INGR - Ingredion: Volume Recovery And Margin Expansion

2024-01-16 01:07:31 ET

Summary

- Ingredion has shown strong revenue growth but a slight contraction in margin driven by rising inflation.

- Falling corn prices and decelerating destocking are expected to support margin expansion and volume recovery, leading to a positive growth outlook for 2023.

- INGR outperforms its competitors in terms of forward revenue growth and net income margin, making it a buy case.

Synopsis

Ingredion ( INGR ) is a company that specializes in providing ingredient solutions. It turns basic ingredients, such as corn, into value-added ingredients and biomaterials for the food industry.

INGR's historical financial performance has shown robust revenue recovery and growth. Despite COVID affecting the business, its margins remained robust throughout the years. In 3Q23, revenue growth was modest as better price and product mix were offset by volume, but it was recovering sequentially due to decelerating destocking.

Looking ahead, falling corn prices are expected to bolster margin expansion, while recovering volume will bolster the growth outlook. As a result of all these tailwinds, management is positive about the 2023 growth outlook, and they have raised EPS guidance. All these point to management's confidence in the business outlook. Overall, I am recommending a buy rating for INGR.

Past Financial Performance

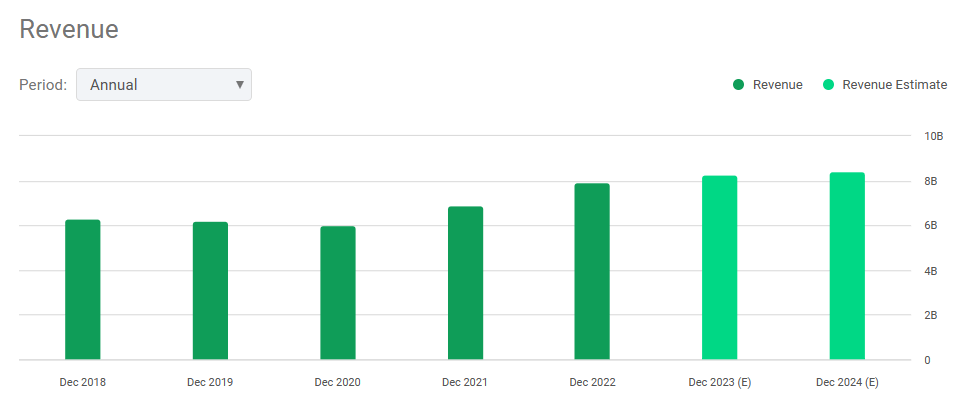

Over the last four years , INGR's revenue year-over-year growth has been strong. In 2020 , growth was negative due to the impact of COVID-19. As it eased, INGR's revenue growth recovered strongly and grew in a double-digit range. In both 2021 and 2022, revenue year-over-year growth is ~15%.

Author's Chart

Even though revenue has been volatile over the years, INGR's margins, such as gross profit margin, operating income margin, and net income margin, have remained quite robust, although there was a slight contraction in all of them. The margin contraction was primarily driven by rising inflation, which drove COGS and operating expenses higher.

Author's Chart

Analysis of 3Q23 Earnings Results

INGR reported robust 3Q23 earnings results. For the quarter, net sales were up 1% year-over-year, driven by strong price and product mix but offset by volumes. However, volume is recovering when compared to the previous quarter.

As a result of better pricing and product mix, both gross profit and operating income for the quarter increased year-over-year. INGR's gross profit increased 13% year-over-year, and gross profit margin expanded to 20.7%, up from the previous period of 18.5%. Its adjusted operating income for the quarter increased 15% year-over-year to $219 million, up from the previous period's $191 million. Its adjusted diluted EPS grew 15% to $2.33, up from the previous period's $1.73.

Margin Expansion and Falling Corn Prices

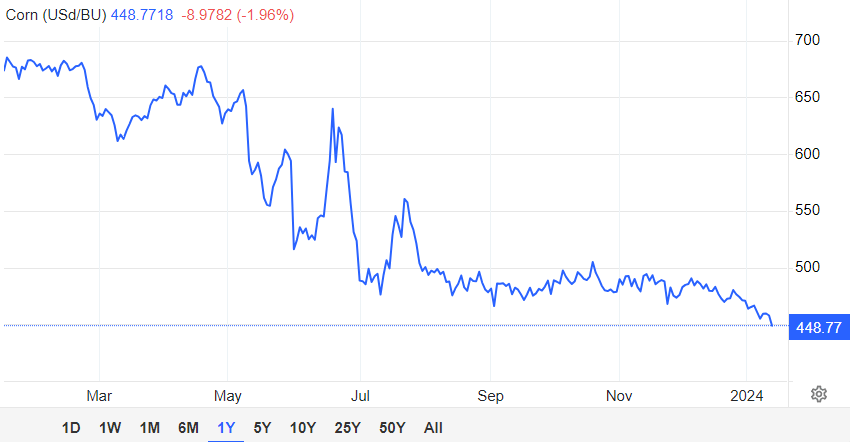

In 2024, INGR's margin is expected to expand, driven by its renewed several multiyear contracts with large customers, as these contracts ensure a significant base volume. As ~50% of North American revenue is from contracts that are adjusted monthly based on corn input cost, the anticipated lower corn cost in 2024 is anticipated to support margin expansion.

In January 2024 , corn prices fell after the United States Department of Agriculture [USDA] World Agricultural Supply and Demand Estimates [WASDE] reported and raised global corn production for 2024. Apart from the US, China's agriculture ministry also raised its 2024 corn production. Overall, corn production is expected to increase in 2024, and these reports support management's anticipation of lower corn costs in 2024.

{kind=link}

Decelerating Destocking

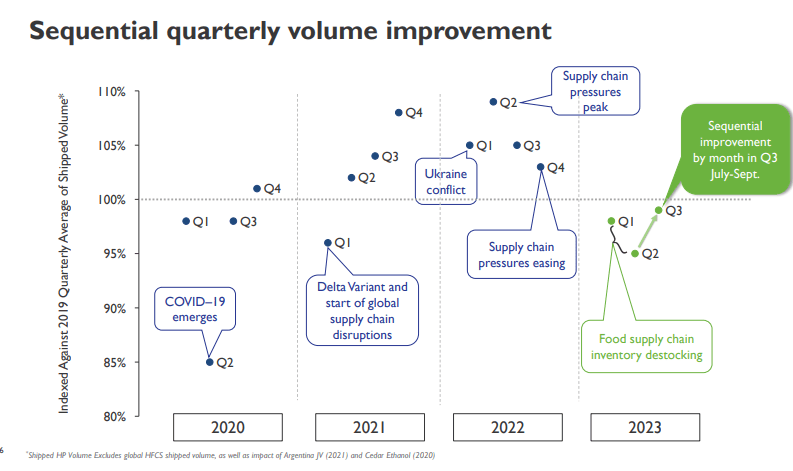

As mentioned earlier, INGR's revenue growth has been partially offset by weaker volume. Based on the following chart , it's clear that 3Q23's volume is still below 2019's benchmark level and significantly lower than the previous period. However, on the bright side, 3Q23's volume has improved sequentially from the previous quarter. This improvement can be attributed to the slowdown in inventory destocking.

Moving onto 2024, management is expecting the sequential improvement in volumes to continue based on 3Q23 and preliminary 4Q23 results. Based on INGR's customer feedback, INGR noticed that the destocking situation was almost over.

Quote: "I think as it relates to volumes, we are encouraged to see that sequentially, volumes month on month throughout quarter 3 have improved. And what I would also say is that based on Q3 results and early indications for quarter 4, we anticipate sequential improvements in volume shipments should continue."

{kind=link}

2023 Full-Year Estimates

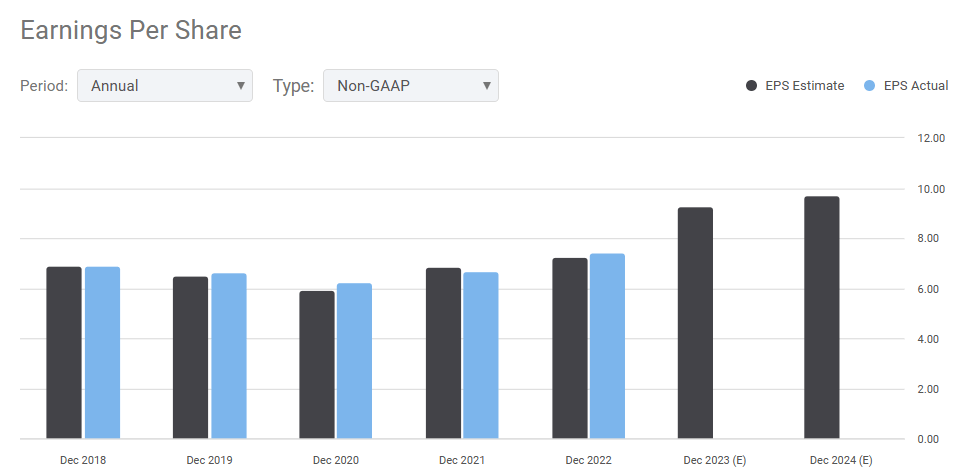

As a result of the decelerating destocking situation and falling corn prices, management is positive about INGR's 2023 outlook. Total revenue is expected to grow in the mid-single digits, while adjusted operating income is expected to grow in the high double digits. Adjusted EPS has also been raised and is expected to reach $9.05 to $9.45.

Overall, the outlook for 2023 is looking positive, and management's anticipation of growth, margin expansion, and raising of EPS shows that they are confident in the business as well.

Comparable Valuation Model

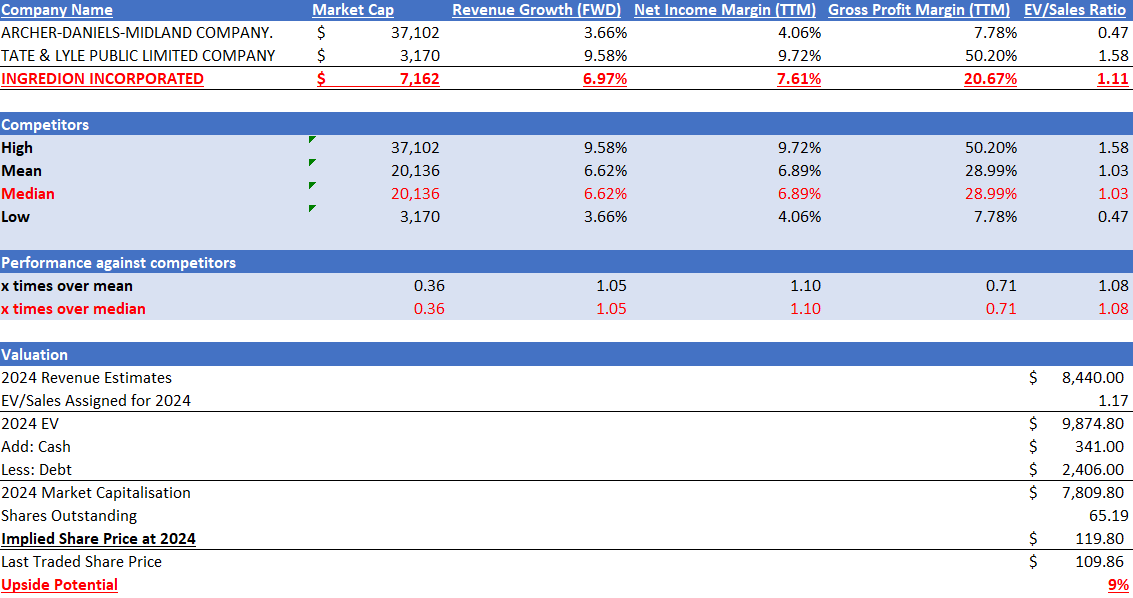

Based on INGR's annual report, it stated that its competitors are Archer-Daniels-Midland ( ADM ) and Tate & Lyle ( TATYF ). In terms of market size, INGR is only 0.36x its competitors' median. INGR's market capitalization is $7.16 billion vs. competitors' median of $20.14 billion.

Despite INGR's smaller size, it outperformed its competitors in terms of both forward revenue growth outlook and net income margin TTM. INGR's forward revenue growth rate is 6.97%, 5% higher than the median of 6.62%. Moving on, INGR has a net income margin TTM of 7.61%, 10% higher than the median of 6.89%. The impressive part is that INGR is able to achieve a higher net income margin with a lower gross profit margin. INGR's gross profit margin is 20.67%, while the median is 28.99%.

Currently, INGR has a higher forward EV/Sales of 1.11x vs. the median of 1.03x. Given its better performance, I argue that this is justified. However, it is lower when compared to INGR's 5-year average forward EV/Sales of 1.17x.

The market revenue estimate for INGR is anticipated to reach $8.30 billion in 2023 and $8.44 billion in 2024. In terms of EPS, it is expected to expand to $9.29 in 2023 and $9.71 in 2024. These estimates are reliable as they tie in with management's guidance as well as the growth catalysts and financial strength I discussed earlier.

By applying forward EV/Sales of 1.17x to its 2024 revenue estimate, my price target for 2024 is $119.80, representing an upside potential of 9%. Overall, I am recommending a buy rating for INGR.

{kind=link}

{kind=link}

{kind=link}

Risk

One downside risk of investing in INGR is its dependency on corn price fluctuations for margin expansion. Even though there have been improvements in sales volumes recently and anticipation of lower corn costs, these factors are volatile and are subject to unpredictable external influences, such as weather conditions and geopolitical tensions. If the situation turns for the worse and is expected to reverse, INGR's valuation might be revised.

Conclusion

In conclusion, INGR's past financial performance has demonstrated strong revenue growth after the onset of COVID-19. Over the past four years, margins have remained strong despite the disruption, although I have noticed a slight contraction due to inflation.

In its most recent earnings, revenue continued to grow, but at a modest level, as strong price and product mix were offset by volume. Although volume was weak, it has sequentially improved, driven by the deceleration in destocking. Moving ahead, management expects volume to continue recovering, which will bolster its growth outlook. In addition, corn prices have been falling, driven by higher corn production predictions. As corn prices fall, it is expected to strengthen INGR's forward margins.

When compared to its competitors, INGR outperformed them in both forward revenue growth rate and profitability. The upside potential combined with a positive growth outlook leads me to recommend a buy rating for INGR.

For further details see:

Ingredion: Volume Recovery And Margin Expansion