HOLX - InMode: No Respect - Take Off Soon

2023-07-11 09:00:00 ET

Summary

- InMode's valuations have been discounted drastically compared to its 3Y means and its peers, suggesting its overly depressed price target of $48.30.

- However, we believe an upward revision to P/E of 18x is warranted, suggesting a more optimistic long-term price target of $60.84, providing investors with handsome upside potential.

- The INMD management competently maintains robust gross and operating margins, despite the rising inflationary pressure and increased headcounts.

- Things may normalize in the near term, once the inflation rate moderates in Israel, boosting its profit margins and stock prices by 2025.

- For now, we are cautiously hopeful for a raised FY2023 guidance, potentially allowing the stock to break out of $38 for good.

INMD's Investment Thesis Is Even More Beautiful, After The Correction

We previously covered InMode ( INMD ) in November 2022, highlighting its raised FY2022 guidance and the management team's stellar execution thus far. We had concluded the article with a Hold rating, given the stock's notable elevated valuations at that time.

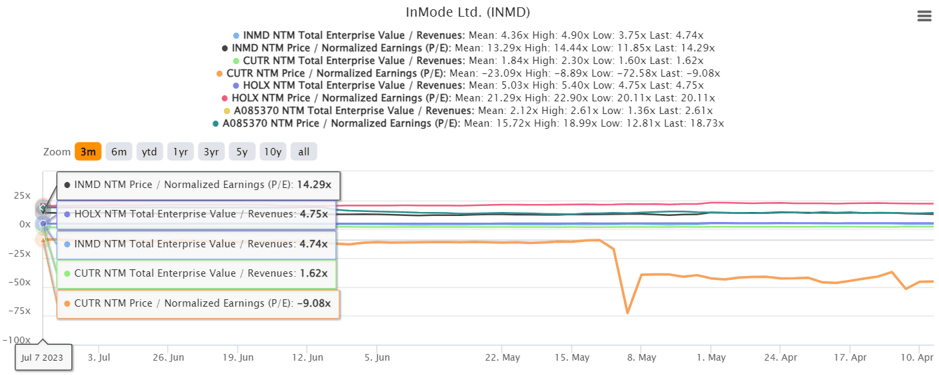

INMD 3M EV/Revenue and P/E Valuations

{kind=link}

By now, INMD's valuations have been further discounted to NTM EV/ Revenues of 4.74x/ NTM P/E of 14.29x, compared to the previous November 2022 levels of 5.17x/ 15.62x and 3Y mean of 7.36x/ 22.66x, respectively, thanks to the peak recessionary fears.

Interestingly, we have not seen a similar moderation in its Women Health Care/ Aesthetic peers, such as Hologic, Inc. ( HOLX ) at NTM P/E of 20.11x/ 3Y P/E mean of 18.27x and Lutronic Corporation at 18.73x/ 18.46x, respectively. Cutera, Inc. ( CUTR ) has been excluded for now, since it remains unprofitable.

Based on INMD's NTM P/E and the market analysts' FY2025 adj EPS projection of $3.38, we are looking at a long-term price target of $48.30, suggesting a decent +26.8% upside potential from current level.

However, we believe that there are great opportunities for shareholders who are patient, since the stock's valuations may be eventually upgraded nearer to its historical means and peers. This is because the management continues to achieve ~80% in gross margins while optimizing its operating expenses during this rising inflationary environment.

For example, INMD maintains its excellent gross margins of 83.8% over the last twelve months [LTM], while expanding its annualized top-line to $424.28M (-20.5% QoQ/ +23.5% YoY) by the latest quarter, otherwise, increasing its gross profits at a CAGR of +39.48% since FY2019.

Most importantly, the management has been able to optimize costs, with its annualized operating expenses only growing to $187.28M (-11.1% QoQ/ +29.5% YoY) by the latest quarter, otherwise, at a CAGR of +34.77% since FY2019. This cadence explained why the company has been able to grow its operating margins to 43% over the LTM, compared to FY2019 levels of 38.1%.

While INMD's gross and operating margins may seem lower compared to the FY2021 peak of 85% and 46.8%, respectively, we believe it stock valuations may be upgraded in the intermediate term. This is due to its outperformance, compared to HOLX's margins at 62.7%/ 23.2% and Lutronic Corporation at 64.6%/ 20% over the LTM, respectively.

It is also important to note that INMD's third party manufacturers are likely impacted by the uncertain macroeconomics, with Israel reporting a core inflation index of 4.7% by May 2023 , compared to 2019 levels of 0.84% . Therefore, things may lift from 2025 onwards once the country's inflation rate normalizes. Only time may tell.

Either way, the management has already guided FY2023 revenues of $527.5M (+16.1% YoY), gross margins of 84% (+0.2 points YoY), adj operating income of $237M ( +6.6% YoY ), adj operating margin of 44.9% (-4 points YoY), and adj EPS of $2.59 (+7% YoY) at the midpoint.

Based on these numbers, it appears that INMD's operating expenses may have accelerated, as witnessed in its recent performance. This is mostly attributed to the increased marketing spend and staffing for the ramp up of the Morpheus A, Envision, and Empower platforms thus far, with the next-gen Evoke to be launched by H2'23.

Given the increased headcounts, it is unsurprising that its Stock-Based Compensation expenses have also grown to $25.57M (+107% sequentially) over the LTM.

These developments suggest that the INMD management is aggressively investing in its long-term capabilities, at a time when its top-line growth has been decelerating, compared to FY2022 levels of +27%, FY2021 levels of +73.5%, and FY2019 levels of +56.1%.

While its bottom line appears to have been impacted as a result of its intensified SG&A expenses of $43.72M (-11.5% QoQ/ +31.1% YoY) and R&D expenses of $3.1M (-4.9% QoQ/ +9.9% YoY), we remain confident about its potential turnaround moving forward.

Combined with INMD's zero reliance on debt and rich balance sheet with cash/ short term investments of $574.45M (+4.9% QoQ/ +43.8% YoY) by the latest quarter, investors may be rest assured about the management team's prudent execution.

So, Is INMD Stock A Buy , Sell, or Hold?

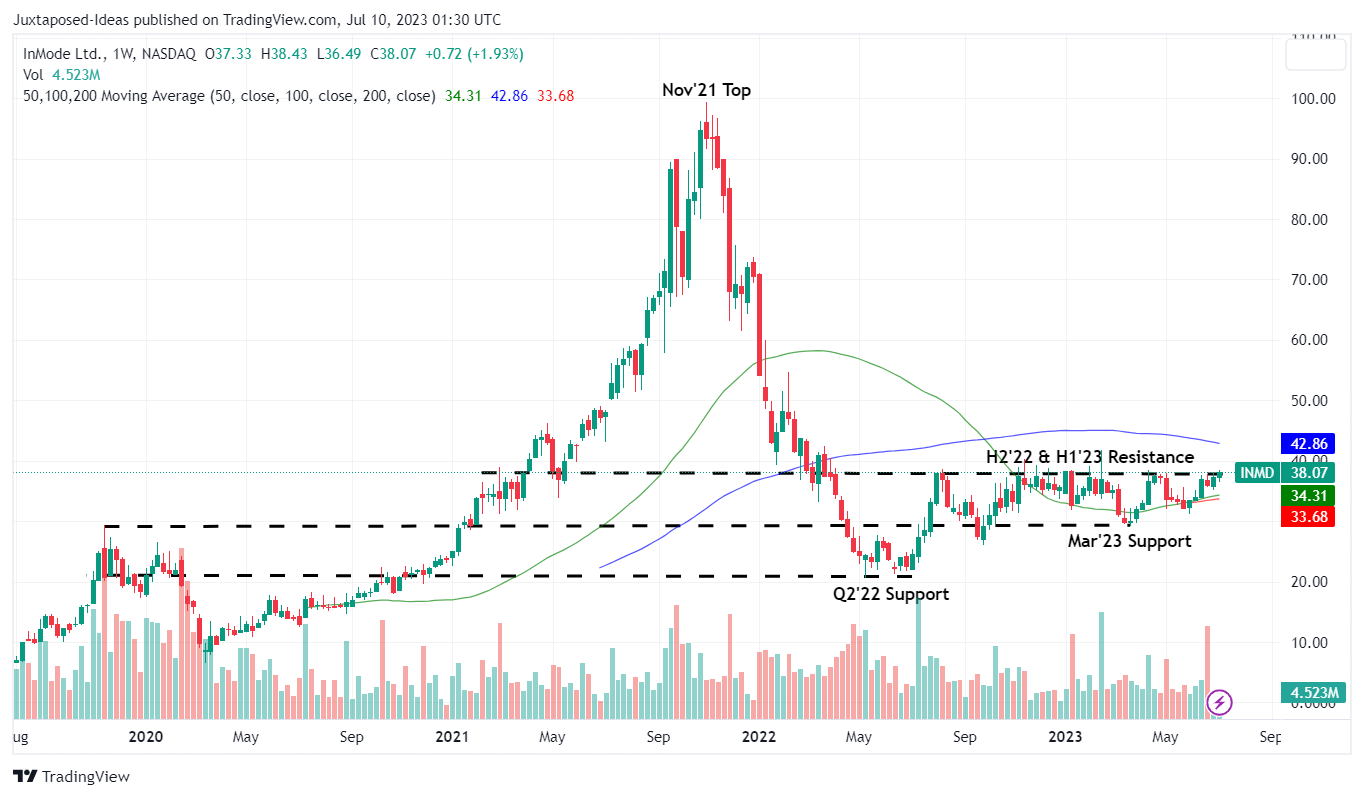

INMD 5Y Stock Price

{kind=link}

As a result of these optimistic developments, we are raising our long-term price target to $60.84, based on an upsized P/E target of 18x. This valuation also provides interested shareholders with an excellent upside potential of +59.7% from current levels, triggering our Buy rating for the INMD stock.

However, we must also highlight that the stock has been facing immense resistance at these levels, potentially triggering further sideways movement in the near term, depending on how the management executes in the near term.

Then again, while bottom-fishing investors may consider adding at its previous March 2023 support levels of $30 for an improved margin of safety, we believe the risk reward ratio appears to be highly attractive here, since we remain convinced about its long-term prospects.

Most importantly, the INMD management has hinted that a raised FY2023 guidance may be possible in the FQ2'23 earnings call, potentially triggering the stock's break out of the $38 for good.

For further details see:

InMode: No Respect - Take Off Soon