INMD - InMode: A Brief Analysis Of Profitability And Efficiency Reaffirms Buy Rating

Summary

- Although INMD's return on equity has decreased over the years, it still remains very attractive relative to most of the firms in the health care equipment industry.

- While the profit margin has contracted somewhat in 2022, due to the challenging macroeconomic environment, it has expanded substantially over the past years.

- While INMD has very little leverage, we would like to see the firm start using its cash and short-term investments more efficiently.

- All in all, we maintain our "buy" rating.

InMode Ltd. ( INMD ) designs, develops, manufactures, and markets minimally invasive aesthetic medical products based on its proprietary radiofrequency assisted lipolysis and deep subdermal fractional radiofrequency technologies in the United States and internationally.

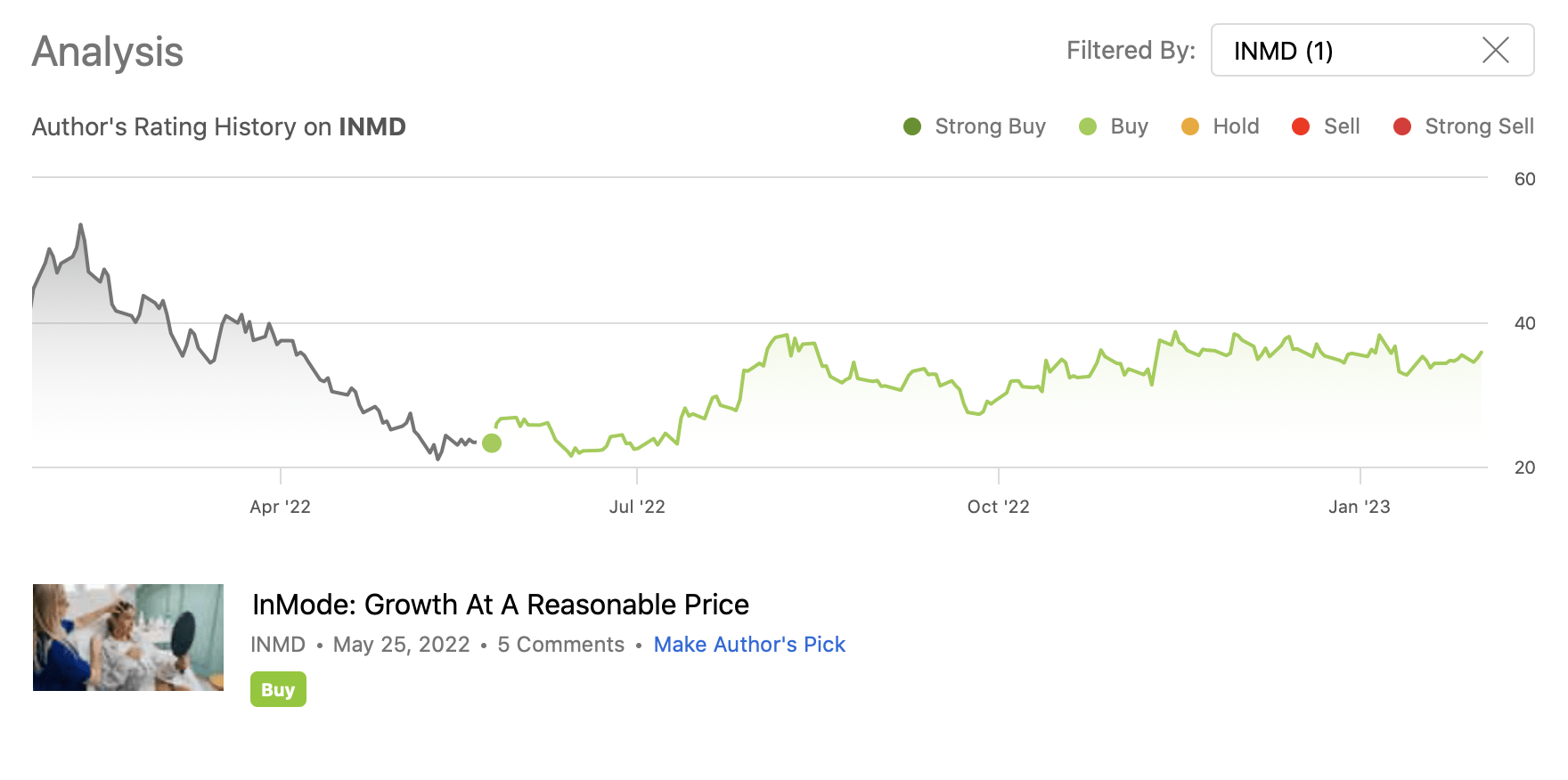

We have already published an article on the firm on Seeking Alpha in 2022, titled: " InMode: Growth At A Reasonable Price ". Back then, our view was bullish on the firm, because of its strong revenue and earnings growth, its high gross margins and its relative valuation based on price multiples.

{kind=link}

Today, we are going to look at InMode's business from a different perspective, focusing primarily on its profitability and efficiency by analysing its return on equity ((ROE)). We will also decompose the ROE measure to three parts, namely to the net profit margin, the asset turnover and the equity multiplier, to understand what have been the primary drivers of the dynamics over the past years.

{kind=link}

Return on Equity

ROE is an important measure of financial performance, and it is often used to gauge the corporation's profitability and its efficiency of generating profits. An improving or stable ROE is normally a good sign, if it happens for the right reasons.

When looking at INMD's ROE over the years, we can see that it has been quite volatile over the years. The following chart shows INMD's ROE over the past years.

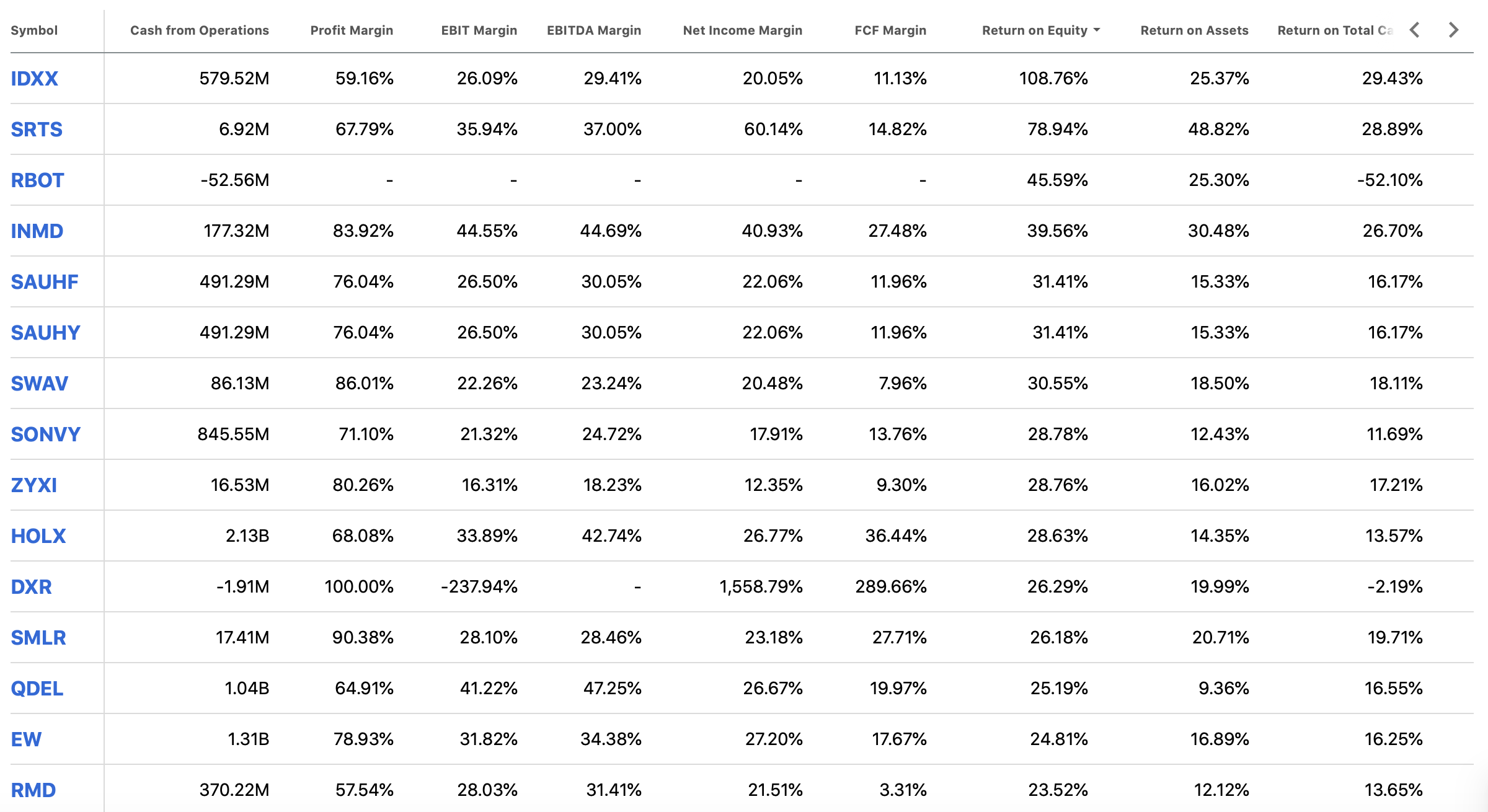

While this measure has declined from over 60% to 40%, we are not necessarily concerned about it. First of all, a 40% ROE is still exceptional. To put this into perspective, the following table summarises some of the profitability measures of several firms in the health care equipment industry. When comparing InMode to other firms in the industry, we can see it still has one of the highest ROEs, despite the decline.

{kind=link}

This is not the only reason, why we are not concerned. To explain why, let us decompose the return on equity now, and see what have been the primary drivers of the changes and volatility.

Net profit margin

Despite the declining ROE, the net margin has actually improved significantly. It is even more impressive, if we take into account the challenging macroeconomic environment in 2022. Despite the inflationary pressures, the poor consumer confidence, the geopolitical tensions in the Eastern European region, the high energy price and elevated freight costs, InMode has still managed to expand its net profit margin.

Looking forward, we believe that the company will be able to maintain these high margins, or even slightly improve them. In our opinion, the macroeconomic environment is likely to start improving in the coming quarters, which could provide tailwinds for INMD's business.

Asset turnover

One of the key reasons for the declining ROE is the asset turnover. The asset turnover ratio (or sometimes called asset utilization) measures the value of a company's sales or revenues relative to the value of its assets. It indicates how effectively the company is using its assets to generate sales.

There are 2 reasons why this measure may decline: decreasing sales and increasing assets.

The following chart shows how InMode's sales have been developing over the past years. We can see that revenue has increased significantly, despite showing some slowing in 2022. Important to understand, whether the firm is trying to 'improve' its sales by offering better credit terms to customers and therefore creating artificial demand, or pulling demand forward from future periods. This can be identified by look at the accounts receivable. If the accounts receivable grow at a faster pace than sales do, such a manipulative practice is likely.

Over the past years, in most quarters, accounts receivable growth has been below sales growth, which is a good sign. In 2022, however, accounts receivable have grown faster than sales, which likely improved by the poor macroeconomic situation. It has likely had an indirect impact on the net margins and therefore on the ROE as well.

Now we know that it is not the sales that caused the asset turnover to decline.

In fact, in the same period, assets have increased by more than 600%. And the reason for this is the growth in current assets, mainly short-term investments. It indicates that the firm has a lot of current assets on hand, but it is not able to use it in a way, which could make the business more profitable or more efficient.

While it is a good sign that the firm's asset base has been growing, and that it has remained largely debt free, we would like to see the firm utilising this money. Either by investing into further growth or by returning value to shareholders in the form of dividends or through share buybacks.

Equity multiplier

The last part of the three-step decomposition of the ROE is the equity multiplier, which is simply the ratio of assets to shareholder equity. A higher ratio indicates more leverage, meaning that the firm is using a larger amount of debt to finance its assets. This measure is telling largely the same story as the asset utilisation ratio. The firm has barely any liabilities, and it has even been decreasing over the past years.

At the same time, InMode's liquidity ratios have been gradually improving. The current and quick ratios are used to see whether the firm can cover its current liabilities with its current assets. The difference between the two is that the quick ratio excludes inventories. Both the quick and the current ratios are above 9. Just to put it into perspective, normally if they are above 1 it is already a good sign.

We believe that INMD has outstanding financial flexibility, it could be able to handle much more liability than they currently have.

To sum up

Despite the declining/volatile ROE over the past years, our view remains bullish on the firm.

While the challenging macroeconomic environment had a negative impact on the firm, overall they have still managed to expand their net profit margin and increase their sales, even if accounts receivable also increased substantially.

The firm has been having an increasing asset base, driven primarily by the increase in current assets, while they remain largely leverage free.

Ideally, we would like to see the firm use its cash and short-term investments to either finance further growth opportunities or to return value to its shareholders in the form of dividends or share buybacks.

All in all, we maintain our "buy" rating.

For further details see:

InMode: A Brief Analysis Of Profitability And Efficiency Reaffirms Buy Rating