INMD - InMode: Despite Attractive Valuation I Believe It's Premature To Dive In - Here's Why

2024-01-03 03:16:23 ET

Summary

- InMode has a depressed valuation with a forward P/E of 8.70 in 2024.

- The company is facing challenges with falling revenue and EBITDA, despite being highly profitable.

- The weakening of Covid pent-up demand adds an interesting layer to the investment landscape.

- Despite the traditionally robust Q4 seasonality argument, a surprising twist emerges - InMode's management expresses a lack of confidence in the quarter's strength.

Editor's note: Seeking Alpha is proud to welcome Invest Wise as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

InMode Ltd. ( INMD ) recently surfaced in my investment screener, catching my attention as an attractive opportunity for 2024. As we approach the new year, the prevailing market trend sees elevated valuations for resilient and growth stocks. In light of this, I advocate adopting a "Buy High, Sell Higher" strategy, a concept familiar to readers of Joe Terranova's insights. Implementing this strategy requires foresight and planning, and for 2024, InMode is a key player in my investment playbook.

Despite the stock's appealing valuation, I exercise caution, recognizing that the opportune moment to initiate a position has not yet arrived. My approach involves a comprehensive analysis, integrating macroeconomic trends, fundamental indicators, and technical analysis to pinpoint the optimal entry point for this investment. Importantly, I emphasize the need to preserve capital by refraining from boarding the "train" if conditions aren't conducive to a profitable journey. Hence, I am assigning a "Hold" Rating for now.

Introduction

InMode stands as a pioneering force in the realm of innovative medical technologies, carving a niche as a global leader. The company is dedicated to the development, manufacturing, and marketing of devices centered around novel radio-frequency ((RF)) technology. InMode's mission is to usher in minimally invasive procedures and enhance existing treatments across various medical disciplines, including plastic surgery, gynecology, dermatology, otolaryngology, and ophthalmology.

At the forefront of InMode's offerings is a breakthrough skin rejuvenation device, designed for individuals seeking smoother and more youthful skin. This cutting-edge medical device, characterized by adaptable applicators, facilitates a range of facial and body enhancements through minimally invasive techniques. The outcomes include reduced scarring, minimal downtime, lower costs, fewer potential risks, and expedited results.

InMode takes pride in its innovative, all-in-one approach to cosmetic treatment and care, addressing a spectrum of aesthetic concerns, from loose and sagging skin to unwanted body hair. The company's commitment to providing advanced solutions is underscored by a comprehensive line of technologies, offering minimally invasive and non-invasive body and facial rejuvenation treatments.

Decoding InMode In The Macro Landscape

INMD's revenue decline that helped the stock to drop to this attractive valuation is due to three reasons as per the management. They are as follows:

The management attributes InMode's Q3 revenue drop to the unique seasonality of the medical aesthetics industry. Traditionally, Q3 tends to be a slower quarter due to the summer season when individuals are hesitant to undergo treatments while on vacation. However, the abnormal strength in Q3 during 2021 and '22, influenced by the early-year impact of the COVID pandemic, created an atypical trend. This deviation from the norm has contributed to the perceived decline in InMode's stock value.

The second reason is linked to financing concerns. With leasing costs ranging from 14% to 15% annually, resembling interest rates that one would avoid for a mortgage, there's a hesitation among doctors. Despite the machinery's revenue-generating capability, the extended return on investment period at such high interest rates becomes a deterrent. The broader economic slowdown adds to the uncertainty, as rising interest rates, currently at 14% to 15% for leasing financing, prompt doctors to rethink their investment decisions.

The third reason is the tightening procedures and screening by leasing companies. Fearing potential doctor bankruptcies, these leasing firms now subject purchase orders to an extended processing time, often spanning two to three weeks. This prolonged period opens the door for competitors, creating a scenario where doctors reconsider their decisions, contemplating a delay in their purchasing decisions.

In light of the three reasons outlined by the management and their potential impact, my macro outlook for 2024 positions these factors within a broader economic context. The anticipated macro environment, characterized by expected interest rate cuts and a loosening of credit conditions, aligns with the challenges outlined by the management.

For the first reason, the unique seasonality in the medical aesthetics industry, the market is urged to acclimate to this pattern. Assuming the company's accuracy in predicting a reflection of this seasonality in Q4 earnings, it becomes a factor to watch. Moreover, the loosening macro conditions and potential rate cuts , estimated conservatively by me at 3-4, could act as a tailwind, mitigating the impact of the atypical seasonality.

In the realm of financing (the second reason), the expected interest rate cuts are a crucial variable. With financing costs currently at 14% to 15%, a reduction in interest rates could alleviate the hesitation among doctors, making the return on investment more favorable and potentially accelerating decision-making.

Regarding the third reason, the tightening procedures and screening by leasing companies, efforts outlined by InMode management in the Q3 earnings call, and a more accommodative macro environment may streamline the processing time for purchase orders. The reduced processing duration could minimize the window of opportunity for competitors and, in turn, positively influence doctors' decisions.

In conclusion, while the outlined challenges are present, the macro outlook for 2024, featuring interest rate cuts and a more lenient credit environment, suggests potential tailwinds for InMode. The interplay of these factors invites cautious optimism, considering the company's positioning within the evolving economic landscape.

Decoding InMode Fundamentals

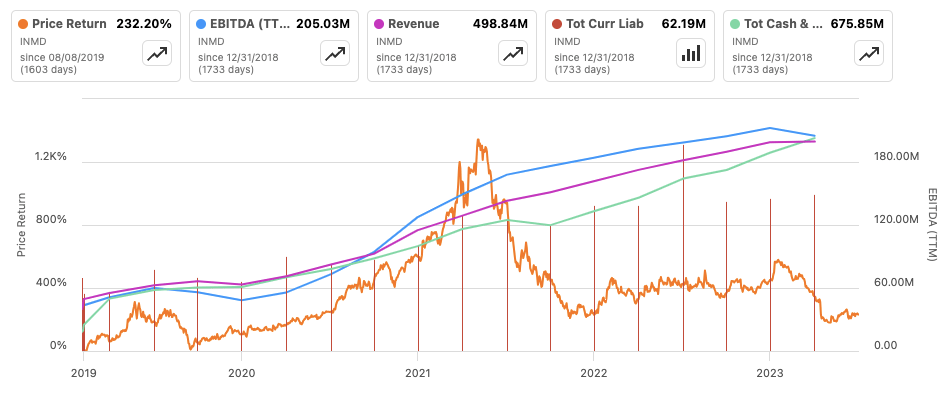

InMode boasts a robust balance sheet , flaunting $678 million in cash & ST Investments against a mere $70 million in total liabilities. As a highly profitable company, it maintains a targeted gross margin of 83-85%, supported by a substantial 15% in recurring revenue from consumables - a segment less prone to cancellations.

InMode - Fundamentals (Seeking Alpha)

{kind=link}

As evident from the SA Chart above, Q3 2023 experienced a decline in both revenue and EBITDA growth, contributing to the decreased stock price. This pattern is typical for growth stocks, where a slowdown in growth often leads to a significant drop in stock value. Q3 Revenue of 131M registered just 2% YoY growth, but 9% QoQ decline. EBIDTA of 46.5M registered a 13.6% decrease in YoY growth.

However, amidst these challenges, it's crucial to note the positive indicators. The company's Total Cash and short-term investments have risen to 675 million, signaling financial strength. Additionally, the Consumables and Service segment exhibited robust growth, marking a noteworthy 28% YoY increase. This growth underscores the recurring nature of consumables and sustained demand for ongoing treatments.

It's important to highlight that the revenue contribution from Envision, the latest ophthalmic treatment, is anticipated to commence from Q4 2023 onwards. This noteworthy development is expected to positively impact the company's financials starting in the fourth quarter.

Valuation

In assessing InMode as a growth stock, attempting to determine an intrinsic value appears futile. Therefore, I employ a relative and PEG ratio analysis. Relative to its industry peers, InMode is currently deemed considerably undervalued. The forward P/E of 8.70, in contrast to the sector's median of 18.5, presents an appealing valuation. Management's guidance for 2023 anticipates revenue of 505 million and non-GAAP EPS of 2.55.

The 2023 estimated EPS of 2.47 indicates a modest 2.1% growth rate, resulting in a PEG ratio of 4%. This higher PEG ratio, influenced by the declining rates of both Revenue growth and EPS growth, is not very appealing. However, the potential for a return to growth mode becomes more plausible with the improving macroeconomic situation. The anticipated macroeconomic improvement introduces a hopeful outlook for the company, suggesting the possibility of a positive shift in its growth trajectory.

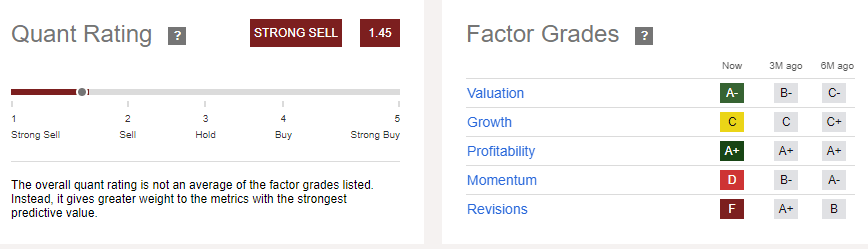

Seeking Alpha Quant rating currently gives InMode a strong sell rating with the below Grades.

{kind=link}

Quant rates InMode as A- for Valuation and A+ for Profitability. However, it's crucial to note that the strong sell rating is primarily influenced by earning revisions and stock momentum. These factors, though currently negative, have the potential to reverse if the company successfully regains its growth trajectory within a favorable macroeconomic environment.

If InMode can reignite its growth, considering the sector median P/E of 18.5 and a 5-year average P/E ratio of 23, the fair value of InMode should surpass $45. This presents a substantial upside, exceeding 100% of its current valuation.

Despite its financial strength and compelling valuation, The CEO's response during the Q3 Earnings call to questions on the source of the slowdown adds a layer of uncertainty, highlighting the challenge of pinpointing the exact contributors to the economic downturn. This lack of clarity, combined with the current macro situation, prompts a cautious stance.

Moreover, the management's commitment to maintaining expenditures, despite the challenging landscape, raises concerns. While they are doubling down on marketing, sales promotion, and R&D, the reluctance to cut costs amid uncertainty about 2024 projections may intensify investor apprehensions. The CEO's assurance of retaining and hiring personnel, while admirable, poses a potential risk as the company navigates a period of economic uncertainty.

Adding to the complexity, the management's seeming lack of appreciation for the benefits of stock buybacks as a means of returning capital to shareholders raises eyebrows. Instead, their focus on M&A activities, potentially non-synergistic acquisitions, introduces an additional layer of risk to the company's future outlook. Investors may be wary of the potential repercussions of this strategic direction, emphasizing the need for a more comprehensive understanding of capital allocation strategies.

InMode's Technical Landscape: Chart Patterns And Key Indicators Unveiled

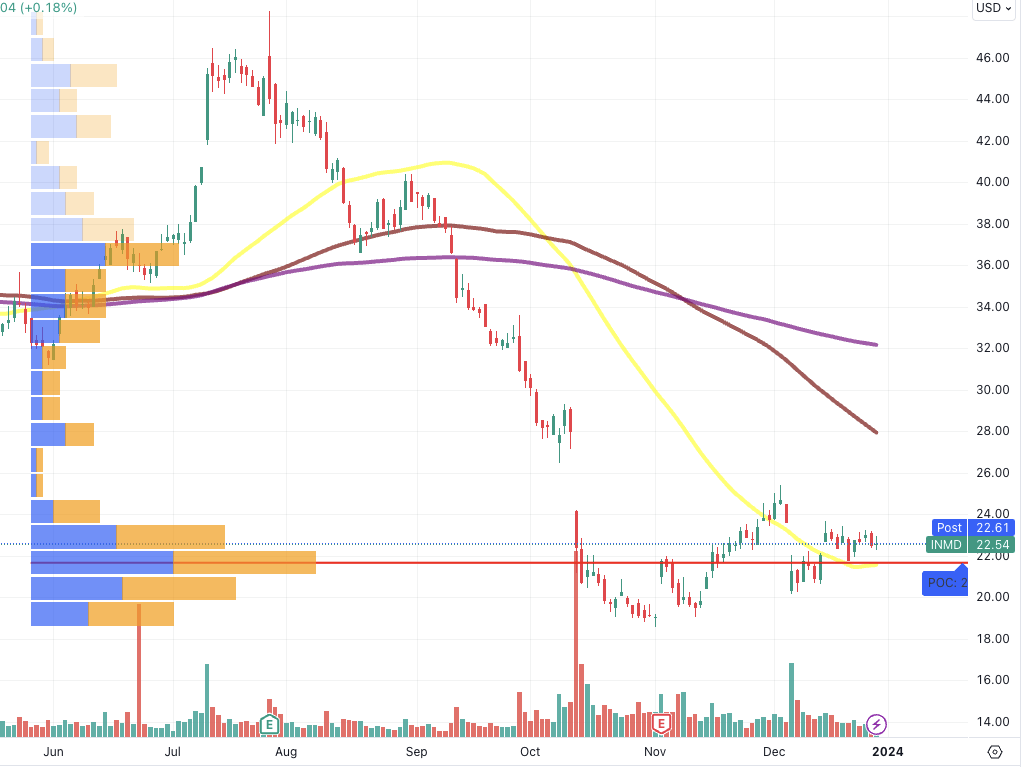

As we examine the technical setup for InMode, the volume profile suggests a possible consolidation phase at current levels. However, a closer look reveals a stock positioned below its 200-day and 100-day moving averages, with only a precarious perch just above the 50-day moving average.

InMode - Technical Setup (TradingView)

{kind=link}

While the 50-day moving average provides some support, it's crucial to juxtapose this technical analysis with the broader fundamental and macroeconomic context. In the long term, stocks typically align with fundamentals, yet the current unclear management outlook for 2024 complicates the assessment.

The absence of short-term catalysts and the unresolved 2024 outlook urge a cautious stance. Following a 'buy high and sell higher' strategy, the emphasis shifts to awaiting a substantial improvement in both the macro and fundamental aspects. Capital preservation emerges as the primary objective, even if it means potentially missing the initial surge in the stock. I advocate a conservative approach for 2024 acknowledging the market's overbought condition in the short term and advocating a measured and strategic investment strategy.

Risk To My Thesis

My investment strategy is a fusion of macroeconomic analysis, company fundamentals, and technical analysis, prioritizing capital preservation as the primary objective. With this approach, I perceive minimal investment risk. However, there's a potential scenario where the stock price appreciates significantly while I await confirmation from the indicators mentioned. This situation is inherent to the "buy high, sell higher" approach. Despite the possibility of missing the stock's bottom, this strategy enables effective capital preservation. Simultaneously, closely tracking company fundamentals helps mitigate the risk of buying the stock at unfavorable points, especially when the growth trajectory is unclear.

Conclusion

As I conclude my analysis of InMode, the confluence of factors presents a nuanced picture for investors. Fundamentally, the company showcases resilience with a robust balance sheet, attractive valuation, and a commitment to strategic investments. However, the uncertainties surrounding revenue, EBITDA, and the management's cautious stance introduce a layer of complexity.

On the technical front, the stock's consolidation amidst moving averages signals caution, highlighting the need for a careful blend of technical analysis with the broader economic and fundamental context. The buy high and sell higher strategy underscores the importance of patience, particularly in the face of a market overbought in the short term.

As we traverse the intricate landscape of 2024, a conservative approach becomes imperative, prioritizing capital preservation over immediate gains. While the potential for missing the initial upswing is acknowledged, the focus remains on strategic entries contingent on a substantial improvement in the macro and fundamental outlook.

Looking ahead, specific catalysts become pivotal in shaping the investment landscape. The upcoming Q4 earnings analysis is poised to reveal insights into potential revenue bottoming, providing a critical checkpoint for investors. Additionally, the introduction of Envision, a new ophthalmic treatment, and its revenue mix in Q4 could act as a transformative factor.

Furthermore, investors keenly await any shifts in management strategy, particularly regarding stock buybacks or cost-cutting measures. A change in this regard could significantly alter the stock's trajectory. Finally, the broader macroeconomic scenario, especially confirmation or narrative shifts regarding rate cuts from the Federal Reserve, remains a key determinant in charting the course for InMode.

In essence, the path forward demands a judicious balance, recognizing both the opportunities and challenges inherent in the dynamic interplay of fundamentals, technical indicators, and the unfolding macroeconomic landscape, with a keen eye on these potential catalysts.

For further details see:

InMode: Despite Attractive Valuation, I Believe It's Premature To Dive In - Here's Why