QDEL - InMode: High Growth High Margin Medical Device Company On Sale

Summary

- InMode Ltd. has 80%+ gross margins and 40%+ operating margins within a growing industry.

- The market is overestimating short-term worries that likely won't have a material effect on long-term cash flows.

- On both a relative basis and through a discounted cash flow, I estimate InMode Ltd. is undervalued by at least 40%.

Thesis Overview

For a long time now, I have been intrigued by a little known company based in Israel called InMode Ltd. (INMD). There are multiple reasons why I believe, at this time, that this company is undervalued. First, the market is underestimating the market share that InMode has in a growing industry. Second, the profitability of the company is severely underappreciated. With gross margins of over 80% and net income margin of over 40%, this company is a legitimate cash cow. Last, I believe that the market is overreacting to short-term worries including gross margin decreasing, inflation, and consumer demand shortages. In this article, I will discuss why I believe that InMode Ltd. is an opportunity too good to pass up.

Company Overview

InMode Ltd. is a medical device company that develops and manufactures devices that do non or minimally invasive aesthetic and wellness solutions. Their proprietary technology is industry-disrupting and has the possibility to continue taking market share. The company has four main types of technology that they currently use; Radiofrequency Assisted Lipolysis, Deep Subdermal Fractional RF, Hands-Free Body Remodeling, and Hands-Free Facial Remodeling. Each of these are used in different ways, but the main idea of all of them is to use radio frequencies to improve the aesthetics of a person's body. All of these technologies were developed from the co-founders of the company, who both have PhDs and have decades of experience.

Layout of Current Products (InMode Investor Presentation)

{kind=link}

Why InMode is Undervalued

Increasing Market Share in a Growing Industry

The market that InMode has established itself in is the non/minimally invasive aesthetic treatment market. This market has seen significant increases over the last couple of decades as consumers continue to want more aesthetic treatments.

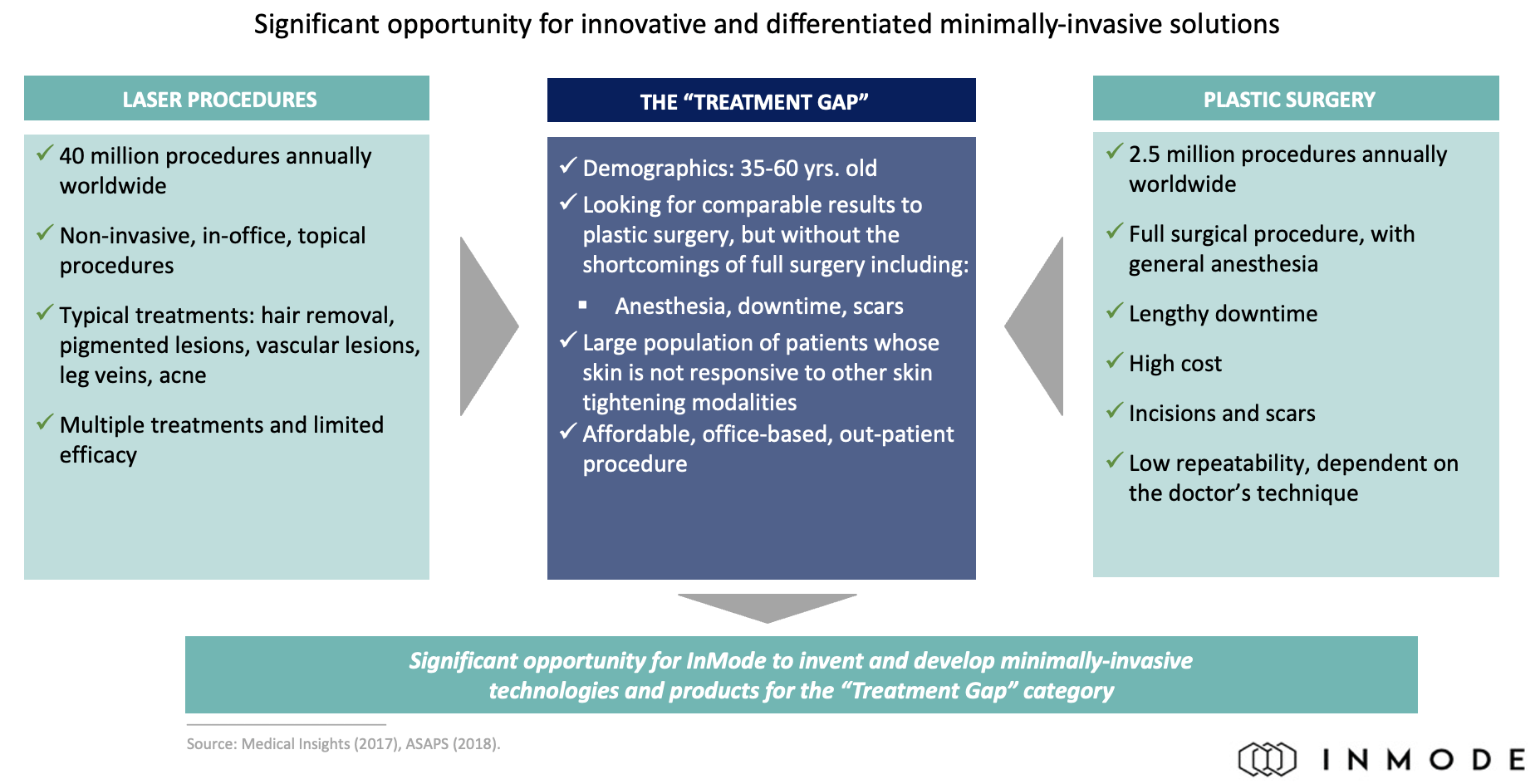

The current offerings of InMode Ltd. put it in great position to be an industry leader for the continued success. In my research, there were multiple times where the management team mentioned how InMode is trying to close the "treatment gap." This idea of a treatment gap is that the industry is in between a transition of aesthetic treatment options from plastic surgery to laser procedures. They believe that their products are a good balance between being non-invasive like laser procedures and being accurate and efficient like plastic surgery is. I have strong conviction that InMode's suite of products will continue to provide consumers with better options than available for the foreseeable future.

Description of the "Treatment Gap" (InMode Investor Presentation)

{kind=link}

High Profitability

One of the first things that caught my eye when first looking at InMode Ltd. was how efficient it is at producing cash flow. The profitability of the company is unmatched in the industry and continues to be a huge differentiator from its peers. With gross margins of over 80% and net income margins of over 40%, there are not many companies out there with those high of margins while still growing revenue double digits every year.

The reason why I have this as a mispricing is that since InMode has such a better margin profile than its peers, any downturn in the economy or industry will all the company to not be affected as much. With the huge margin of safety in their margins, the company is well protected from any significant downturn given their ability to give up short-term margins to maintain their solid customer base.

Overreaction to Short-Term News

The last major mispricing that I see with InMode Ltd. is that I believe the market is overreacting to short-term news related to things such as decreasing gross margins, inflation, and a consumer demand shortages. While it is important to know that short-term economic events could hurt InMode in the near future, there is no reason to believe that the negative news will have any effect on the long-term growth of the company.

In recent earnings announcements over the last couple quarters, InMode's financials showed that their gross margin decreased slightly. The reason why this does not make me worry at all is that even if it does decrease a little bit, the company still has over 80% gross margins. One might expect that gross margins that high are tough to keep. I am comfortable even if those gross margins shrink to 75% because they already have that margin of safety. Similar to a slight decrease in gross margin, some investors worry that inflation will continue to hamper the profitability of the company, however I hold the belief that by the end of FY 2023, inflation will not be nearly the issue it is now.

The last thing I want to note about the short-term news is that there is some belief that if we are indeed going into a recession that customers will be less likely to get non-invasive aesthetic procedures. On a general note, I believe that we will enter a mild recession with minor cutbacks in household spending. With that in mind, I believe that InMode's customers will continue to use their products. The customer base that they have established is worldwide and the physician's office that buy InMode's products continue to do so even with the economic uncertainty.

Discounted Cash Flow Valuation

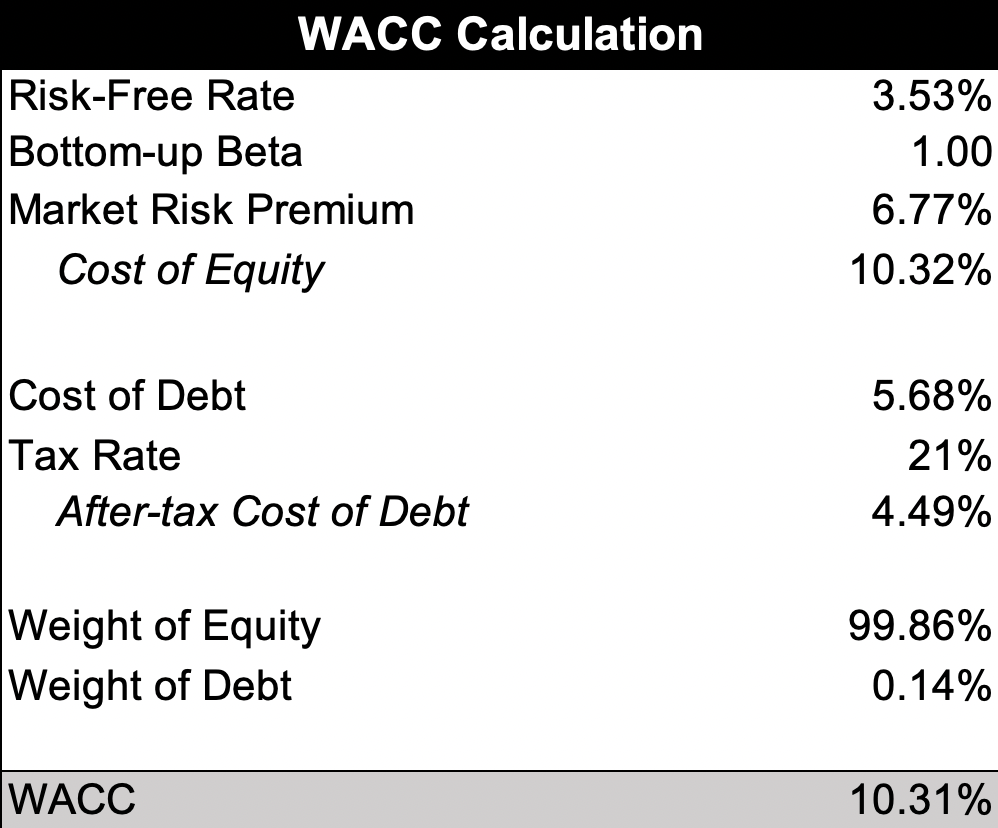

The first valuation method that I used was a discounted cash flow ("DCF") analysis using free cash flow to the firm. First, for my calculation of InMode's WACC, I used a bottom-up beta to incorporate the risk of the industry and the capital structure of its peers. Given the levered 5 year beta of 2.2, I feel that a bottom-up beta is more representative of its risk relative to its peers and the overall market. For the risk-free rate, I used the updated 10 year treasury bill and a conservative market risk premium of 6.77%. Something else to note about InMode is that it has virtually no debt, so that it one reason why their bottom-up beta is 1.00, not 2.20.

InMode's WACC Calculation (My Model)

{kind=link}

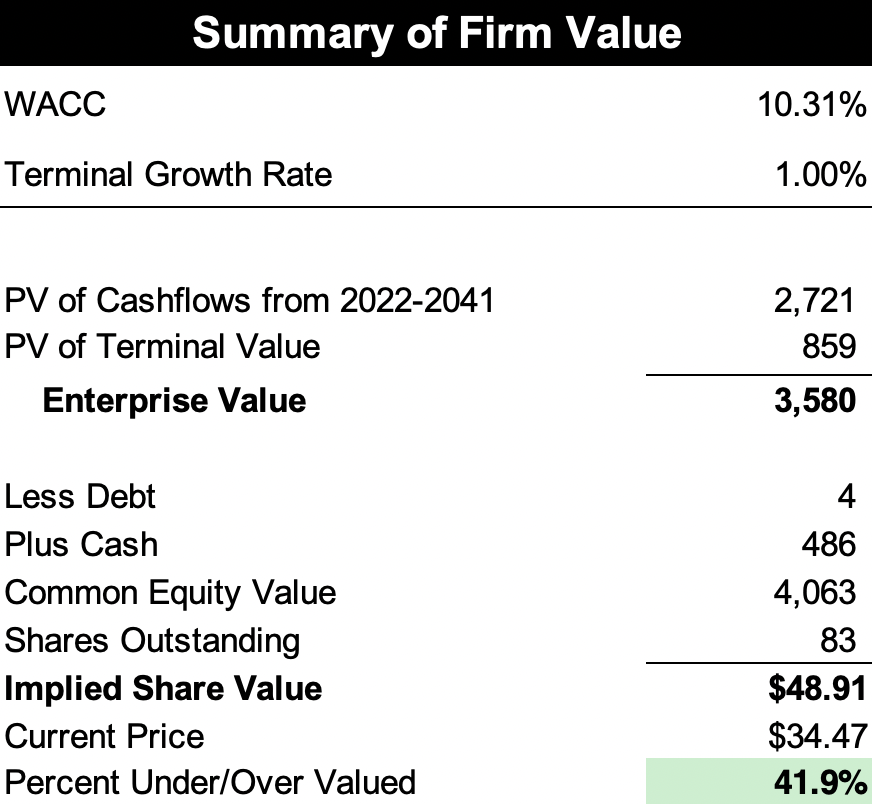

For my free cash flow ("FCF") to the firm model, I forecasted InMode's revenue for the next 20 years based on my industry and company specific research. I believe that there is still substantial growth opportunities for all of their products, and I have no doubt that the company will continue to develop new, industry leading, innovative products that will further their growth prospects. To account for the uncertain economic environment in the next two years or so, I have forecasted revenue below analyst consensus to further the margin of safety. I discounted back the future free cash flow back using the WACC I calculated and arrived at an intrinsic share price of $48.91, representing an almost 42% undervaluation.

InMode's DCF Calculation (My Model)

{kind=link}

Relative Valuation

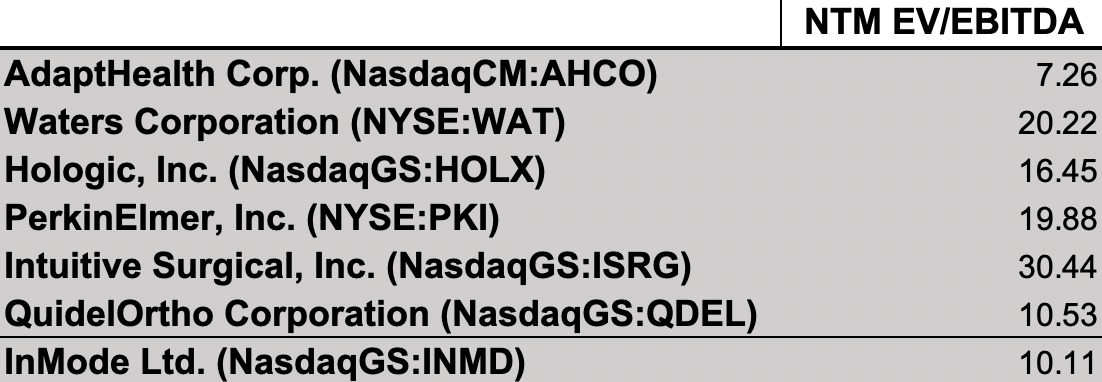

On top of my discounted cash flow calculation, I also wanted to take a look at where InMode is trading relative to its peer group. The companies who I incorporated in my relative valuation include

- AdaptHealth ( AHCO )

- Waters ( WAT )

- Hologic ( HOLX )

- PerkinElmer ( PKI )

- Intuitive Surgical ( ISRG )

- QuidelOrtho ( QDEL ).

Comparable Companies (My Model)

{kind=link}

When looking at who to compare InMode to, there are a few companies that allow us to assess how InMode is valued. While InMode makes products that have not been made before, we can look at companies who compete in a similar industry and piece it together. As shown in the chart above, it is evident that InMode is vastly undervalued no matter how you look at it. The two companies similar or lower multiples, AdaptHealth and QuidelOrtho, have worse margins and worse profitability than InMode.

With this in mind, I felt very comfortable assigning a multiple that was higher than it is currently priced. I chose a next twelve months EV to EBITDA multiple of 15.5 for InMode because I feel it is most representative of InMode's profitability, growth, efficiency, and risk. I would even say that 15.5x is conservative and one could easily make the argument that the multiple should be 20x instead. However, for the purpose of the model, I felt that 15.5x was appropriate for InMode. With an NTM EV to EBITDA multiple of 15.5, that would mean an implied share price of $50.46, representing an undervaluation of over 46%.

InMode's Relative Valuation (My Model)

Risks

Political/Regulative Risk

As I mentioned in the beginning, the company is headquartered in Israel. There is a possibility that there could be political risk with the uncertainty in the Middle East, especially Israel at the moment. While it is something to note, I do not think it is a major issue given how global the company is, and since they don't have many assets in Israel, it would be easy to relocate if they wanted to.

Shift in Consumer Demand

As stated in the mispricing section, there is risk that there are long-term effects from a recession that include major household spending cuts which would have a negative effect on InMode and its entire industry. There is a chance that consumers over time might want to change how they get non-invasive aesthetic treatments and any big shift away from the industry would obviously have a major impact on InMode's business.

Competition Risk

Going off of the previous risk, there is also a chance that a different company creates technology that is more efficient and at a cheaper price. This would mean that InMode would risk losing customers to cheaper alternatives. While there is a chance new competitors enter the market, I believe that InMode's patented technology has enabled the company to create an economic moat and has created strong relationships with physicians all over the world.

Conclusion

I have been pleasantly surprised with what I have found in my research of InMode Ltd. I believe that the business model has set the company up for continued success and the fact it is so undervalued right now makes me even more excited about its future. After doing research on the company, I felt so confident that I initiated a position in InMode, as I believe in its long-term growth prospects and my valuation conclusion that InMode Ltd. stock is a buy .

For further details see:

InMode: High Growth, High Margin Medical Device Company On Sale