INMD - InMode: A Compelling Investment In The Fast-Growing Medical Aesthetics Market

2023-05-05 23:26:46 ET

Summary

- InMode is a leading provider of innovative, energy-based, and minimally invasive aesthetic and medical treatment solutions.

- The company has seen explosive growth on both the top line and bottom line with revenues and EBITDA growing at a 46% and 58% CAGR, respectively.

- After a strong Q1, management's previous guidance last quarter for the full year is likely conservative.

- At 10.7x EV/EBITDA, INMD stock is trading at a substantial discount to its historical average multiple of 21.3x EV/EBITDA.

Company Overview

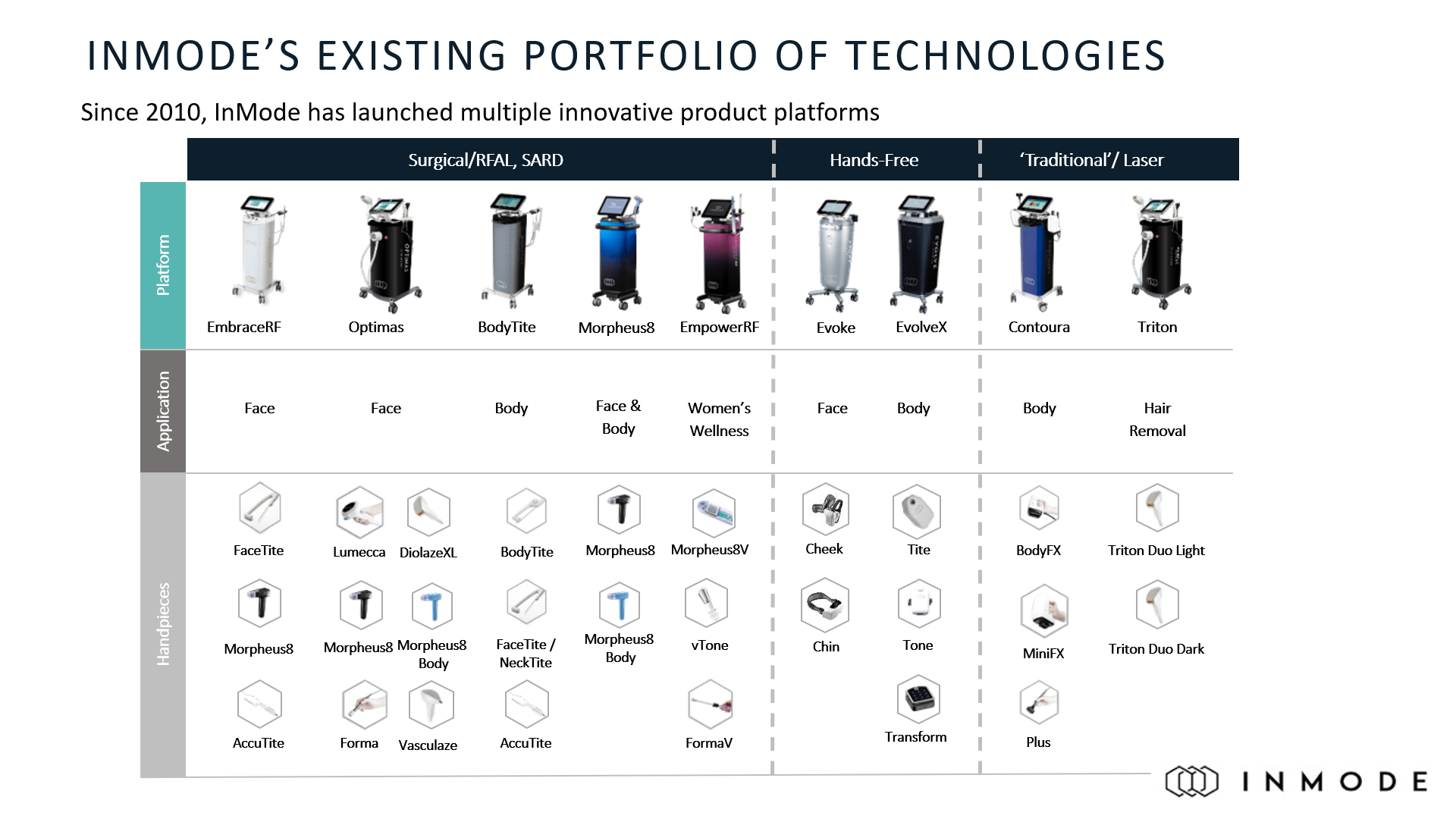

InMode Ltd ( INMD ) is a leading global provider of innovative, energy-based, and minimally invasive aesthetic and medical treatment solutions. Based in Israel, the company offers products spanning various medical fields, including plastic surgery, dermatology, gynecology, and ophthalmology. Its three main segments are Minimally Invasive, Non-Invasive (Laser), and Hands-Free. The Minimally Invasive segment, which includes products such as BodyTite, Optimas, EmbraceRF, Votiva, and Morpheus8, accounts for 80% of total revenues. The Non-Invasive segment, which includes Contoura and Triton, accounts for 10% of total revenues and has primary applications in hair removal, body contouring, and skin tightening. The remaining 10% of revenue comes from the Hands-Free segment, which includes Evolve and Evoke, both focused on skin rejuvenation, body contouring, and skin tightening. InMode's proprietary Radiofrequency ((RF)) technologies enable the company to deliver surgical-grade results with significantly reduced risks of scarring, downtime, pain, and other complications associated with surgical procedures. The company generates almost 70% of its revenue through sales in the United States and the remainder internationally, and through direct and third-party sales in over 130 countries.

{kind=link}

Investor Presentation

InMode generates recurring revenue by selling products to its traditional customer base of plastic and facial surgeons, aesthetic surgeons, and dermatologists, and by expanding its customer base to include non-traditional customers, such as ENT physicians, ophthalmologists, general practitioners, and aesthetic clinicians. The company's ability to routinely introduce novel and patented products to the market with platforms that are lightweight compared to competitors' larger and heavier products is a significant competitive advantage.

In addition, InMode also has established itself as a market leader with strong brand recognition in the industry with a portfolio that is well-known by both physicians and patients. The company also provides after-sales service and support, including training and education for physicians and other healthcare professionals, leading to stronger customer retention. The specialized training and equipment requirements of the company's products make it difficult and costly for aestheticians to switch to competitor products, giving InMode a competitive edge in the market.

Investment Thesis

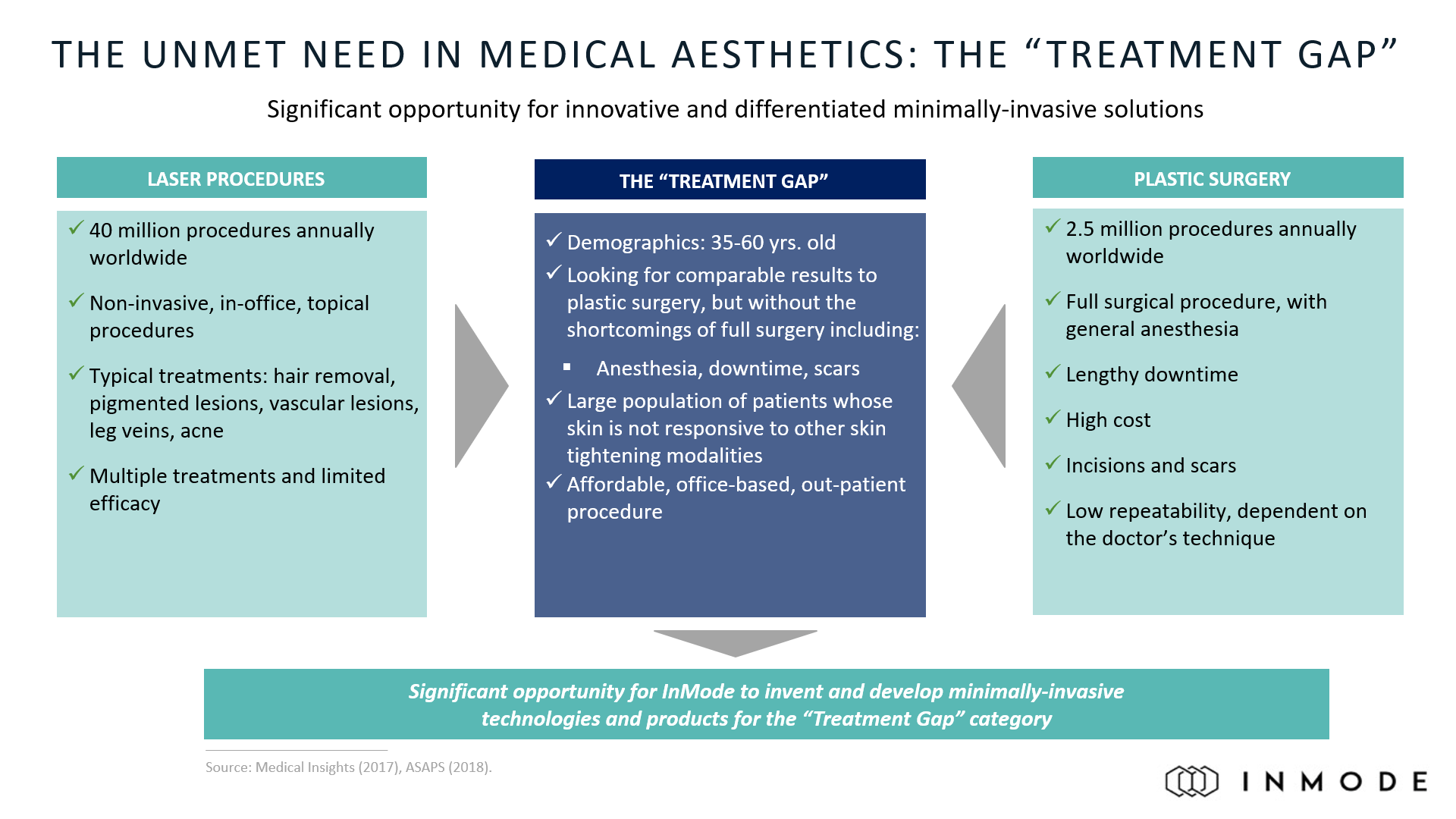

As a leading provider of medical aesthetic solutions, InMode aims to address the unmet needs of patients through its unique approach to the "Treatment Gap". With capital equipment sales accounting for more than 85% of its total revenue, the company offers a range of technologies that deliver results comparable to plastic surgery without the limitations of traditional procedures. InMode's solutions are performed in-office, without general anesthesia, lengthy downtime, or incisions, making them accessible and affordable to a wider patient base.

{kind=link}

Investor Presentation

In order to maintain its market dominance and support continued growth, InMode invests heavily in research and development, with a goal of introducing two new platforms annually to expand its offerings and enter new markets. Recently, the company entered the women's health and wellness sector, targeting the needs of OBGYNs and their patients. With more than 40,000 OBGYNs in the U.S., this presents InMode with a runway to take market share from competitors and expand the company's total addressable market.

InMode operates in a capital-intensive industry but maintains a competitive edge through its innovative business model. Each new platform the company launches must achieve an 85% gross margin, which it accomplishes by leveraging its patented RF technology to charge a premium price. The high cost of these platforms, which range from $120,000 to $130,000, acts as a barrier to entry for competitors. Additionally, competitors face a lengthy FDA approval process that can take around 5 years, further cementing InMode's dominance in the market.

In terms of cost efficiency, InMode adopts a lean business model with low fixed costs thanks to outsourced manufacturing in Israel. Its R&D margins are also kept at a low 2-3%, compared to nearly triple that for most of its competitors. These measures enable the company to generate high operating margins in the mid-40s and maintain an attractive return on invested capital above 25%.

Finally, InMode is dedicated to customer satisfaction, a focus that fosters their propensity to purchase additional products. The company's efforts are evident in that more than half of its existing clients have acquired more than one product. As its operations expand worldwide, with over 15,000 systems installed globally, consumables are emerging as a critical component of its revenue mix, accounting for approximately 15% of total revenue. This growing consumables business represents a recurring revenue stream and a significant advantage for the company's continued growth. By offering these consumables at an affordable price doctors are incentivized to adopt them. In my view, the scalability of the company's consumables segment represent a substantial advantage and should contribute significantly to the firm's overall growth strategy going forward.

Competitive Positioning

Over the years, InMode has proven itself as an excellent operator through its management of its operations, business mix, and supply chain. This was demonstrated during the early days of the pandemic where unlike its competitors who were reducing staffing and cutting back on operational expenses, InMode invested heavily in research and development, capacity expansion, and attracting top talent from competitors. This has paid off well a few years later with the company exhibiting strong revenue growth and record profitability.

In my view, InMode's business model differs from traditional laser companies as over two-thirds of the company’s revenue is generated from its patented non-invasive RF technology, with the highly competitive traditional laser only accounting for 10% of total revenue. On the other hand, industry players like Alma, Cutera and Venus generate virtually all of their revenue from laser. With laser being a highly competitive space, most of these competitors are barely profitable and struggle to break even.

Through its impressive supply chain management, InMode has reduced its reliance on a sole component supplier, ensuring the prompt delivery of orders within 10 days, a stark contrast to the 6 to 9 month lead times typical of its competitors. This strategic approach has enabled the company to maintain control over its margins and sustain a loyal customer base, contributing to its overall market dominance.

Financials

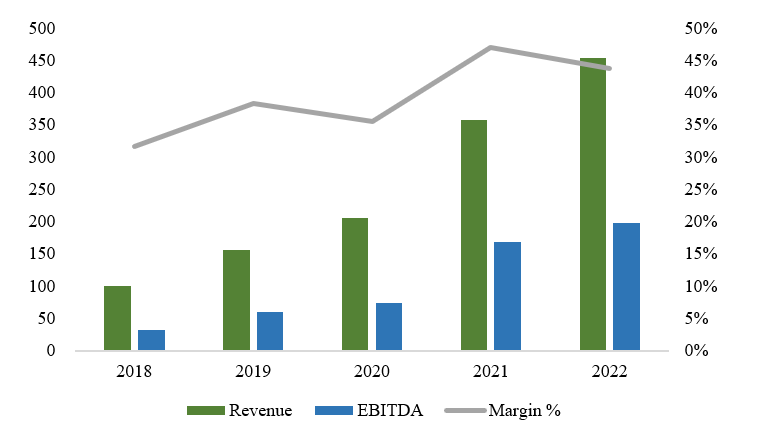

Since 2018, InMode has grown revenues at a 46% CAGR and EBITDA at a 58% CAGR . While maintaining industry-leading gross margins and operating margins, averaging 85% and 45%, respectively, InMode has seen impressive top line and bottom line growth. Much of this success can be attributed to the company's ability to meet customer needs in the market and the use of strategic manufacturing in Israel which allow for low fixed costs. In addition, these low costs also allow for lower R&D costs as a percentage of revenue, at around 3%. Along with its increasing margins, the company has also made some prudent capital allocation decisions.

{kind=link}

Author, based on data from S&P Capital IQ

Over the years, InMode has consistently prioritized investment into R&D to enhance its breadth of products and services. While the industry is capital intensive, InMode has been focused on growing organically by reinvesting cash flows back into the business with an average return on invested capital over 25%. With a cash position of $93.0 million and $481.5 million in liquid short-term investments, the company is in a strong financial position with no debt on its balance sheet. I believe that this financial flexibility should allow the company to weather any potential macroeconomic headwinds in the near term, while also supporting growth opportunities, either through continued expansion into new platforms or acquiring complementary businesses that can enhance its offerings.

When looking at InMode's most recent quarter , revenue was $106.1 million for the quarter, up 23.5% year over year, primarily driven by an increase in consumables and disposable sales. Capital equipment sales made up 81% of revenues for the quarter while consumables made up 19% of revenues. On the earnings call , management noted that M&A is still on the table and that they are currently exploring acquisitions with similar profitability to InMode for an acquisition that will be accretive for shareholders. Here's what the CEO had to say:

Well, that's the $64,000 question, I would say. Yes, we are exploring opportunities, more than one. And some of them are -- we even spend money to check to due diligence, et cetera. One thing I want to say, very difficult to find a company that will be with the same -- with the same profitability structure of InMode. So any company that we will acquire should not dilute the shareholders. It should be accretive and not dilutive. And it's not easy. It's not easy because of the profitability structure of InMode. So we're very careful in the analysis that we're doing on companies that we would like or that we're exploring a possibility to do M&A. I cannot announce anything special today. The only thing I can say that we spend on the time, money, management attention and we're looking for acquisition.

In my view, the CEO's comments show a willingness to be disciplined and deploy capital prudently. It also suggests a responsible approach to managing the company's resources. It can be easy to get trigger happy with the kind of cash InMode has however this approach to managing its balance sheet will help to ensure the long-term viability of the business and its ability to weather any unexpected challenges. By being disciplined in its spending and investment decisions and waiting for opportunities, the company can avoid the temptation to pursue short-term gains at the expense of long-term growth.

Finally, management also reiterated its guidance for 2023 with revenues between $525 million and $530 million, non-GAAP gross margin between 83% to 85%, and non-GAAP earnings per diluted share between $2.58 and $2.60. With a very strong start to the year with nearly 24% growth in the first quarter, I believe it's likely that this guidance is on the conservative side (projecting a 16% annual increase in revenues from 2022).

Valuation

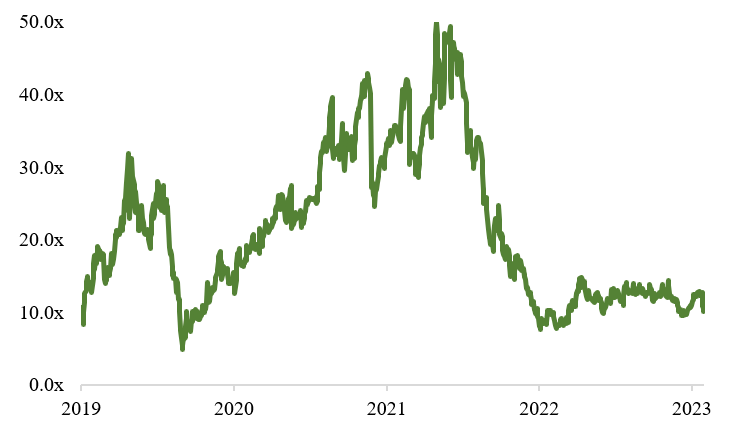

Based on the 5 analysts with one year target prices on InMode, the average target price is $49.60, with a high estimate of $60.00 and a low estimate of $40.00. From the average price, this implies about 47.1% upside from the current price. At 10.7x EV/EBITDA and 16.9x P/E, the company's valuation metrics are well below its 5-year historical multiples of 21.3x EV/EBITDA and 28.1x P/E. While its unlikely the company can continue growing revenues at a 46% CAGR and some deceleration in the growth rate should be expected, I believe such a disconnect is unwarranted for an industry leader that should be able to grow in the double-digits and maintain high margins.

{kind=link}

Historical EV/EBITDA Range

Conclusion

In summary, InMode is a leading provider of innovative, energy-based, and minimally invasive aesthetic and medical treatment solutions. With its high investment in R&D to address the unmet needs of patients, the company has positioned itself as a market leader and has been growing revenues and EBITDA of 46 and 58%, respectively. While the company's growth rate is likely to decelerate going forward in the mid-twenties, I believe management is being conservative with their guidance for the full year after a great Q1. Trading at a substantial discount to its average historical multiple at 10.7x EV/EBITDA, I believe INMD stock looks attractive today.

For further details see:

InMode: A Compelling Investment In The Fast-Growing Medical Aesthetics Market