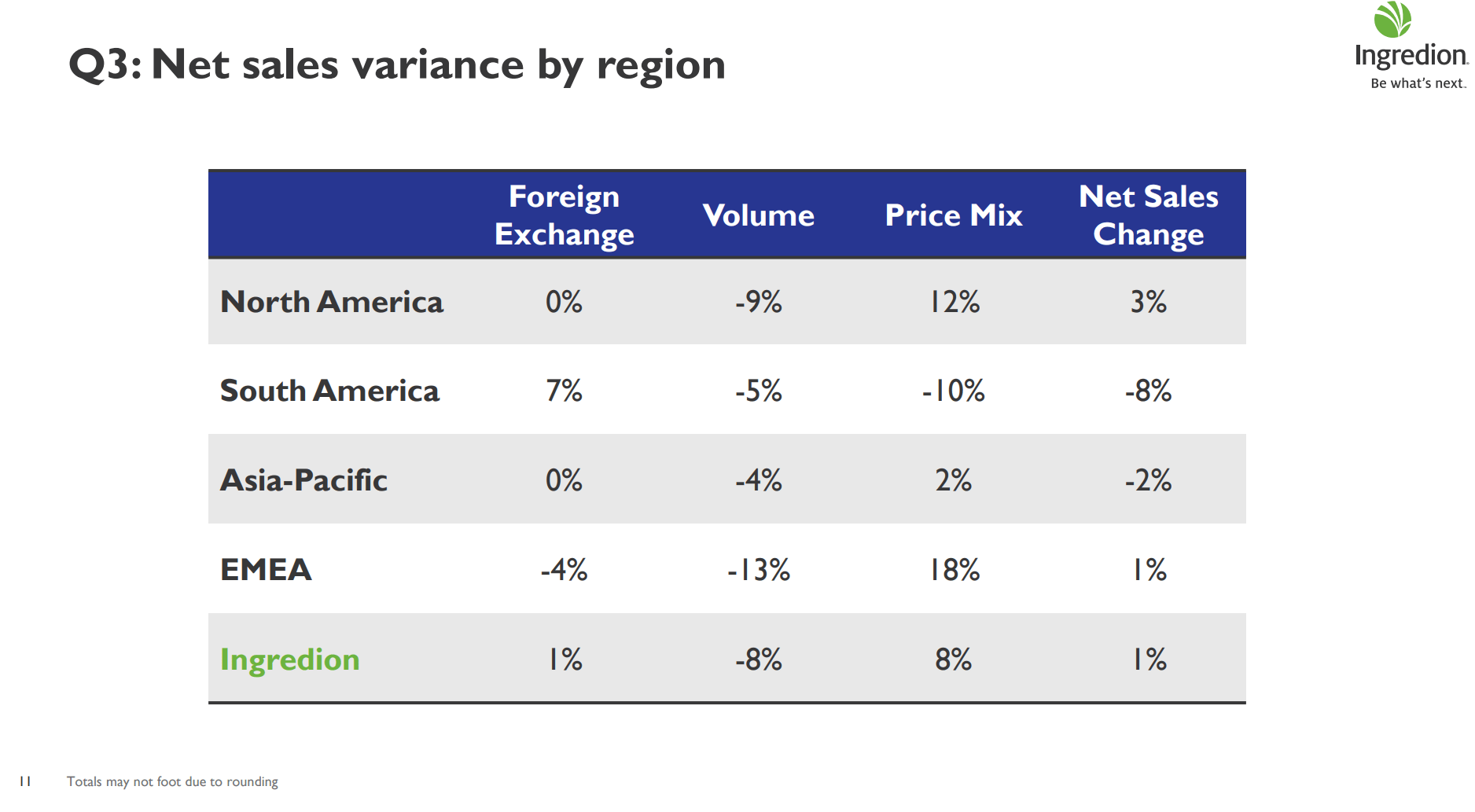

INGR Q3/2023 revenues benefited from improved pricing and customer mix. However, volumes detracted from sales, with volume declines especially pronounced in North America and EMEA (Figure 6). Net/net, INGR's revenues grew 1% YoY in Q3/2023.

Figure 6 - Price/volume trade-off accelerating (INGR investor presentation)

{kind=link}

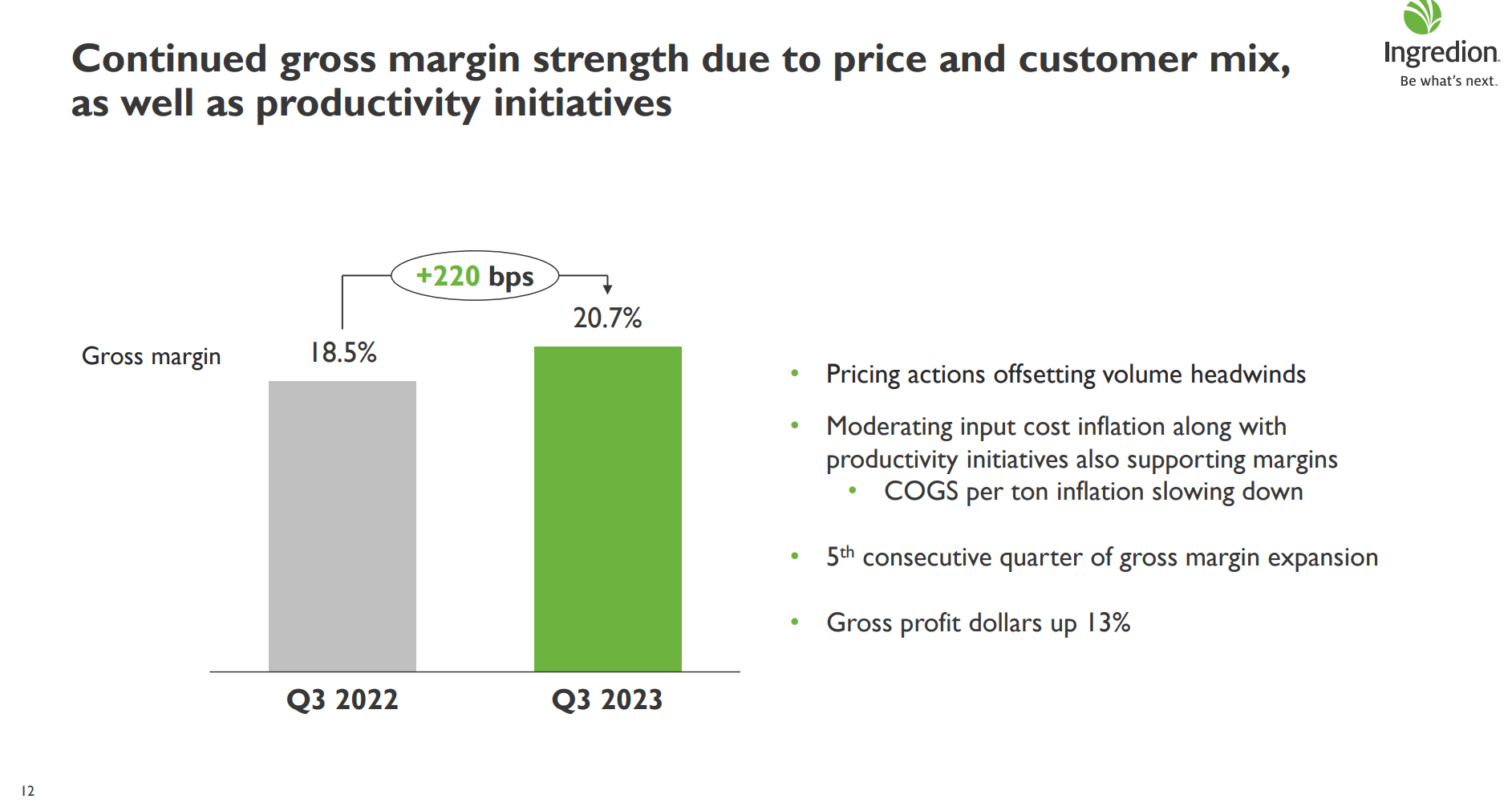

While continued volume declines are concerning, INGR was able to manage margins well, with gross margins improving for a fifth consecutive quarter as pricing actions more than offset volume declines and cost inflation moderated (Figure 7).

Figure 7 - INGR was able to manage margins well (INGR investor presentation)

{kind=link}

Valuation Cheaper Than In 2022

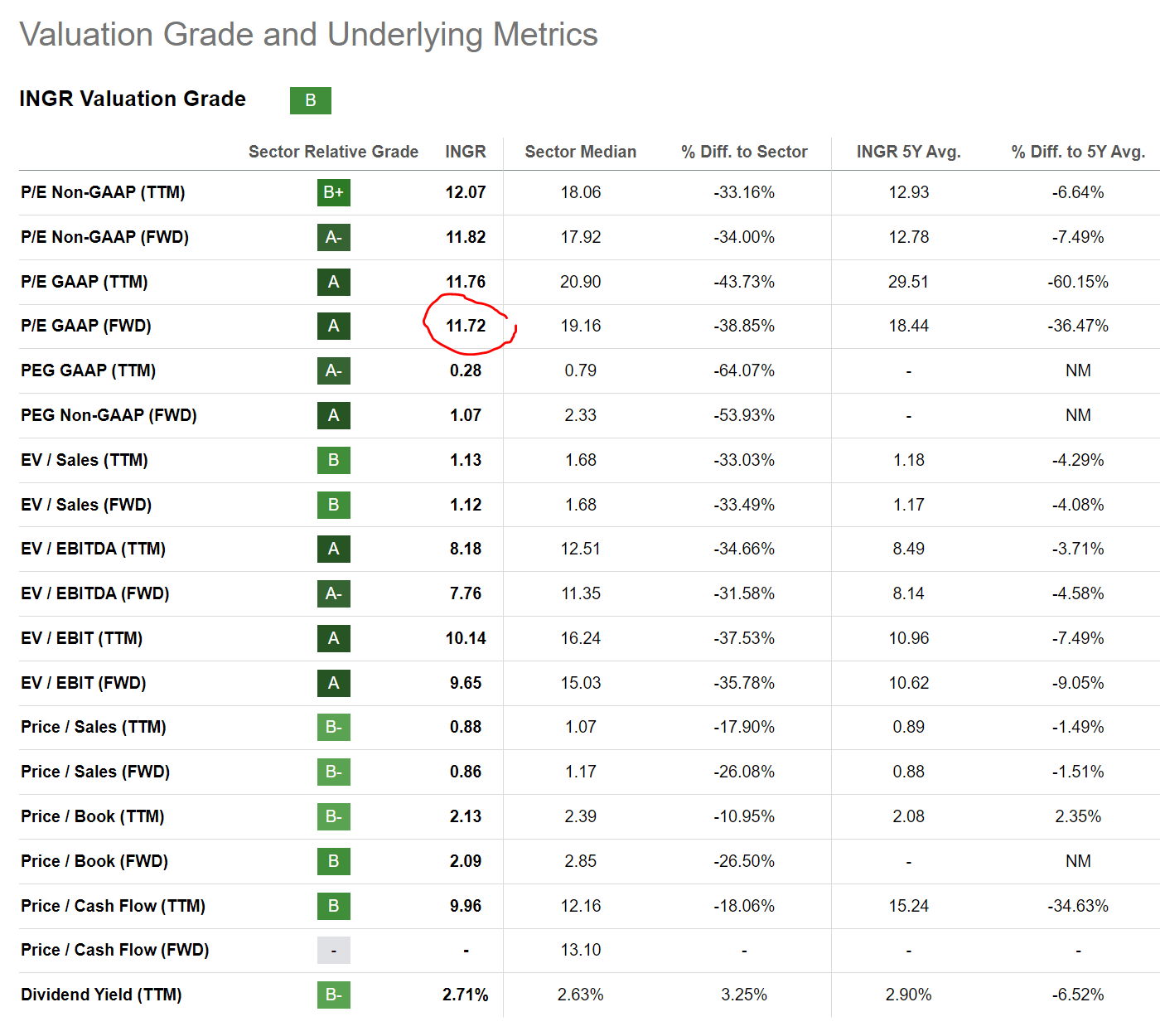

In my prior article, I found INGR's valuation compelling, as the company was only trading at 13.0x 2022E P/E compared to the sector at 18.8x. Despite the stock rallying by almost 20% since November 2022, INGR's valuation has actually gotten cheaper, with the company currently trading at 11.7x Fwd P/E compared to the sector median at 19.2x (Figure 8).

Figure 8 - INGR's valuation got cheaper despite stock rally (Seeking Alpha)

{kind=link}

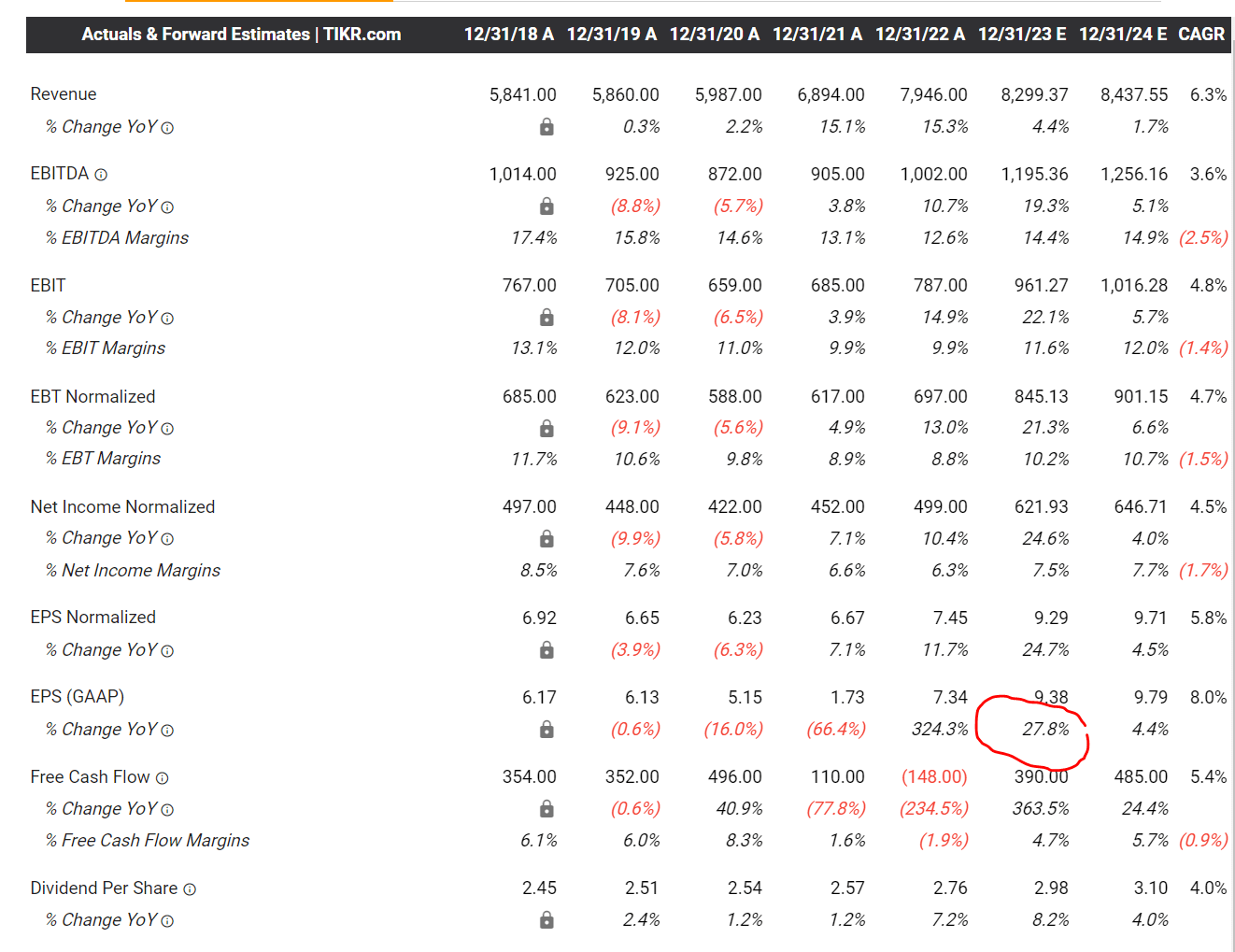

This is because the company has done a phenomenal job of improving margins and delivering earnings growth, with forward earnings estimates growing faster than its stock price (Figure 9).

Figure 9 - INGR was able to achieve this feat by improving earnings faster than the stock price (tikr.com)

{kind=link}

However, looking forward, earnings growth is expected to slow down in 2024 to a mid-single-digit ("MSD") rate. The implication is that INGR's stock appreciation may also slowdown in the coming quarters.

Risks To Ingredion

While Ingredion's shares continue to look cheap, I believe the biggest risk to INGR shares is the limits to the price/volume tradeoff. To date, Ingredion has been able to offset volume declines with price action and customer mix, allowing topline revenues to continue growing modestly. However, with volume declines now a steep 8% overall YoY in the latest quarter, I fear we may be nearing the limits of what consumers are willing to bear in terms of price increases.

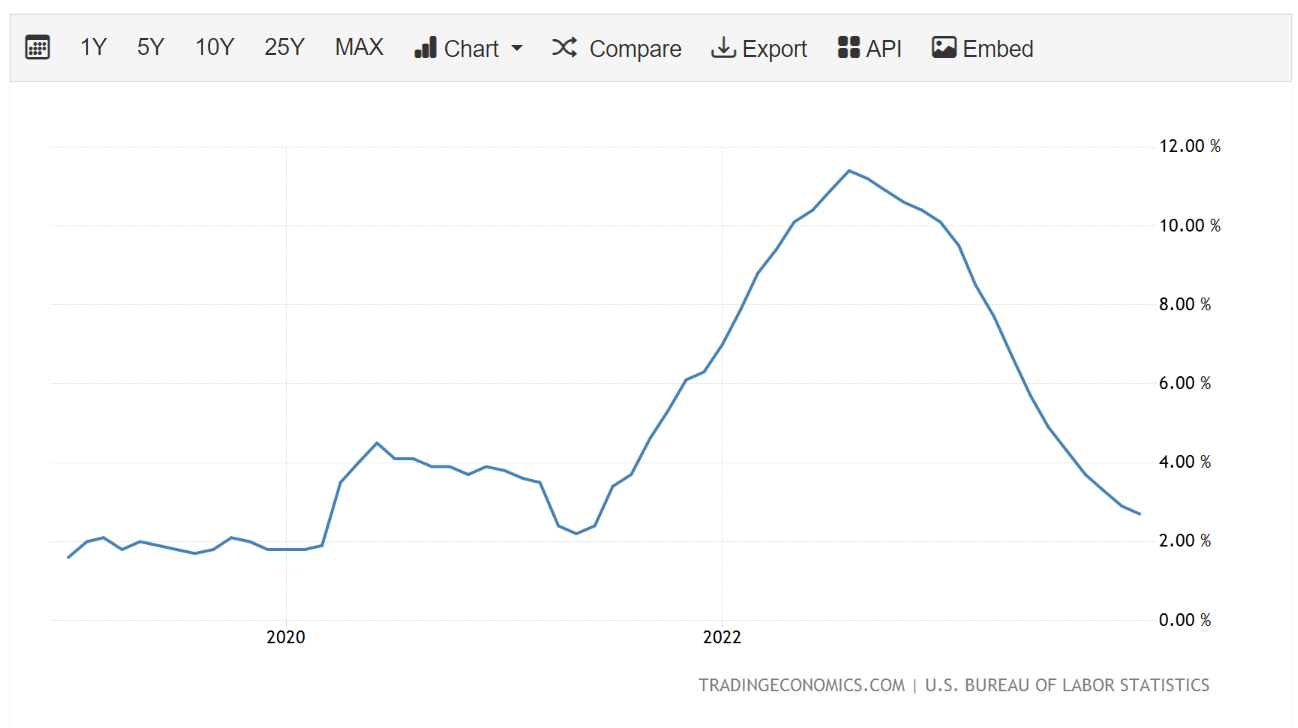

In fact, with consumer food inflation moderating to 2.7% YoY in December, any significant price actions from Ingredion will start to stand out like a sore thumb and may exacerbate the company's volume declines as consumers switch to substitute products and/or brands (Figure 10).

Figure 10 - Food inflation has moderated (tradingeconomics.com)

{kind=link}

Alternatively, if INGR does not take price action, then the company's margins may start to suffer, impacting earnings growth.

Conclusion

Ingredion continues to screen cheap, as the company has been able to grow earnings faster than its stock price appreciation, leaving the shares cheaper than when I recommended them in November 2022.

However, looking forward, earnings growth may moderate as price actions may be harder to implement in the coming quarters with moderating food inflation. With earnings growth expected to slow down, I believe the risk/reward is more balanced and I am downgrading INGR to a hold .

For further details see:

Ingredion: Earnings Growth Slowing Down