INMD - InMode: A Deep Analysis Into Its Mixed Picture

2023-12-04 12:23:31 ET

Summary

- InMode Ltd. is a company in the medical aesthetics space known for their cutting-edge, minimally invasive technologies (a description of each product they offer is in the analysis).

- The company's financial performance for Q3 2023 showed modest but significant growth, reflecting resilience in a challenging economic climate.

- InMode's celebrity endorsements and innovative treatments have positively impacted their market position and brand perception.

Investment Thesis

Based on the research I have conducted, I will be sharing my comprehensive take on InMode Ltd. ( INMD ), which stands at a crossroads of opportunity and challenge, making it a fascinating subject for potential investors and industry observers alike. The focus will not just be on the dry numbers but also on what lies behind them – the innovative spirit, the strategic moves, and the resilience in the face of economic headwinds. I find myself at a 'hold' position, not swayed by short-term fluctuations but looking towards the horizon where InMode's potential could unfold.

Introduction

InMode Ltd. is a company specializing in the development, manufacture, and marketing of innovative medical technologies. They focus primarily on minimally invasive and non-invasive procedures for body contouring, skin treatment, and various medical aesthetic applications. InMode's technology platforms, which include radiofrequency, laser, and pulsed light, cater to a wide range of treatments. These treatments encompass facial and body contouring, skin rejuvenation, hair removal, and anti-aging procedures. The company's offerings are designed to provide effective results with minimal downtime for patients, making them a popular choice in the aesthetics and dermatology industry. Each of the treatments are described more in-depth below:

- Morpheus8: a minimally invasive treatment utilizing bipolar radiofrequency energy, particularly effective for fractional coagulation of subcutaneous tissue. Celebrities such as Bella Thorne, Jessica Simpson, Lisa Rinna, and January Jones have chosen Morpheus8 for its ability to deliver deep fractional treatments with minimal invasiveness. This treatment is known for its depth of penetration and the ability to customize treatments, making it suitable for various aesthetic enhancements????.

- Morpheus8 Body : designed specifically for larger and deeper tissue treatments. It extends the capabilities of Morpheus8 to body areas, offering deep fractional coagulation. Kim Kardashian, Eva Longoria, D’Andra Simmons, and Michelle Maturo have opted for Morpheus8 Body. This choice highlights the treatment's effectiveness in addressing larger body areas with the same precision and minimal downtime as the original Morpheus8, making it a popular choice for comprehensive body contouring and rejuvenation????.

-

Forma: a treatment that uses bipolar radiofrequency energy for skin heating, has been chosen by celebrities like Kim Kardashian, Eva Longoria, Kourtney Kardashian, Sydney Sweeney, Emma Roberts, Shay Mitchell, Chrissy Teigen, Amber Rose, and Britney Spears. This treatment improves skin appearance and reveals a radiant look, making it popular among those in the public eye seeking non-invasive skin rejuvenation????.

-

EvolveX: a hands-free platform for body transformation. It combines multiple technologies like Tite ((Bipolar RF)), Tone ((EMS)), and Transform ((Bipolar RF and EMS)) for skin treatment, muscle toning, and body tissue transformation. Celebrities like Jordyn Wood, JuJu Smith-Schuster, Dalvin Cook, Francesca Farago, Nick Scott, and Delilah Belle have opted for EvolveX, drawn by its non-invasive nature and ability to deliver transformative results without downtime????.

-

FaceTite: a minimally invasive radiofrequency treatment for small areas in a single session. These treatments have been selected by celebrities such as AJ McLean, Ireland Baldwin, Braunwyn Windham Burke, Michelle Money, and Kelly Dodd. Their ability to deliver significant aesthetic improvements without the need for extensive surgery makes them a preferred choice for those looking for quick and effective facial rejuvenation????.

-

BodyTite: a minimally invasive treatment for large body areas through soft tissue coagulation, attracting celebrities like Braunwyn Windham Burke, Sarah Leann, Mia Jackson, and Paige Hathaway. It offers results similar to excisional procedures but with minimal downtime, attracting those seeking body contouring without the scars associated with traditional surgery????.

-

EmpowerRF: a multi-functional platform delivering women’s wellness therapies, which has been used by celebrities like Amanza Smith, Aurora Culpo, and Braunwyn Windham Burke. It offers therapies like intravaginal electrical muscle stimulation ((EMS)), bipolar radiofrequency ((RF)) for deep heating, and sub-dermal fractional microneedling and coagulation. This treatment is especially significant for addressing a range of issues from urinary incontinence to improving blood circulation, making it a versatile choice for women's wellness????.

The utilization of these treatments by celebrities significantly impacts InMode's market position and brand perception. Celebrity endorsements naturally attract public interest, enhancing brand visibility and credibility. We also know that consumers are very keen to follow recommendations of those they follow on social media. This association not only validates the effectiveness of InMode's treatments but also broadens their appeal to a larger audience seeking similar aesthetic and wellness results.

Financials and Outlook

Q3 Read-out

As of the latest reports , InMode has $3.58 million in debt, a decrease from a previous high of $5 million. This debt level, set against a backdrop of $675.85 million in cash, gives a net cash position of $672.27 million, indicating a relatively stable financial condition??.

InMode has presented its financial performance for the third quarter of 2023, revealing insights crucial for understanding its current market standing and future trajectory. Their revenue of $123.1 million, marking a 2% increase compared to the same quarter in 2022, suggests resilience in a challenging economic climate. Growth was modest but significant considering the global economic headwinds and restoration of seasonal norms following the pandemic. Also, the revenue distribution reflects a strong international presence as sales in Asia amounted to $44.9 million, accounting for 36% of total revenues. By diversifying its operations across regions, InMode is able to hedge risks associated with regional market fluctuation that demonstrates a successful penetration strategy.

In terms of operational efficiency, InMode has maintained an impressive gross margin of 84%, within their target range of 83% to 85%. This high margin reflects their operational efficiency, pricing power, and ability to manage costs amidst inflationary pressures. Although sales and marketing costs shot up from $43.1 million to the current $50.8 million, it seems like an aggressive but worth-it investment for growth, albeit momentarily pressing down on net profits. Though these investments are necessary for the growth, they may also dent short term earnings.

In terms of capital allocation, InMode's cautious approach to stock buybacks, preferring to explore M&A opportunities, suggests a long-term vision focused on sustainable growth and market leadership. This strategy, while not immediately beneficial to stock prices, aligns with InMode's overall goal of building a resilient and growth-oriented business.

Considering the stock performance of InMode, the financials provide a mixed signal. On one hand, the company's steady revenue growth, impressive gross margins, and continuous innovation indicate a strong foundation and potential for future growth. On the other hand, the challenges posed by economic conditions, increased financing costs, and competitive market dynamics necessitate a cautious approach. The stock's performance in the market will likely continue to reflect these complex interplays of internal strengths and external challenges.

The introduction of Envision as a non-surgical ophthalmic platform and Define, a hands-free technology for facial treatments, is indicative of the company’s product portfolio and commitment to innovation. These launches are the underlying strategy to InMode’s aim at extending their global footprint, increasing the technological capacities in the company. Nonetheless, InMode is plagued by extremely high-interest rates for credit deals and agreements, especially in America. Such a scenario has slowed down sales velocity since customers act cautiously while making investment decisions. InMode’s management is engaging with leasing companies on ways to address the situation, which demonstrates responsiveness toward market conditions.

Resilience of supply chain & inventory management at InMode is praiseworthy. The company has enough inventory to cover anticipated customer needs through the next quarters in order to maintain seamless services and deliverables. Timeliness of this process makes it important for customer faithfulness and sustenance of competition within a field where customer confidence and a competitive edge are essential factors.

InMode’s management, in particular the CEO Moshe Mizrahy, provided emphasis on innovation, operational efficacy, as well as strategic progression. During the earnings call, Mizrahy emphasized the need for adaptation, growth through investing in R&D, and marketing in order to grow. This symbolizes a proactive leadership acknowledging present day problems in the market as well as exploiting chances for more expansion.

However, looking at InMode corporate analysis, the company sits well in a dynamically changing industry. Although there are intense competitive pressures and a difference amongst consumer preferences, this shows that InMode’s ability to drive revenues and maintain gross margins is strong.

In conclusion, maintaining a "hold" rating on InMode is justified based on their current financials and market position. This rating balances the recognition of InMode's strong fundamentals and growth potential against the backdrop of economic uncertainties and market challenges. Investors are advised to closely monitor the company's performance, particularly in areas such as product innovation, market expansion strategies, and responses to economic and market pressures. The upcoming quarters will be critical in assessing InMode's ability to sustain its growth trajectory and adapt to the dynamic market environment.

Forward Guidance

Analyzing InMode's future outlook from my perspective as an investor, I'm inclined to maintain a 'hold' stance on the stock. The third quarter of 2023 revealed some key insights that are pivotal in shaping this decision. InMode's CEO Moshe Mizrahy mentioned, "InMode has been in an accelerator growth rate as we establish our presence in the US and globally." This statement underlines the company's robust expansion strategy, which has been a positive driving force. However, it's important to note that the third quarter saw a slowdown, with revenue only increasing by 2% compared to the same period in 2022. This slowdown, attributed to normal industry seasonality and exacerbated by the COVID-19 pandemic, suggests a return to more traditional market patterns, which could impact future growth rates.

Another critical aspect to consider is the impact of very high interest rates on leasing agreements in the aesthetic device industry. Mizrahy's observation that "record interest rates impacted the financing environment" could signal a challenge in maintaining the sales momentum, especially in the U.S. market. This is particularly significant because capital equipment sales form a substantial portion of InMode's revenue.

However, there are positives to consider. The company's commitment to innovation and technology upgrades, as indicated by Mizrahy's statement, "We constantly improve and upgrade our technology," positions InMode well for long-term industry leadership. This is reinforced by their strategy to "aggressively enhance and protect our IP and patent," which could be a significant moat against competition.

The geopolitical situation in Israel, where InMode is based, is also a factor. While current operations seem unaffected, as per Mizrahy's reassurance, any escalation could potentially disrupt production, although the company appears to have contingency plans in place.

Lastly, the performance in different global markets varies, with regions like Asia still showing strong demand. This diversification of market presence could buffer against regional downturns.

In conclusion, while InMode's strong commitment to innovation and global expansion presents a positive outlook, factors like market seasonality, high interest rates affecting sales, and potential geopolitical risks suggest a cautious approach. Balancing these dynamics, I maintain a 'hold' position, keeping a close eye on how these factors evolve in the near future.

Risks

One of the key financial challenges for InMode are the effects of highly charged interests. The company has suffered increased costs of operation and slow revenue growth due to longer leasing agreements and extended sales cycles. This situation becomes even more critical as they are a company that almost entirely runs on an equipment leasing basis. High interest rates may lead to reduced equipment sales, which is a major part of InMode’s revenue.

My uncertainty is also fueled by geopolitical factors. InMode operates within Israel and is liable to political developments within the region that may jeopardize investor confidence or undermine its operability. Stock volatility is prevalent during such geopolitical tension coupled with the revision of 2023 revenues forecasts, which was caused by slow growth.

One other element of risk which can be associated with InMode is that it is very niche focused. It is an advantage and at the same time a challenge when a company specializing in a radiofrequency microneedling technology is using the cosmetic application for solely these purposes. Therefore, InMode is vulnerable to fast-changing market tendencies, consumers demand/preferences, and breakthrough competitor technologies.

Lastly, InMode faces a sluggish seasons. Due to the high interest rates that contributed to the reduction of purchasing power for the company’s equipment buyers, we then observed the projected 2023 revenues being lowered by management. This highlights the challenges the company faces in maintaining growth momentum in the competitive and constant changing cosmetic medical sector?.

All in all, there are significant challenges in the form of high-interest rates, geopolitical factors, niche market risks, and seasonal fluctuations, which contribute to the uncertainty and support my personal view of a 'hold.'

Valuation

To begin with, the Forward Price to Earnings (P/E) Non-GAAP ratio stands at 9.04 , which, when placed against a sector median of 18.58, paints InMode as undervalued. This lower P/E ratio, which comes with a Seeking Alpha grade of 'A', might typically signal a buying opportunity, suggesting that the stock could be a bargain relative to its earnings potential. However, the -51.36% change reflects significant investor skepticism or an expectation of decreased earnings. This juxtaposition creates a complex narrative: the stock seems affordable, yet there's a cloud of uncertainty about future growth, justifying my 'hold' stance.

Moving onto the Forward Price to Sales (P/S) ratio, we see a figure of 3.78 with a 'C+' grade from Seeking Alpha. While this is slightly below the sector median of 3.95%, it doesn't indicate the same level of undervaluation as the P/E ratio. This suggests that while InMode is generating sales, the market isn't valuing these as highly as other sector companies. It's not enough to compel a buy, but it's not so out of step with the sector to warrant a sell either.

Lastly, the Forward Price to Book (P/B) ratio is 2.40, which is virtually in line with the sector median of 2.45 and has been given a 'C+' grade. A P/B ratio close to the sector median indicates that the market is valuing InMode's assets in harmony with its peers. The slight underperformance of -2.12% is not alarming as it suggests INMD is on par with comparative companies.

These metrics collectively suggest that InMode's stock is priced reasonably in terms of sales and assets but is potentially undervalued when it comes to earnings. In the context of my 'hold' thesis, these figures bolster a cautious approach. The forward-looking nature of these metrics underscores the importance of potential growth and profitability, which are not entirely convincing in InMode's case. The stock isn't exorbitantly priced relative to its peers, but it isn't a standout bargain either. It's this middle-of-the-road positioning, coupled with the backdrop of the broader market uncertainties, that anchors my decision to hold.

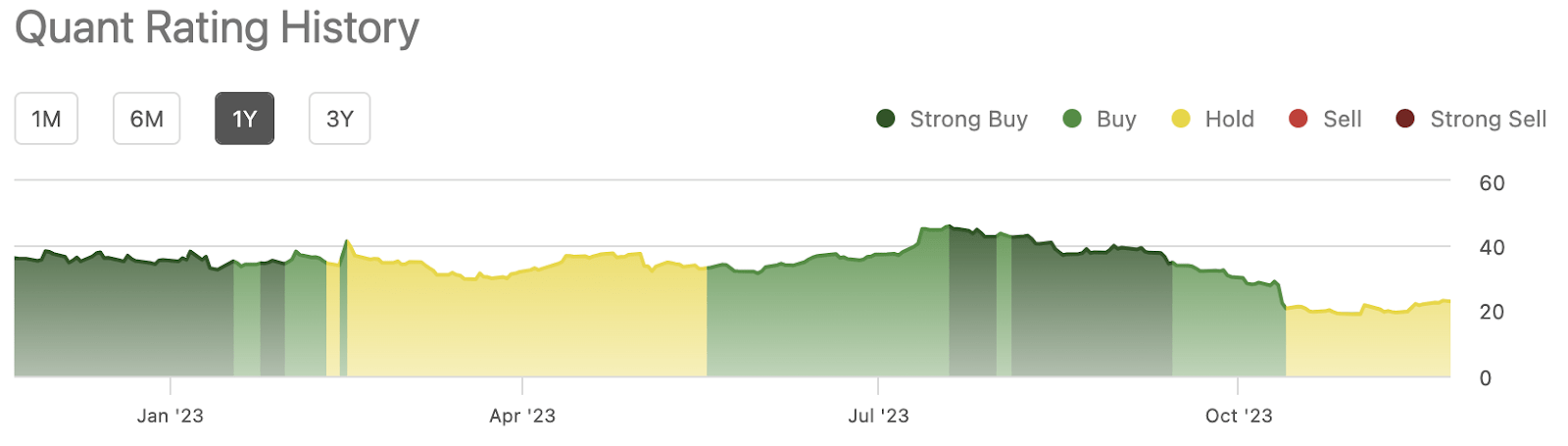

Additionally, to further my argument, below I have attached the Quant Rating score of 2.53 which aligns with my hold thesis. This Quant Rating has recently been assigned a little over a month ago, as viewed in the rating history figure, illustrating the adjusted score of INMD promotes an uncertain outlook.

Quant Rating (Seeking Alpha) Quant Rating History (Seeking Alpha)

{kind=link}

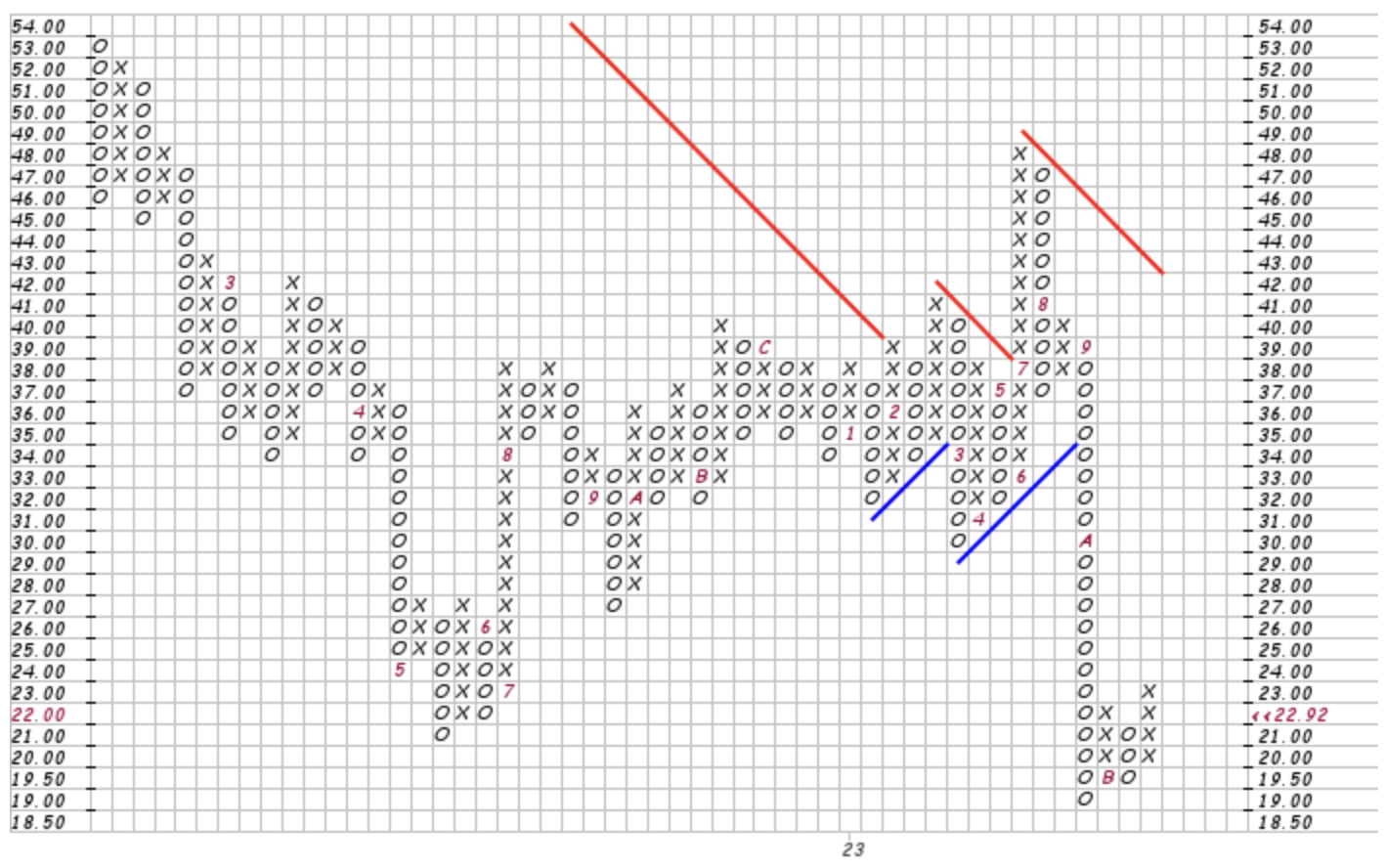

Following, according to the following graph I have provided below, a point and figure chart in a traditional 3 box reversal method, I see INMD in an uncertain position. If we bring our attention to the bottom right section of the figure, the support level is at 19.50, which is currently three dollars under the stock price. Therefore, in my opinion, I could see a 3 box reversal in the near future and observe the stock testing the support-line. From that point going forward is totally up for debate. If the stock breaks through the support line then the price could fall much lower based on this method, but if the support is held at 19.50 then a green light will be flashing for potential upside. Due to this uncertainty, I heavily emphasize a ‘hold’ rating as I will be standing on the sideline for now.

INMD Point & Figure (Stock Charts)

{kind=link}

I also wanted to mention that based on 2023 financials, the medical aesthetics market is estimated to be valued at about $15.4 billion (based on revenue). The outlook of the market value is approximated to reach $25.9 billion by 2028. For InMode this is encouraging, if in-fact they can continue to increase their market share, which is very possible based on current products and innovative techniques.

In a wholistic view that includes forward-looking valuation metrics, comparisons to sector medians, graph technicals, and supportive Quant Scores, I believe an attractive entry point would be in the price range of 20.00-20.75. I do not necessarily believe there is a specific price for InMode that I would avoid the stock altogether, but I think a deeper value, marked by my specified range, would offer major upside in the long-term.

Conclusion

In my analysis of InMode Ltd. I find the company at an intriguing juncture. While their innovative minimally invasive technologies and global presence position them well for long-term growth, modest revenue increases and rising operational costs necessitate a cautious investment approach. The company's diverse global footprint and strong technology portfolio position it well for long-term growth. Yet, external factors like economic conditions and high interest rates pose challenges to immediate profitability. InMode's management has demonstrated adaptability and strategic foresight, particularly in navigating these challenges and investing in growth. My 'hold' stance is reinforced by the market's projected growth and InMode's capacity to expand market share, tempered by the need to navigate economic challenges and competitive dynamics. As an investor, I recommend a vigilant, balanced view, focusing on InMode's product innovation and strategic responses to market fluctuations.

For further details see:

InMode: A Deep Analysis Into Its Mixed Picture