INMD - InMode: Overblown Reaction On Guidance A Rare Valuation

2023-10-26 12:07:25 ET

Summary

- The business entered my High Quality and Bad Momentum Screener.

- War concerns have had limited impact on the company's sales and profitability, as most of its sales are from foreign markets.

- InMode revealed slashed EPS and revenue guidance for FY 2023 and Q3. The company has a strong balance sheet with a significant cash position, reflecting 34% of the current capitalization.

- Based on many valuation angles, the company is the cheapest in the industry based on profit margin, forward PE comparison, balance sheet, and valuation dashboard.

InMode (INMD) and its stock first came to my attention just a few days ago, when I refreshed my Seeking Alpha key High Quality and Bad Momentum stock screener. I began to investigate further. In the analysis, I will place a great deal of emphasis on the company's track record, its future growth potential, and, most importantly, the valuations, which are extremely low for a firm with such high margins and profitability. However, growth concerns due to a high interest rate environment are dragging down the stock price and impacting the company's clientele. The new impact occurred after the company lowered its preliminary guidance for the third quarter and fiscal year 2023, which is expected to decrease by 8% compared to the previous consensus; however, the stock price has declined by more than 30% over the past few days. In addition, war fears made the stock even cheaper, despite the fact that Israel contributes only 1% of the company's revenues. I see only a limited impact from this vantage point. At the current price, the company holds of 34% - 40% of the current market capitalization in the company's pure assets: cash and s/t investments minus liabilities. I believe numerous other companies may be interested in purchasing this business. Therefore, a "clear cash position" of $6.9 is considered when purchasing this stock for $19.9. You cannot find easily a company with such high margins and a low forward PE, based on our industry research.

In the past, the company was significantly overvalued, but that has changed dramatically, and I now view it as an excellent bargain for the reasons I will explain later. However, based on the company's balance sheet, I determined that the company's margin of safety is substantial, as the Cash and Short-term investments minus total liabilities calculated per share is close to $7. Compare it to the stock price of $20; this will help you evaluate the situation in which, in my opinion, Mr. Market is wrong.

Slashed Guidance and Overblown Reaction

There is a great deal of negative fundamentals, which is aggressively dragging the stock price down. However, I will attempt to determine whether it was caused by psychology or actual events. As a future shareholder, I view the current events as a phenomenal investment opportunity because, as I will reveal in the valuation section, the company is facing headwinds, but the price has been cut by more than 30 percent in recent weeks. In terms of valuation, it begins to be truly safe near this point, as the margin of safety increases significantly in my view.

However, one of the primary drivers of the most recent price decline is the company's slashed guidance , as reported here on SA:

The Israeli maker of aesthetics medical equipment said it now sees full year revenue in the range of $500M to $510M , down from its prior guidance of $530M to $540M . For Q3, InMode expects to report adjusted Q3 earnings of $0.59 to $0.60, adjusted gross margins of 83% to 85%, and revenue of $122.8M to $123M.

Downward Revision Trend Started and Macro Implications

According to management, there are solid reasoning for this, including the company's return to normal, seasonality in Q3, and economic slowdown, as well as the company's observation of a decrease in summertime purchase decisions. Additional reasons cited here were:

Moreover, constraints in financing of medical equipment, marked by higher interest rates, tighter leasing approval standards, and bottlenecks in loan processing, have also dampened InMode platform sales activity worldwide.

In conclusion, there is a decline of 8.5% from the highest (old) estimate to the lowest (current) estimate, but still a substantial margin. In a short period of time, revenue forecasts for the current, subsequent, and two fiscal years out have dropped significantly, and this trend may continue. However, despite this decline, Forward PE is still very attractive.

The margin is still quite high, and in the event of further demand concerns, a typical easing in cyclical sectors could occur. Nevertheless, this is a cyclical point. To find out more about the macroeconomic outlook, you should read my most recent analysis here . I believe the company is on the right track based on its history and the industry's continued growth.

War Concerns are Terrible, but have Small Impact

As INMD is an Israel-based company, the entire stock market experienced a significant sell-off, led by the stock index TA 35, which fell by more than -10% in the first trading days following Hamas's multi-pronged attack on Israel. The Israeli prime minister also declared war. Uncertain as to how this will impact the economy as a whole, there is a possibility of a consumer shock manifested by decreased consumption, retail sales, investments, and migration. From this point forward, there may be a significant impact on the Israel business unit. Furthermore, it is a new geopolitical risk that could result in even more aggressive global tightening if the price of oil reacts by increasing.

However, below I provide the company's geographical revenue breakdown from its SEC filings, which indicates that 66% of sales are made in the United States, 11% in Europe, and 23% internationally. My subjective point was that only a fraction of total sales are in Israel, perhaps 1-5%. Later, the company cleared t his up later:

We don't anticipate any interruption to production. Our inventory levels globally and in Israel are sufficient and include components and subassemblies for the next three quarters. The contribution of revenues generated from Israel is less than 1%.

InMode Revenue Breakdown (InMode, SEC)

{kind=link}

In the initial reaction, the stock price fell -6% on the first trading day, and then more than 25% after reduced guidance; however, the company is getting closer to "pure value," as I term it. Currently, the stock price is fluctuating near $20, accompanied by a pervasive negative sentiment.

Risks Arising from Macro and War

Where I see potential risk from the conflict is not in Israel sales, but rather in the form of additional pressures on energy prices, which could lead to an increase in CPI and, potentially, a prolonged tightening in tandem with a decline in consumption. Many individuals may become more cautious and prefer to delay certain consumption habits. On the other hand, geopolitical risk carries the potential to trigger additional tightening from market participants and central banks. As some current FOMC members have stated in the past week, the significant increase in bond yield has nearly eliminated the need for additional rate hikes. Such aggressive moves on the bond market, in my opinion, not only reveal the great opportunity out there, but also cause much stronger tightening than the overall 25 basis points by the FOMC. Until the end of the year, it is uncertain whether rates will increase once more. However, in my opinion, risks associated with overtightening are increasing rapidly, and with the addition of geopolitical tension, which could cause growth concerns, this is the ideal time to focus on stock picking based on extremely strict criteria and a long-term outlook.

In my previous analysis , where I am bullish ( AGG ) as of early September explains why my outlook on bonds with current yields is becoming increasingly bullish. Yes, I was a little more preliminary, but this was the current pricing set-up:

However, such yields are ideal for asset managers and also attractive for retail investors. Imagine the following long-term yields: 4.24 percent for 10 years, 4.55 percent for 20 years, and 4.33 percent for 30 years. These are the levels that investors and many analysts believed would never be reached again. Levels last seen in 2009. Nonetheless, this threat persists. From a timing perspective I believe, there could be a little bit spark up by 10-20 bps from current yields, which could pull down the AGG and TLT down. This could be solid opportunity.

Honestly, the US 10-year yield has just reached 4.9%, the 20-year yield has reached 5.2%, and the 30-year yield has risen to 5%. So, from my perspective, there was no perfect timing, even when considering a further move of 10-20 bps, but this makes me an even stronger bull on the market, as Bill Ackman recently disclosed :

Bill Ackman - positioning (Bill Ackman on X platform)

I strongly concur with this viewpoint. However, additional risks could result in a further decline in the stock price. And for this reason, I emphasize the importance of being a strong bull for US bonds (with combination of short opinions on SPX and Nasdaq in last 3 months) and a cautious, critical stock picker. And INMD is one of few companies that offers a very large margin of safety, a stunning valuation, and solid balance sheet criteria despite the current growth concerns.

How the Worsening Macro is Affecting the Business Model

As the majority of the company's revenue came from equipment sales rather than the subscription model, it makes sense to concentrate on lending standards. Initially, it is essential to consider the clientele and business model. The company's primary source of revenue is the sale of its aesthetic market-focused medical devices and technology. The clientele of InMode consists of companies, plastic surgeons, dermatologists, and other professionals who provide such services and treatments to patients.

A climate of rising interest rates can have a significant impact on the company's clientele. First, these professionals who purchase InMode's devices and technology can rely on financing to acquire its likely expensive products. The current interest rate environment can make financing a client's equipment more expensive and difficult. The second possibility is that they want to postpone future investments or purchases, will reconsider purchasing InMode's products, and may struggle due to their reduced budget. In general, a higher interest rate can have a greater influence on consumer demand. However, the extremely robust industry demand significantly mitigates a number of these factors, as will be demonstrated below.

Industry Outlook is Very Promising

Although the sector outlook is very promising, a great win for the business as a whole is still increasing demand in the aesthetic medicine market, where, according to Grand View Research :

The global aesthetic medicine market size was valued at USD 112.0 billion in 2022 and is projected to grow at a compound annual growth rate CAGR of 14.7% from 2023 to 2030.

Moreover, in the report called: Global Medical Aesthetics Market Forecast to 2028 - COVID-19 Impact and Global Analysis By Product, is projecting:

The medical aesthetics market is projected to reach US$ 16,034.87 million by 2028 from US$ 7,039.06 million in 2021; it is expected to register a CAGR of 12.5% from 2021 to 2028.

Global Medical Aesthetics Market Forecast (Research And Markets)

My High Quality and Bad Momentum Screener

I would like to mention briefly that no screener is the holy grail, and that I can be affected by incorrect selection assumptions. Nonetheless, I believe that searching for a quality stock using specific criteria increases the likelihood of success. Consider that this stock screener includes stocks with negative momentum but a superior business model. There are more than five or six choices, but this one captured my attention on the first and second viewing. In other words, the screener reveals a high-quality business model based on its criteria, but cannot guarantee that the price will not drop further. Because "the shape" of negative momentum carries this risk. However, you need not catch the bottom, as Warren Buffett stated:

It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

However, based on the pricing, business development, and industry outlook, I believe I could buy shares of this wonderful company at a wonderful price.

Here are the first criteria:

- Quant rating: Hold to Strong Buy (due to great ability of the quant rating),

- PE GAAP ('TTM'): 0.0 to 25.0,

- PE Non-GAAP ('FWD'): 0.0 to 15.0 (these conditions help me ensure a cheap selection of promising companies with EPS growth expectations),

- Revenue (over 3 years): 15% to >40% (I want to find companies that have experienced significant growth over the past three years, but not too much due to the risks associated with big growth),

- Revenue ('FWD'): 15.0% to >40.0%,

- Net income (3Y): 10.0% to >60% (I want to see a solid track record of growth in Net income),

- Net income margin ('TTM'): to range from 5.0% to >50.0%.

- I consider the quick ratio, where the lower bound should be higher than 0.8, and the debt-to-equity ratio, which should be as low as possible, i.e. between 0% and 60%, to be the most important balance sheet criteria. I believe that these ratios are safe from a liquidity and leverage standpoint,

- The final and one of the most crucial factors is the Momentum Grade, which should range from F to C+ (we want high-quality companies with temporary momentum issues).

The filter results should be considered as very preliminary and as first-view narrative, as indicated by my previous analysis with focus on lithium stocks that are highly susceptible to commodity price-related risks, but are still gainers. My experience has taught me that it is preferable to concentrate on businesses that exclude such risks as INMD, where there are no external factors other than common macro ones. There were many successful small picks in the screener, such as (ACLS), (PERI), (TGLS), and (FN), which are no longer included in the screener because they no longer satisfy the condition of bad momentum. Despite the fact that ALB is down 30% in my previous screener-based analysis, I continue to believe it possesses enormous potential. However, I cautioned that the decline is possible, as it is a bad momentum filter risk in the very short-term; however, the long-term perspective is different. Nevertheless, the lithium stock is performing significantly below expectations due, among other external factors, to the price of lithium. From this point of view, we should focus on companies where there is no-commodity related risk.

The Comparison to the Screener

In the screener I had revealed key criteria and here is the summary of InMode:

- PE GAAP ('TTM'): 9.25,

- PE Non-GAAP (Forward): 7.51 and PE GAAP (Forward): 8.38 (following the downward revision already reflected into Wall Street's forecast),

- Revenue 3y and 5y growth: 46.4% and 44%,

- Forward revenue growth was reduced to 0.6% to 2.6% year-over-year ($497 million for FY 2022 and $500 - $510 million for FY 2023). This is the only criterion not met by the thesis after it was reduced.

- Net Income 3y and 5y growth: 53% and 55%,

- Net Income margin for FY 2022 and TTM: 35.5% and 36.7%,

- Balance Sheet: Quick ratio at 11, absolutely safety, balance sheet consists of very liquid assets, debt to equity is 0.5% (= no leverage),

- Momentum Grade is bad at D+ (we want high quality companies with bad momentum due to temporary issues).

In conclusion, InMode is a great company with a solid trend, a pure balance sheet with no leverage, and only temporary issues; however, the stock is under pressure due to growth concerns stemming from lowered guidance due to strong tightening conditions (their clients may struggle to borrow and delay investments) and potential harm in overall spending and CAPEX by other companies. However, a mitigating factor is the industry's optimistic outlook and extremely low valuation levels.

Valuation Focus

Relative Comparison

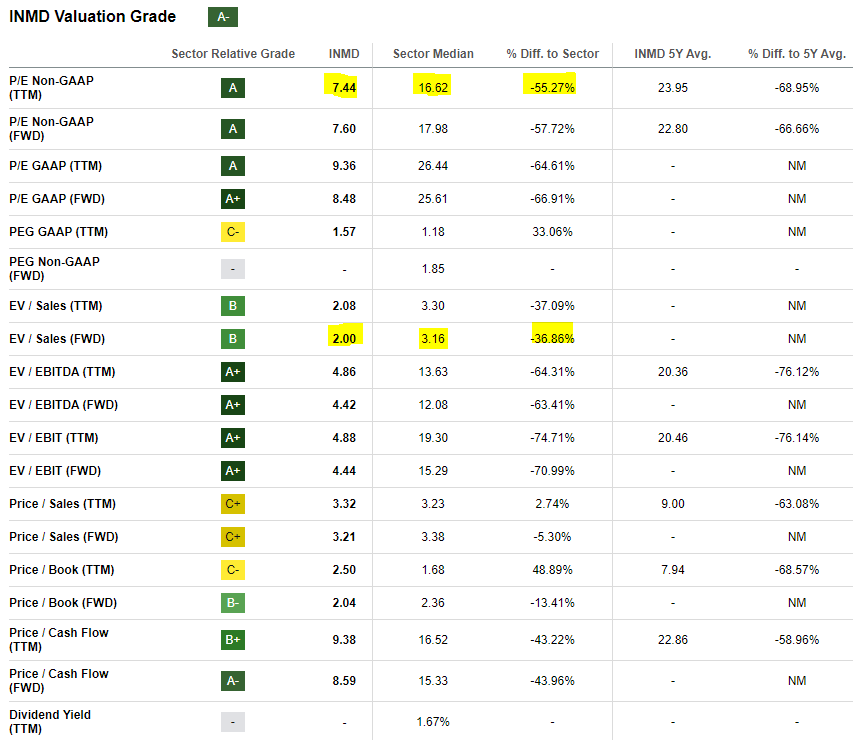

First, I see an excellent valuation summary in Seeking Alpha's valuation section, which indicates that the company is very cheap with an A- grade and very cheap relative to the sector from every angle. Regarding forward PE, PB, PS, and PCF, there is a 36%-55% discount to the sector's overall valuation. This indicates that the margin of safety is substantial. Consequently, I observe a wildly overblown reaction to the updated revenue guidance (downwards) and war concerns, which I believe are extremely disconnected from reality.

InMode - Valuation Grade (Seeking Alpha)

{kind=link}

The price has a strong correlation with both the revision trend and Wall Street's price target. However, there is currently a wide gap between the current price and price targets. Almost certainly, we will experience a further downward revision, but we will be better informed after the next earnings report in a few weeks.

Before comparing the company's profit margin and forward price-to-earnings ratio to the overall sector's profit margin and forward PE, I typically assess the company's valuation. We can conclude that InMode is in a very rare position, in the right corner, and is therefore a company with extremely high margins and a low market value. Companies with a profit margin between 20 and 27%, but a higher valuation, are most comparable (little bit left). This indicates, according to the sector's margin, that the company's valuation is quite attractive. There is no comparable company facing similar circumstances. This is another reason why I believe the revenue decline and war fears to be exaggerated reactions that drove the stock price substantially and largely unjustifiably lower.

P/E Fwd vs. Net Income Margin in Sector (Lucid Vision)

Balance Sheet Approach

As stated in the very first lines of the analysis, the balance sheet is devoid of any indication of leverage due to screener criteria. In addition, a deeper examination reveals that the working capital is extremely valuable, as total current assets significantly and multiple times exceed total current liabilities.

However, I calculated "Cash Value" in the chart below, which I consider to be Pure Cash. This is why. First, we must define what I have categorized as pure cash. The item consists of cash and short-term investments (market investments) that can be quickly converted to cash, but at least generate a return. Then, I deducted "all liabilities," including not only current liabilities but also long-term debt, etc. Then it was divided by the total shares. The following are the calculations:

- "Cash Value" or "Pure Cash" = (Cash + S/t Investments) - All Liabilities),

- Working Capital = Total Current Assets - Total Current Liabilities,

- Finally, you obtain results in millions, which you can use to compare to market capitalization; however, I have divided by the number of shares to determine value per share.

- In summary: Pure Cash Value Per Share = $6.8

- Working Capital Value Per Share = $7.9

As shown in the graph below, the trend in cash generation is enormous and will continue with extreme certainty in my view, despite reduced revenue projections for FY 2023. And it is driven primarily by high margins. However, this indicates that based on the current price of $20, $6.8 are fully reflected by cash. In other words, 33-35 percent of the current market price is fully adjusted for "pure cash," or if you purchase a share of stock for $19.8, $6.8 of that amount is fully adjusted cash. Moreover, I am convinced that if price pressures continue, the company has more than $560 million in highly liquid assets (more than one-third of its market capitalization) to announce any potential buybacks.

InMode Pure Cash and WC per Share (Lucid Vision)

Summary

Despite all of the data and growth concerns, I am convinced that the market's reaction to the company's guidance has been exaggerated. Current macroeconomic conditions have a significant negative impact on the company's clientele and their capital expenditures, but the industry outlook appears to be quite positive with a high CAGR. In addition, there is a great deal of negative sentiment surrounding the stock price, which is also affected by the conflict in Israel and its potential repercussions. There is still a risk of additional downward pressure on future earnings and revenue forecasts heading into FY 2024, but the company is navigating these challenging times with great skill. There are almost no direct effects of war (on InMode's operations) I see, with the exception of a possible global effect that could weaken consumer demand. Despite all of these threats and risks, which I described in the macro implication section, I am confident that the valuation is extremely attractive, based on both relative ratios, such as Forward PE, and relative to the sector, where I compared profit margin with Forward PE, as well as a very healthy balance sheet with a strong cash position and strong cash generation. I believe that this long-term trend represents an opportunity. I believe the fair value of the stock price is between $32 and $38, which is assuming valuations close to the sector average. Using a balance sheet approach as well as a great valuation table from Seeking Alpha, I can say that the stock is extremely undervalued relative to its track record, growth, challenging times, and unleveraged business model with solid potential.

Before investing in the company, it is strongly advised that you conduct your own research. The analysis is based solely on my thoughts and opinions and should not be considered investment advice.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

InMode: Overblown Reaction On Guidance, A Rare Valuation