INMD - InMode: Good Margin Of Safety At Current Levels

2024-01-21 03:49:13 ET

Summary

- InMode's stock valuation has fluctuated over time, with high multiples in 2021 due to impressive growth.

- The company's growth has since slowed down as it has matured.

- However, current multiples seem perhaps too punishing, with short-term possible catalysts.

Editor's note: Seeking Alpha is proud to welcome Red Kraken Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

InMode Ltd. ( INMD ) offers, at current levels, a formidable margin of safety as well as key technical support points. While the company has faced headwinds in the last couple of months, I argue why some of them are temporary and why it seems as if the current discount is a bit too steep.

Overview

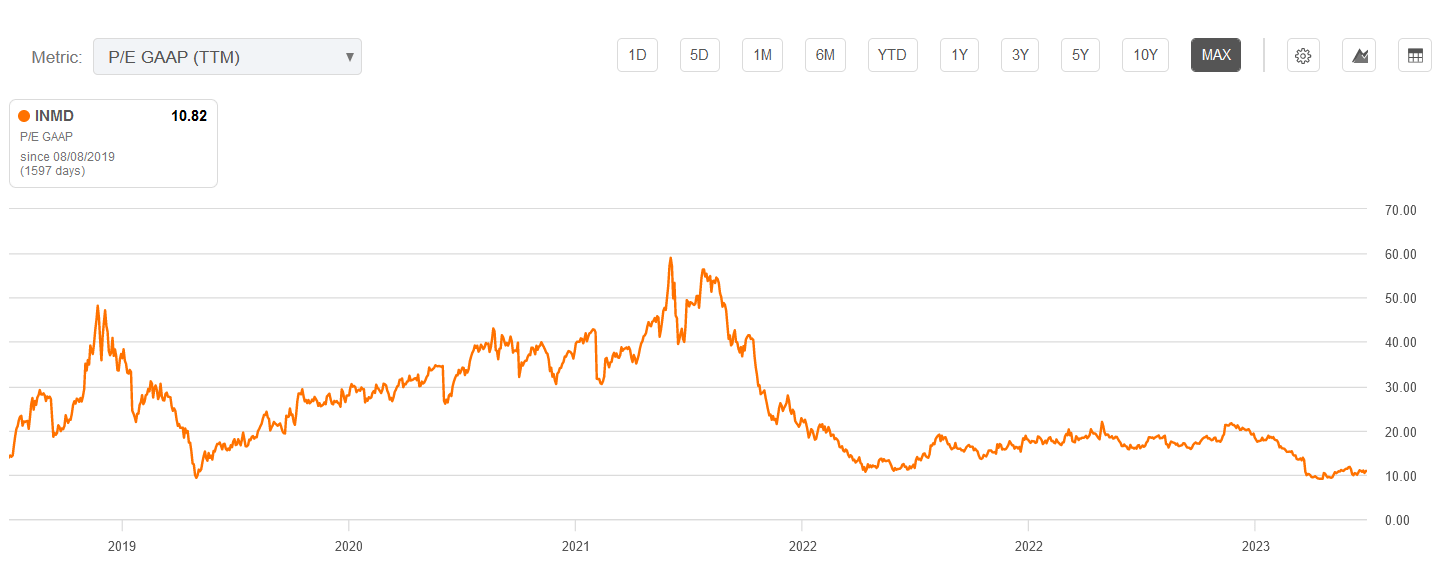

InMode has had its ups and downs in Mr. Market's eyes. Not that long ago, back in 2021, markets were more than happy to pay hefty multiples for the stock, between 30-50 times earnings.

{kind=link}

Naturally, that came from the company's astonishing growth at the time, which has slowed down as it matured.

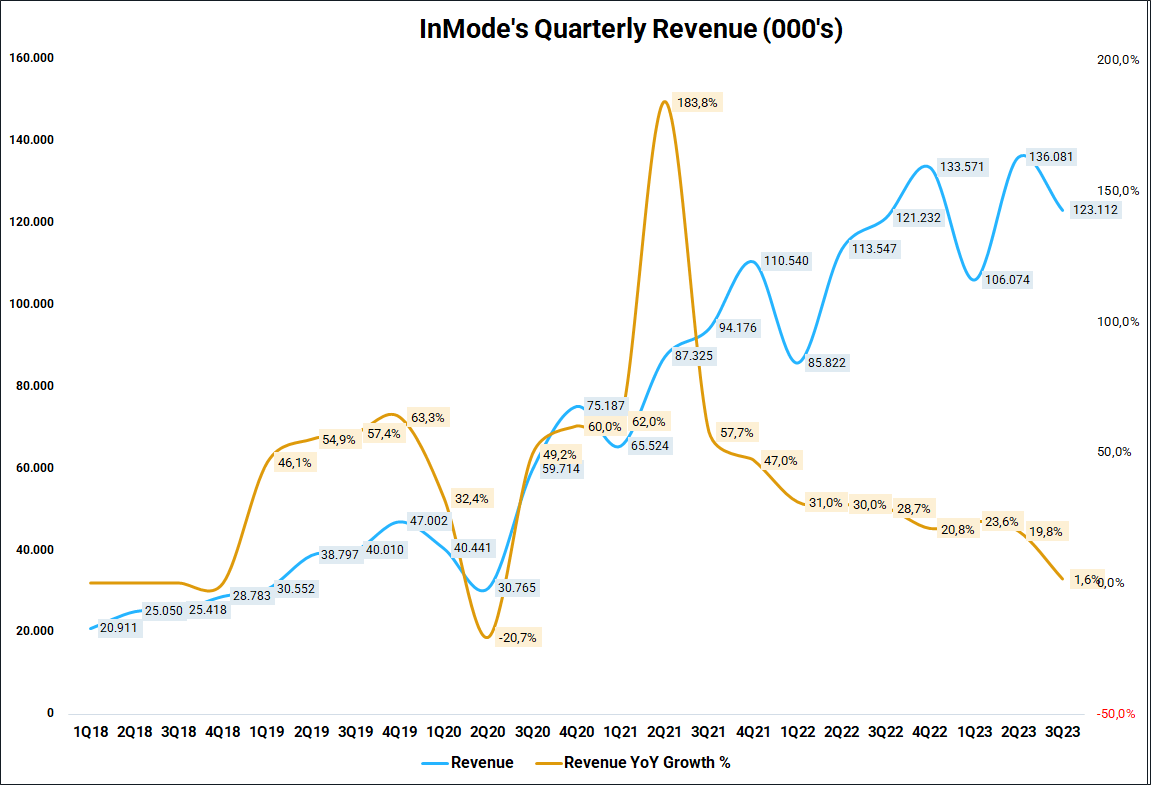

Company's Financials, Author's chart

{kind=link}

Despite the magnificent growth in revenue (blue line), the growth rate slowing down (golden line) has gotten many analysts feeling nervous about the company's prospects. The company also missed 3Q23 analyst estimates - something that hadn't happened since 1Q20.

{kind=link}

In order to understand why and, most importantly, how likely is for this decline to continue, we need to delve a little deeper into the company's products.

What Exactly Does InMode Sell?

I'm not going to waste too much time in here because there have been many recent articles talking about it.

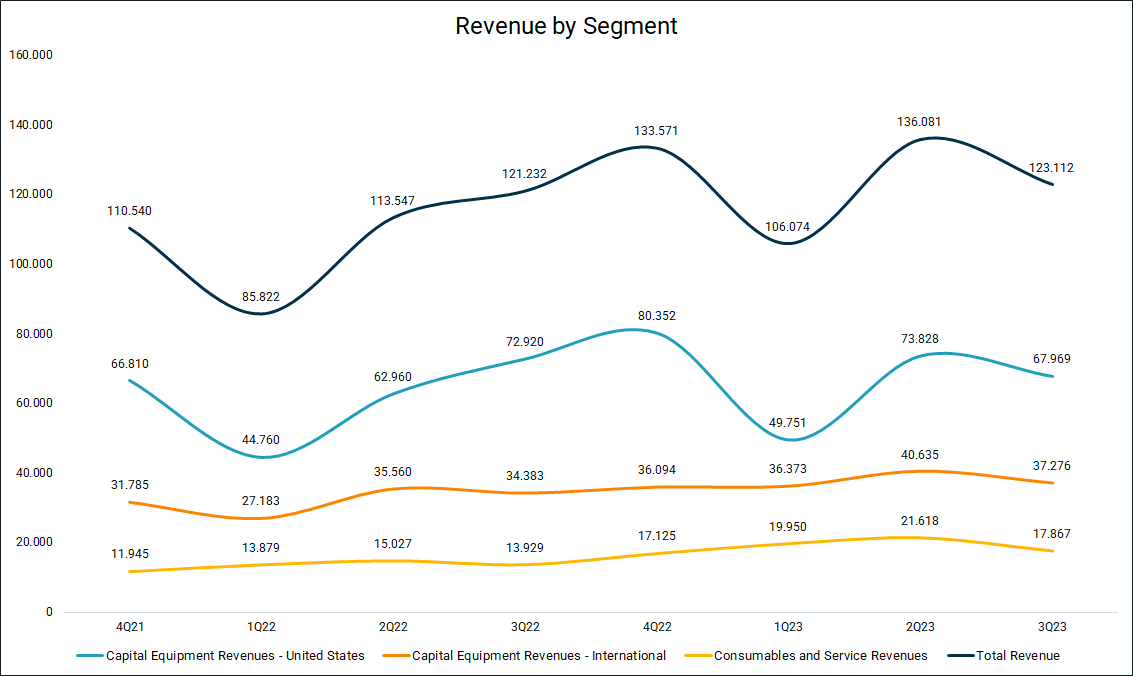

Company's Financials, Author's chart

{kind=link}

Suffice it to say that most of the revenue comes from the light-blue line, which is capital equipment sales in the United States. They've been trying to grow the yellow line - consumables and service revenues - but it still isn't too relevant in the total revenue picture. Orange line (capital equipment revenues outside of the US) has been growing steadily, and it's probably where they can find more room to grow, but it's still inferior to sales in the US.

What do they sell, in case this is your first time reading an InMode article?

These:

{kind=link}

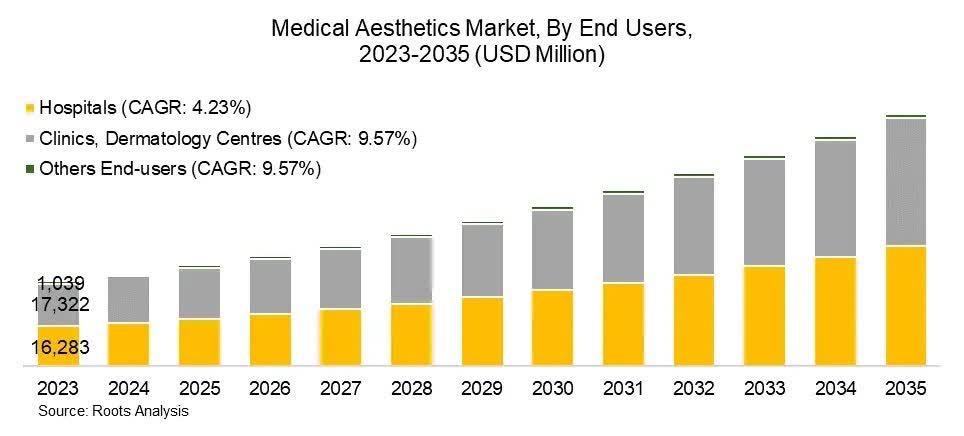

These are radio-frequency, minimally-invasive procedures dedicated to enhancing existing medical, and aesthetic treatments which involve plastic surgery, gynecology, and dermatology, among others. If it sounds too complicated to you, just think of them as non-invasive, skin rejuvenation machines. Customer demand for these types of procedures has been booming in the past few years and it's pretty much consensus that it will continue to do so in the foreseeable future - matter of fact, plenty of people with "Ozempic Face" come for these treatments, so you get the picture. A recent study published by Roots Analysis estimates that the medical aesthetics markets will grow at a CAGR of around 9.3% over the forecast period 2023-2035.

{kind=link}

It's important to note that their sales are often leased by the doctors. Leasing costs (as well as interest rates, obviously) are an important factor to consider. We'll talk more about that later.

Peers

It's tricky to find direct peers to compare InMode's financials. Mostly because it's still a very niche market, with very few competitors being public companies for us to be able to compare multiples. Those that are public companies are micro-caps. Here's a few examples:

HydraFacial - A company using patented technology, focused on skincare treatment. Moshe Mizrahy, InMode's CEO, even acknowledges them as a direct competitor in InMode's Q3 earnings call . It's owned by The Beauty Health Company (SKIN). However, the market cap of the parent company (as of Jan/24) is only around ~$350 mm, very tiny compared to InMode's ~$1.7 bn.

Cutera - Cutera, Inc. (CUTR) provides aesthetic and dermatology solutions for doctors worldwide. Its market cap is even tinier though, at only ~$75 mm.

Candela Medical - Formerly known as Syneron Medical or Syneron Candela (as far as I'm aware, they market themselves as Candela Medical now) offers similar, laser-based technologies that mainly focus on skin rejuvenation. In 2017, the company was taken private by private equity fund Apax Partners, at a $400 mm valuation.

Comparing companies with such massive gaps in market cap is a fruitless endeavor. Therefore, it's best to compare InMode with the rest of the Health Care sector. While not perfect, I think it's the best we can do when it comes to such a niche, small-cap company.

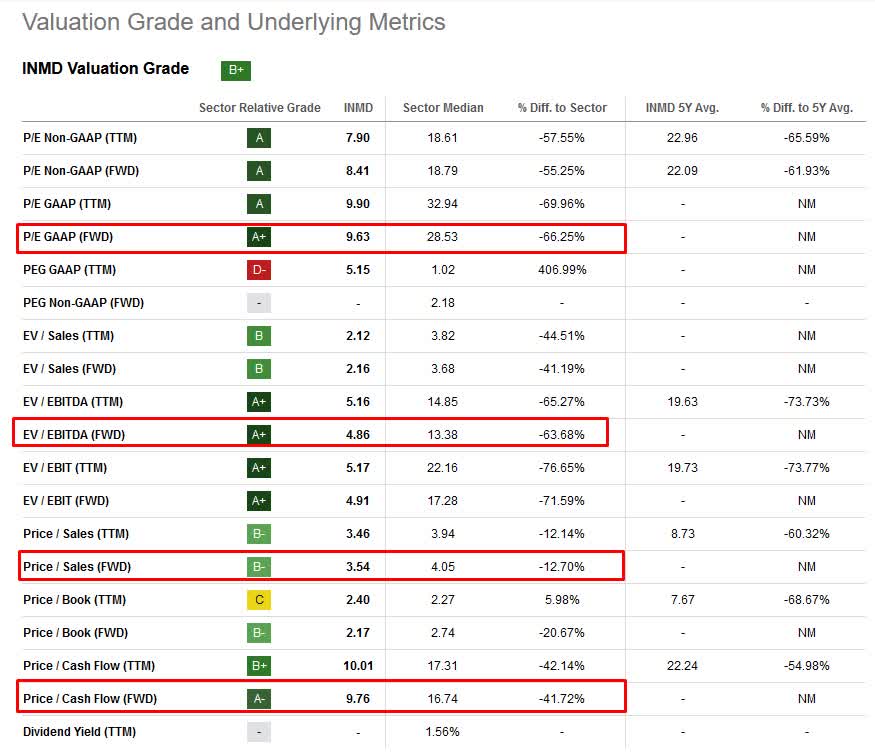

{kind=link}

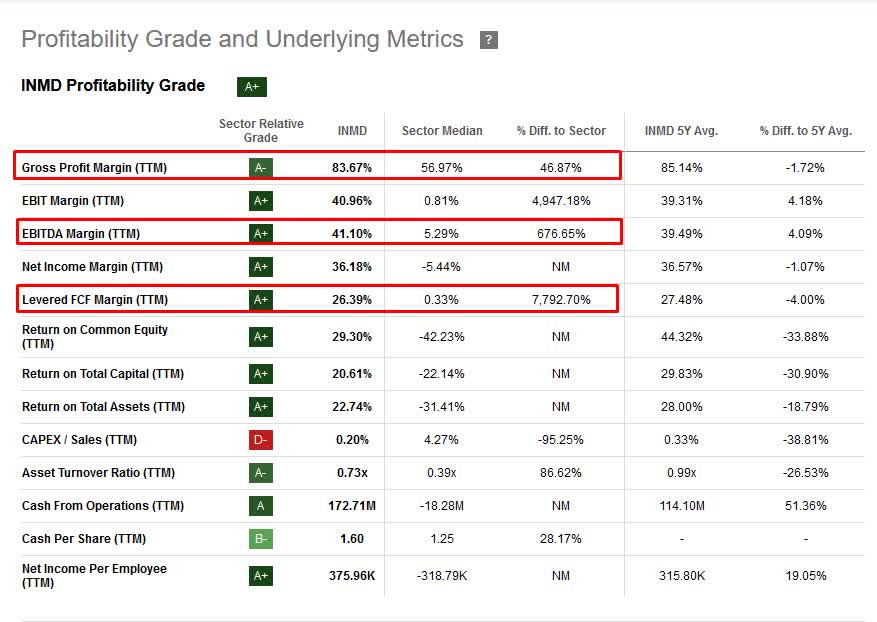

I've highlighted the multiples I look at the most. InMode not only seems to be incredibly cheap - it boosts great margins, as well as strong free cash flow generation.

{kind=link}

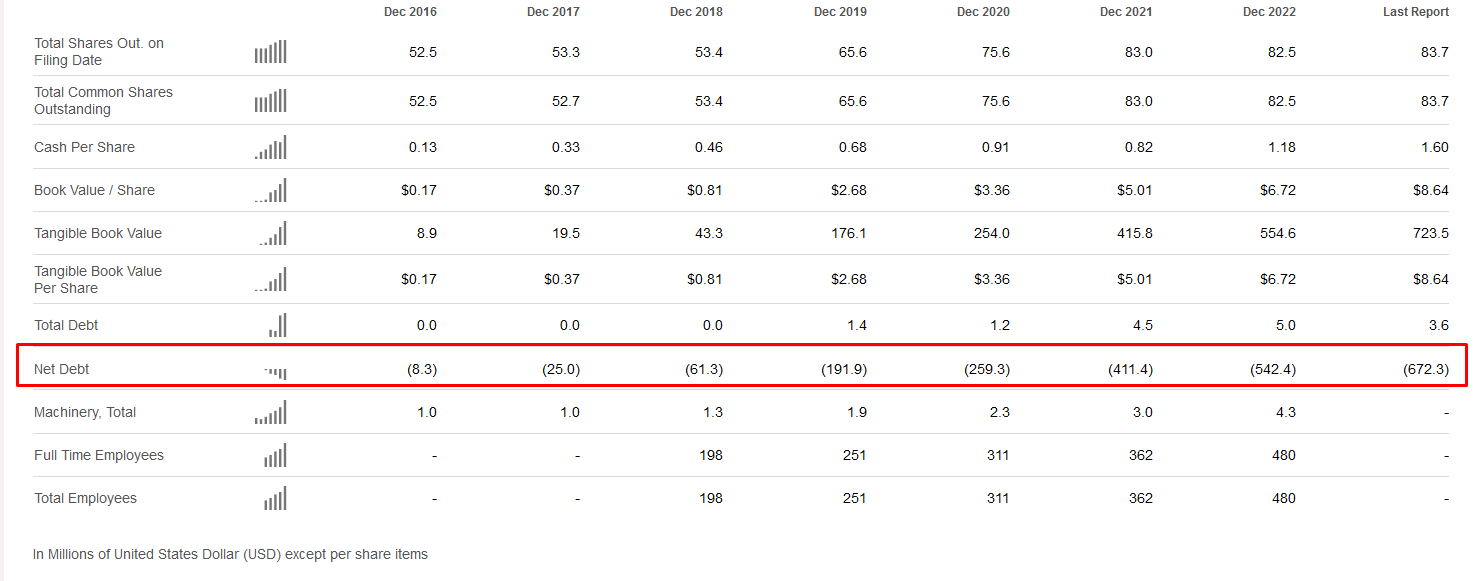

And, to add to all that, InMode's balance sheet is extremely strong, with a net cash position of $672.3 mm as of September 2023.

{kind=link}

No matter what kind of analysis you use, InMode almost always appears undervalued, with strong margins and free cash flow generation, as well as virtually no debt and a pile of cash.

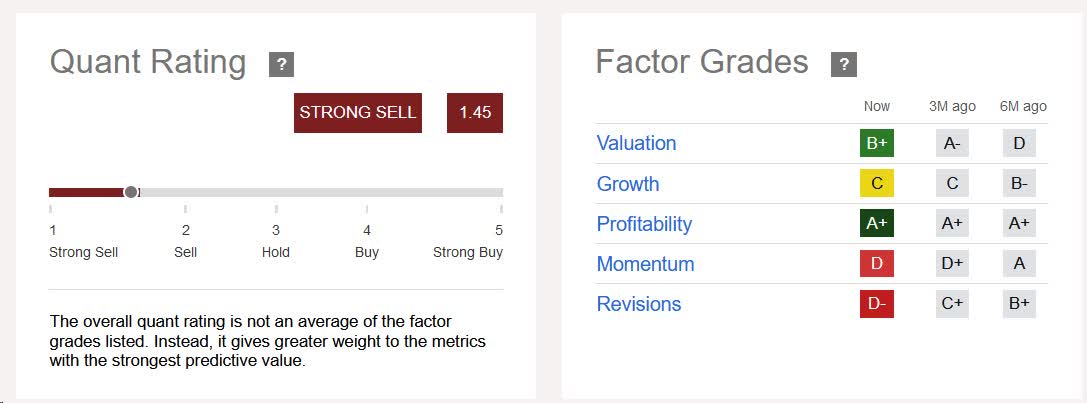

Low Multiples And A STRONG SELL Quant Rating

{kind=link}

We can see that while InMode scores high in profitability and valuation, it's the momentum and revisions grades that are mostly weighing down their Quant Rating.

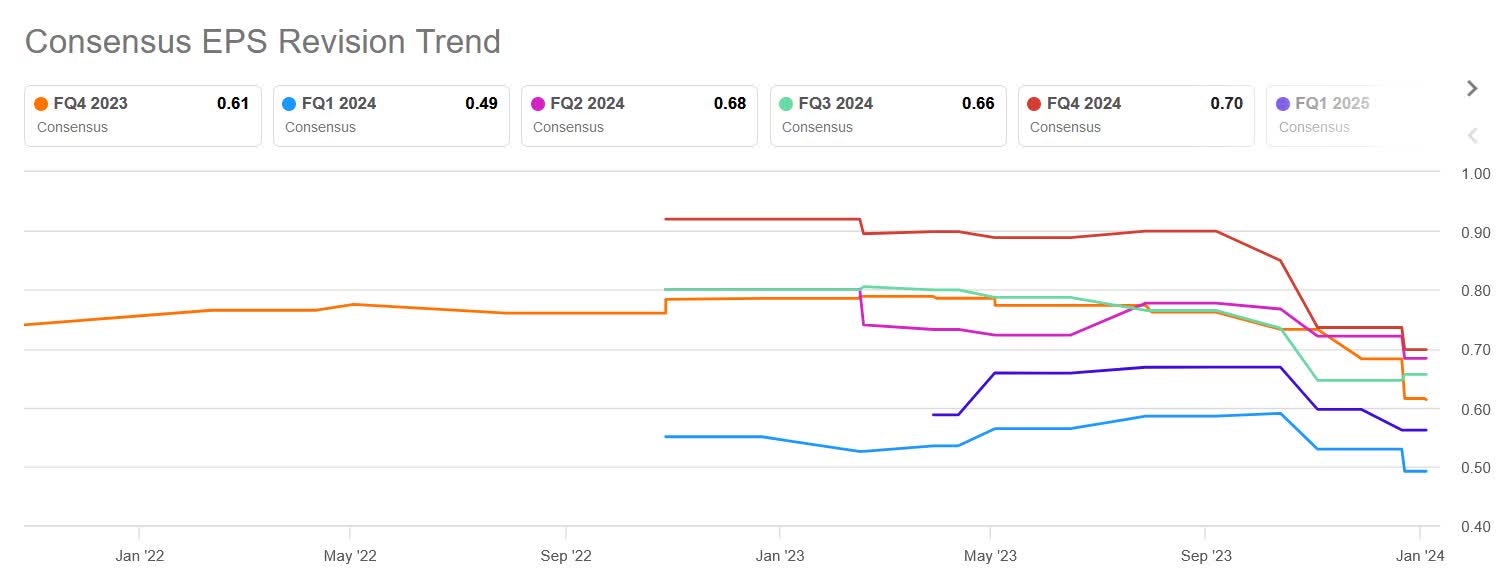

With Revisions, I think it's difficult to argue; that InMode is a former growth stock. Like most growth stocks, analysts went from very optimistic about growth to a more modest, current stance. That naturally means that estimates were slashed down in the process, an inevitable part of the transition from a growth story to a value story.

{kind=link}

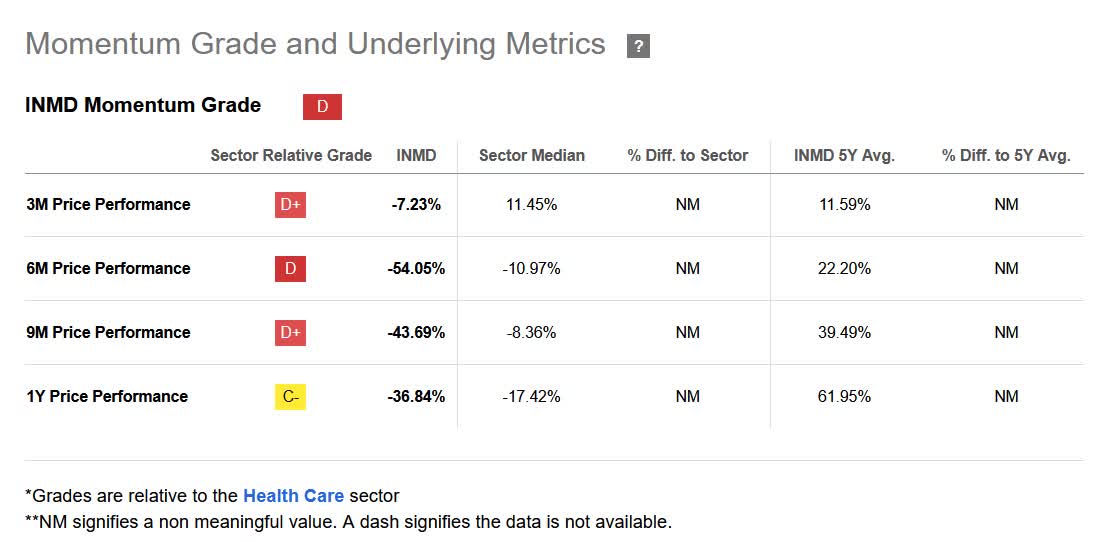

The momentum for the stock price is certainly bad though, and 2023's second semester was particularly painful.

{kind=link}

From a high of $48.25 to a low of $18.57, INMD seems to have found a bottom. However, by any momentum metrics, it will certainly score badly.

{kind=link}

Why, though? Why such a sharp decline? I think there are several factors that, when put together, explain the sharp sell-off. I also think many of them are temporary, which is why I think the sell-off went too far.

First of all, we have the war in Gaza. InMode is an Israeli company, situated in Israel. While management assured investors in the call that the war is unlikely to impact the company directly, I think part of the sale was investors simply selling Israeli-based names.

Moshe Mizrahy, replying to a question about the war during 3Q23 earnings call:

... We have two production facilities, both of them on the north part of Israel, which are not affected currently. They are not affected with the war, but it's mainly on the south part of Israel. All the team in Israel is safe. We are located in the northern part of Israel in a city called Yokneam, which is relatively not close to the war area. All the team in Israel is safe and their families, we are taking care of them. We have accumulated inventory in the US and in Israel and in some countries in Europe in order to take care of the supply for at least two quarters of finished goods and three quarters of component and subassembly...

Second of all, we have the CEO's negative commentaries about a buyback. Many investors were eagerly anticipating a buyback program to take place, but InMode's CEO was pretty adamant against it in the earnings call.

Moshe Mizrahy replying to a question about buybacks:

... Well, we thought about buyback. We thought about buyback for a long time. But I have to say two things. One, our previous experience with buyback, actually we did buyback for $100 million, did not help, did not help at all. And the stock did not react to that. It was not now, but it did. Second, I'm sure you know that one of our competitors, a company called HydraFacial, which market the product to the same market that we do, mainly to spas and less to doctors, but they sell also to doctors. They have announced six weeks ago that they are doing buyback of $100 million, official buyback, $100 million. We all expected their stock to go up. The stock price when they announced it was $6.3. The stock price today is $4. So they lost 35% of their value in the last six weeks right after they announced the buyback. So it's made us to think twice if this is the best way to support the stock, to do a buyback...

I questioned their Investor Relations in late December about a potential M&A and buyback and here's their reply:

Thanks for contacting us and for your support of InMode. We appreciate your feedback and will pass it onto management.

InMode continues to actively look at all options, including M&A, instituting another stock buyback program as well as issuing dividends, or a combination of these. Currently, M&A is the priority, and they want to exhaust that option first.

When the company and its board of directors decides on a plan, we will announce it in a press release.

While the CEO's comments in the earnings call could have been constructed better, I don't view them as malice or as a complete refusal to do a buyback - especially since they've been getting pestered about those comments ever since. I think their M&A strategy is valid and, if that fails, the company will relent and do either a buyback or extraordinary dividend, per the IR's reply. I'm certain that we will hear more about that in the 4Q23 earnings call, since it's such a hot topic.

Third of all - which I'm not sure most investors are aware - the company faced seasonality in the third quarter that hadn't faced before. Moshe Mizrahy explains it in their 3Q23 call:

... I believe we specified the three main reasons why we are a little bit short on what the market expects. First, I believe the seasonality, which is now normal in the medical aesthetic, as you probably know, in 2021 and '22 was COVID year and the COVID was in the beginning of the year and therefore Q3 was much stronger than expected and sometimes stronger than Q2. But that's not normal in the medical aesthetic. I've been in the medical aesthetic for 25 years all the way for me at C-Luminous, Syneron and now InMode. And it's always the case that the third quarter summertime, because people don't want to get treatment during the summer and exposed to the sun on their vacation, it's a slower quarter and the fourth quarter usually is the strongest one...

And, as a final headwind, we have interest rates. High interest rates impact lease rates all around the world - InMode estimates the final leasing costs are between 14%-15% annually for doctors. Not only do you have a direct impact on their customers, the negative credit conditions make the process slower; leasing companies are much more careful when providing the leases to doctors. High interest rates impact the whole economy, and while the Fed has adopted a dovish stance, it's still unknown when the rate cuts will begin. One point I would like to make here is that InMode is currently pursuing strategies that might work regardless of the Fed's dovish cycle, such as using their own, strong balance sheet to finance customers. Moshe Mizrahy talks about that in the 3Q23 earnings call:

Third reason is the fact that leasing company are tightening their procedure and their screening. They are afraid doctors will go bankrupt and they will not see the money. And therefore before the issue of purchase order to us to actually take the order, they do a very long, I would say, a very long processing time. Sometimes it takes two to three weeks. And when you have two to three weeks, some of our competitors are coming. Doctors think twice. They already think maybe I need to wait a little bit. All this process is taking place now. How we overcome it? I mean we have a lot of resources, especially we have a lot of money. And therefore we're working with the leasing company to come up with some solution. First, to optimize the processing. So it will not take three weeks. It might take a few days as it used to. We might do some other activity of in-house financing and other programs to ease the financing to certain doctors. The main project is to work with the leasing company to find solutions. We have some ideas. We already discussed with them when the process to implement that, hopefully in Q4, it will ease a little bit. Not ease the rate. The rate will stay 14% to 15%, but at least ease the process and work better. That's the only thing that we can do.

I believe the combination of those four factors cited has created the sharp selloff we've seen in the past couple of months. I also believe that most of them are temporary and should improve throughout 2024 and beyond, which should be a positive factor for the stock price.

Risks

Continuing slowing growth. Markets are mostly concerned about this. While it remains the biggest risk factor, it could also work in reverse; if InMode starts growing again, this could be a significant jump in the valuations. This applies to this industry in particular since the research race for patents is so prevalent. The company and its competitors are constantly trying to develop new technology, and new products can disrupt the market very quickly, rapidly swinging the numbers in a quarter. For instance, we'll begin to see the impact of InMode's new product, Envision, during the 4Q23.

Escalation of war in the Middle East. While it doesn't seem to be impacting InMode right now, new developments might. This doesn't include only the war in Gaza, which seems to be slowing down, but further conflicts in the region. Even if Israel isn't directly involved, being so near the war could punish both InMode's operations as well as valuation.

Higher interest rates for longer. This is a risk almost all companies face, but if inflation doesn't come down and the Fed has to back down on its dovish stance, it would be negative for InMode operations. While the company has virtually no debt, the biggest problem is the impact on lease rates, ultimately slowing down the sales process and making doctors (InMode's main customers) think twice before financing an expensive machine.

Valuation

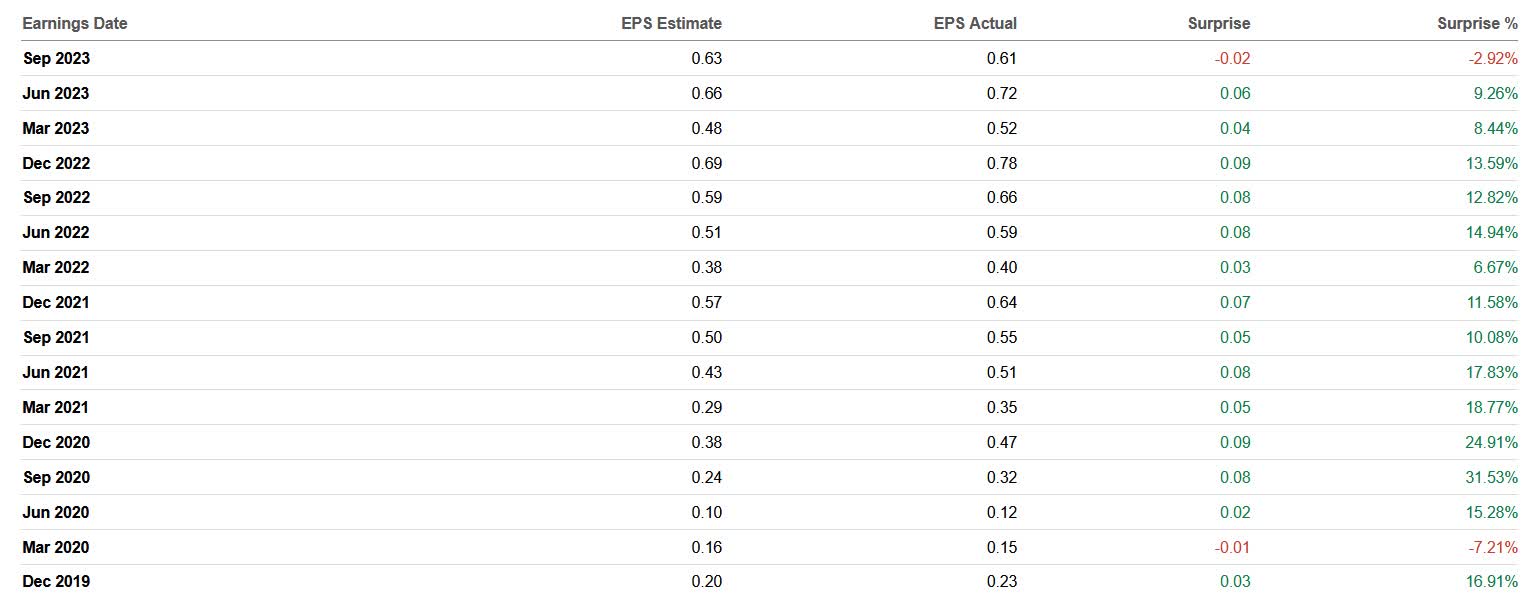

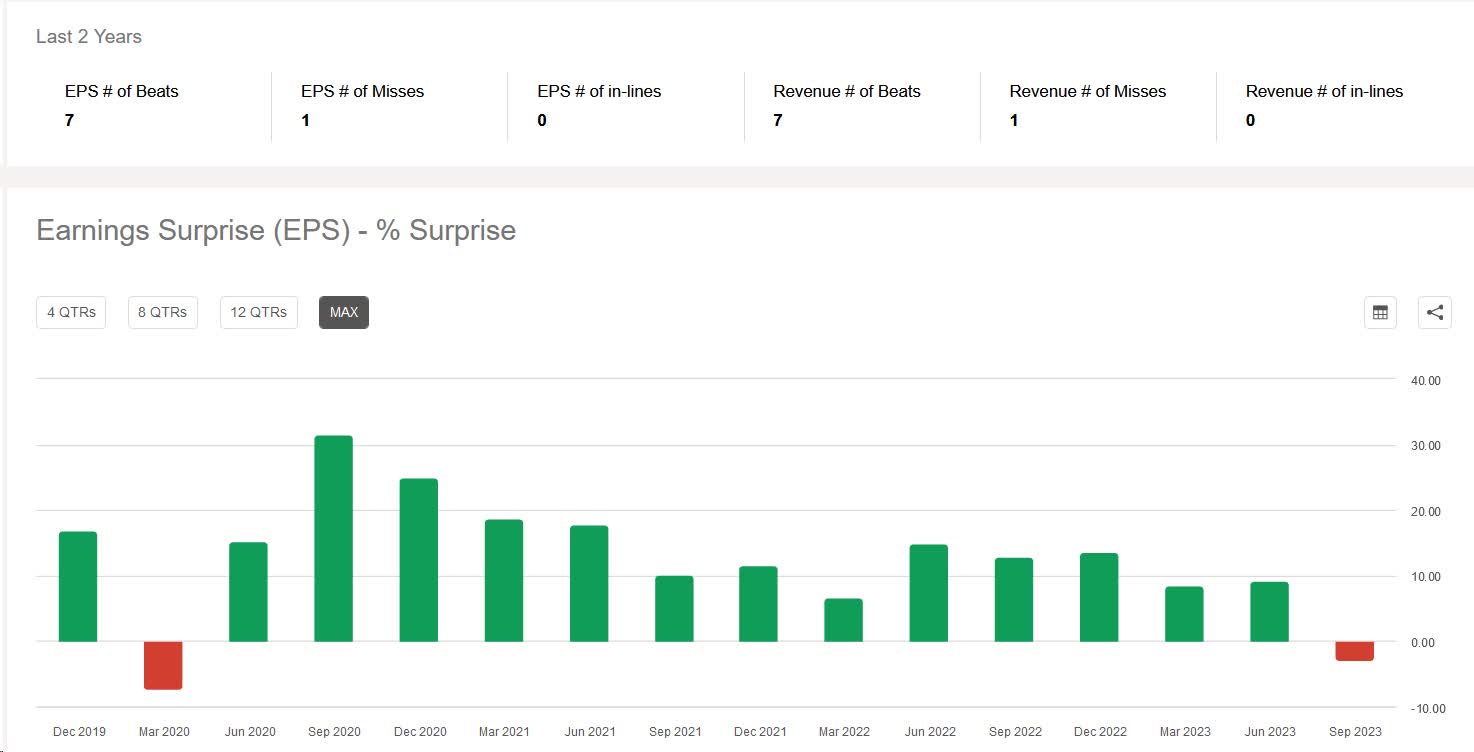

The company has recently released a statement giving their estimates for the 4Q23 - which beat analysts' expectations - and 2024 full-year revenue guidance, which was in the range of $495M to $505M, below consensus of $519.84M. When you look at their history of earnings surprise, InMode tends to beat analyst's estimates - probably because management is rather conservative in its guidance. In the last sixteen quarters, they have failed to beat analyst's expectations only twice.

{kind=link}

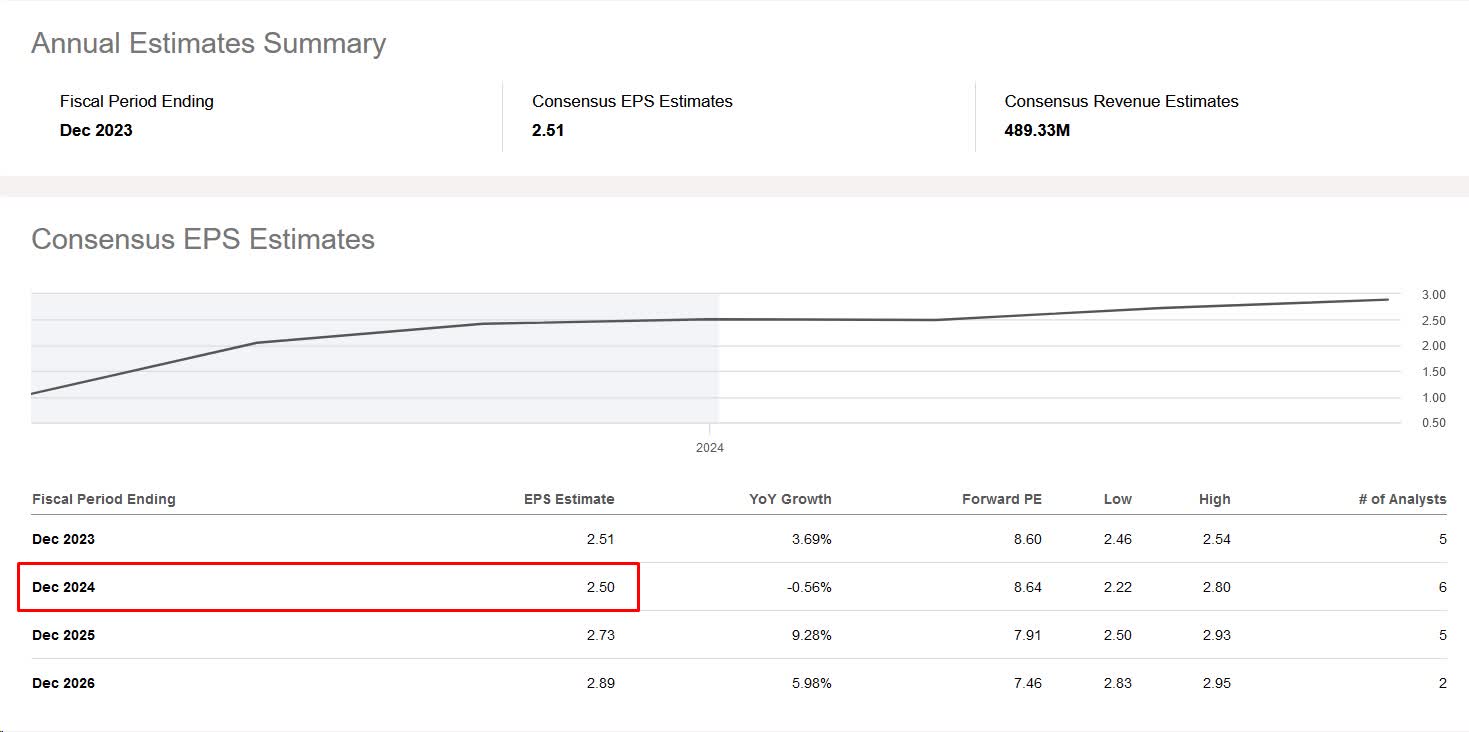

Current analyst's expectations for 2024 FY EPS is $2.50, which I will use below.

{kind=link}

One of the reasons InMode's multiples look so cheap compared to the HealthCare sector is that its growth has slowed down considerably. It's a mature, small-cap, foreign company. Therefore, I think it makes more sense to compare it to P/E multiples of the MSCI World Small Cap Index . As of Dec 29, 2023, its forward P/E multiple was of 16.04.

MSCI World Small Cap Index, Author

{kind=link}

As you can see from the table above, even in my most pessimistic scenario, where I slap a -30% adjustment to InMode's 2024 estimates, if you apply MSCI World's Small Cap Index Forward P/E multiples, InMode should be trading at roughly ~$28.00. Keep in mind that Healthcare Multiples can often be even higher, since plenty of players in that sector are growth companies.

From the table above, my current target price for InMode would be in the range of $28-$35. Even then, I still think it's cheap and that management is more likely to beat estimates than not; however, until we get more color about 2024, I think the margin of safety gets much smaller at those levels. As of the writing of this article, InMode is trading in the range of $20.40-$22.00, which puts it below my worst case.

Also keep in mind that the above calculations give absolutely zero value to InMode's almost ~$700M cash pile. If they complete an M&A or do a buyback, 2024's EPS could be potentially much higher even with lackluster growth.

Conclusion

InMode is a company that is trading at extremely cheap multiples in almost any comparison you can make. Its fundamentals are extremely healthy, which makes me very comfortable in having a position. While headwinds have negatively impacted the company recently, I believe that the market is overly pessimistic about the stock. The price seems to have hit a bottom recently, and current levels offer a good risk-reward ratio for the stock.

For the 4Q23, we will see the impact of new products such as Envision, which could surprise analysts positively. I'm also not taking into account the possibility of a good M&A being announced, which I believe would be extremely positive for the stock price since the market seems to be completely ignoring InMode's cash position.

For further details see:

InMode: Good Margin Of Safety At Current Levels