INMD - InMode: Undervalued Even Under Recessionary Conditions

2023-05-02 11:17:09 ET

Summary

- InMode is a pioneer, first mover and leader in the field of minimally-invasive treatment and it generates mouth-watering returns.

- InMode is set to exceed investors' expectations embedded in today's share price even if a recession hits. Demand will likely prove far more resilient than the market is pricing in.

- My long thesis supports a 50%+ gain with a target price of ~$60.

Demand for InMode's (INMD) products will prove to be more resilient than the market is currently pricing in - even if a recession strikes. This company offers best-in-class margins and returns, has a dominant market position, has a rich product pipeline, and generates abundant cash to fund operations and growth. Shares are undervalued and have >50% upside potential from today's price.

InMode designs, develops, manufactures and markets minimally-invasive and non-invasive aesthetic medical products. Its products target an array of procedures including permanent hair reduction, facial skin rejuvenation, wrinkle reduction, cellulite treatment, and skin appearance and texture. It was founded in 2008 (by Moshe Mizrahy (current CEO) and Dr Michael Kreindel (current CTO), taken public in 2019 and is headquartered in Yokneam, Israel. Within the aesthetic solutions market, INMD develops and provides energy-based, minimally invasive surgical medical treatment solutions that primarily address three end markets: face and body contouring, aesthetics, and women's health. The company also sells consumables (13% of revenue) that practitioners use for each individual treatment and contribute to the visibility of the model. INMD now has 220 direct sales reps and 69 distributors worldwide. InMode's products are currently sold in 63 countries and serve a clientele of aesthetic and wellness practitioners such as plastic surgeons, dermatologists, OB/GYNs and ENTs (Ear, Nose & Throat) and Ophthalmologists. Roughly 66% of revenue is generated in the US and the remaining internationally.

I know what you're thinking. Ultra-discretionary treatments are extremely vulnerable to the economic cycle, right? Stick with me, read through the article and you will see why INMD is a good risk-adjusted opportunity even through a recession.

First off, let me explain what are the criteria I look for when owning a stock through a recession:

- Exceptional profitability

- Capital efficiency

- Industry-leading cash flow generation

- De minimus debt

- Industry-leading position and benefiting

- Management with skin in the game

- Operating in an industry with secular growth drivers and a track record of innovative product launches

- Undervalued stock price relative to growth and profitability prospects

The combination of all the above gives an investor a wide margin of safety in fundamentals as well as valuation. In fact, when all the boxes are ticked, a recession benefits the company in the long term as it sheds light on new opportunities to execute M&A at reasonable prices, invest while competitors are cutting costs and prepare for the next upcycle while everyone else fights for survival. InMode ticks all the boxes.

Seeking Alpha

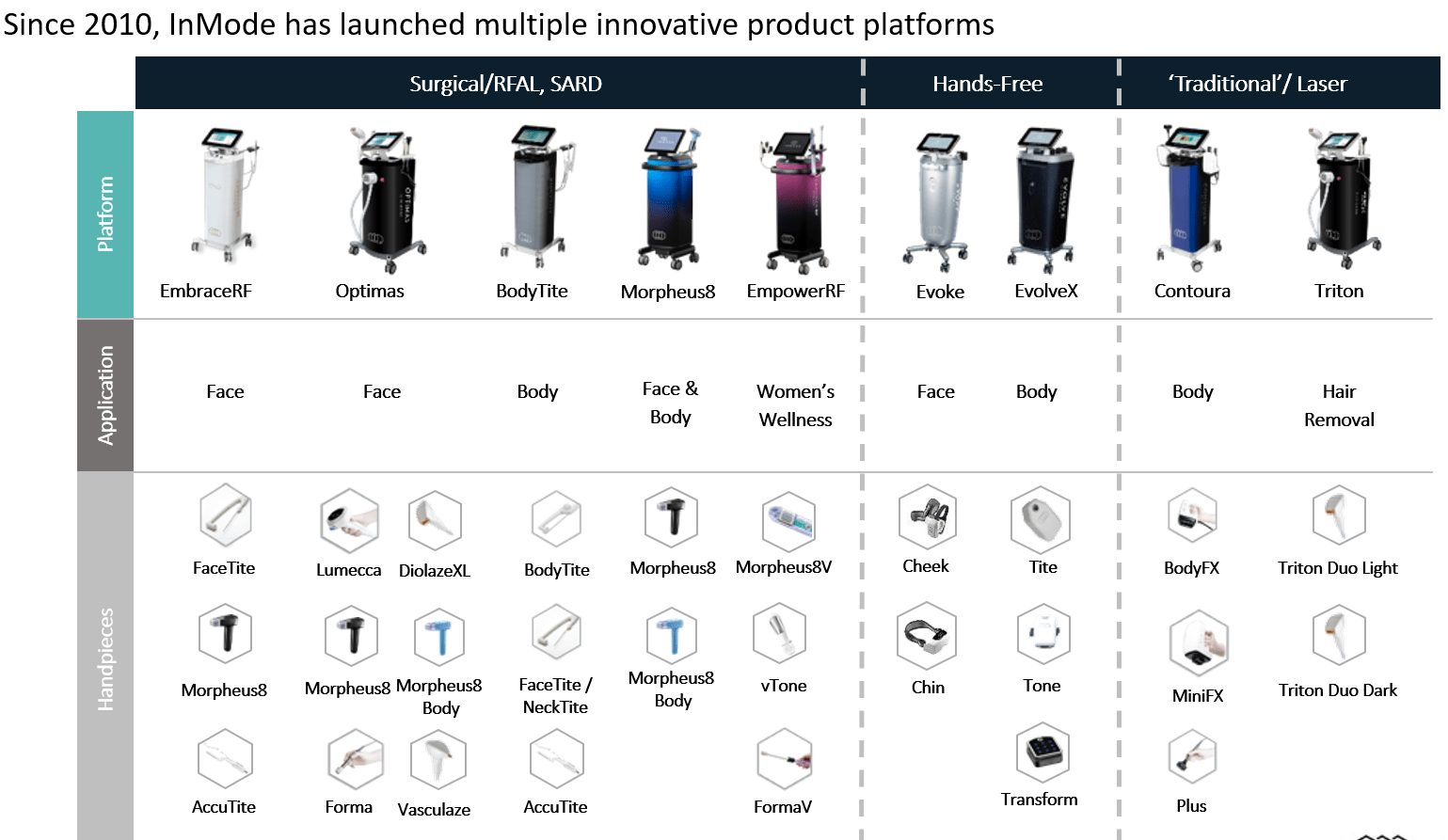

Product Range & Segments

{kind=link}

Some of these in-office procedures enabled by InMode include:

- Skin resurfacing

- Pigmentation

- Hair removal

- Wrinkle treatment

- Cellulite

- Face contouring

- Body contouring

- Skin contraction

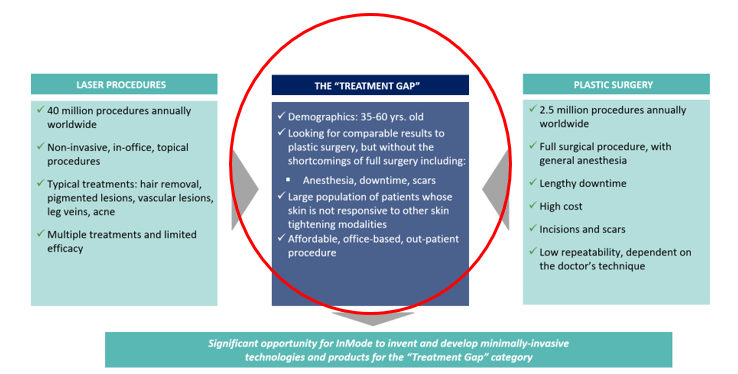

The "Treatment Gap" that INMD is Addressing

{kind=link}

Uniquely Positioned in the Industry

InMode essentially pioneered the field of minimally invasive treatments that stands between traditional invasive plastic surgery and arguably abortive non-invasive laser treatments. The biggest benefit of minimally invasive treatments is minimal downtime compared to surgery which would cause significant lifestyle disruptions. This highly lucrative niche was partially cleared from competition when the US regulators put the Women's Health market under the microscope in 2017 and forced a number of competitors out of the market. INMD's product quality helped it survive the crackdown and enjoy further growth in that market.

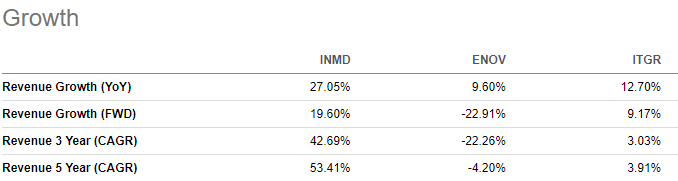

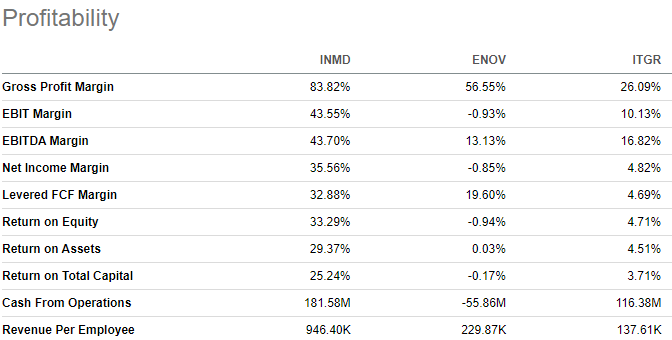

InMode's market leadership in the growing niche of minimally invasive treatments paints a positive picture on the financials. InMode has exemplary growth relative to peers.

Financials and Drivers

{kind=link}

{kind=link}

The biggest question for the prudent investor is: will a recession hamper growth? The answer to this question has to be contextualised by what is being priced in the market. Hence, I will answer this question in two parts: First, what are the growth drivers and how resilient will they be in a recession, and the second question will be answered in the valuation section where I analyse what is being priced in today's price.

Currently, the medical aesthetics market is ~$14B and it is projected to grow HSD-LDD through to 2030 according to research by Research&Markets . Over the past 10 years, there has been a pronounced shift in preference away from traditional invasive beauty treatments to non-invasive or minimally invasive treatments. These innovative approaches are appealing due to less scarring, reduced pain and lower recovery period. According to InMode's investor relations physicians' TAM is roughly 200k practices across the globe (including Aesthetic, plastic, and Gynecology surgeons) and for the time being, InMode has a relationship with 14k - 6.5k of them based in the US. For 2023, Management is guiding for ~15% growth, 83-85% gross margins, and non-GAAP EPS growth of 7% (with the slowdown in operating profitability being linked to ramping up product launches). I consider management's expectations conservative, as they have been since going public, and would expect the following three catalysts to drive higher growth:

- International growth in China

- Resilient demand in the Western world despite recession fears. Although demand for luxury aesthetic treatments may seem cyclical at first glance, in fact, it benefits from secular growth forces and the clientele undertaking treatments at Medical Spas (MedSpa for short) are, for the most part, affluent enough to continue doing them even in downturns. Google trends for "Medspa" have consistently trended higher over the past 5 years.

- Successful launch of new products including Evoke, Evolve and Envision.InMode has a decade-long track record of taking product platforms to market successfully (BodyTite, Optimas, Votiva, Contoura, Triton, EmbraceRF, EmpowerRF, Morepheus8 and EvolveX)

InMode has some of the best profit margins of any in the publically traded med-tech space. It features outstanding profitability on every level with unmatched capital efficiency and labour productivity (defined as revenue per employee). In recessionary times, capital-intensive business models suffer due to the following reasons:

- Cut down on investments that lead to product innovation and market leadership

- Margin erosion due to high fixed costs and

- Usually take on debt to endure the storm. InMode's capital-light business model (has exceptional cash flow generation and is a great candidate to weather any storm, especially considering its net cash position.

Looking forward, I expect profit margins to be maintained at current high levels as the product pipeline is filled with innovative products that have similar ground-breaking potential as the current product portfolio. InMode's product differentiation and brand name will be crucial for its profitability going forward. On the operating level, I expect some volatility considering the product launches and frankly, the company can afford to invest heavily, yet prudently, to successfully commercialise new technologies. However, gross margin is the key metric I will be looking to assess the level of pricing power going forward. The CEO made encouraging statements regarding gross margin at the Needham Conference last year.

From the drawing board, from the first day, when we start to develop the product, we think about the gross margins. And that's what we do. That's the philosophy and DNA of this company. As far as the cost of manufacturing is concerned, we have also been very productive - Moshe Mizrahy, CEO

{kind=link}

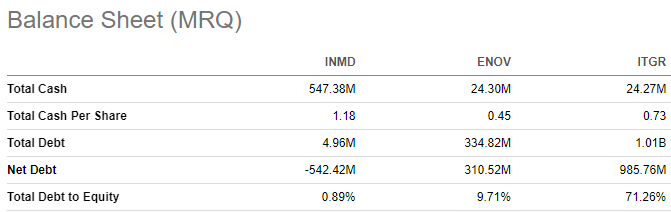

The company has ~$500mn in retained earnings, spends de minimis cash on Capex (<1% of sales), 3% of revenue on R&D and invests its cash in government bonds (for the most part). InMode's balance sheet is pristine. Minimal debt, and lots of cash. In fact, during recession times, you want to own businesses that reinvest in themselves to grow their product leadership through rigorous innovation while their competitors/peers struggle just to make ends meet with their expenses and are forced to stop chasing product leadership. Healthy companies come out stronger during crises and InMode is a great candidate to demonstrate this.

{kind=link}

We've established that InMode is flushed with cash. The next big question is what do they do with it. They have ~$500mn in dry powder and generates roughly $50mn a quarter. Management has spent ~$100mn in share repurchases over the past 3 years but in a recent Canaccord Genuity conference , comments favoured disciplined M&A. However, management clearly stated that they are not interested in buying companies in adjacencies that are commoditised but relevant (i.e. laser treatment etc.). It will likely be more oriented to plastic surgery, implant fillers, or complementary technology. From the conference speech, it sounded like an M&A deal announcement will almost certainly come in 2023.

Competitive advantages play an important role in protecting abnormal returns on capital. InMode has a first mover advantage as a pioneer in the minimally invasive space. The following quote is from INMD's 20-F highlighting the status, length and nature of their patents.

As of February 14, 2023, we own six issued U.S. patents and one issued Korean patent. As of February 14, 2023, we have filed eleven patent applications that are pending in the United States Patent and Trademark Office. Out of those applications, one was filed also under The Patent Cooperation Treaty and one in Europe. Our issued U.S. patents are projected to expire between 2027 and 2038 (assuming pending U.S. patent applications are approved). These patents and patent applications cover the technologies described herein, and contribute to the protection of sour rights to our proprietary technology. Our patents relate to radio frequency-based technology that may be used for minimally invasive aesthetic solutions, such as fat destruction, and fractional skin ablation relating to skin tightening and fat destruction, among others, and cover our existing products.

The above quote from the 20-F implies that the earliest date that competitors can begin to develop technologies rivalling INMD's is 2027. That gives the company a time window of 3-4 years of uninterrupted competitive environment to grow, strengthen its moat and come up with new product lines. In fact, it took 3 FDA approvals to commercialize InMode's Bodytite over 6 years of development, so one can expect a similar timeline for competitors. InMode's patent protection is bolstered by a degree of brand equity as it has executed very well in marketing using influencers/celebrities ( InMode's Celebrity Treatments ) to promote the admittedly excellent results through their treatments with results noticeable 2-3 weeks after the treatments ( Morpheus8 review: Are the results really equivalent to a facelift? ). Frankly, the results are remarkable. Besides, physicians tend to be sticky because the economics of INMD's products are highly lucrative for them. An average treatment would cost somewhere between ~$6-10k and if the practice carries out 5-6 treatments per month, the payback period for the machine is 5-7 months. INMD projects that ~70% of its business will be in the more protected area (MIS/surgical) than the 20% in the hands-free area and laser and non-invasive RF 8-10% of the business.

Valuation

Seeking Alpha

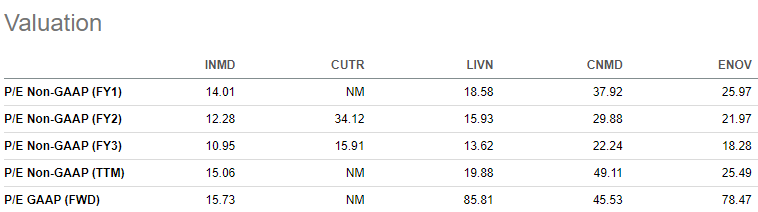

In a recession, I seek to find companies that generate substantial cash flow to fund operations and spare some for growth and safety and ideally have low levels of debt so they can retain the flexibility of leverage if need be. INMD meets all the above criteria and is trading at a significant discount to the sector. In my view, a company with such mouth-watering financials should be trading at par, at least, with the sector.

{kind=link}

in fact, trades on a relative discount to all its publicly traded peers on a forward-looking basis; despite having the best growth, cash generation and profitability metrics out of all. Assuming the company meets its conservative guidance of ~$238M EBIT, and it re-rates to multiples closer to the sector average, then we can expect >55% upside at ~20x EV/EBIT. My target price is ~$60. I believe management's guidance will prove conservative and the company will exceed long-term expectations which are currently anchored around industry growth of ~10%, which will also warrant a sustainably higher multiple.

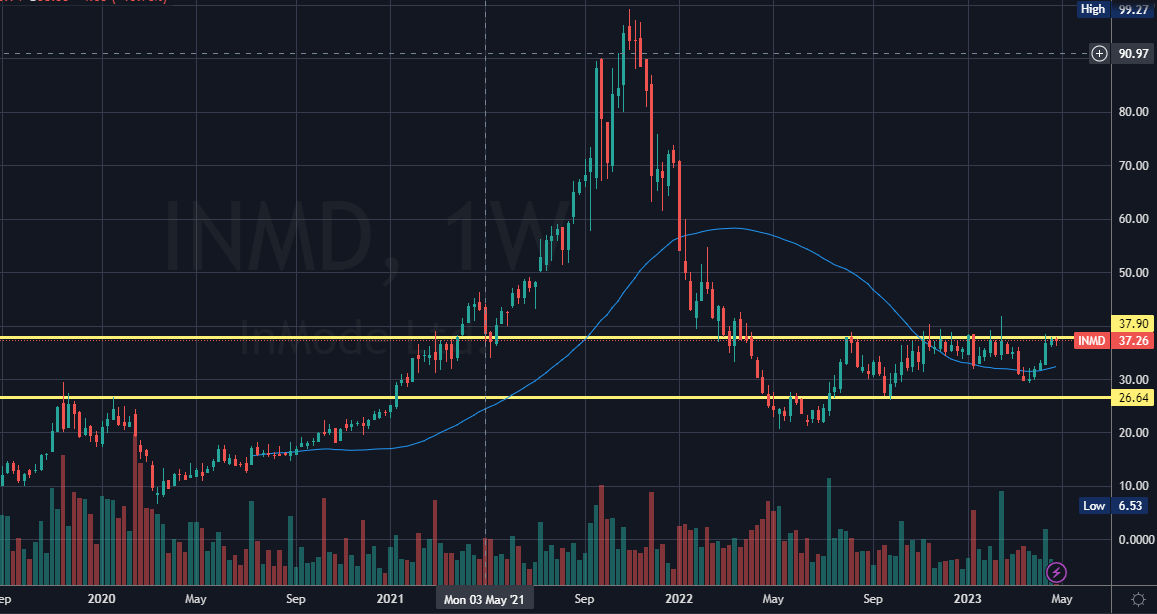

Technical Analysis

{kind=link}

The bulls have been knocking on the door for months now to break through the $30-40 range but the set-up is looking optimistic, especially considering that the company reported Q1 results and beat consensus estimates with positive commentary. Additionally, the company will prove its demand resilience even in a recessionary environment (if and when it comes) and investors will once again appreciate the company's unique positioning. The nearest support would be ~$30 and would expect negative swings in sentiment to find a price floor in that price area.

Risks

Elective aesthetic treatments are discretionary by nature and are paid out of pocket without insurance contributions (for the time being) which can cause swings in demand. I argue that the demand trends for treatments in medical spas are resilient and demand will hold up better than expected even in a recessionary environment.

Even though management owns ~14% of the company, it is important to mention that the company is still steered by the co-founders which may prove to be a double-edged sword. Founders sometimes get carried away and make unreasonable investment decisions that may lead to value-destructive outcomes with minimal pushback.

According to data on Seeking Alpha , INMD's 24M Beta is 1.76 which is quite high relative to its beers which range from 0.93 to 1.33. During turbulent market conditions, there can be violent swings in the share price.

Recent management statements lead me to believe that M&A is highly likely in 2023. M&A execution risk will tap into unchartered territory as it will be InMode's biggest acquisition. Just like any other M&A transaction, there are execution and integration risks involved, especially when they will be the company's first acquisition.

Conclusion

InMode has carved its own niche in an untapped market and is reaping the benefits by generating outstanding returns in a significantly lucrative and patent-protected market. I consider management's guidance to be conservative and the market's expectations tempered relative to the company's potential. The demand for InMode's products will, in my opinion, prove more resilient than the market is pricing in, even in a recessionary environment. If my projections come to fruition, I expect a >50% return with a target price of ~$60 at 19-20x FY23 EBIT.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

InMode: Undervalued Even Under Recessionary Conditions