INGR - Ingredion Incorporated: A Purely Dividend Play

2024-01-17 04:05:34 ET

Summary

- Ingredion Incorporated is a food ingredient company that produces a variety of food additives and sweeteners using plant products.

- The company's revenue growth has been slow, averaging about 2% per year over the past 10 years and profits rose a bit faster due to efficiency gains in its operations.

- Ingredion has a strong history of steady dividend hikes and offers a decent yield of close to 3%, which is well-covered and sustainable.

- This is most likely an income play rather than a growth play. Investors shouldn't expect much growth from it with the exception of dividend growth.

Ingredion Incorporated (INGR) is a food ingredient company that uses corn, potatoes, grains, fruits, vegetables and other plant products into a variety of food additives such as sweeteners and other ingredients often used by the food and beverage industry. Some of the company's products include industrial and food grade starches, animal feed products, edible corn oil and a variety of sweeteners such as glucose syrups, high maltose syrups and high fructose corn syrup.

The company owns or operates a total of 47 production facilities 22 of which are located in North America and 7 are located in South America while the rest of them are located in other parts of the world such as Asia (some ownership being through joint ventures). The company also owns close to 90% of PureCircle which is one of the leading producers of stevia sweeteners globally.

This is a stable business but not exactly a fast-growing business either. Large food producers are constantly looking for ways to cut their costs and there is a lot of competition in the ingredient business which means that margins will be usually in check and growth will be muted. In the last 10 years, this company posted a total revenue growth of 28% (averaging about 2% per year) and most of this growth came in 2021 and 2022 when food prices were rising due to raging inflation.

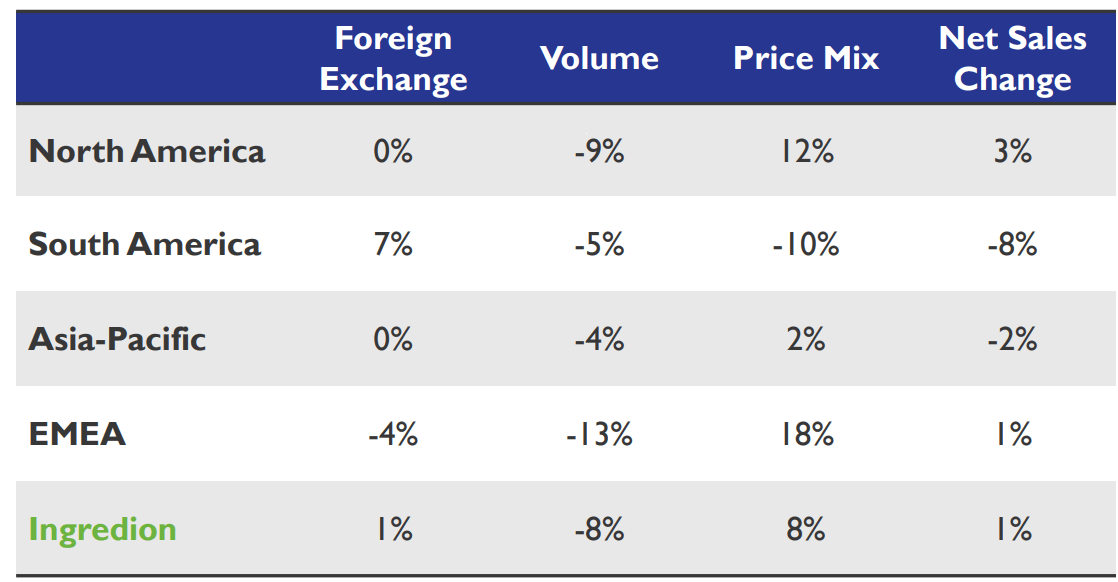

Last quarter it was interesting to see the inverse relationship between the company's sales volume and price mix. All in all, the company's price mix was up 8% while its volume was down -8% which meant its YoY revenue growth was almost flat, rising only 1%. The company was able to raise its prices to pass on some of its rising costs to its customers but this also resulted in its demand volume falling by almost the same percentage. In North America, prices were up 12% while volume was down -9% while in EMEA (Europe, Middle East & Africa) we saw an even more dramatic inverse relationship where prices were up 18% while volume was down -13%. It appears that customers weren't exactly eating up higher costs.

{kind=link}

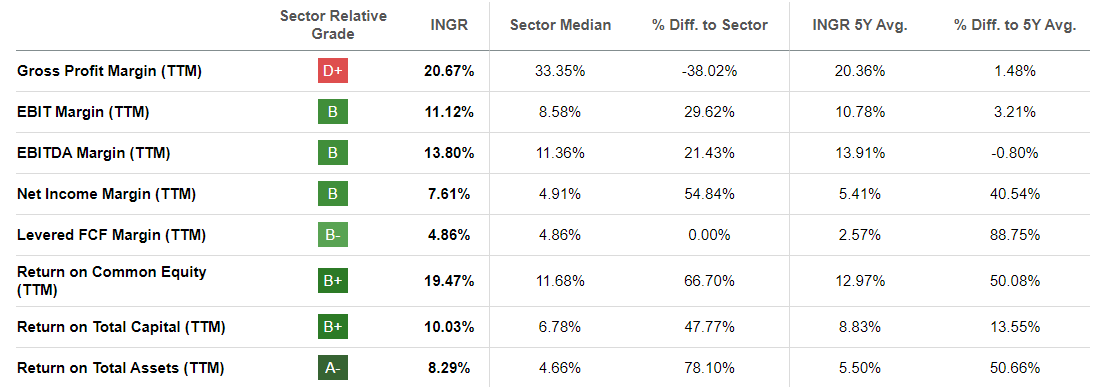

While the company's gross margins starting dropping in the last 2 quarters on QoQ basis, they were still up from a year ago. The company's current gross margin level of 20.7% is very similar to its long-term average of 20.4% and it should stabilize around here unless we see inflation raging once again which is possible but unlikely.

Still, the company's net income grew by 55% and its EPS (earnings per share) grew by 63% in the last 5 years, outpacing its revenue growth and gross margin growth as the company achieved better price mix, cost management and operating efficiencies. Having a slightly fewer diluted share count also helped the matters a little bit. You can only achieve so much profitability growth by only focusing on costs though. Sooner or later, most companies' profit growth starts matching their revenue growth rate unless they are aggressively buying back shares which this company isn't exactly doing.

Having said that, this is still a good dividend company with its decent yield of close to 3% (2.85% to be exact) and a strong history of steady dividend hikes going over more than 2 decades (the company has hiked dividends for 13 years in a row but the long term trend has been generally upwards for about 23 years). The company hiked its quarterly dividends by 24% in the last 5 years and by 85% in the last 10 years. Since 2000, dividends rose more than tenfold from a few cents per share to 78 cents per share and there are reasons to believe that this dividend growth can continue for quite some time even with slow growth the company has been experiencing.

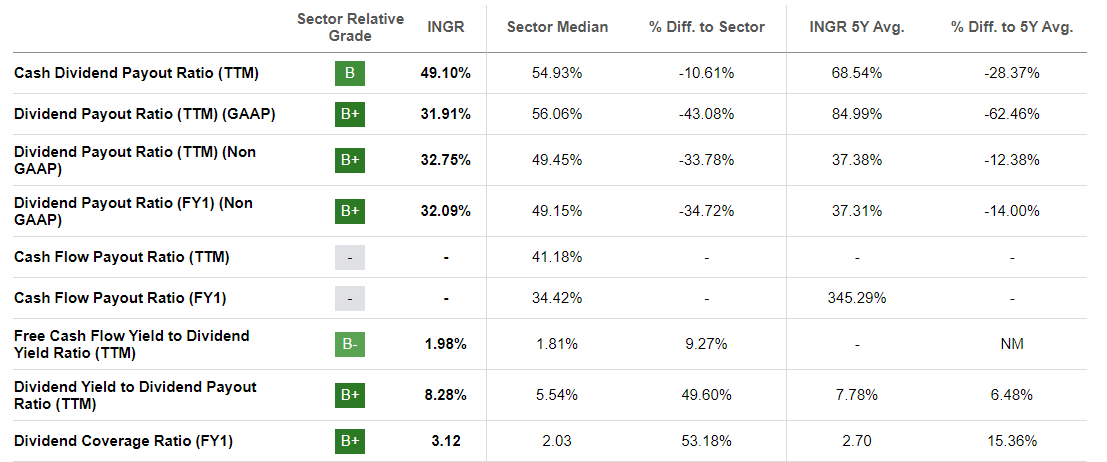

The company's cash payout ratio is 49% which is slightly below the sector median of 55% indicating that the company can comfortably cover its current dividend. This is also below the company's 5-year average of 68% even though the company's dividend payments grew by 24% during this time. More importantly, the company's dividend payout ratio based on GAAP terms is only 32% as compared to sector average of 59%. This metric indicates how much of its profits a company is distributing to its shareholders and the company is distributing only one third of its earnings whereas other companies in the sector are distributing two thirds. This also gives the company a dividend coverage ratio of 3.12 versus industry average of 2.03 meaning that the company makes more than three times as much money as it distributes.

{kind=link}

When we look at the company's earnings yield as compared to its dividend yield, the company's earnings yield comes at 8.50% versus it's dividend yield of 2.71% for the last 12 months or more like 2.85% if we look at its forward yield.

The company generates about $10.73 per share in operating cash flow which is much higher than its annual dividend expense which is around $3.62 per year. The company could easily double its dividends without suffering much based on this metric based on its operating cash flow.

When we look at the company's debt status, its debt-to-assets ratio is a low 32% and its debt-to-equity ratio is also relatively low 0.71. I would start worrying about this if debt to assets ratio was above 60% and if the debt to equity was above 1 but current levels are highly sustainable from a dividend standpoint. It's debt to EBITDA ratio is 2.21 indicating that it would take just a little over 2 years for the company to pay off all of its debt if it allocated all its EBITDA for this purpose which tells me that there isn't much of a problem there either.

The company's profitability metrics actually look interesting, which we already mentioned above. While the company's gross margins are lower than its peers at only 21% versus industry average of 33%, its operating margins are better than the industry. This looks like the company isn't able to pass most of its costs to its customers but it is running a highly efficient operation which allows it to generate more EBITDA from its smaller gross profits than what its peers can generate from higher gross margins which is impressive. The company's Return on Equity is 19% and Return on Total Capital is 10% versus its competition which posted 11% and 7% in these metrics respectively.

{kind=link}

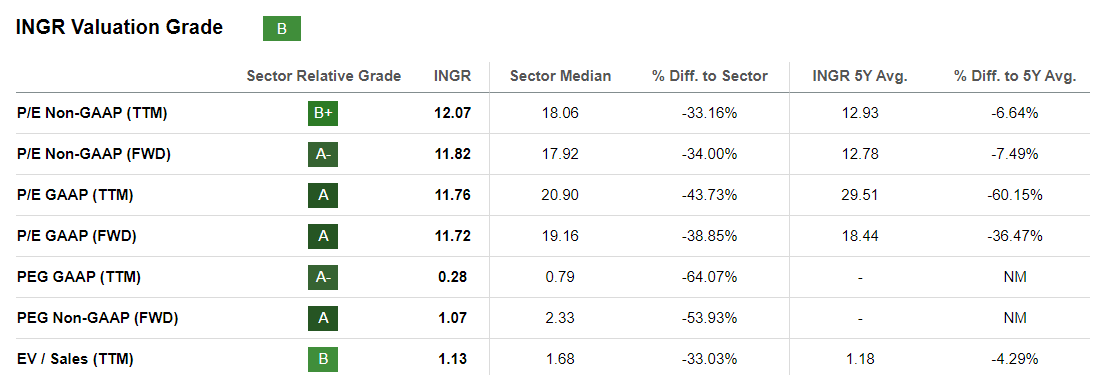

The company's valuation appears cheap but it is probably justified considering its relatively slow growth rate. Investors are paying this company only 11-12 times its GAAP earnings assigning a PEG ratio of 0.28 as compared to industry average P/E of 18 and PEG of 0.79 which indicates that it is pretty cheap but this is probably for a good reason. This stock is more of an income play and investors shouldn't treat this as a growth bet if they don't want to be disappointed.

{kind=link}

With its nice dividend yield approaching 3% and 20-year history of rising dividends not to mention its dividend being well-covered and having room for more increases based on the company's earnings yield, I actually consider this a pretty good dividend play as long as your expectations remain that this is a strictly income play. If the share price also appreciates, that would be a good plus but you should be prepared to accept it if your share price stays flat for a while and keep collecting those dividends.

For further details see:

Ingredion Incorporated: A Purely Dividend Play