INMD - InMode: A Laser-Focused Investment Opportunity

2023-07-18 10:59:50 ET

Summary

- I discuss the investment potential of InMode, a company specializing in laser equipment for aesthetic medicine treatments, which has seen significant growth and offers high growth prospects with attractive profit margins.

- My analysis of InMode's business model, competitive position, and intrinsic value suggests it is a strong investment opportunity, with a unique market position, protected by patents, and negligible debts.

- I conclude that despite the inherent uncertainties of any investment, the strong financials and market position of InMode make it a promising addition to their main portfolio.

I've always been fascinated by Peter Lynch's idea of deriving investment clues from everyday experiences. A few days ago, while chatting with a doctor specializing in aesthetic medicine, we veered onto the topic of laser treatments. This category of treatments has seen enormous growth over the past decade for several reasons: it's significantly cheaper than surgery, less invasive, delivers tangible results, doesn't require an operating room, and can be performed in the time it takes for a lunch break.

My conversant confirmed that laser treatments, along with botox injections, are now the most sought-after in his practice. He provided me with one particular name to focus my research on: InMode ( INMD ). As a diligent investor, I wasted no time in conducting due diligence. The result was striking: a company that has seen extraordinary growth over the years, offers high growth prospects combined with very attractive profit margins, and has almost negligible debts.

Just a cursory glance at the financial information and data was enough for me to consider this stock a potential 'buy'. I was able to confirm this instinct by constructing a Discounted Cash Flow model, which I present here as the central point of my analysis.

The InMode Business Model

InMode is a company specializing in laser equipment for aesthetic medicine treatments, founded in 2008 and headquartered in Israel. The convenience of laser treatments, from an economic standpoint and in terms of patient recovery time, coupled with visible results, has led to a strong, global surge in market demand over time.

The equipment is purchased or leased by doctors who can then use them in their clinics without needing to reserve an operating room. Normally, a single doctor, with no need for nurses or other personnel, can perform the procedures on a patient.

InMode focuses on the design and marketing of laser equipment. The manufacturing is assigned to outsourced suppliers, to whom InMode pays a fixed price per unit. This strategy makes the company's operational cost structure flexible and predictable. The management team comprises professionals with at least 15 years of experience in this field, who previously worked for InMode's main competitors (Syneron Candela and Cynosure).

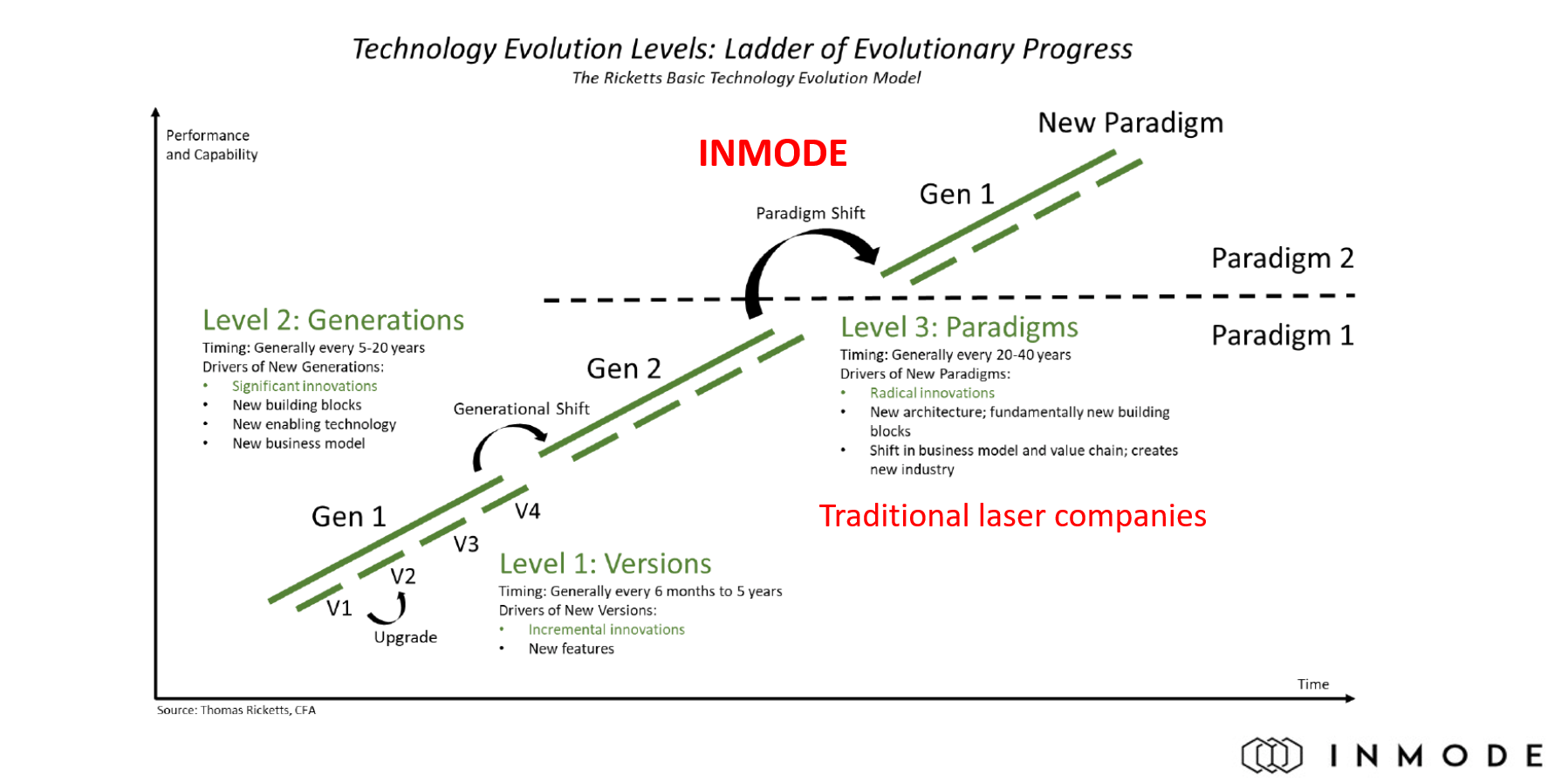

The market for aesthetic medicine laser equipment operates on three cycles:

-

New versions of the same product every 6-12 months, which are improved versions of the existing technology;

-

New generations every 5-20 years, which lead to better and more effective use of the technologies deployed in the previous version;

-

New paradigms every 20-40 years, bringing radical technological innovations to the functioning of laser equipment.

Nobody knows for sure which company will win the race for the next paradigm shift in laser technology applied to aesthetic medicine. However, with current technologies, InMode establishes itself as a leader capable of creating more advanced products than its competition and providing a broader range of solutions.

{kind=link}

InMode Q1 2023 Investors Presentation

InMode's Competitive Position

InMode's main competitors are Syneron Candela, Cynosure, Solta Medical, Lumenis, and Cutera. These companies focus on laser equipment that can be used for non-surgical treatments, such as permanent hair removal or facial rejuvenation. Their strength lies in leveraging the convenience of laser technology to offer solutions that do not require operating rooms, surgeries of any kind, and can be performed in a minimal amount of time.

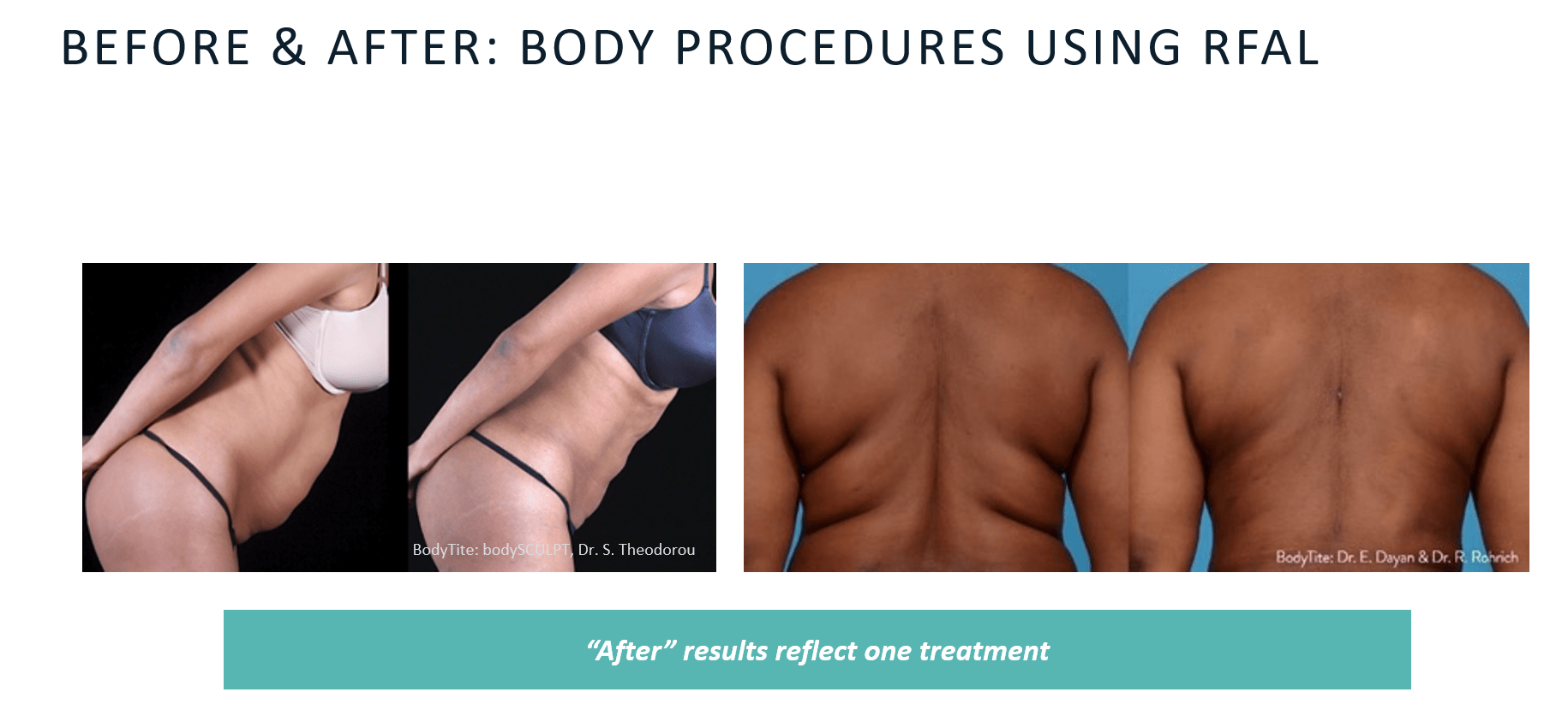

InMode occupies a unique position within this market. Only 2 of the 9 products in the company's portfolio are 'traditional' lasers. The other 7 products utilize one of the two main proprietary technologies developed over more than 250,000 manhours of R&D ( as of Q1 2023 ):

-

5 make use of the RFAL technology, invented by InMode, which is useful for providing minimally invasive or ablative surgery treatments. This means more noticeable and quicker results than treatments that do not involve any aspect of surgery, as well as a faster recovery time from the procedure compared to traditional surgery;

-

2 use hands-free technology that allows the doctor to leave the machinery to operate on the patient without having to manually use it. This enables covering larger areas, reducing the training time needed for machine usage, and streamlining the patient's treatment process.

In this way, InMode positions itself uniquely compared to its competitors and offers products that meet different needs.

Market positioning is also protected by 4 patents. InMode's most advanced lasers include 2,800+ components, creating a technological barrier that prevents competitors from easily entering the same market. Furthermore, even though official data is not available because they are mostly unlisted companies, based on available information, InMode does not face players with significantly larger market shares or revenues.

{kind=link}

InMode Q1 2023 Investors Presentation

Calculating the Intrinsic Value of InMode

The main point in favor of my rating is the calculation of the intrinsic value of this company. This is a company that has already gone through its exponential growth phase and is already profitable; therefore, it's perfectly suited to valuation via DCF.

I have projected InMode's numbers up to 2029, after which I used the terminal value to estimate the company's value from that point onward. Future cash flows are discounted based on the WACC, for which I will also provide the calculation.

Assumptions Used in the Model Construction

The fundamental assumption for constructing the discounted cash flow involves revenues. InMode has shown strong revenue growth over the years, but the growth rate is slowing down as the company is saturating the TAM. If we exclude the 2020-21 period, the growth rate is following a quite evident trajectory; in 2020 the company sold less due to the pandemic, and in 2021 it sold more due to the recovery of orders not received the previous year. Normalizing the numbers based on this hypothesis, I simply built a curve showing the slowing growth rate and estimated revenues for the coming years.

The only exception is the revenues for 2023, on which the company has recently revised its estimates upwards . In this case, I simply used the estimates provided by management.

The other important assumptions for projecting the balance sheet numbers for the coming years are as follows:

-

The net income/revenue ratio has consistently remained in the 35-40% range over the years, so I used it as a reference for forecasting net income for the coming years;

-

The D&A value shows a strong correlation with revenues, so I used this value as a reference. For each projected year, the value associated with D&A is based on the average D&A/revenue ratio of the previous 4 years. The same method is used to calculate the change in net working capital;

-

CapEx has always remained roughly stable around 0.35% of revenues, even considering that production is outsourced. For this reason, I simply assumed that it will continue to be around 0.35% of revenues in the future. The assumptions related to the company valuation method, on the other hand, are as follows:

-

I used the average beta of the last 5 years for the WACC calculation;

-

For the terminal value calculation, I considered a multiple of 14x of the net income of the last projected year. This is quite a conservative estimate compared to major medical equipment manufacturers.

WACC and Discounted Cash Flow Analysis

Based on this, the WACC calculation is as follows:

| WACC |

| Total debt |

| 3,307,000.00 |

| % debt |

| 0.09% |

| Cost of debt |

| 5.50% |

| Tax Rate |

| 9% |

| Equity |

| 3,734,868,037.00 |

| % Equity |

| 99.91% |

| Cost of Equity |

| 10.07% |

| Risk free rate |

| 3.80% |

| Beta |

| 2.09 |

| Risk premium |

| 3% |

| TOT (Equity + Debt) |

| 3,738,175,037.00 |

| WACC |

| 10.07% |

Moving on with the analysis of the DCF:

| 2023 |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| 2029 |

| Revenue |

| 535 |

| 659.1 |

| 786.7 |

| 908.8 |

| 1015.0 |

| 1094.6 |

| 1138.4 |

| % growth |

| 17.76% |

| 23.20% |

| 19.36% |

| 15.52% |

| 11.68% |

| 7.84% |

| 4.00% |

| Net income |

| 210.2 |

| 259.3 |

| 315.3 |

| 350.5 |

| 399.1 |

| 430.5 |

| 447.6 |

| % revenue |

| 39.29% |

| 39.34% |

| 40.08% |

| 38.56% |

| 39.32% |

| 39.33% |

| 39.32% |

| D&A (+) |

| 0.7 |

| 1.08 |

| 1.33 |

| 1.50 |

| 1.63 |

| 1.79 |

| 1.88 |

| % revenue |

| 0.17% |

| 0.16% |

| 0.17% |

| 0.17% |

| 0.16% |

| 0.16% |

| 0.17% |

| CapEx -ì(-) |

| -1.9 |

| -2.3 |

| -2.8 |

| -3.2 |

| -3.6 |

| -3.8 |

| -4.0 |

| % revenue |

| -0.35% |

| -0.35% |

| -0.35% |

| -0.35% |

| -0.35% |

| -0.35% |

| -0.35% |

| Delta NWC (-) |

| 15.2 |

| 11.2 |

| 10.2 |

| 9.1 |

| 13.9 |

| 14.7 |

| 14.3 |

| % revenue |

| 1.49% |

| 1.70% |

| 1.29% |

| 1.00% |

| 1.37% |

| 1.34% |

| 1.25% |

| Unlevered FCF |

| 193.8 |

| 246.9 |

| 303.7 |

| 339.7 |

| 383.2 |

| 413.7 |

| 431.3 |

| Discounted FCF |

| 193.8 |

| 224.3 |

| 250.7 |

| 254.7 |

| 261.1 |

| 256.1 |

| 242.6 |

Calculating the intrinsic value

Now that we have a forecast of the discounted FCF for the upcoming years, let’s calculate the terminal value, the present value of the terminal value and put everything together.

| INTRINSIC VALUE CALCULATION |

| Sum of DCF 2023-29 |

| 1,683.40 |

| Terminal Value ((TV)) |

| 6266.8 |

| Present value of TV |

| 3,202.47 |

| Debt (-) |

| 3.30 |

| Cash (+) |

| 93.00 |

| Intrinsic Value |

| 4,975.58 |

It can be interesting to note how all of this translates into potential upside for the stock:

| Mkt cap today |

| 3,740.00 |

| Calculated intrinsic value |

| 4,975.58 |

| Stock Price today |

| $45.02 |

| Intrinsic value of the stock |

| $59.89 |

| Upside (downside) potential |

| 33.04% |

All this, of course, bearing in mind that the analysis does not present any particular positive catalysts, that the multiples used for the terminal value calculation are conservative, and that the company could acquire some of its smaller competitors. Based on all this, I feel there's a good safety margin to invest in InMode.

Conclusions and Final Considerations

I wouldn't have thought that a simple chat with a friend could lead to such an interesting investment idea. InMode is a company with stellar margins on sales (83-85%), capable management, and a highly competitive market position. Most importantly, though, I was convinced by the numbers analysis: no DCF can be 100% accurate, but with such a large safety margin, I'm not at all scared by the idea of investing in InMode.

I also believe that it's not an 'intriguing gamble,' as was the case with my latest analyses on Terran Orbital and Ouster . InMode is a well-established, highly profitable company with a very clear target market. For this reason, I intend to give it a space in my main portfolio, not among the side-bets. In a market that is fearful and undervaluing many mid-cap companies, I'm finding many interesting opportunities among companies with a market cap under $5 billion.

For further details see:

InMode: A Laser-Focused Investment Opportunity